Fundamental Accounting Principles 22th Edition by John Wild ,Ken Shaw,Barbara Chiappetta

Edition 22ISBN: 978-0077862275Fundamental Accounting Principles 22th Edition by John Wild ,Ken Shaw,Barbara Chiappetta

Edition 22ISBN: 978-0077862275 Exercise 2

Following is selected financial information for Kojo Company for the year ended December 31, 2015.

Required

Prepare the 2015 statement of owner's equity for Kojo Company.

Required

Prepare the 2015 statement of owner's equity for Kojo Company.

Explanation Verified

Verified

Retained earnings

Retained earnings refers to the part of the net earning or income which is not paid in the form of dividend and retained by the organization for the purpose of reinvestment or making payment towards its debt. It is generally written underlying the equity shareholder underlying the balance sheet

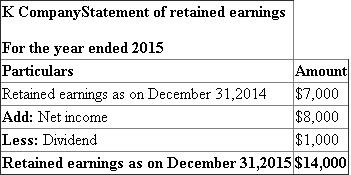

Therefore, the statement of retained earnings pertaining to K Company for the year 2015 is shown below:

Hence, it is ascertained that the retained earnings as on December 31, 2015 accounts for

Hence, it is ascertained that the retained earnings as on December 31, 2015 accounts for

Retained earnings refers to the part of the net earning or income which is not paid in the form of dividend and retained by the organization for the purpose of reinvestment or making payment towards its debt. It is generally written underlying the equity shareholder underlying the balance sheet

Therefore, the statement of retained earnings pertaining to K Company for the year 2015 is shown below:

Hence, it is ascertained that the retained earnings as on December 31, 2015 accounts for Fundamental Accounting Principles 22th Edition by John Wild ,Ken Shaw,Barbara Chiappetta

Why don’t you like this exercise?

Other Minimum 8 character and maximum 255 character

Character 255