Accounting for Decision Making and Control 8th Edition by Jerold Zimmerman

Edition 8ISBN: 978-0078025747Accounting for Decision Making and Control 8th Edition by Jerold Zimmerman

Edition 8ISBN: 978-0078025747 Exercise 19

Federal Mixing

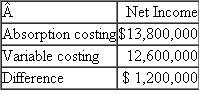

Federal Mixing (FM) is a division of Federal Chemicals, a large diversified chemical company. FM provides mixing services for both outside customers and other Federal divisions. FM buys or receives liquid chemicals and combines and packages them according to the customer's specifications. FM computes its divisional net income on both a fully absorbed and variable costing basis. For the year just ending, it reported

Overhead is assigned to products using machine hours.

Overhead is assigned to products using machine hours.

There is no finished goods inventory at FM, only work-in-process (WIP) inventory. As soon as a product is completed, it is shipped to the customer. The beginning inventory based on absorption costing was valued at $6.3 million and contained 70,000 machine hours. The ending WIP inventory based on absorption costing was valued at $9.9 million and contained 90,000 machine hours.

Required:

Write a short nontechnical note to senior management explaining why variable costing and absorption costing net income amounts differ.

Federal Mixing (FM) is a division of Federal Chemicals, a large diversified chemical company. FM provides mixing services for both outside customers and other Federal divisions. FM buys or receives liquid chemicals and combines and packages them according to the customer's specifications. FM computes its divisional net income on both a fully absorbed and variable costing basis. For the year just ending, it reported

Overhead is assigned to products using machine hours.There is no finished goods inventory at FM, only work-in-process (WIP) inventory. As soon as a product is completed, it is shipped to the customer. The beginning inventory based on absorption costing was valued at $6.3 million and contained 70,000 machine hours. The ending WIP inventory based on absorption costing was valued at $9.9 million and contained 90,000 machine hours.

Required:

Write a short nontechnical note to senior management explaining why variable costing and absorption costing net income amounts differ.

Explanation Verified

Verified

Overhead Costs:

These are the expenses ...

Accounting for Decision Making and Control 8th Edition by Jerold Zimmerman

Why don’t you like this exercise?

Other Minimum 8 character and maximum 255 character

Character 255