Deck 7: Inflation

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

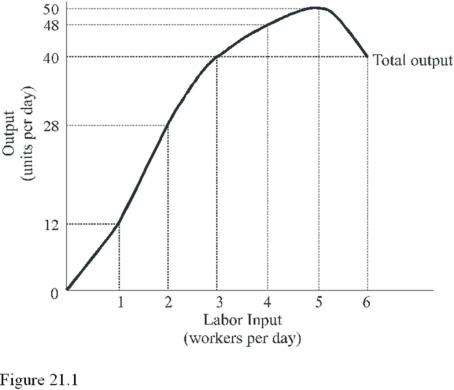

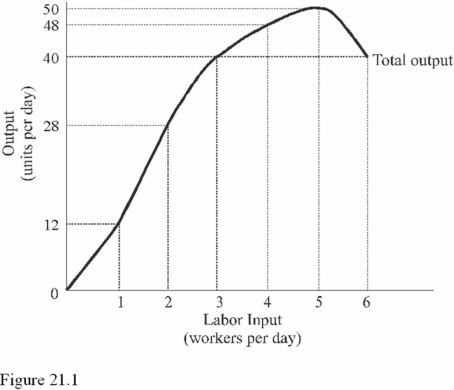

In Figure 21.1, diminishing marginal returns first occur with the

In Figure 21.1, diminishing marginal returns first occur with theA) Fifth worker.

B) Fourth worker.

C) Third worker.

D) Second worker.

Question

Question

Question

Question

Question

Question

The marginal physical product of labor in Figure 21.1 is negative for the

The marginal physical product of labor in Figure 21.1 is negative for theA) Third worker.

B) Fourth worker.

C) Fifth worker.

D) Sixth worker.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

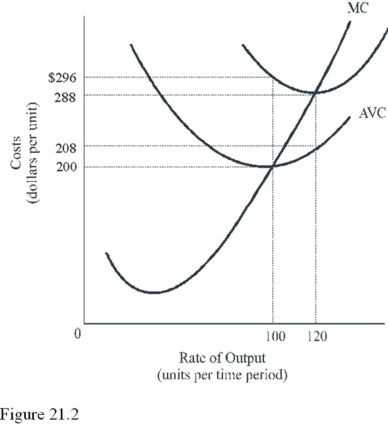

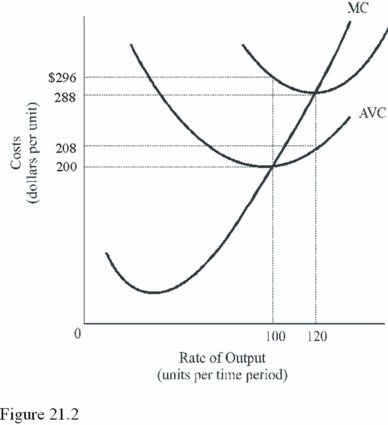

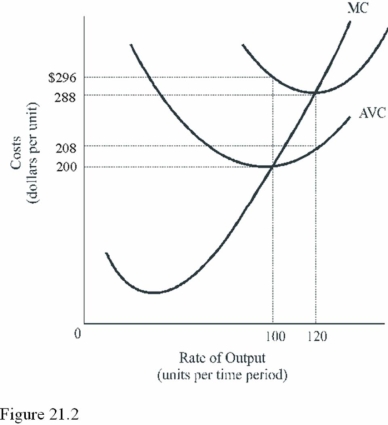

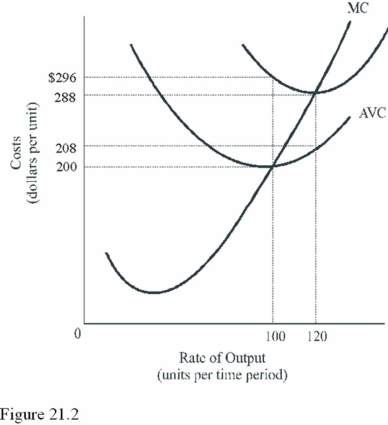

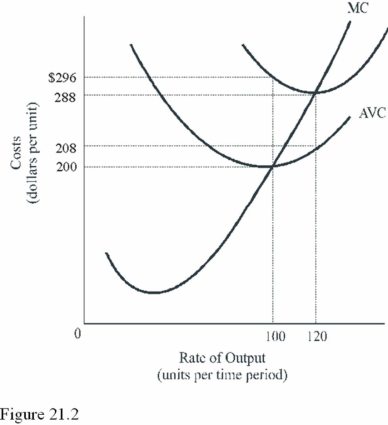

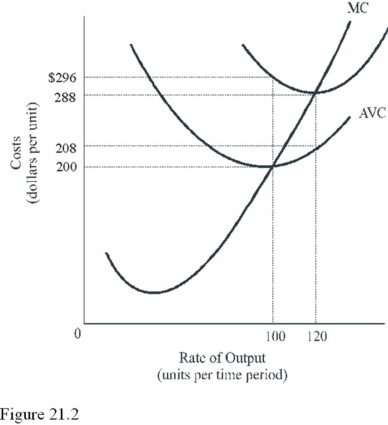

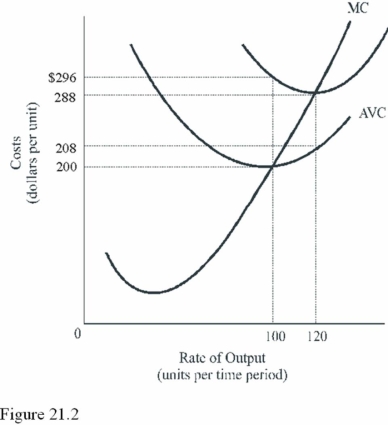

What is the total fixed cost in Figure 21.2?

What is the total fixed cost in Figure 21.2?A) $80.

B) $10,000.

C) $9,600.

D) $29,600.

Question

What is the total cost of 120 units in Figure 21.2?

What is the total cost of 120 units in Figure 21.2?A) $34,560.

B) $9,600.

C) $24,960.

D) $10,560.

Question

Question

Question

Question

At what output level do diminishing marginal returns begin in Figure 21.2?

At what output level do diminishing marginal returns begin in Figure 21.2?A) 40 units.

B) 100 units.

C) 120 units.

D) Only the production function will indicate when diminishing marginal returns begin.

Question

Question

Question

Question

Question

In Figure 21.2, at what output does this firm maximize technical efficiency?

In Figure 21.2, at what output does this firm maximize technical efficiency?A) 0 units.

B) 40 units.

C) 100 units.

D) 120 units.

Question

What is the average fixed cost when output is 120 units in Figure 21.2?

What is the average fixed cost when output is 120 units in Figure 21.2?A) $0.67.

B) $80.00.

C) $96.00.

D) $208.00.

Question

Question

What is the total variable cost when output is 100 units in Figure 21.2?

What is the total variable cost when output is 100 units in Figure 21.2?A) $9,600.

B) $296.

C) $200.

D) $20,000.

Question

Question

Question

Question

Question

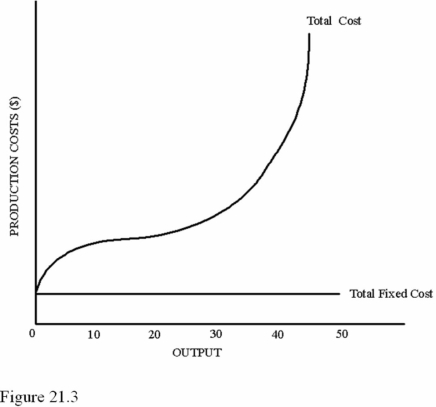

Refer to Figure 21.3. The vertical difference between the total cost curve and the total fixed cost curve represents

Refer to Figure 21.3. The vertical difference between the total cost curve and the total fixed cost curve representsA) Total variable costs.

B) Total marginal costs.

C) Average fixed costs.

D) Average variable costs.

Question

What is the marginal cost of the 120th unit of output in Figure 21.2?

What is the marginal cost of the 120th unit of output in Figure 21.2?A) $1.20.

B) $200.00.

C) $208.00.

D) $288.00.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

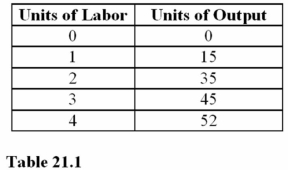

With which unit of labor do diminishing marginal returns first appear in Table 21.1?

With which unit of labor do diminishing marginal returns first appear in Table 21.1?A) The first.

B) The second.

C) The third.

D) The fourth.

Question

Question

If workers are paid $10, what is the labor cost per unit of output in Table 21.1 when output is increased from 15 to 35 units of output?

If workers are paid $10, what is the labor cost per unit of output in Table 21.1 when output is increased from 15 to 35 units of output?A) $0.28 per unit.

B) $0.50 per unit.

C) $10 per unit.

D) $20 per unit.

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/150

Play

Full screen (f)

Deck 7: Inflation

1

The marginal physical product is the

A) Change in total input required to produce one additional unit of output.

B) Change in total output associated with one additional unit of the variable input.

C) Number of units of output obtained from all units of input employed.

D) Additional cost of an additional unit of output.

A) Change in total input required to produce one additional unit of output.

B) Change in total output associated with one additional unit of the variable input.

C) Number of units of output obtained from all units of input employed.

D) Additional cost of an additional unit of output.

B

2

When a firm produces at a technically efficient output level, it is

A) Producing the output at the minimum MC curve.

B) Using the fewest resources to produce a good or service.

C) Producing the output where the AVC curve is at a minimum.

D) Producing the best combination of goods and services.

A) Producing the output at the minimum MC curve.

B) Using the fewest resources to produce a good or service.

C) Producing the output where the AVC curve is at a minimum.

D) Producing the best combination of goods and services.

B

3

In the short run, the law of diminishing returns

A) Occurs for only a few economies.

B) Can be observed in every production process.

C) Does not occur in command economies.

D) Can be overcome by using more variable inputs.

A) Occurs for only a few economies.

B) Can be observed in every production process.

C) Does not occur in command economies.

D) Can be overcome by using more variable inputs.

B

4

A production function shows

A) How a firm's production increases as it adds more labor.

B) How a firm's costs of production increase as it produces more goods.

C) How production changes as its unit costs go up.

D) How total costs increase as labor is added.

A) How a firm's production increases as it adds more labor.

B) How a firm's costs of production increase as it produces more goods.

C) How production changes as its unit costs go up.

D) How total costs increase as labor is added.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

5

Which of the following is a factor of production for the Little Biscuit Bread Company?

A) Flour.

B) Bread.

C) Productivity.

D) Money.

A) Flour.

B) Bread.

C) Productivity.

D) Money.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

6

The change in total output associated with one additional unit of input is the

A) Opportunity cost of the output.

B) Average productivity.

C) Marginal physical product.

D) Marginal cost.

A) Opportunity cost of the output.

B) Average productivity.

C) Marginal physical product.

D) Marginal cost.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

7

Labor productivity will increase in response to

A) Lower wages.

B) An increase in the amount of physical capital per worker.

C) Higher resource costs.

D) An increase in diminishing returns.

A) Lower wages.

B) An increase in the amount of physical capital per worker.

C) Higher resource costs.

D) An increase in diminishing returns.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

8

If a firm could hire all the workers it wanted at a zero wage (i.e., the workers are volunteers), the firm should hire

A) Enough workers to produce the output where diminishing returns begin.

B) Enough workers to produce the output where worker productivity is the highest.

C) Enough workers to produce where the MPP equals zero.

D) All the workers that can fit into the factory.

A) Enough workers to produce the output where diminishing returns begin.

B) Enough workers to produce the output where worker productivity is the highest.

C) Enough workers to produce where the MPP equals zero.

D) All the workers that can fit into the factory.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

9

The period in which at least one input is fixed in quantity is the

A) Long run.

B) Production run.

C) Short run.

D) Investment decision.

A) Long run.

B) Production run.

C) Short run.

D) Investment decision.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

10

In Figure 21.1, diminishing marginal returns first occur with theA) Fifth worker.

B) Fourth worker.

C) Third worker.

D) Second worker.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

11

The most desired goods and services that are given up in order to get more of another good are the

A) Average total cost.

B) Variable cost.

C) Marginal cost.

D) Opportunity cost.

A) Average total cost.

B) Variable cost.

C) Marginal cost.

D) Opportunity cost.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

12

Diminishing returns occur because

A) Of inefficiency in the production process.

B) Of the use of inferior factors of production.

C) A firm increases the amount of a variable input without changing a fixed input.

D) Of lower opportunity costs of the factors of production.

A) Of inefficiency in the production process.

B) Of the use of inferior factors of production.

C) A firm increases the amount of a variable input without changing a fixed input.

D) Of lower opportunity costs of the factors of production.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

13

A production function shows the

A) Minimum amount of output that can be obtained from alternative combinations of inputs.

B) Maximum quantity of inputs required to produce a given quantity of output.

C) Maximum output that can be produced with varying combinations of factor inputs.

D) Output capacity of the entire economy.

A) Minimum amount of output that can be obtained from alternative combinations of inputs.

B) Maximum quantity of inputs required to produce a given quantity of output.

C) Maximum output that can be produced with varying combinations of factor inputs.

D) Output capacity of the entire economy.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

14

Which of the following are factors of production?

A) Output in a production function.

B) Productivity.

C) Land, labor, capital, and entrepreneurship.

D) Implicit and explicit costs.

A) Output in a production function.

B) Productivity.

C) Land, labor, capital, and entrepreneurship.

D) Implicit and explicit costs.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

15

Greater labor productivity means

A) Lower output per labor-hour.

B) Higher labor cost per unit of output.

C) Lower output per worker.

D) Higher output per worker.

A) Lower output per labor-hour.

B) Higher labor cost per unit of output.

C) Lower output per worker.

D) Higher output per worker.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

16

The marginal physical product of labor in Figure 21.1 is negative for theA) Third worker.

B) Fourth worker.

C) Fifth worker.

D) Sixth worker.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

17

Ceteris paribus, the law of diminishing returns states that beyond some point, the

A) Returns on stocks and bonds diminish with higher security prices.

B) Addition to total utility diminishes as more units of a good are consumed.

C) Marginal physical product of a factor of production diminishes as more of that factor is used.

D) Output of any good increases as more of a variable input is used.

A) Returns on stocks and bonds diminish with higher security prices.

B) Addition to total utility diminishes as more units of a good are consumed.

C) Marginal physical product of a factor of production diminishes as more of that factor is used.

D) Output of any good increases as more of a variable input is used.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

18

Which of the following is the slope of the production function with respect to an input?

A) The marginal physical product of the input.

B) The average product of the input.

C) The unit cost of the input.

D) The input price.

A) The marginal physical product of the input.

B) The average product of the input.

C) The unit cost of the input.

D) The input price.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

19

Technical efficiency is achieved when a firm produces

A) At an amount indicated by a point on the production function.

B) Below the opportunity cost for the resources it uses.

C) Enough output to cover the opportunity cost of resources.

D) An amount less than or equal to the production function.

A) At an amount indicated by a point on the production function.

B) Below the opportunity cost for the resources it uses.

C) Enough output to cover the opportunity cost of resources.

D) An amount less than or equal to the production function.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

20

The short-run production function shows how output changes when

A) The quantity of labor changes.

B) The quantity of land changes.

C) Technology changes.

D) The fixed inputs change.

A) The quantity of labor changes.

B) The quantity of land changes.

C) Technology changes.

D) The fixed inputs change.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

21

If an additional unit of labor costs $20 and has a MPP of 15 units of output, the marginal cost is

A) $0.75.

B) $1.33.

C) $30.00.

D) $300.00.

A) $0.75.

B) $1.33.

C) $30.00.

D) $300.00.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

22

If the marginal physical product (MPP) is falling, then the

A) Marginal cost of each unit of output is falling.

B) Marginal cost of each unit of output is rising.

C) Total cost of each unit of output is falling.

D) Total cost of each unit of output is rising.

A) Marginal cost of each unit of output is falling.

B) Marginal cost of each unit of output is rising.

C) Total cost of each unit of output is falling.

D) Total cost of each unit of output is rising.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

23

Average total cost is equal to

A) Total cost divided by fixed cost.

B) Total cost multiplied by quantity.

C) The sum of average variable cost and marginal cost.

D) Total cost divided by quantity produced.

A) Total cost divided by fixed cost.

B) Total cost multiplied by quantity.

C) The sum of average variable cost and marginal cost.

D) Total cost divided by quantity produced.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

24

In the short run, when a firm produces zero output, total cost equals

A) Zero.

B) Variable costs.

C) Fixed costs.

D) Marginal costs.

A) Zero.

B) Variable costs.

C) Fixed costs.

D) Marginal costs.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

25

In the short run, which of the following is most likely a variable cost?

A) Contractual lease payments.

B) Labor and raw materials costs.

C) Property taxes.

D) Interest payments on borrowed funds.

A) Contractual lease payments.

B) Labor and raw materials costs.

C) Property taxes.

D) Interest payments on borrowed funds.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

26

Changes in short-run total costs result from changes in

A) Variable costs.

B) Fixed costs.

C) Profit.

D) The price elasticity of demand.

A) Variable costs.

B) Fixed costs.

C) Profit.

D) The price elasticity of demand.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

27

Which of the following costs do not change when output changes in the short run?

A) Average variable costs.

B) Variable costs.

C) Average fixed costs.

D) Fixed costs.

A) Average variable costs.

B) Variable costs.

C) Average fixed costs.

D) Fixed costs.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

28

Marginal cost

A) Is the change in total output from hiring one more factor of production.

B) Is the change in total cost from producing one additional unit of output.

C) Falls when there are diminishing returns.

D) Is the change in the total cost when hiring one more factor of production.

A) Is the change in total output from hiring one more factor of production.

B) Is the change in total cost from producing one additional unit of output.

C) Falls when there are diminishing returns.

D) Is the change in the total cost when hiring one more factor of production.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

29

Which of the following is the best explanation of why the law of diminishing returns does not apply in the long run?

A) In the long run, firms can increase the availability of space and equipment to keep up with the increase in variable inputs.

B) The MPP does not change in the long run.

C) In the long run, firms have enough time to find the most qualified workers.

D) All factors of production are fixed in the long run.

A) In the long run, firms can increase the availability of space and equipment to keep up with the increase in variable inputs.

B) The MPP does not change in the long run.

C) In the long run, firms have enough time to find the most qualified workers.

D) All factors of production are fixed in the long run.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

30

Profit is

A) The difference between total cost and variable cost.

B) The difference between total revenue and total cost.

C) Earned at all points along the production function.

D) Possible only with technical efficiency.

A) The difference between total cost and variable cost.

B) The difference between total revenue and total cost.

C) Earned at all points along the production function.

D) Possible only with technical efficiency.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

31

Which of the following is most likely a fixed cost?

A) Raw materials cost.

B) Labor cost.

C) Energy cost.

D) Property taxes.

A) Raw materials cost.

B) Labor cost.

C) Energy cost.

D) Property taxes.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

32

Which of the following is most likely a fixed cost?

A) The material used to make jackets.

B) The labor on an automotive assembly line.

C) The rent for a factory.

D) The electricity used to run packaging equipment.

A) The material used to make jackets.

B) The labor on an automotive assembly line.

C) The rent for a factory.

D) The electricity used to run packaging equipment.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

33

Marginal cost is equal to

A) The change in total costs divided by the change in quantity produced.

B) The change in fixed costs as more units are produced.

C) Total cost divided by quantity produced.

D) Average total cost multiplied by quantity produced.

A) The change in total costs divided by the change in quantity produced.

B) The change in fixed costs as more units are produced.

C) Total cost divided by quantity produced.

D) Average total cost multiplied by quantity produced.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

34

The most desirable rate of output for a firm is the output that

A) Minimizes total costs.

B) Maximizes total profit.

C) Minimizes marginal costs.

D) Maximizes total revenue.

A) Minimizes total costs.

B) Maximizes total profit.

C) Minimizes marginal costs.

D) Maximizes total revenue.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

35

As an In and Out Burger restaurant increases the number of employees for a specific restaurant,

A) Total production of hamburgers will fall.

B) Costs of production will fall.

C) Efficiency will suffer as the restaurant becomes too crowded with employees.

D) The production function will increase.

A) Total production of hamburgers will fall.

B) Costs of production will fall.

C) Efficiency will suffer as the restaurant becomes too crowded with employees.

D) The production function will increase.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

36

Marginal cost

A) Rises as a direct result of diminishing returns.

B) Falls whenever marginal physical product decreases.

C) Falls in the short run because some resources are fixed.

D) Rises whenever marginal revenue product rises.

A) Rises as a direct result of diminishing returns.

B) Falls whenever marginal physical product decreases.

C) Falls in the short run because some resources are fixed.

D) Rises whenever marginal revenue product rises.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

37

At any given rate of output, the difference between total cost and fixed cost is

A) Marginal cost.

B) Average variable cost.

C) Zero in the short run.

D) Variable cost.

A) Marginal cost.

B) Average variable cost.

C) Zero in the short run.

D) Variable cost.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

38

The shape of the marginal cost curve reflects the

A) Law of diminishing returns.

B) Competitiveness of the firm.

C) Law of diminishing marginal utility.

D) Law of demand.

A) Law of diminishing returns.

B) Competitiveness of the firm.

C) Law of diminishing marginal utility.

D) Law of demand.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

39

An increase in production in the short run definitely results in an increase in

A) Average total costs.

B) Marginal costs.

C) Total costs.

D) Average fixed costs.

A) Average total costs.

B) Marginal costs.

C) Total costs.

D) Average fixed costs.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

40

The sum of fixed cost and variable cost at any rate of output is

A) Total variable cost.

B) Total cost.

C) Average total cost.

D) Average marginal cost.

A) Total variable cost.

B) Total cost.

C) Average total cost.

D) Average marginal cost.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

41

What is the total fixed cost in Figure 21.2?A) $80.

B) $10,000.

C) $9,600.

D) $29,600.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

42

What is the total cost of 120 units in Figure 21.2?A) $34,560.

B) $9,600.

C) $24,960.

D) $10,560.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

43

A U-shaped average total cost curve implies

A) First diminishing returns, and then increasing returns.

B) First marginal cost below average total cost, and then marginal cost above average total cost.

C) That total costs are at a minimum at the minimum of the average cost curve.

D) A linear total cost curve.

A) First diminishing returns, and then increasing returns.

B) First marginal cost below average total cost, and then marginal cost above average total cost.

C) That total costs are at a minimum at the minimum of the average cost curve.

D) A linear total cost curve.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

44

If the marginal cost curve is rising, which of the following must be true?

A) The average total cost curve must be rising.

B) The average total cost curve must be below the marginal cost curve.

C) The average total cost curve must be above the marginal cost curve.

D) Total costs must be rising.

A) The average total cost curve must be rising.

B) The average total cost curve must be below the marginal cost curve.

C) The average total cost curve must be above the marginal cost curve.

D) Total costs must be rising.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

45

The average variable cost curve slopes upward with a higher rate of output in the short run because of

A) The effect of diminishing returns.

B) The shape of the average fixed cost curve.

C) Diseconomies of scale.

D) Implicit but not explicit costs.

A) The effect of diminishing returns.

B) The shape of the average fixed cost curve.

C) Diseconomies of scale.

D) Implicit but not explicit costs.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

46

At what output level do diminishing marginal returns begin in Figure 21.2?A) 40 units.

B) 100 units.

C) 120 units.

D) Only the production function will indicate when diminishing marginal returns begin.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

47

When the average total cost curve is rising, the marginal cost curve will be

A) Below the average fixed cost curve.

B) Falling with greater output.

C) Above the average total cost curve.

D) Below the average total cost curve.

A) Below the average fixed cost curve.

B) Falling with greater output.

C) Above the average total cost curve.

D) Below the average total cost curve.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

48

In the long run, which of the following is likely to be a variable cost?

A) Factory rental but not wage costs.

B) Wage costs but not costs for equipment.

C) Interest payments on borrowed funds but not utilities.

D) Rent, wages, and all other costs are variable in the long run.

A) Factory rental but not wage costs.

B) Wage costs but not costs for equipment.

C) Interest payments on borrowed funds but not utilities.

D) Rent, wages, and all other costs are variable in the long run.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

49

In the short run, when a firm produces zero output, variable cost equals

A) Zero.

B) Total cost.

C) Fixed cost.

D) Marginal cost.

A) Zero.

B) Total cost.

C) Fixed cost.

D) Marginal cost.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

50

The marginal cost curve intersects the minimum of the curve representing

A) TC.

B) ATC.

C) AFC.

D) MPP.

A) TC.

B) ATC.

C) AFC.

D) MPP.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

51

In Figure 21.2, at what output does this firm maximize technical efficiency?A) 0 units.

B) 40 units.

C) 100 units.

D) 120 units.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

52

What is the average fixed cost when output is 120 units in Figure 21.2?A) $0.67.

B) $80.00.

C) $96.00.

D) $208.00.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

53

Sam's surf shop has total costs of $2,000 when it is not producing any surfboards. This means that

A) Variable costs are $2000.

B) Fixed costs are $2,000.

C) The shop is very inefficient in its production.

D) Fixed costs are zero.

A) Variable costs are $2000.

B) Fixed costs are $2,000.

C) The shop is very inefficient in its production.

D) Fixed costs are zero.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

54

What is the total variable cost when output is 100 units in Figure 21.2?A) $9,600.

B) $296.

C) $200.

D) $20,000.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

55

Which of the following is always downward-sloping?

A) The marginal cost curve when it is below the average total cost curve.

B) The marginal cost curve when it is above the average total cost curve.

C) The average total cost curve when it is below the marginal cost curve.

D) The average total cost curve when it is above the marginal cost curve.

A) The marginal cost curve when it is below the average total cost curve.

B) The marginal cost curve when it is above the average total cost curve.

C) The average total cost curve when it is below the marginal cost curve.

D) The average total cost curve when it is above the marginal cost curve.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

56

The average total cost (ATC) curve will be negatively sloped so long as

A) Average variable cost is less than average total cost.

B) Marginal cost is greater than average total cost.

C) Average fixed cost is less than average total cost.

D) Marginal cost is less than average total cost.

A) Average variable cost is less than average total cost.

B) Marginal cost is greater than average total cost.

C) Average fixed cost is less than average total cost.

D) Marginal cost is less than average total cost.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

57

Average total cost is important to a business because

A) It tells the firm what the profit per unit produced is.

B) It always declines as more output is produced.

C) It tells the firm what its fixed costs are.

D) It is an indicator of the production function.

A) It tells the firm what the profit per unit produced is.

B) It always declines as more output is produced.

C) It tells the firm what its fixed costs are.

D) It is an indicator of the production function.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

58

The average fixed cost (AFC) curve

A) Is U-shaped as a result of diminishing returns.

B) Declines as long as output increases.

C) Is intersected at its minimum point by marginal cost.

D) Intersects the marginal cost curve at its minimum point.

A) Is U-shaped as a result of diminishing returns.

B) Declines as long as output increases.

C) Is intersected at its minimum point by marginal cost.

D) Intersects the marginal cost curve at its minimum point.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

59

Refer to Figure 21.3. The vertical difference between the total cost curve and the total fixed cost curve representsA) Total variable costs.

B) Total marginal costs.

C) Average fixed costs.

D) Average variable costs.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

60

What is the marginal cost of the 120th unit of output in Figure 21.2?A) $1.20.

B) $200.00.

C) $208.00.

D) $288.00.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

61

Explicit costs

A) Include only payments to labor.

B) Are the sum of actual monetary payments made for resources used to produce a good.

C) Include the market value of all resources used to produce a good.

D) Are the total value of resources used to produce a good but for which no monetary payment is made.

A) Include only payments to labor.

B) Are the sum of actual monetary payments made for resources used to produce a good.

C) Include the market value of all resources used to produce a good.

D) Are the total value of resources used to produce a good but for which no monetary payment is made.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

62

Economies of scale

A) Exist in both the short run and the long run.

B) Explain why average variable and average total costs decline in the short run.

C) Explain why average total costs decline as output increases in the long run.

D) Explain why average total costs increase as output increases in the long run.

A) Exist in both the short run and the long run.

B) Explain why average variable and average total costs decline in the short run.

C) Explain why average total costs decline as output increases in the long run.

D) Explain why average total costs increase as output increases in the long run.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

63

In economics, the long run is considered to be

A) The time period when all costs are variable.

B) The time period when all costs are explicit.

C) One year.

D) More than two years.

A) The time period when all costs are variable.

B) The time period when all costs are explicit.

C) One year.

D) More than two years.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

64

Economies of scale are reductions in average

A) Total cost that result from declining average fixed costs.

B) Fixed cost that result from reducing the firm's scale of operations.

C) Total cost that result from using operations of larger size.

D) Fixed cost resulting from improved technology and production efficiency.

A) Total cost that result from declining average fixed costs.

B) Fixed cost that result from reducing the firm's scale of operations.

C) Total cost that result from using operations of larger size.

D) Fixed cost resulting from improved technology and production efficiency.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

65

Which of the following statements about the relationship between economic costs and accounting costs is true?

A) Accounting costs are always less than or equal to economic costs.

B) Accounting costs must always equal economic costs.

C) Accounting costs are always greater than economic costs.

D) Accounting costs are equal to or greater than economic costs.

A) Accounting costs are always less than or equal to economic costs.

B) Accounting costs must always equal economic costs.

C) Accounting costs are always greater than economic costs.

D) Accounting costs are equal to or greater than economic costs.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

66

Which of the following is a long-run concept?

A) Diminishing marginal productivity.

B) Diminishing returns.

C) Diseconomies of scale.

D) Fixed costs.

A) Diminishing marginal productivity.

B) Diminishing returns.

C) Diseconomies of scale.

D) Fixed costs.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

67

Assume a given amount of output can be produced by several small plants or one large plant with identical minimum per-unit costs. This long-run situation reflects the existence of

A) Economies of scale.

B) Diseconomies of scale.

C) Constant returns to scale.

D) Diminishing returns.

A) Economies of scale.

B) Diseconomies of scale.

C) Constant returns to scale.

D) Diminishing returns.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

68

The marginal physical product is the difference in total output associated with one additional unit of input, which is 20 (35 - 15).

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

69

Megan used to work at the local pizzeria for $15,000 per year but quit in order to start her own deli. To buy the necessary equipment, she withdrew $20,000 from her inheritance (which paid 8 percent interest). Last year she paid $25,000 for ingredients and $500 per month rent but had revenue of $50,000. She asked her dad the accountant and her mom the economist to calculate her costs for her.

A) Dad says her cost is $9,000 and Mom says her cost is $2,400.

B) Dad says her cost is $31,000 and Mom says her cost is $35,000.

C) Dad says her cost is $25,000 and Mom says her cost is $16,600.

D) Dad says her cost is $31,000 and Mom says her cost is $47,600.

A) Dad says her cost is $9,000 and Mom says her cost is $2,400.

B) Dad says her cost is $31,000 and Mom says her cost is $35,000.

C) Dad says her cost is $25,000 and Mom says her cost is $16,600.

D) Dad says her cost is $31,000 and Mom says her cost is $47,600.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

70

When the size of a factory (and all its associated inputs) doubles and, as a result, output more than doubles,

A) The law of diminishing returns must not apply in the smaller factory.

B) Economies of scale must exist.

C) The short-run ATC curve must be declining.

D) Marginal costs must be declining.

A) The law of diminishing returns must not apply in the smaller factory.

B) Economies of scale must exist.

C) The short-run ATC curve must be declining.

D) Marginal costs must be declining.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

71

Intel's chief executive says the company might expand the technology it is using in its planned $2.5 billion chip-manufacturing factory in China if the U.S. government allows it, underscoring the technology giant's ambitions in the world's fourth-biggest economy. The Intel executive is making a

A) Long-run decision, and therefore an investment decision.

B) Long-run decision, and therefore a production decision.

C) Decision that would definitely increase costs.

D) Decision that would cause ATC to increase.

A) Long-run decision, and therefore an investment decision.

B) Long-run decision, and therefore a production decision.

C) Decision that would definitely increase costs.

D) Decision that would cause ATC to increase.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

72

Implicit costs

A) Include only payments to labor.

B) Are the sum of actual monetary payments made for resources used to produce a good.

C) Include the value of all resources used to produce a good.

D) Are the value of resources used to produce a good but for which no monetary payment is made.

A) Include only payments to labor.

B) Are the sum of actual monetary payments made for resources used to produce a good.

C) Include the value of all resources used to produce a good.

D) Are the value of resources used to produce a good but for which no monetary payment is made.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

73

With which unit of labor do diminishing marginal returns first appear in Table 21.1?A) The first.

B) The second.

C) The third.

D) The fourth.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

74

Accounting costs and economic costs differ because

A) Economic costs include implicit costs and accounting costs do not.

B) Accounting costs include implicit costs and economic costs do not.

C) Economic costs include explicit costs and accounting costs do not.

D) Accounting costs include explicit costs and economic costs do not.

A) Economic costs include implicit costs and accounting costs do not.

B) Accounting costs include implicit costs and economic costs do not.

C) Economic costs include explicit costs and accounting costs do not.

D) Accounting costs include explicit costs and economic costs do not.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

75

If workers are paid $10, what is the labor cost per unit of output in Table 21.1 when output is increased from 15 to 35 units of output?A) $0.28 per unit.

B) $0.50 per unit.

C) $10 per unit.

D) $20 per unit.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

76

Diseconomies of scale are reflected in

A) The downward-sloping segment of the long-run average total cost curve.

B) The downward-sloping segment of the long-run marginal cost curve.

C) A downward shift of the long-run average total cost curve.

D) The upward-sloping segment of the long-run average total cost curve.

A) The downward-sloping segment of the long-run average total cost curve.

B) The downward-sloping segment of the long-run marginal cost curve.

C) A downward shift of the long-run average total cost curve.

D) The upward-sloping segment of the long-run average total cost curve.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

77

Economic cost

A) Includes both implicit and explicit costs.

B) Is the sum of actual monetary payments made for resources used to produce a good.

C) Includes only implicit costs.

D) Decreases as the level of production increases.

A) Includes both implicit and explicit costs.

B) Is the sum of actual monetary payments made for resources used to produce a good.

C) Includes only implicit costs.

D) Decreases as the level of production increases.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

78

The period in which there are no fixed costs is the

A) Production run.

B) Long run.

C) Short run.

D) Implicit run.

A) Production run.

B) Long run.

C) Short run.

D) Implicit run.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

79

The long-run average total cost curve is constructed from the

A) Minimum points of the short-run marginal cost curves.

B) Minimum points of the short-run average variable cost curves.

C) Lowest average total cost for producing each level of output.

D) Minimum points of the long-run marginal cost curves.

A) Minimum points of the short-run marginal cost curves.

B) Minimum points of the short-run average variable cost curves.

C) Lowest average total cost for producing each level of output.

D) Minimum points of the long-run marginal cost curves.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

80

The best estimate of where diminishing marginal returns begin is 20 because that is the output level where the total cost curve begins getting steeper, which means the costs are rising faster as output increases.

Unlock Deck

Unlock for access to all 150 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 150 flashcards in this deck.