Global Business 4th Edition by Mike Peng

Edition 4ISBN: 978-1305500891Global Business 4th Edition by Mike Peng

Edition 4ISBN: 978-1305500891 Exercise 2

What Makes Analysts Say Buy

A research study conducted by Harvard Business School professors regarding analyst ratings of companies which provide buy, sell, or hold ratings for those companies sought to answer whether there were differences between analysts in different parts of the world. This synopsis of their findings appeared in the Harvard Business Review. Head about their findings and answer the questions at the end of the case.

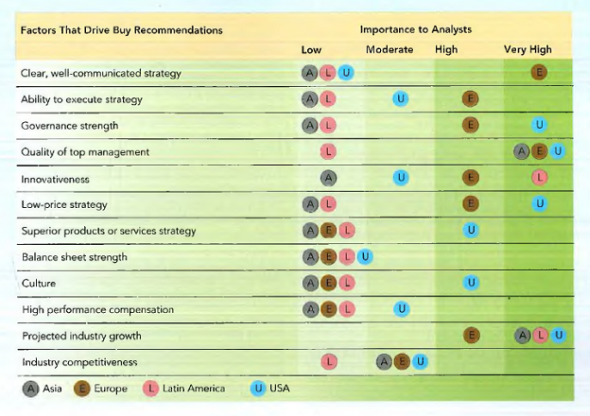

Wall Street analysts' recommendations can move markets. But even though leaders of public companies spend significant amounts of time interacting with this constituency, there's little information about how analysts arrive at their recommendations. What factors most influence their thinking

We set out to answer that question through a global study of analyst forecasts and stock performance over two consecutive years in the mid-2000s. We surveyed nearly 1,000 analysts in Asia, Europe, Latin America, and in the U.S., asking them to rate almost 1,000 large companies on 12 factors, using a scale of one to five, and to forecast revenue growth, earnings growth, and gross margin on the basis of those ratings. We also estimated how important each factor was to their ultimate recommendations.

The strongest determinant of a buy or sell recommendation, we learned, is projected industry growth, followed by the quality of the top management team. Analysts in different regions often weighed factors quite differently, though. For example, having a clear, well-communicated strategy was of "very high " importance to analysts in Europe but of "low" importance to those in other regions. One of the most interesting findings was the uneven importance of governance: It's much more significant to U.S. and European analysts than to analysts in Latin America and Asia. Why Our best guess is that increased governance disclosure and regulation in the U.S. and Europe have made governance an area of focus for many analysts in those regions.

Some of the factors that affect analysts' views lie beyond a company's or an executive's power-a manager has little sway over industry growth, for example. But many are well within executive control. For instance, it's the job of the CEO and the Manage- V) ment team to communicate the team's strengths to the market.

Leaders can use this research to shape what they emphasize in managing their companies and when sharing information about them with the outsiders who drive market cap. The rewards, though also variable by region, can be significant. Consider this finding: A new buy recommendation for large firms that analysts viewed as having high-quality top management increased market cap, on average, by $2.4 billion in Asia, $1.4 billion in Europe, and $40 million in Latin America. And if the buy recommendation is contrarianthat is, if the consensus recommendation is hold or sell- the effect is even greater.

Source: B. Groysberg, P. Healy, N. Nohria, G. Serafeim What Makes Analysts Say "Buy" Harvard Business Review, November, 2012.\

Why do analysts in the US and Europe pay more attention to corporate governance

A research study conducted by Harvard Business School professors regarding analyst ratings of companies which provide buy, sell, or hold ratings for those companies sought to answer whether there were differences between analysts in different parts of the world. This synopsis of their findings appeared in the Harvard Business Review. Head about their findings and answer the questions at the end of the case.

Wall Street analysts' recommendations can move markets. But even though leaders of public companies spend significant amounts of time interacting with this constituency, there's little information about how analysts arrive at their recommendations. What factors most influence their thinking

We set out to answer that question through a global study of analyst forecasts and stock performance over two consecutive years in the mid-2000s. We surveyed nearly 1,000 analysts in Asia, Europe, Latin America, and in the U.S., asking them to rate almost 1,000 large companies on 12 factors, using a scale of one to five, and to forecast revenue growth, earnings growth, and gross margin on the basis of those ratings. We also estimated how important each factor was to their ultimate recommendations.

The strongest determinant of a buy or sell recommendation, we learned, is projected industry growth, followed by the quality of the top management team. Analysts in different regions often weighed factors quite differently, though. For example, having a clear, well-communicated strategy was of "very high " importance to analysts in Europe but of "low" importance to those in other regions. One of the most interesting findings was the uneven importance of governance: It's much more significant to U.S. and European analysts than to analysts in Latin America and Asia. Why Our best guess is that increased governance disclosure and regulation in the U.S. and Europe have made governance an area of focus for many analysts in those regions.

Some of the factors that affect analysts' views lie beyond a company's or an executive's power-a manager has little sway over industry growth, for example. But many are well within executive control. For instance, it's the job of the CEO and the Manage- V) ment team to communicate the team's strengths to the market.

Leaders can use this research to shape what they emphasize in managing their companies and when sharing information about them with the outsiders who drive market cap. The rewards, though also variable by region, can be significant. Consider this finding: A new buy recommendation for large firms that analysts viewed as having high-quality top management increased market cap, on average, by $2.4 billion in Asia, $1.4 billion in Europe, and $40 million in Latin America. And if the buy recommendation is contrarianthat is, if the consensus recommendation is hold or sell- the effect is even greater.

Source: B. Groysberg, P. Healy, N. Nohria, G. Serafeim What Makes Analysts Say "Buy" Harvard Business Review, November, 2012.\

Why do analysts in the US and Europe pay more attention to corporate governance

Explanation Verified

Verified

A research was conducted by HB school pr...

Global Business 4th Edition by Mike Peng

Why don’t you like this exercise?

Other Minimum 8 character and maximum 255 character

Character 255