Essentials of Economics 7th Edition by Gregory Mankiw

Edition 7ISBN: 978-1285165950Essentials of Economics 7th Edition by Gregory Mankiw

Edition 7ISBN: 978-1285165950 Exercise 25

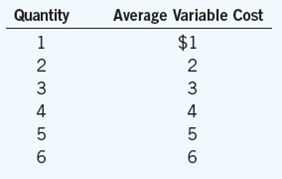

An industry currently has 100 firms, each of which has fixed costs of $16 and average variable costs as follows:

a. Compute a firm's marginal cost and average total cost for each quantity from 1 to 6.

b. The equilibrium price is currently $10. How much does each firm produce? What is the total quantity supplied in the market?

c. In the long run, firms can enter and exit the market, and all entrants have the same costs as above. As this market makes the transition to its long-run equilibrium, will the price rise or fall? Will the quantity demanded rise or fall? Will the quantity supplied by each firm rise or fall? Explain your answers.

d. Graph the long-run supply curve for this market, with specific numbers on the axes as relevant.

a. Compute a firm's marginal cost and average total cost for each quantity from 1 to 6.

b. The equilibrium price is currently $10. How much does each firm produce? What is the total quantity supplied in the market?

c. In the long run, firms can enter and exit the market, and all entrants have the same costs as above. As this market makes the transition to its long-run equilibrium, will the price rise or fall? Will the quantity demanded rise or fall? Will the quantity supplied by each firm rise or fall? Explain your answers.

d. Graph the long-run supply curve for this market, with specific numbers on the axes as relevant.

Explanation Verified

Verified

a.

Total cost:

Total cost can be calcu...

Essentials of Economics 7th Edition by Gregory Mankiw

Why don’t you like this exercise?

Other Minimum 8 character and maximum 255 character

Character 255