Introductory Econometrics 4th Edition by Jeffrey Wooldridge

Edition 4ISBN: 978-0324660609Introductory Econometrics 4th Edition by Jeffrey Wooldridge

Edition 4ISBN: 978-0324660609 Exercise 20

Let hy6t denote the three-month holding yield (in percent) from buying a six-month T-bill at time (t - 1) and selling it at time t (three months hence) as a three-month

T-bill. Let hy3t-1 be the three-month holding yield from buying a three-month T-bill at time (t - 1). At time (t - 1), hy3t-1 is known, whereas hy6t is unknown because p3t (the price of three-month T-bills) is unknown at time (t - 1). The expectations hypothesis (EH) says that these two different three-month investments should be the

same, on average. Mathematically, we can write this as a conditional expectation:

where It-1 denotes all observable information up through time t - 1. This suggests estimating the model and testing H0: = 1. (We can also test H0: 0 = 0, but we often allow for a term premium for buying assets with different maturities, so that 0 0.)

and testing H0: = 1. (We can also test H0: 0 = 0, but we often allow for a term premium for buying assets with different maturities, so that 0 0.)

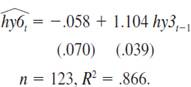

(i) Estimating the previous equation by OLS using the data in INTQRT.RAW (spaced every three months) gives

Do you reject H0: 1=1 against H0: 1 1 at the 1% significance level Does the estimate seem practically different from one

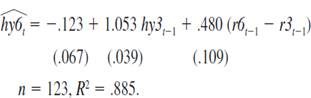

(ii) Another implication of the EH is that no other variables dated as t - 1 or earlier should help explain hy6t, once hy3t-1 has been controlled for. Including one lag of the spread between six-month and three-month T-bill rates gives

Now, is the coefficient on hy3t - 1 statistically different from one Is the lagged spread term significant According to this equation, if, at time t - 1, r6 is above r3, should you invest in six-month or three-month T-bills

(iii) The sample correlation between hy3t and hy3t - 1 is.914. Why might this raise some concerns with the previous analysis

(iv) How would you test for seasonality in the equation estimated in part (ii)

T-bill. Let hy3t-1 be the three-month holding yield from buying a three-month T-bill at time (t - 1). At time (t - 1), hy3t-1 is known, whereas hy6t is unknown because p3t (the price of three-month T-bills) is unknown at time (t - 1). The expectations hypothesis (EH) says that these two different three-month investments should be the

same, on average. Mathematically, we can write this as a conditional expectation:

where It-1 denotes all observable information up through time t - 1. This suggests estimating the model

and testing H0: = 1. (We can also test H0: 0 = 0, but we often allow for a term premium for buying assets with different maturities, so that 0 0.)(i) Estimating the previous equation by OLS using the data in INTQRT.RAW (spaced every three months) gives

Do you reject H0: 1=1 against H0: 1 1 at the 1% significance level Does the estimate seem practically different from one

(ii) Another implication of the EH is that no other variables dated as t - 1 or earlier should help explain hy6t, once hy3t-1 has been controlled for. Including one lag of the spread between six-month and three-month T-bill rates gives

Now, is the coefficient on hy3t - 1 statistically different from one Is the lagged spread term significant According to this equation, if, at time t - 1, r6 is above r3, should you invest in six-month or three-month T-bills

(iii) The sample correlation between hy3t and hy3t - 1 is.914. Why might this raise some concerns with the previous analysis

(iv) How would you test for seasonality in the equation estimated in part (ii)

Explanation Verified

Verified

Consider ![]() to be three month holding yiel...

to be three month holding yiel...

Introductory Econometrics 4th Edition by Jeffrey Wooldridge

Why don’t you like this exercise?

Other Minimum 8 character and maximum 255 character

Character 255