Fundamentals of Advanced Accounting 5th Edition by Joe Ben Hoyle,Thomas Schaefer,Timothy Doupnik

Edition 5ISBN: 978-1260575910Fundamentals of Advanced Accounting 5th Edition by Joe Ben Hoyle,Thomas Schaefer,Timothy Doupnik

Edition 5ISBN: 978-1260575910 Exercise 58

On March 1, 2013, Nu-Auto Corporation announced its plan to acquire 90 percent of the outstanding 1,000,000 shares of Battery Tech Corporation's common stock in a business combination later in the year following regulatory approval. Nu-Auto will account for the transaction in accordance with ASC 805, Business Combinations.

On October 1, 2013, Nu-Auto acquired the 90 percent controlling interest in Battery Tech. On this date, Nu-Auto paid $60 million in cash and issued 1 million shares of Nu-Auto common stock to the selling shareholders of Battery Tech. Nu-Auto's share price was $20 on the announcement date and $27 on the acquisition date. Battery Tech's remaining 100,000 shares of common stock traded in the $108 to $112 per share range in the weeks before and after October 1, 2013.

The parties agreed that Nu-Auto would issue to the selling shareholders an additional 1 million shares contingent upon the achievement of certain performance goals during the first 18 months following the acquisition. The acquisition-date fair value of the contingent stock issue was estimated at $10 million.

Battery Tech has a research and development (R D) project underway to develop a proprietary fast-charging battery technology. The technology has a fair value of $14 million. Nu-Auto considers this R D as in-process because it has not yet reached technological feasibility and additional R D is needed to bring the project to completion. No assets have been recorded in Battery Tech's financial records for the research and development costs related to its fast-charging battery technology.

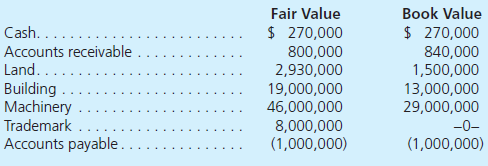

Battery Tech's other assets and liabilities include the following:

Neither the receivables nor payables involve Nu-Auto.

Answer the following questions citing relevant support from the ASC and IFRS.

What is the acquisition-date value assigned to the 10 percent noncontrolling interest What are the potential noncontrolling interest valuation alternatives available under IFRS

On October 1, 2013, Nu-Auto acquired the 90 percent controlling interest in Battery Tech. On this date, Nu-Auto paid $60 million in cash and issued 1 million shares of Nu-Auto common stock to the selling shareholders of Battery Tech. Nu-Auto's share price was $20 on the announcement date and $27 on the acquisition date. Battery Tech's remaining 100,000 shares of common stock traded in the $108 to $112 per share range in the weeks before and after October 1, 2013.

The parties agreed that Nu-Auto would issue to the selling shareholders an additional 1 million shares contingent upon the achievement of certain performance goals during the first 18 months following the acquisition. The acquisition-date fair value of the contingent stock issue was estimated at $10 million.

Battery Tech has a research and development (R D) project underway to develop a proprietary fast-charging battery technology. The technology has a fair value of $14 million. Nu-Auto considers this R D as in-process because it has not yet reached technological feasibility and additional R D is needed to bring the project to completion. No assets have been recorded in Battery Tech's financial records for the research and development costs related to its fast-charging battery technology.

Battery Tech's other assets and liabilities include the following:

Neither the receivables nor payables involve Nu-Auto.

Answer the following questions citing relevant support from the ASC and IFRS.

What is the acquisition-date value assigned to the 10 percent noncontrolling interest What are the potential noncontrolling interest valuation alternatives available under IFRS

Explanation Verified

Verified

Under U.S. GAAP, the acquisition-date no...

Fundamentals of Advanced Accounting 5th Edition by Joe Ben Hoyle,Thomas Schaefer,Timothy Doupnik

Why don’t you like this exercise?

Other Minimum 8 character and maximum 255 character

Character 255