Accounting for Decision Making and Control 6th Edition by Jerold Zimmerman

Edition 6ISBN: 9780071283700Accounting for Decision Making and Control 6th Edition by Jerold Zimmerman

Edition 6ISBN: 9780071283700 Exercise 7

Haking Cameras, a Hong Kong firm, assembles digital cameras in its plant located in the south of China. It assembles cameras for Kodak, Fuji, and Canon. These companies purchase the parts for their cameras and send them to Haking, which builds the complete digital cameras.

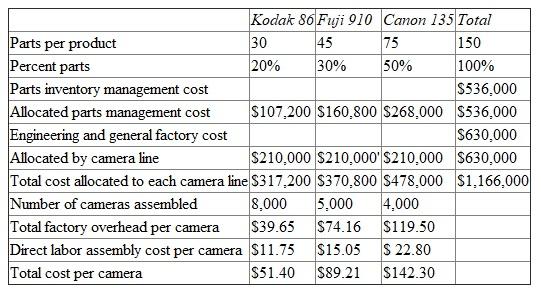

Haking uses an ABC system to cost the three digital cameras that it assembles. There are two activity cost pools comprising total factory overhead: parts management costs, and engineering and general factory costs. Parts management arranges for the delivery, unpacking, and inspection of each part and then inventories the parts and delivers them as needed by the assembly department to build the cameras. The number of parts in each camera is the assumed cost driver of the parts management activity cost pool. The engineering and general factory activity cost pool consists of all other indirect costs incurred in the plant. The cost driver of this activity cost pool is assumed to be the number of different digital cameras assembled during the year. There are only three different cameras being assembled this year.

The following table computes the ABC cost of each camera in Hong Kong dollars (HK$).

Required:

Required:

a. Haking is considering adopting a traditional absorption costing system where all the factory costs (parts inventory management and engineering and factory overhead) are allocated to cameras based on the direct labor cost of assembling each camera. Calculate the absorption-based full cost per camera of assembling each of the three camera types using total direct labor cost to allocate all the factory overhead costs.

b. Discuss some possible reasons why Haking might want to shift from its ABC system to absorption costing.

Haking uses an ABC system to cost the three digital cameras that it assembles. There are two activity cost pools comprising total factory overhead: parts management costs, and engineering and general factory costs. Parts management arranges for the delivery, unpacking, and inspection of each part and then inventories the parts and delivers them as needed by the assembly department to build the cameras. The number of parts in each camera is the assumed cost driver of the parts management activity cost pool. The engineering and general factory activity cost pool consists of all other indirect costs incurred in the plant. The cost driver of this activity cost pool is assumed to be the number of different digital cameras assembled during the year. There are only three different cameras being assembled this year.

The following table computes the ABC cost of each camera in Hong Kong dollars (HK$).

Required: a. Haking is considering adopting a traditional absorption costing system where all the factory costs (parts inventory management and engineering and factory overhead) are allocated to cameras based on the direct labor cost of assembling each camera. Calculate the absorption-based full cost per camera of assembling each of the three camera types using total direct labor cost to allocate all the factory overhead costs.

b. Discuss some possible reasons why Haking might want to shift from its ABC system to absorption costing.

Explanation Verified

Verified

Two widely used method of allocating ove...

Accounting for Decision Making and Control 6th Edition by Jerold Zimmerman

Why don’t you like this exercise?

Other Minimum 8 character and maximum 255 character

Character 255