Cost Management 6th Edition by Edward Blocher,David Stout ,Paul Juras,Gary Cokins

Edition 6ISBN: 978-0078025532Cost Management 6th Edition by Edward Blocher,David Stout ,Paul Juras,Gary Cokins

Edition 6ISBN: 978-0078025532 Exercise 15

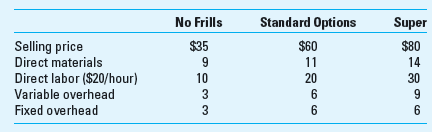

Product-Profitability Analysis; Scarce Resources Santana Company produces a variety of consumer electronic products. Unit selling prices and costs for three models of one of its product lines are as follows:

Variable overhead is charged to products on the basis of direct labor dollars; fixed overhead is allocated to products on the basis of machine-hours.

Required

1. What is fundamentally different about the fixed versus variable overhead assigned to products (Answer the question within the context of the relevance of this difference to the determination of short-term product mix.)

2. Calculate for each product both the gross profit per unit and the contribution margin per unit. Are either of these profitability measures useful for planning the optimum short-term product mix Why or why not

3. If the company has excess machine capacity but a limited amount of labor time, how should the optimum short-term product mix be determined

4. Assume now that machine-hours, not direct labor-hours, is the limiting resource. How, if at all, would this affect the product-mix decision

5. How can the optimum product mix be determined when there are only two products, and one or more constraints

6. How can the optimum product mix be determined when there are more than two products, and one or more constraints

7. What is the primary role of the management accountant in terms of planning the optimum short-term product mix

Variable overhead is charged to products on the basis of direct labor dollars; fixed overhead is allocated to products on the basis of machine-hours.

Required

1. What is fundamentally different about the fixed versus variable overhead assigned to products (Answer the question within the context of the relevance of this difference to the determination of short-term product mix.)

2. Calculate for each product both the gross profit per unit and the contribution margin per unit. Are either of these profitability measures useful for planning the optimum short-term product mix Why or why not

3. If the company has excess machine capacity but a limited amount of labor time, how should the optimum short-term product mix be determined

4. Assume now that machine-hours, not direct labor-hours, is the limiting resource. How, if at all, would this affect the product-mix decision

5. How can the optimum product mix be determined when there are only two products, and one or more constraints

6. How can the optimum product mix be determined when there are more than two products, and one or more constraints

7. What is the primary role of the management accountant in terms of planning the optimum short-term product mix

Explanation Verified

Verified

Answer Sub Part (1)

The variable costs ...

Cost Management 6th Edition by Edward Blocher,David Stout ,Paul Juras,Gary Cokins

Why don’t you like this exercise?

Other Minimum 8 character and maximum 255 character

Character 255