Cornerstones of Managerial Accounting 6th Edition by Maryanne Mowen,Don Hansen ,Dan Heitger

Edition 6ISBN: 978-1305103962Cornerstones of Managerial Accounting 6th Edition by Maryanne Mowen,Don Hansen ,Dan Heitger

Edition 6ISBN: 978-1305103962 Exercise 39

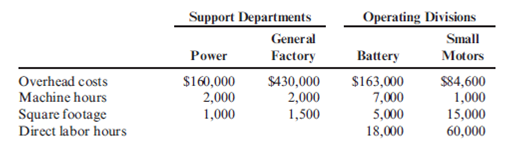

( Appendix 5B ) Direct Method of Support Department Cost Allocation

Stevenson Company is divided into two operating divisions: Battery and Small Motors. The company allocates power and general factory costs to each operating division using the direct method. Power costs are allocated on the basis of the number of machine hours and general factory costs on the basis of square footage. Support department cost allocations using the direct method are based on the following data:

Required:

1. Calculate the allocation ratios for Power and General Factory. ( Note : Carry these calculations out to four decimal places.)

2. Allocate the support service costs to the operating divisions. ( Note : Round all amounts to the nearest dollar.)

3. Assume divisional overhead rates are based on direct labor hours. Calculate the overhead rate for the Battery Division and for the Small Motors Division. ( Note : Round overhead rates to the nearest cent.)

Stevenson Company is divided into two operating divisions: Battery and Small Motors. The company allocates power and general factory costs to each operating division using the direct method. Power costs are allocated on the basis of the number of machine hours and general factory costs on the basis of square footage. Support department cost allocations using the direct method are based on the following data:

Required:

1. Calculate the allocation ratios for Power and General Factory. ( Note : Carry these calculations out to four decimal places.)

2. Allocate the support service costs to the operating divisions. ( Note : Round all amounts to the nearest dollar.)

3. Assume divisional overhead rates are based on direct labor hours. Calculate the overhead rate for the Battery Division and for the Small Motors Division. ( Note : Round overhead rates to the nearest cent.)

Explanation Verified

Verified

1.

Calculate allocation ratios for powe...

Cornerstones of Managerial Accounting 6th Edition by Maryanne Mowen,Don Hansen ,Dan Heitger

Why don’t you like this exercise?

Other Minimum 8 character and maximum 255 character

Character 255