McGraw-Hill's Taxation of Business Entities 3rd Edition by Connie Weaver, Brian Spilker, Edmund Outslay, John Robinson, Ronald Worsham, Benjamin Ayers, John Barrick

Edition 3ISBN: 9780077924522McGraw-Hill's Taxation of Business Entities 3rd Edition by Connie Weaver, Brian Spilker, Edmund Outslay, John Robinson, Ronald Worsham, Benjamin Ayers, John Barrick

Edition 3ISBN: 9780077924522 Exercise 25

Abigail, Bobby, and Claudia are equal owners in Lafter, an S corporation that was a C corporation several years ago. While Abigail and Bobby actively participate in running the company, Claudia has a separate day job and is a passive owner. Consider the following information for 2011:

• As of January 1, 2011, Abigail, Bobby, and Claudia each have a basis in Lafter stock of $15,000 and a debt basis of $0. On January 1, the stock basis is also the at-risk amount for each shareholder.

• Bobby and Claudia also are passive owners in Aggressive LLC, which allocated business income of $14,000 to each of them in 2011. Neither has any other source of passive income (besides Lafter, for Claudia).

• On March 31, 2011, Abigail lends $5,000 of her own money to Lafter.

• Anticipating the need for basis to deduct a loss, on April 4, 2011, Bobby takes out a loan using his car as collateral-he wants to limit his losses to the value of the automobile just in case he can't pay back the loan-to make a contribution of $10,000 to Lafter.

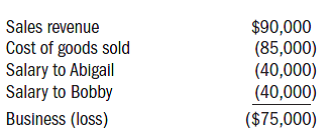

• Lafter has an accumulated adjustments account balance of $45,000 as of January 1, 2011.• Lafter has C corporation earnings and profits of $15,000 as of January 1, 2011.• During 2011, Lafter reports a business loss of $75,000, computed as follows:

• Lafter also reported $12,000 of tax-exempt interest income.

a. What amount of Lafter's 2011 business loss of $75,000 tax loss are Abigail, Bobby, and Claudia allowed to deduct on their individual tax returns What are each owner's stock basis and debt basis (if applicable) and each owner's at-risk amount with respect to the investment in Lafter at the end of 2011

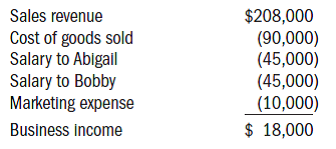

• During 2012, Lafter made several changes to its business approach and reported $18,000 of business income, computed as follows:

• Lafter also reported a long-term capital gain of $24,000 in 2012.• Lafter made a cash distribution on July 1, 2012, of $20,000 to each shareholder.

b. What amount of gain/income does each shareholder recognize from the cash distribution on July 1, 2012

• As of January 1, 2011, Abigail, Bobby, and Claudia each have a basis in Lafter stock of $15,000 and a debt basis of $0. On January 1, the stock basis is also the at-risk amount for each shareholder.

• Bobby and Claudia also are passive owners in Aggressive LLC, which allocated business income of $14,000 to each of them in 2011. Neither has any other source of passive income (besides Lafter, for Claudia).

• On March 31, 2011, Abigail lends $5,000 of her own money to Lafter.

• Anticipating the need for basis to deduct a loss, on April 4, 2011, Bobby takes out a loan using his car as collateral-he wants to limit his losses to the value of the automobile just in case he can't pay back the loan-to make a contribution of $10,000 to Lafter.

• Lafter has an accumulated adjustments account balance of $45,000 as of January 1, 2011.• Lafter has C corporation earnings and profits of $15,000 as of January 1, 2011.• During 2011, Lafter reports a business loss of $75,000, computed as follows:

• Lafter also reported $12,000 of tax-exempt interest income.

a. What amount of Lafter's 2011 business loss of $75,000 tax loss are Abigail, Bobby, and Claudia allowed to deduct on their individual tax returns What are each owner's stock basis and debt basis (if applicable) and each owner's at-risk amount with respect to the investment in Lafter at the end of 2011

• During 2012, Lafter made several changes to its business approach and reported $18,000 of business income, computed as follows:

• Lafter also reported a long-term capital gain of $24,000 in 2012.• Lafter made a cash distribution on July 1, 2012, of $20,000 to each shareholder.

b. What amount of gain/income does each shareholder recognize from the cash distribution on July 1, 2012

Explanation Verified

Verified

What amount of Lafter's 2011 business lo...

McGraw-Hill's Taxation of Business Entities 3rd Edition by Connie Weaver, Brian Spilker, Edmund Outslay, John Robinson, Ronald Worsham, Benjamin Ayers, John Barrick

Why don’t you like this exercise?

Other Minimum 8 character and maximum 255 character

Character 255