Microeconomic Theory 11th Edition by Walter Nicholson,Christopher Snyder

Edition 11ISBN: 978-1111525538Microeconomic Theory 11th Edition by Walter Nicholson,Christopher Snyder

Edition 11ISBN: 978-1111525538 Exercise 2

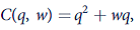

Suppose there are 1,000 identical firms producing diamonds. Let the total cost function for each firm be given by

where q is the firm's output level and w is the wage rate of diamond cutters.

a. If w = 10, what will be the firm's (short-run) supply curve? What is the industry's supply curve? How many diamonds will be produced at a price of 20 each? How many more diamonds would be produced at a price of 21?

b. Suppose the wages of diamond cutters depend on the total quantity of diamonds produced, and suppose the form of this relationship is given by

w = 0.002 Q ; here Q represents total industry output, which is 1,000 times the output of the typical firm.

In this situation, show that the firm's marginal cost (and short-run supply) curve depends on Q. What is the industrysupply curve? How much will be produced at a price of 20? How much more will be produced at a price of 21? What doyou conclude about the shape of the short-run supply curve?

where q is the firm's output level and w is the wage rate of diamond cutters.

a. If w = 10, what will be the firm's (short-run) supply curve? What is the industry's supply curve? How many diamonds will be produced at a price of 20 each? How many more diamonds would be produced at a price of 21?

b. Suppose the wages of diamond cutters depend on the total quantity of diamonds produced, and suppose the form of this relationship is given by

w = 0.002 Q ; here Q represents total industry output, which is 1,000 times the output of the typical firm.

In this situation, show that the firm's marginal cost (and short-run supply) curve depends on Q. What is the industrysupply curve? How much will be produced at a price of 20? How much more will be produced at a price of 21? What doyou conclude about the shape of the short-run supply curve?

Explanation Verified

Verified

Perfect Competition is a market structur...

Microeconomic Theory 11th Edition by Walter Nicholson,Christopher Snyder

Why don’t you like this exercise?

Other Minimum 8 character and maximum 255 character

Character 255