Cornerstones of Cost Management 2nd Edition by Don Hansen ,Maryanne Mowen

Edition 2ISBN: 978-1111824402Cornerstones of Cost Management 2nd Edition by Don Hansen ,Maryanne Mowen

Edition 2ISBN: 978-1111824402 Exercise 63

Environmental Responsibility Accounting, Cost Trends

At the beginning of 2010, Heber Company, an international telecommunications company, embarked on an environmental improvement program. The company set a goal to have all its facilities ISO 14001 registered by 2013. (There are 60 facilities worldwide.) To communicate the environmental progress made, management decided to issue, on a voluntary basis, an annual environmental progress report. Internally, the Accounting Department issued monthly progress reports and developed a number of measures that could be reported even more frequently to assess progress. Heber also asked an international CPA firm to prepare an auditor's report that would comment on the reasonableness and fairness of Heber's approach to assessing and measuring environmental performance.

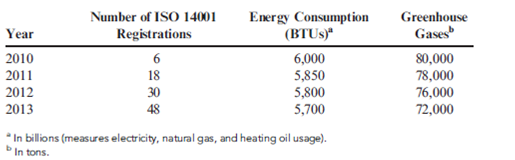

At the end of 2013, the controller had gathered data that would be used in preparing the environmental progress report. A sample of the data collected is as follows:

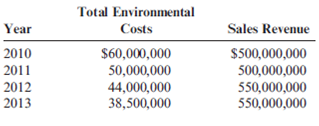

As part of its environmental cost reporting system, Heber tracks its total environmental costs. Consider the following cost and sales data:

Required:

1. Using the data, prepare a bar graph for each of the three environmental variables provided (registrations, energy, and greenhouse gases). Comment on the progress made on these three dimensions.

2. Prepare a bar graph for environmental costs expressed as a percentage of sales. Assuming that environmental performance has improved, explain why environmental costs have decreased.

3. Normalize energy consumption by expressing it as a multiple of sales (BTUs/Sales). Now, prepare a bar graph for energy. Comment on the progress made in reducing energy consumption. How does this compare with the conclusion that would be reached using a nonnormalized measure of progress? Which is the best approach? Explain.

At the beginning of 2010, Heber Company, an international telecommunications company, embarked on an environmental improvement program. The company set a goal to have all its facilities ISO 14001 registered by 2013. (There are 60 facilities worldwide.) To communicate the environmental progress made, management decided to issue, on a voluntary basis, an annual environmental progress report. Internally, the Accounting Department issued monthly progress reports and developed a number of measures that could be reported even more frequently to assess progress. Heber also asked an international CPA firm to prepare an auditor's report that would comment on the reasonableness and fairness of Heber's approach to assessing and measuring environmental performance.

At the end of 2013, the controller had gathered data that would be used in preparing the environmental progress report. A sample of the data collected is as follows:

As part of its environmental cost reporting system, Heber tracks its total environmental costs. Consider the following cost and sales data:

Required:

1. Using the data, prepare a bar graph for each of the three environmental variables provided (registrations, energy, and greenhouse gases). Comment on the progress made on these three dimensions.

2. Prepare a bar graph for environmental costs expressed as a percentage of sales. Assuming that environmental performance has improved, explain why environmental costs have decreased.

3. Normalize energy consumption by expressing it as a multiple of sales (BTUs/Sales). Now, prepare a bar graph for energy. Comment on the progress made in reducing energy consumption. How does this compare with the conclusion that would be reached using a nonnormalized measure of progress? Which is the best approach? Explain.

Explanation Verified

Verified

Environmental Responsibility Accounting ...

Cornerstones of Cost Management 2nd Edition by Don Hansen ,Maryanne Mowen

Why don’t you like this exercise?

Other Minimum 8 character and maximum 255 character

Character 255