Business Mathematics Brief 12th Edition by Stanley Salzman ,Gary Clendenen, Charles Miller

Edition 12ISBN: 978-0132605540Business Mathematics Brief 12th Edition by Stanley Salzman ,Gary Clendenen, Charles Miller

Edition 12ISBN: 978-0132605540 Exercise 143

Compare level premium term insurance to universal life insurance. Which would you prefer for yourself? Why?

Term insurance. Term insurance is the lowest-cost type of life insurance. It provides the most insurance per dollar spent, but it does not build up any cash values for retirement. This type of insurance coverage is usually renewable until some age, such as 70, when the insured is no longer allowed to renew it. As a result, most people discontinue term insurance before they die. Still, term insurance is a low-cost way to provide protection against an early death.

Individuals can buy a level-premium term policy in which the premium remains constant for a period of time, such as 10 years or 20 years. Thereafter, premiums increase rapidly.

Quick TIP

Mortgage insurance is usually much more expensive than a regular term insurance policy. Compare prices before you buy.

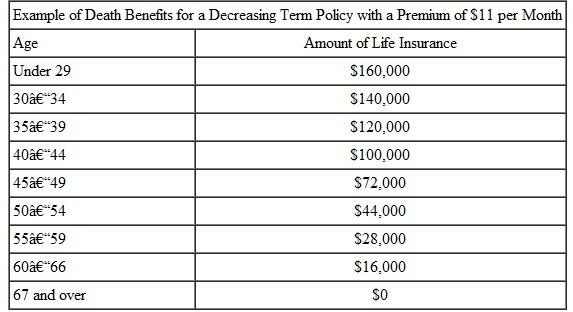

Decreasing term insurance. This is a type of term insurance with fixed premiums commonly to age 60 or 65, but the amount of life insurance decreases periodically. An example of this is a mortgage insurance policy on a home. The amount of life insurance on the owner decreases as the amount owed to the mortgage company decreases. Many large companies provide decreasing term insurance to employees as a benefit. The table provides an example of the benefits of one particular decreasing term policy.

Whole life (also called straight life, ordinary life , or permanent ). This type of insurance provides a death benefit and a savings plan. The insured commonly pays a constant premium until death or retirement, whichever occurs first. If the policy is in force at the time of death, a death benefit is paid. Alternatively, the insured may choose to convert the accumulated cash value to a retirement benefit.

Whole life (also called straight life, ordinary life , or permanent ). This type of insurance provides a death benefit and a savings plan. The insured commonly pays a constant premium until death or retirement, whichever occurs first. If the policy is in force at the time of death, a death benefit is paid. Alternatively, the insured may choose to convert the accumulated cash value to a retirement benefit.

Universal life. This type of insurance provides the life insurance protection of term insurance plus a tax-deferred way to accumulate assets. It sometimes allows people to establish a permanent policy at a lower premium than they would have to pay under a whole life policy, and it gives the insured more flexibility. For example, universal life can help a family obtain more insurance when young children are at home and then help accumulate savings later after the children are grown.

Different investment options may be available for the portion of the premium going into retirement benefits, but the options are often limited.

Variable life. This type of insurance allows the policyholder to make choices among several investment options. It places the investment risk on the policyholder by allowing the insured to invest in any of the following: money market funds, bond funds, stock funds, or a combination of the three.

Quick TIP

Limited-payment and endowment policies cost more, but they accumulate more money for use later in life.

Limited-payment life insurance. Limited-payment life is similar to whole life insurance, except that premiums are paid for only a fixed number of years, such as 20. This type of insurance is thus often called 20-pay life, representing payments for 20 years. The premium for limited-payment life is higher than that for whole life policies. Limited-payment life is most appropriate for athletes, actors, and others whose income is likely to be high for several years and then decline.

Endowment policies are the most expensive type of policy since they accumulate cash more rapidly than the other types of life insurance. These policies guarantee payment of a fixed amount of money to a given individual, whether or not the insured lives. Endowment policies might be taken out by parents to guarantee a sum of money for their children's college education. Because of the high premiums, this is one of the least popular types of policies today.

Term insurance. Term insurance is the lowest-cost type of life insurance. It provides the most insurance per dollar spent, but it does not build up any cash values for retirement. This type of insurance coverage is usually renewable until some age, such as 70, when the insured is no longer allowed to renew it. As a result, most people discontinue term insurance before they die. Still, term insurance is a low-cost way to provide protection against an early death.

Individuals can buy a level-premium term policy in which the premium remains constant for a period of time, such as 10 years or 20 years. Thereafter, premiums increase rapidly.

Quick TIP

Mortgage insurance is usually much more expensive than a regular term insurance policy. Compare prices before you buy.

Decreasing term insurance. This is a type of term insurance with fixed premiums commonly to age 60 or 65, but the amount of life insurance decreases periodically. An example of this is a mortgage insurance policy on a home. The amount of life insurance on the owner decreases as the amount owed to the mortgage company decreases. Many large companies provide decreasing term insurance to employees as a benefit. The table provides an example of the benefits of one particular decreasing term policy.

Whole life (also called straight life, ordinary life , or permanent ). This type of insurance provides a death benefit and a savings plan. The insured commonly pays a constant premium until death or retirement, whichever occurs first. If the policy is in force at the time of death, a death benefit is paid. Alternatively, the insured may choose to convert the accumulated cash value to a retirement benefit.Universal life. This type of insurance provides the life insurance protection of term insurance plus a tax-deferred way to accumulate assets. It sometimes allows people to establish a permanent policy at a lower premium than they would have to pay under a whole life policy, and it gives the insured more flexibility. For example, universal life can help a family obtain more insurance when young children are at home and then help accumulate savings later after the children are grown.

Different investment options may be available for the portion of the premium going into retirement benefits, but the options are often limited.

Variable life. This type of insurance allows the policyholder to make choices among several investment options. It places the investment risk on the policyholder by allowing the insured to invest in any of the following: money market funds, bond funds, stock funds, or a combination of the three.

Quick TIP

Limited-payment and endowment policies cost more, but they accumulate more money for use later in life.

Limited-payment life insurance. Limited-payment life is similar to whole life insurance, except that premiums are paid for only a fixed number of years, such as 20. This type of insurance is thus often called 20-pay life, representing payments for 20 years. The premium for limited-payment life is higher than that for whole life policies. Limited-payment life is most appropriate for athletes, actors, and others whose income is likely to be high for several years and then decline.

Endowment policies are the most expensive type of policy since they accumulate cash more rapidly than the other types of life insurance. These policies guarantee payment of a fixed amount of money to a given individual, whether or not the insured lives. Endowment policies might be taken out by parents to guarantee a sum of money for their children's college education. Because of the high premiums, this is one of the least popular types of policies today.

Explanation Verified

Verified

Term insurance is a life insurance of th...

Business Mathematics Brief 12th Edition by Stanley Salzman ,Gary Clendenen, Charles Miller

Why don’t you like this exercise?

Other Minimum 8 character and maximum 255 character

Character 255