Accounting 26th Edition by Carl Warren ,Jim Reeve ,Jonathan Duchac

Edition 26ISBN: 978-1337498159Accounting 26th Edition by Carl Warren ,Jim Reeve ,Jonathan Duchac

Edition 26ISBN: 978-1337498159 Exercise 42

Variance interpretation

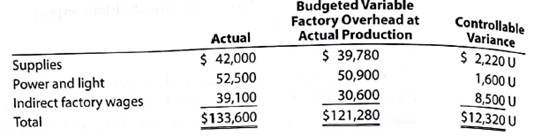

Vanadium Audio Inc. is a small manufacturer of electronic musical instruments. The plant manager received the following variable factory overhead report for the period:

Actual units produced: 15,000 (90% or practical capacity)

The plant manager is not pleased with the $12,320 unfavorable variable factory overhead controllable variance and has come to discuss the matter with the controller. The following discussion occurred:

Plant Manager: I just received this factory report for the latest month of operation. I'm not very pleased with these figures. Before these numbers go to headquarters, you and I will need to reach an understanding.

Controller: Go ahead, what's the problem

Plant Manager: What's the problem Well, everything. Look at the variance. If's too large. If I understand the accounting approach being used here, you are assuming that my costs are variable to the units produced. Thus as the production volume declines, so should these costs. Well, I don't believe that these costs are variable at all. I think they are fixed costs. As a result, when we operate below capacity, the costs really don't go down at all. I'm being penalized for costs I have no control over at all. I need this report to be redone to reflect this fact. If anything, the difference between actual and budget is essentially a volume variance. Listen, I know that you're a team player. You really need to reconsider your assumptions on this one.

If you were in the controller's position, how would you respond to the plant manager

Vanadium Audio Inc. is a small manufacturer of electronic musical instruments. The plant manager received the following variable factory overhead report for the period:

Actual units produced: 15,000 (90% or practical capacity)

The plant manager is not pleased with the $12,320 unfavorable variable factory overhead controllable variance and has come to discuss the matter with the controller. The following discussion occurred:

Plant Manager: I just received this factory report for the latest month of operation. I'm not very pleased with these figures. Before these numbers go to headquarters, you and I will need to reach an understanding.

Controller: Go ahead, what's the problem

Plant Manager: What's the problem Well, everything. Look at the variance. If's too large. If I understand the accounting approach being used here, you are assuming that my costs are variable to the units produced. Thus as the production volume declines, so should these costs. Well, I don't believe that these costs are variable at all. I think they are fixed costs. As a result, when we operate below capacity, the costs really don't go down at all. I'm being penalized for costs I have no control over at all. I need this report to be redone to reflect this fact. If anything, the difference between actual and budget is essentially a volume variance. Listen, I know that you're a team player. You really need to reconsider your assumptions on this one.

If you were in the controller's position, how would you respond to the plant manager

Explanation Verified

Verified

Analysis:

The plant manager received $ ...

Accounting 26th Edition by Carl Warren ,Jim Reeve ,Jonathan Duchac

Why don’t you like this exercise?

Other Minimum 8 character and maximum 255 character

Character 255