McGraw-Hill's Taxation of Business Entities 3rd Edition by Connie Weaver, Brian Spilker, Edmund Outslay, John Robinson, Ronald Worsham, Benjamin Ayers, John Barrick

Edition 3ISBN: 9780077924522McGraw-Hill's Taxation of Business Entities 3rd Edition by Connie Weaver, Brian Spilker, Edmund Outslay, John Robinson, Ronald Worsham, Benjamin Ayers, John Barrick

Edition 3ISBN: 9780077924522 Exercise 55

LeBron, Dennis, and Susan formed the Bar T LLC at the beginning of the current year. LeBron and Dennis each contributed $200,000 and Susan transferred several acres of agricultural land she had purchased two years earlier to the LLC. The land had a tax basis of $50,000 and was appraised at $300,000. The land was also encumbered with a $100,000 nonrecourse mortgage (i.e., qualified nonrecourse financing) for which no one was personally liable. The members plan to use the land and cash to begin a cattle-feeding operation. Susan will work full-time operating the business, but LeBron and Dennis will devote less than two days per year to the operation. All three members agree to split profits and losses equally. At the end of the first year, Bar T had accumulated $40,000 of accounts payable jointly guaranteed by LeBron and Dennis and had made a $9,000 principal payment on the mortgage. None of the members have passive income from other sources.

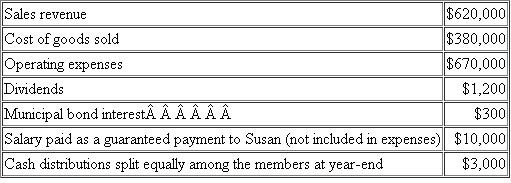

For the first year of operations, the partnership records disclosed the following information:

a. Compute the adjusted basis of each member's interest immediately after the formation of the LLC.

a. Compute the adjusted basis of each member's interest immediately after the formation of the LLC.

b. When does each member's holding period for his or her LLC interests begin

c. What is Bar T's tax basis and holding period in its land

d. What is Bar T's required tax year-end

e. What overall methods of accounting are available to Bar T

f. List the separate items of partnership income, gains, losses, deductions and other items that will be included in each member's Schedule K-1 for the first year of operations. Use the proposed self-employment tax regulations to determine each member's self-employment income or loss.

g. What are the members' adjusted bases in their LLC interests at the end of the first year of operations

h. What are the members' at-risk amounts in their LLC interests at the end of the first year of operations

i. How much loss from Bar T, if any, will the members be able to deduct on their individual returns from the first year of operations .

For the first year of operations, the partnership records disclosed the following information:

a. Compute the adjusted basis of each member's interest immediately after the formation of the LLC. b. When does each member's holding period for his or her LLC interests begin

c. What is Bar T's tax basis and holding period in its land

d. What is Bar T's required tax year-end

e. What overall methods of accounting are available to Bar T

f. List the separate items of partnership income, gains, losses, deductions and other items that will be included in each member's Schedule K-1 for the first year of operations. Use the proposed self-employment tax regulations to determine each member's self-employment income or loss.

g. What are the members' adjusted bases in their LLC interests at the end of the first year of operations

h. What are the members' at-risk amounts in their LLC interests at the end of the first year of operations

i. How much loss from Bar T, if any, will the members be able to deduct on their individual returns from the first year of operations .

Explanation Verified

Verified

a. LeBron's adjusted basis is $216...

McGraw-Hill's Taxation of Business Entities 3rd Edition by Connie Weaver, Brian Spilker, Edmund Outslay, John Robinson, Ronald Worsham, Benjamin Ayers, John Barrick

Why don’t you like this exercise?

Other Minimum 8 character and maximum 255 character

Character 255