Fundamentals of Cost Accounting 2nd Edition by William Lanen, Carolyn Wells, Michael Maher

Edition 2ISBN: 978-0077274993Fundamentals of Cost Accounting 2nd Edition by William Lanen, Carolyn Wells, Michael Maher

Edition 2ISBN: 978-0077274993 Exercise 12

Pricing Decisions

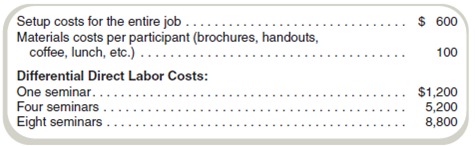

Sam, Martina, Aretha, Roxi, and Tomas (SMART) operate a management consulting firm. The firm has just received an inquiry from a prospective client about its prices for educational seminars to teach its supervisors better communications skills. The prospective client wants bids for three alternative activity levels: (1) one seminar with 20 participants, (2) four seminars with 20 participants each (80 participants total), or (3) eight seminars with 140 participants in total. The consulting firm's accountants have provided the following differential cost estimates:

In addition to the preceding differential costs, SMART allocates fixed costs to jobs on a directlabor- cost basis, at a rate of 75 percent of direct labor costs (excluding setup costs). For example, if direct labor costs are $100, SMART would also charge the job $75 for fixed costs. SMART charges clients for its costs plus 25 percent. For the purpose of charging customers, costs equal the setup costs plus materials costs plus differential labor costs plus allocated fixed costs. SMART has enough excess capacity to handle this job with ease.

Required

a. Assume SMART's bid equals the total cost, including fixed costs allocated to the job, plus the 25 percent markup on cost. What should SMART bid for each of the three levels of activity

b. Compute the differential cost (including setup costs) and the contribution to profit for each of the three levels of activity. Note that fixed costs are not differential costs.

c. Assume the prospective client gives three options. It is willing to accept either of SMART's bids for the one-seminar or four-seminar activity levels, but the prospective client will pay only 85 percent of the bid price for the eight-seminar package. SMART's president responds, "We can't make money in this business by shaving our bids! Let's take the four-seminar option because we make the most profit on it." Do you agree What would be the contribution to profit for each of the three options

Sam, Martina, Aretha, Roxi, and Tomas (SMART) operate a management consulting firm. The firm has just received an inquiry from a prospective client about its prices for educational seminars to teach its supervisors better communications skills. The prospective client wants bids for three alternative activity levels: (1) one seminar with 20 participants, (2) four seminars with 20 participants each (80 participants total), or (3) eight seminars with 140 participants in total. The consulting firm's accountants have provided the following differential cost estimates:

In addition to the preceding differential costs, SMART allocates fixed costs to jobs on a directlabor- cost basis, at a rate of 75 percent of direct labor costs (excluding setup costs). For example, if direct labor costs are $100, SMART would also charge the job $75 for fixed costs. SMART charges clients for its costs plus 25 percent. For the purpose of charging customers, costs equal the setup costs plus materials costs plus differential labor costs plus allocated fixed costs. SMART has enough excess capacity to handle this job with ease.

Required

a. Assume SMART's bid equals the total cost, including fixed costs allocated to the job, plus the 25 percent markup on cost. What should SMART bid for each of the three levels of activity

b. Compute the differential cost (including setup costs) and the contribution to profit for each of the three levels of activity. Note that fixed costs are not differential costs.

c. Assume the prospective client gives three options. It is willing to accept either of SMART's bids for the one-seminar or four-seminar activity levels, but the prospective client will pay only 85 percent of the bid price for the eight-seminar package. SMART's president responds, "We can't make money in this business by shaving our bids! Let's take the four-seminar option because we make the most profit on it." Do you agree What would be the contribution to profit for each of the three options

Explanation Verified

Verified

Pricing decisions:

A pricing decision i...

Fundamentals of Cost Accounting 2nd Edition by William Lanen, Carolyn Wells, Michael Maher

Why don’t you like this exercise?

Other Minimum 8 character and maximum 255 character

Character 255