Accounting Information Systems 8th Edition by James Hall

Edition 8ISBN: 978-1111972141Accounting Information Systems 8th Edition by James Hall

Edition 8ISBN: 978-1111972141 Exercise 64

FIXED ASSET SYSTEM

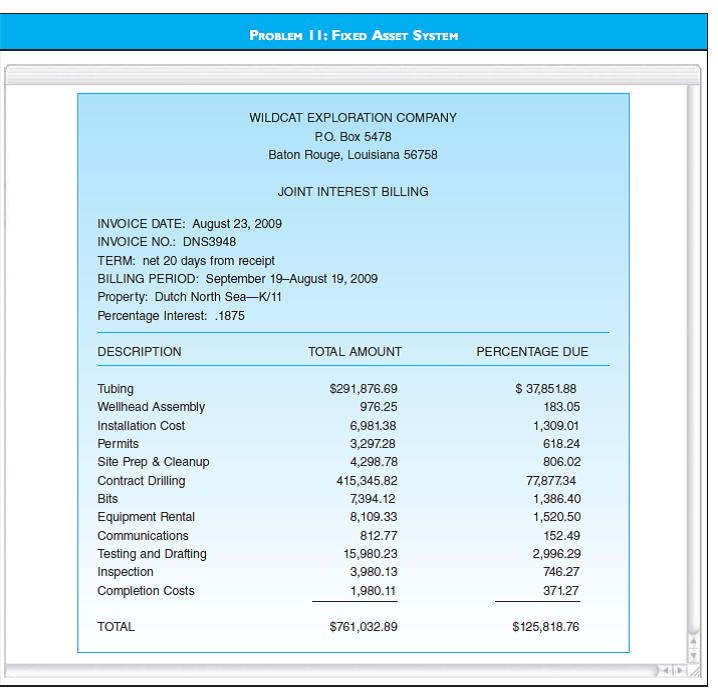

The treatment of fixed asset accounting also includes accounting for mineral reserves, such as oil and gas, coal, gold, diamonds, and silver. These costs must be capitalized and depleted over the estimated useful life of the asset. The depletion method used is the units of production method. An example of a source document for an oil and gas exploration firm is presented in the figure for Problem 11. The time to drill a well from start to completion may vary from 3 to 18 months, depending on the location. Further, the costs to drill two or more wells may be difficult to separate. For example, the second well may be easier to drill because more is known about the conditions of the field or reservoir, and the second well may be drilled to help extract the same reserves more quickly or efficiently.

Solving this problem may require additional research beyond the readings in the chapter.

Required

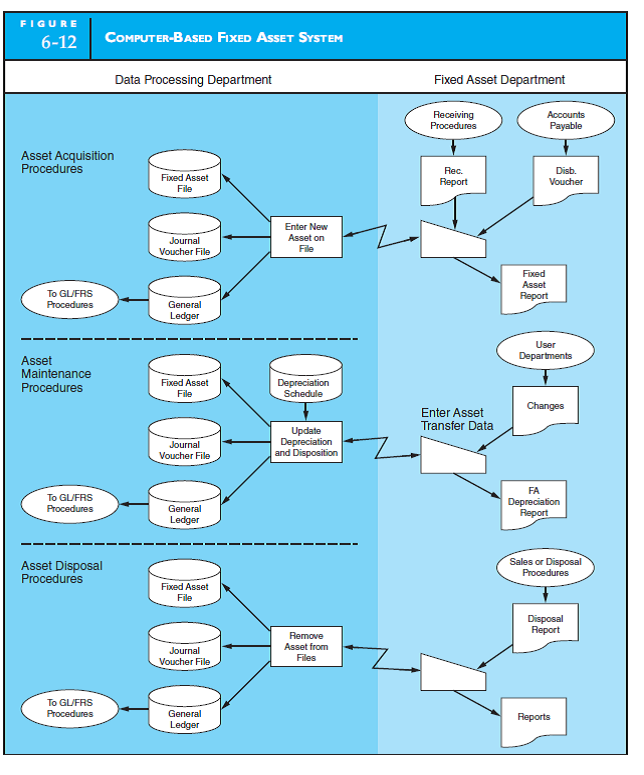

a. In Figure 6-10, the source documents for the fixed asset accounting system come from the receiving department and the accounts payable department. For an oil and gas firm, from where would you expect the source documents to come?

b. Assume that a second well is drilled to help extract the reserves from the field. How would you allocate the drilling costs?

c. The number of reserves to be extracted is an estimate. These estimates are constantly being revised. How does this affect the fixed asset department's job? In what way, if at all, does Figure 6-12 need to be altered to reflect these adjustments?

d. How does the auditor verify the numbers that the fixed asset department calculates at the end of the period?

Figure:

The treatment of fixed asset accounting also includes accounting for mineral reserves, such as oil and gas, coal, gold, diamonds, and silver. These costs must be capitalized and depleted over the estimated useful life of the asset. The depletion method used is the units of production method. An example of a source document for an oil and gas exploration firm is presented in the figure for Problem 11. The time to drill a well from start to completion may vary from 3 to 18 months, depending on the location. Further, the costs to drill two or more wells may be difficult to separate. For example, the second well may be easier to drill because more is known about the conditions of the field or reservoir, and the second well may be drilled to help extract the same reserves more quickly or efficiently.

Solving this problem may require additional research beyond the readings in the chapter.

Required

a. In Figure 6-10, the source documents for the fixed asset accounting system come from the receiving department and the accounts payable department. For an oil and gas firm, from where would you expect the source documents to come?

b. Assume that a second well is drilled to help extract the reserves from the field. How would you allocate the drilling costs?

c. The number of reserves to be extracted is an estimate. These estimates are constantly being revised. How does this affect the fixed asset department's job? In what way, if at all, does Figure 6-12 need to be altered to reflect these adjustments?

d. How does the auditor verify the numbers that the fixed asset department calculates at the end of the period?

Figure:

Explanation Verified

Verified

Fixed Asset System

Consider the case of...

Accounting Information Systems 8th Edition by James Hall

Why don’t you like this exercise?

Other Minimum 8 character and maximum 255 character

Character 255