Fundamentals of Financial Accounting 4th Edition by Fred Phillips,Robert Libby,Patricia Libby

Edition 4ISBN: 978-0078025372Fundamentals of Financial Accounting 4th Edition by Fred Phillips,Robert Libby,Patricia Libby

Edition 4ISBN: 978-0078025372 Exercise 1

Analyzing the Effects of Four Alternative Inventory Methods in a Periodic Inventory System

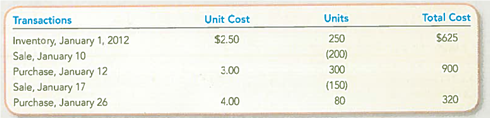

Mojo Industries tracks the number of units purchased and sold throughout each accounting period but applies its inventory costing method at the end of each period, as if it uses a periodic inventory system. Assume its accounting records provided the following information at the end of the accounting period, January 31, 2012. The inventory's selling price is $9 per unit.

Required:

1. Compute the amount of goods available for sale, ending inventory, and cost of goods sold at January 31, 2012, under each of the following inventory costing methods:

a. Weighted average cost.

b. First-in, first-out.

c. Last-in, first-out.

d. Specific identification, assuming that the January 10 sale was from the beginning inventory and the January 17 sale was from the January 12 purchase.

2. Of the four methods, which will result in the highest gross profit Which will result in the lowest income taxes

Mojo Industries tracks the number of units purchased and sold throughout each accounting period but applies its inventory costing method at the end of each period, as if it uses a periodic inventory system. Assume its accounting records provided the following information at the end of the accounting period, January 31, 2012. The inventory's selling price is $9 per unit.

Required:

1. Compute the amount of goods available for sale, ending inventory, and cost of goods sold at January 31, 2012, under each of the following inventory costing methods:

a. Weighted average cost.

b. First-in, first-out.

c. Last-in, first-out.

d. Specific identification, assuming that the January 10 sale was from the beginning inventory and the January 17 sale was from the January 12 purchase.

2. Of the four methods, which will result in the highest gross profit Which will result in the lowest income taxes

Explanation Verified

Verified

Fundamentals of Financial Accounting 4th Edition by Fred Phillips,Robert Libby,Patricia Libby

Why don’t you like this exercise?

Other Minimum 8 character and maximum 255 character

Character 255