Managerial Economics & Organizational Architecture 6th Edition by James Brickley , Clifford Smith ,Jerold Zimmerman

Edition 6ISBN: 978-0073523149Managerial Economics & Organizational Architecture 6th Edition by James Brickley , Clifford Smith ,Jerold Zimmerman

Edition 6ISBN: 978-0073523149 Exercise 7

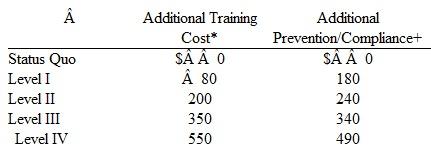

Guest Watches is a division of Guest Fashions, a large, international fashion designer. Guest Watches manufactures highly stylish watches for young adults (18-30) who are fashion conscious. It is a profit center and its senior management's compensation is tied closely to the watch division's reported profits. Guest Watches has succeeded in capturing the fashion market, but a lack of product dependability is eroding these gains. A number of retailers have dropped or are threatening to drop the Guest watch line because of customer returns. Guest Watches carry a 1-year warranty, and 12 percent are returned, compared to an industry average of 4 percent. Besides high warranty costs and lost sales due to reputation, Guest has higher than industry average manufacturing scrap and rework costs. Senior management, worried about these trends and the possible erosion of its market dominance, hired a consulting firm to study the problem and make recommendations for reversing the situation. After a thorough analysis of Guest's customers, suppliers, and manufacturing facilities, the consultants recommended five possible actions, ranging from the status quo to a complete total quality management, zero defects program (Level IV). The table below outlines the various alternatives (in thousands of dollars):

* Includes the annual costs of training employees in TQM methods.

* Includes the annual costs of training employees in TQM methods.

+ All annual costs including certifying suppliers, redesigning the product, and inspection costs to reduce defects.

The consultant emphasized that while first-year startup costs are slightly higher than subsequent years, management must really view the cost estimates in the table as annual, ongoing costs. Given employee turnover and the assumption that supplier changes, training, prevention, and compliance costs are not likely to decline over time, the costs in the preceding table will be annual operating expenses.

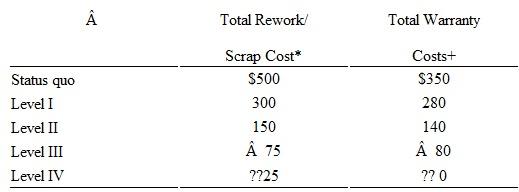

The consulting firm and the newly appointed vice president for quality programs estimated that under level IV, rework and scrap would be $25,000 and warranty costs zero. Level IV was needed to get the firm to zero defects. A task force was convened, and after several meetings, it generated the following estimates of rework/scrap and warranty costs for the various levels of firm commitment:

* The costs of manufacturing scrap and rework.

* The costs of manufacturing scrap and rework.

+ The costs of repairing and replacing products that fail in the hands of customers.

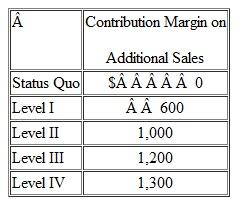

There was considerable discussion and debate about the quantitative impact of increased quality on additional sales. Although no hard-and-fast numbers could be derived, the consensus view was that the total net cash flows (contribution margin) from additional sales as retailers and customers learn of the reduced defect rate would be as follows:

* Includes the annual costs of training employees in TQM methods.+ All annual costs including certifying suppliers, redesigning the product, and inspection costs to reduce defects.

The consultant emphasized that while first-year startup costs are slightly higher than subsequent years, management must really view the cost estimates in the table as annual, ongoing costs. Given employee turnover and the assumption that supplier changes, training, prevention, and compliance costs are not likely to decline over time, the costs in the preceding table will be annual operating expenses.

The consulting firm and the newly appointed vice president for quality programs estimated that under level IV, rework and scrap would be $25,000 and warranty costs zero. Level IV was needed to get the firm to zero defects. A task force was convened, and after several meetings, it generated the following estimates of rework/scrap and warranty costs for the various levels of firm commitment:

* The costs of manufacturing scrap and rework.+ The costs of repairing and replacing products that fail in the hands of customers.

There was considerable discussion and debate about the quantitative impact of increased quality on additional sales. Although no hard-and-fast numbers could be derived, the consensus view was that the total net cash flows (contribution margin) from additional sales as retailers and customers learn of the reduced defect rate would be as follows:

Explanation Verified

Verified

Managerial Economics & Organizational Architecture 6th Edition by James Brickley , Clifford Smith ,Jerold Zimmerman

Why don’t you like this exercise?

Other Minimum 8 character and maximum 255 character

Character 255