Fundamentals of Advanced Accounting 5th Edition by Joe Ben Hoyle,Thomas Schaefer,Timothy Doupnik

Edition 5ISBN: 978-1260575910Fundamentals of Advanced Accounting 5th Edition by Joe Ben Hoyle,Thomas Schaefer,Timothy Doupnik

Edition 5ISBN: 978-1260575910 Exercise 37

Boswell and Johnson form a partnership on May 1, 2011. Boswell contributes cash of $50,000; Johnson conveys title to the following properties to the partnership:

The partners agree to start their partnership with equal capital balances. No goodwill is to be recognized.

According to the articles of partnership written by the partners, profits and losses are allocated based on the following formula:

• Boswell receives a compensation allowance of $1,000 per month.

• All remaining profits and losses are split 60:40 to Johnson and Boswell, respectively.

• Each partner can make annual cash drawings of $5,000 beginning in 2012.

Net income of $11,000 is earned by the business during 2011.

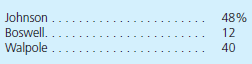

Walpole is invited to join the partnership on January 1, 2012. Because of her business reputation and financial expertise, she is given a 40 percent interest for $54,000 cash. The bonus approach is used to record this investment, made directly to the business. The articles of partnership are amended to give Walpole a $2,000 compensation allowance per month and an annual cash drawing of $10,000. Remaining profits are now allocated:

All drawings are taken by the partners during 2012. At year-end, the partnership reports an earned net income of $28,000.

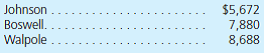

On January 1, 2013, Pope (previously a partnership employee) is admitted into the partnership. Each partner transfers 10 percent to Pope, who makes the following payments directly to the partners:

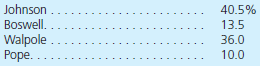

Once again, the articles of partnership must be amended to allow for the entrance of the new partner. This change entitles Pope to a compensation allowance of $800 per month and an annual drawing of $4,000. Profits and losses are now assigned as follows:

For the year of 2013, the partnership earned a profit of $46,000, and each partner withdrew the allowed amount of cash.

Determine the capital balances for the individual partners as of the end of each year: 2011 through 2013.

The partners agree to start their partnership with equal capital balances. No goodwill is to be recognized.

According to the articles of partnership written by the partners, profits and losses are allocated based on the following formula:

• Boswell receives a compensation allowance of $1,000 per month.

• All remaining profits and losses are split 60:40 to Johnson and Boswell, respectively.

• Each partner can make annual cash drawings of $5,000 beginning in 2012.

Net income of $11,000 is earned by the business during 2011.

Walpole is invited to join the partnership on January 1, 2012. Because of her business reputation and financial expertise, she is given a 40 percent interest for $54,000 cash. The bonus approach is used to record this investment, made directly to the business. The articles of partnership are amended to give Walpole a $2,000 compensation allowance per month and an annual cash drawing of $10,000. Remaining profits are now allocated:

All drawings are taken by the partners during 2012. At year-end, the partnership reports an earned net income of $28,000.

On January 1, 2013, Pope (previously a partnership employee) is admitted into the partnership. Each partner transfers 10 percent to Pope, who makes the following payments directly to the partners:

Once again, the articles of partnership must be amended to allow for the entrance of the new partner. This change entitles Pope to a compensation allowance of $800 per month and an annual drawing of $4,000. Profits and losses are now assigned as follows:

For the year of 2013, the partnership earned a profit of $46,000, and each partner withdrew the allowed amount of cash.

Determine the capital balances for the individual partners as of the end of each year: 2011 through 2013.

Explanation Verified

Verified

Fundamentals of Advanced Accounting 5th Edition by Joe Ben Hoyle,Thomas Schaefer,Timothy Doupnik

Why don’t you like this exercise?

Other Minimum 8 character and maximum 255 character

Character 255