Auditing and Assurance Services 9th Edition by Alvin Arens,Mark Beasley,Randy Elder

Edition 9ISBN: 978-0130459206Auditing and Assurance Services 9th Edition by Alvin Arens,Mark Beasley,Randy Elder

Edition 9ISBN: 978-0130459206 Exercise 22

You are auditing the financial statements for your new client, Paper Packaging Corporation, a manufacturer of paper containers, for the year ended March 31, 2014. Paper Packaging's previous auditors had issued a going concern opinion on the March 31, 2013, financial statements for the following reasons:

• Paper Packaging had defaulted on $10 million of unregistered debentures sold to three insurance companies, which were due in 2013, and the default constituted a possible violation of other debt agreements.

• The interest and principal payments due on the remainder of a 10-year credit agreement, which began in 2009, would exceed the cash flows generated from operations in recent years.

• The company had disposed of certain operating units. The proceeds from the sale were subject to possible adjustment through arbitration proceedings, the outcome of which was uncertain at year-end.

• Various lawsuits were pending against the company.

• The company was in the midst of tax proceedings as a result of an examination of the company's federal income tax returns for a period of 12 years.

You find that the status of the above matters is as follows at year-end, March 31, 2014:

• The company is still in default on $4.6 million of the debentures due in 2013 but is trying to negotiate a settlement with remaining bondholders. A large number of bondholders have settled their claims at significantly less than par.

• The company has renegotiated the 2009 credit agreement, which provides for a two-year moratorium on principal payments and interest at 8 percent. It also limits net losses ($2.25 million for 2014) and requires a certain level of defined cumulative quarterly operating income to be maintained.

• The arbitration proceedings were resolved in 2014.

• The legal actions were settled in 2014.

• Most of the tax issues have been resolved, and, according to the company's outside legal counsel, those remaining will result in a net cash inflow to the company.

At year-end, Paper Packaging had a cash balance of $5.5 million and expects to generate a net cash flow of $3.2 million in the upcoming fiscal year.

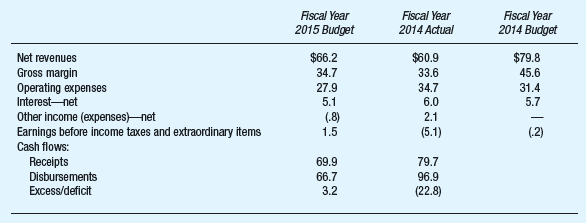

The following information about Paper Packaging's plans for its operations for the fiscal year ending in 2015 may also be useful in arriving at a decision.

Required (for this question, you may wish to reference extant auditing standards):

a. What should you consider in deciding whether to discuss a going concern uncertainty in your report?

b. How much influence should the report on the March 31, 2013, financial statements have on your decision?

c. Should your report for the year ended March 31, 2014, include a discussion of a going concern uncertainty? Briefly explain why or why not.

• Paper Packaging had defaulted on $10 million of unregistered debentures sold to three insurance companies, which were due in 2013, and the default constituted a possible violation of other debt agreements.

• The interest and principal payments due on the remainder of a 10-year credit agreement, which began in 2009, would exceed the cash flows generated from operations in recent years.

• The company had disposed of certain operating units. The proceeds from the sale were subject to possible adjustment through arbitration proceedings, the outcome of which was uncertain at year-end.

• Various lawsuits were pending against the company.

• The company was in the midst of tax proceedings as a result of an examination of the company's federal income tax returns for a period of 12 years.

You find that the status of the above matters is as follows at year-end, March 31, 2014:

• The company is still in default on $4.6 million of the debentures due in 2013 but is trying to negotiate a settlement with remaining bondholders. A large number of bondholders have settled their claims at significantly less than par.

• The company has renegotiated the 2009 credit agreement, which provides for a two-year moratorium on principal payments and interest at 8 percent. It also limits net losses ($2.25 million for 2014) and requires a certain level of defined cumulative quarterly operating income to be maintained.

• The arbitration proceedings were resolved in 2014.

• The legal actions were settled in 2014.

• Most of the tax issues have been resolved, and, according to the company's outside legal counsel, those remaining will result in a net cash inflow to the company.

At year-end, Paper Packaging had a cash balance of $5.5 million and expects to generate a net cash flow of $3.2 million in the upcoming fiscal year.

The following information about Paper Packaging's plans for its operations for the fiscal year ending in 2015 may also be useful in arriving at a decision.

Required (for this question, you may wish to reference extant auditing standards):

a. What should you consider in deciding whether to discuss a going concern uncertainty in your report?

b. How much influence should the report on the March 31, 2013, financial statements have on your decision?

c. Should your report for the year ended March 31, 2014, include a discussion of a going concern uncertainty? Briefly explain why or why not.

Explanation

This question doesn’t have an expert verified answer yet, let Examlex AI Copilot help.

Auditing and Assurance Services 9th Edition by Alvin Arens,Mark Beasley,Randy Elder

Why don’t you like this exercise?

Other Minimum 8 character and maximum 255 character

Character 255