Deck 1: Current Liabilities and Contingencies

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Fill in the following chart.

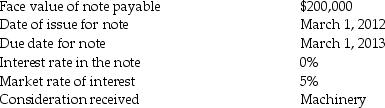

Question

Question

Question

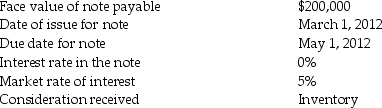

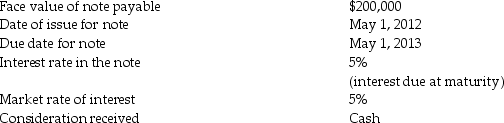

For the following transaction,provide all of the required journal entries from inception to liquidation. Assume a December 31 year end and that the company does not prepare interim statements. Round all amounts to nearest dollar.

Question

Question

For the following transaction,provide all of the required journal entries from inception to liquidation. Assume a December 31 year end and that the company does not prepare interim statements. Round all amounts to nearest dollar.

Question

Question

Question

Question

Question

Question

Question

Question

Fill in the following chart.

Question

Question

Question

Question

Question

Question

Question

On May I,2016,British Columbia Brew Supplies Inc. borrowed USS 180,000 from its bank. British Columbia's year-end is December 31,2016. Exchange rates were as follows:

Requirement:

Requirement:

Prepare the required journal entries to record receipt of the loan proceeds and for any adjustments required at year-end.

Requirement:Prepare the required journal entries to record receipt of the loan proceeds and for any adjustments required at year-end.

Question

Question

Question

Question

Question

Question

Question

Question

Question

For the following transaction,provide all of the required journal entries from inception to liquidation. Assume a December 31 year end and that the company does not prepare interim statements. Round all amounts to nearest dollar.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Consider the following independent situations. The underlined entity is the reporting entity.

1. The Supreme Court of Canada ordered a supplier to pay Towna Haring Inc. $500,000 for breach of contract.

2. Iwas Pharmaceuticals Inc. sued Game Day Agencies Ltd. for $8 million alleging patent infringement. While there may be some substance to Iwas's assertion,Game Day's legal counsel estimates that Iwas's likelihood of success is about 30%.

3. Environment Canada sued Foil Fan Isotopes Ltd. for $18 million seeking to recover the costs of cleaning up Foil Fan's accidental discharge of radioactive materials. Foil Fan acknowledges liability but is disputing the amount,claiming that the actual costs are in the range of$9 million to $12 million. Foil Fan's $18 million environmental insurance policy includes a $6 million deductible clause.

Requirement:

a. For each of the situations,indicate whether the appropriate accounting treatment is to:

b. For each situation that requires the recognition of an asset or liability,record the journal entry.

b. For each situation that requires the recognition of an asset or liability,record the journal entry.

1. The Supreme Court of Canada ordered a supplier to pay Towna Haring Inc. $500,000 for breach of contract.

2. Iwas Pharmaceuticals Inc. sued Game Day Agencies Ltd. for $8 million alleging patent infringement. While there may be some substance to Iwas's assertion,Game Day's legal counsel estimates that Iwas's likelihood of success is about 30%.

3. Environment Canada sued Foil Fan Isotopes Ltd. for $18 million seeking to recover the costs of cleaning up Foil Fan's accidental discharge of radioactive materials. Foil Fan acknowledges liability but is disputing the amount,claiming that the actual costs are in the range of$9 million to $12 million. Foil Fan's $18 million environmental insurance policy includes a $6 million deductible clause.

Requirement:

a. For each of the situations,indicate whether the appropriate accounting treatment is to:

b. For each situation that requires the recognition of an asset or liability,record the journal entry. Question

Question

Question

Question

LMZ Computer Systems Inc. maintains office equipment under contract. The contracts are for labour only; customers must reimburse LMZ for parts. LMZ's rate schedule follows:

LMZ's 2018 sales of maintenance agreements is set out below:

LMZ's 2018 sales of maintenance agreements is set out below:

Requirements:

Requirements:

Assuming that sales occurred evenly through the year:

a. What amount of revenue will LMZ recognize for the year ended December 31,2018?

b. What amount of deferred revenue will LMZ report as a current liability on December 31,2018?

c. What amount of deferred revenue will LMZ report as a non-current liability on December 31,2018?

LMZ's 2018 sales of maintenance agreements is set out below: Requirements:Assuming that sales occurred evenly through the year:

a. What amount of revenue will LMZ recognize for the year ended December 31,2018?

b. What amount of deferred revenue will LMZ report as a current liability on December 31,2018?

c. What amount of deferred revenue will LMZ report as a non-current liability on December 31,2018?

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/90

Play

Full screen (f)

Deck 1: Current Liabilities and Contingencies

1

Which is a non-current liability?

A)HST payable.

B)45 day accounts payable.

C)Five year loan that matures four months after year end reporting date.

D)The creditor has granted a 15-month grace period on a loan in default.

A)HST payable.

B)45 day accounts payable.

C)Five year loan that matures four months after year end reporting date.

D)The creditor has granted a 15-month grace period on a loan in default.

D

2

Which statement about liabilities is not correct?

A)Current liabilities are those that can be settled within one year.

B)Current liabilities are those that can be settled within one operating cycle.

C)Current liabilities are normally presented together with non-current liabilities.

D)Certain held for trading liabilities can also be reported as current liabilities.

A)Current liabilities are those that can be settled within one year.

B)Current liabilities are those that can be settled within one operating cycle.

C)Current liabilities are normally presented together with non-current liabilities.

D)Certain held for trading liabilities can also be reported as current liabilities.

C

3

Which of the following characteristic is required for a "liability" under IFRS Framework?

A)Expected to result in the inflow of economic benefits.

B)Expected to result in the inflow of economic benefits that are measurable.

C)Expected to result in the outflow of economic benefits.

D)Expected to result in the outflow of economic benefits that are virtually certain.

A)Expected to result in the inflow of economic benefits.

B)Expected to result in the inflow of economic benefits that are measurable.

C)Expected to result in the outflow of economic benefits.

D)Expected to result in the outflow of economic benefits that are virtually certain.

C

4

Which of the following is not correct?

A)Financial liabilities held for trading are initially measured at fair value.

B)Other financial liabilities are subsequently measured at amortized cost.

C)Financial and non-financial liabilities are measured at fair value.

D)Non-financial liabilities are measured at management's best estimates.

A)Financial liabilities held for trading are initially measured at fair value.

B)Other financial liabilities are subsequently measured at amortized cost.

C)Financial and non-financial liabilities are measured at fair value.

D)Non-financial liabilities are measured at management's best estimates.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

5

Explain the meaning of "provision" and give an example.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

6

Which is not a current liability?

A)Accounts payable due in 120 days.

B)Bank loan due in three years that is in default.

C)Bonds payable maturing in five years.

D)Certain held for trading liabilities.

A)Accounts payable due in 120 days.

B)Bank loan due in three years that is in default.

C)Bonds payable maturing in five years.

D)Certain held for trading liabilities.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

7

Which statement is correct under the IFRS definition for a "liability"?

A)The obligating event must be probable before the liability can be recognized.

B)The obligating event must be virtually certain before the liability can be recognized.

C)A reliable measure of the obligation must exist before the liability can be recognized.

D)A precise measure of the obligation must exist before the liability can be recognized.

A)The obligating event must be probable before the liability can be recognized.

B)The obligating event must be virtually certain before the liability can be recognized.

C)A reliable measure of the obligation must exist before the liability can be recognized.

D)A precise measure of the obligation must exist before the liability can be recognized.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

8

Which of the following characteristic is required for a "liability" under IFRS Framework?

A)Arises from a past transaction.

B)Arises from a non-financial transaction.

C)Arises from a future transaction.

D)Arises from a forecasted transaction.

A)Arises from a past transaction.

B)Arises from a non-financial transaction.

C)Arises from a future transaction.

D)Arises from a forecasted transaction.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

9

Which statement is not correct?

A)A bank loan due in 5 years is a non-financial liability.

B)Bonds payable are financial liabilities.

C)Sales taxes payable are non-financial liabilities.

D)A bank loan due in 90 days is a financial liability.

A)A bank loan due in 5 years is a non-financial liability.

B)Bonds payable are financial liabilities.

C)Sales taxes payable are non-financial liabilities.

D)A bank loan due in 90 days is a financial liability.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

10

Which is not an example of a non-financial liability?

A)Warranty liability.

B)Bank loan.

C)Income taxes payable.

D)Deferred revenue.

A)Warranty liability.

B)Bank loan.

C)Income taxes payable.

D)Deferred revenue.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

11

Which is not an example of a financial liability?

A)Payment to supplier for raw material received.

B)Obligation to repay a US dollar bank loan.

C)Obligation under a finance lease.

D)Obligation under a customer loyalty program.

A)Payment to supplier for raw material received.

B)Obligation to repay a US dollar bank loan.

C)Obligation under a finance lease.

D)Obligation under a customer loyalty program.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

12

Which of the following is correct about a "liability" under IFRS Framework?

A)a future obligation arising from current events,the settlement of which is expected to result in an outflow of resources

B)a present obligation arising from current events,the settlement of which is expected to result in an outflow of resources

C)a future obligation arising from past events,the settlement of which is expected to result in an outflow of resources

D)a present obligation arising from past events,the settlement of which is expected to result in an outflow of resources

A)a future obligation arising from current events,the settlement of which is expected to result in an outflow of resources

B)a present obligation arising from current events,the settlement of which is expected to result in an outflow of resources

C)a future obligation arising from past events,the settlement of which is expected to result in an outflow of resources

D)a present obligation arising from past events,the settlement of which is expected to result in an outflow of resources

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

13

Explain some of the challenges that exist in determining the amount of a "liability" and factors that influence the value of the indebtedness.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

14

Which statement is correct about financial and non-financial liabilities?

A)A non-financial liability is a contractual obligation to deliver cash to another party.

B)A non-financial liability does not meet all of the criteria for a "liability."

C)The two liabilities are valued differently for financial reporting purposes.

D)A non-financial liability is measured at fair value rather than amortized cost.

A)A non-financial liability is a contractual obligation to deliver cash to another party.

B)A non-financial liability does not meet all of the criteria for a "liability."

C)The two liabilities are valued differently for financial reporting purposes.

D)A non-financial liability is measured at fair value rather than amortized cost.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

15

Which statement is not correct under the IFRS Framework?

A)A reliable estimate for an asset is presumed to exist.

B)A provision exists if the timing of payment is uncertain.

C)A provision exists if the amount of payment is uncertain.

D)A reliable estimate for a liability is presumed to exist.

A)A reliable estimate for an asset is presumed to exist.

B)A provision exists if the timing of payment is uncertain.

C)A provision exists if the amount of payment is uncertain.

D)A reliable estimate for a liability is presumed to exist.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

16

Which statement is correct?

A)HST payable is a financial liability.

B)Bank overdraft is a non-financial liability.

C)Unearned revenue is a non-financial liability.

D)Unearned subscriptions are a financial liability.

A)HST payable is a financial liability.

B)Bank overdraft is a non-financial liability.

C)Unearned revenue is a non-financial liability.

D)Unearned subscriptions are a financial liability.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

17

Which of the following characteristic is required for a "liability" under IFRS Framework?

A)A past obligation.

B)A present obligation.

C)An unknown obligation.

D)A future obligation.

A)A past obligation.

B)A present obligation.

C)An unknown obligation.

D)A future obligation.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

18

What are "liabilities"? Differentiate between financial liabilities and nonfinancial liabilities.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

19

Which is an example of a liability?

A)The decision to borrow $150,000 from the ABC Bank on January 15,2012.

B)Withdrawing $10,000 from the operating line of credit on January 15,2012.

C)Selecting the supplier to provide the raw materials for the manufacturing process.

D)Choosing the site for a future plant expansion from a list of several possible choices.

A)The decision to borrow $150,000 from the ABC Bank on January 15,2012.

B)Withdrawing $10,000 from the operating line of credit on January 15,2012.

C)Selecting the supplier to provide the raw materials for the manufacturing process.

D)Choosing the site for a future plant expansion from a list of several possible choices.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

20

Which of the following is correct about a "liability" under IFRS Framework?

A)A future obligation arising from past events,the settlement of which is expected to result in an inflow of resources.

B)A present obligation arising from past events,the settlement of which is expected to result in an inflow of resources.

C)A past obligation arising from past events,the settlement of which is expected to result in an outflow of resources.

D)A present obligation arising from past events,the settlement of which is expected to result in an outflow of resources.

A)A future obligation arising from past events,the settlement of which is expected to result in an inflow of resources.

B)A present obligation arising from past events,the settlement of which is expected to result in an inflow of resources.

C)A past obligation arising from past events,the settlement of which is expected to result in an outflow of resources.

D)A present obligation arising from past events,the settlement of which is expected to result in an outflow of resources.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

21

Which statement is correct?

A)Contingencies arise from future events.

B)Financial guarantees arise from contracts previously entered into.

C)Current liabilities arise from future events.

D)The amount to be paid for financial guarantees is known or reasonably estimable.

A)Contingencies arise from future events.

B)Financial guarantees arise from contracts previously entered into.

C)Current liabilities arise from future events.

D)The amount to be paid for financial guarantees is known or reasonably estimable.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

22

For a $200,000 trade payable with terms of 2/15,net 50,how much would be reported as "purchase discount lost" under the net method if a payment was made after 60 days?

A)$0

B)$4,000

C)$5,000

D)$30,000

A)$0

B)$4,000

C)$5,000

D)$30,000

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

23

Which is a reason to use the net method to record purchase discounts?

A)Cost-benefit factor is greater for the net method.

B)Reporting "purchase discounts lost" signifies inefficient business practices.

C)Given the materiality of the amounts involved,the net method is used.

D)The net method is technically superior to the gross method.

A)Cost-benefit factor is greater for the net method.

B)Reporting "purchase discounts lost" signifies inefficient business practices.

C)Given the materiality of the amounts involved,the net method is used.

D)The net method is technically superior to the gross method.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

24

Which statement is correct?

A)Supplier discounts can only be accounted for by using the gross method.

B)The amount owing for trade payables is generally not known with a high degree of certainty.

C)An accrued liability is needed when a company has received goods,but not the invoice.

D)Completeness means that obligations are reported in the proper accounting period.

A)Supplier discounts can only be accounted for by using the gross method.

B)The amount owing for trade payables is generally not known with a high degree of certainty.

C)An accrued liability is needed when a company has received goods,but not the invoice.

D)Completeness means that obligations are reported in the proper accounting period.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

25

Explain the meaning of the following terms: current assets,trade payables,expected value,deferred revenue and warranty.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

26

Fill in the following chart.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

27

For a $100,000 trade payable with terms of 2/10,net 45,how much would be reported as "purchase discount lost" under the gross method if a payment was made after 60 days?

A)$0

B)$2,000

C)$4,500

D)$10,000

A)$0

B)$2,000

C)$4,500

D)$10,000

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

28

Which statement is not correct?

A)"Purchase discount lost" is reported if the gross method is used.

B)Cut off means that obligations are reported in the proper accounting period.

C)Supplier discounts can be accounted for by using the gross method.

D)Trade payables are obligations for goods received or services used.

A)"Purchase discount lost" is reported if the gross method is used.

B)Cut off means that obligations are reported in the proper accounting period.

C)Supplier discounts can be accounted for by using the gross method.

D)Trade payables are obligations for goods received or services used.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

29

For the following transaction,provide all of the required journal entries from inception to liquidation. Assume a December 31 year end and that the company does not prepare interim statements. Round all amounts to nearest dollar.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

30

Which statement is not correct?

A)The amount to be paid for contingencies is determined by future events.

B)The amount to be paid for current liabilities is determined by future events.

C)The amount to be paid for financial guarantees is determined by future events.

D)The amount to be paid for current liabilities is known or reasonably estimable.

A)The amount to be paid for contingencies is determined by future events.

B)The amount to be paid for current liabilities is determined by future events.

C)The amount to be paid for financial guarantees is determined by future events.

D)The amount to be paid for current liabilities is known or reasonably estimable.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

31

For the following transaction,provide all of the required journal entries from inception to liquidation. Assume a December 31 year end and that the company does not prepare interim statements. Round all amounts to nearest dollar.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

32

Which statement is not correct?

A)Contingencies arise from past events.

B)Financial guarantees arise from contracts previously entered into.

C)The amount to be paid for financial guarantees is known or reasonably estimable.

D)The amount to be paid for current liabilities is known or reasonably estimable.

A)Contingencies arise from past events.

B)Financial guarantees arise from contracts previously entered into.

C)The amount to be paid for financial guarantees is known or reasonably estimable.

D)The amount to be paid for current liabilities is known or reasonably estimable.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

33

Which statement is not correct?

A)Contingencies arise from future events.

B)The amount to be paid for contingencies is determined by future events.

C)Current liabilities arise from past events.

D)The amount to be paid for current liabilities is known or reasonably estimable.

A)Contingencies arise from future events.

B)The amount to be paid for contingencies is determined by future events.

C)Current liabilities arise from past events.

D)The amount to be paid for current liabilities is known or reasonably estimable.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

34

Which statement is correct?

A)Contingencies arise from future events.

B)The amount to be paid for contingencies is known or reasonably estimable.

C)Current liabilities arise from future events.

D)The amount to be paid for current liabilities is known or reasonably estimable.

A)Contingencies arise from future events.

B)The amount to be paid for contingencies is known or reasonably estimable.

C)Current liabilities arise from future events.

D)The amount to be paid for current liabilities is known or reasonably estimable.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

35

Which statement is correct?

A)Trade payables are supported by a written promise to pay.

B)Trade payables with no stated interest rate do not need to be discounted.

C)Notes payable are legally enforceable and can only be interest bearing.

D)Notes payables are recognized at the face value or transaction price.

A)Trade payables are supported by a written promise to pay.

B)Trade payables with no stated interest rate do not need to be discounted.

C)Notes payable are legally enforceable and can only be interest bearing.

D)Notes payables are recognized at the face value or transaction price.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

36

Which statement is not correct about notes payable?

A)Notes payable are supported by a written promise to pay.

B)Non-interest bearing notes are recognized at their fair value.

C)Non-interest bearing notes are recognized at the transaction price.

D)Fair value can be estimated by using discounted cash flow.

A)Notes payable are supported by a written promise to pay.

B)Non-interest bearing notes are recognized at their fair value.

C)Non-interest bearing notes are recognized at the transaction price.

D)Fair value can be estimated by using discounted cash flow.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

37

What are the three broad categories of liabilities?

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

38

How are "purchase discounts lost" reported in the financial statements?

A)As a reduction of sales.

B)As an increase in liability.

C)As an increase in inventory.

D)As an expense item.

A)As a reduction of sales.

B)As an increase in liability.

C)As an increase in inventory.

D)As an expense item.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

39

Fill in the following chart.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

40

Explain the nature of current liabilities and how these are accounted for in the financial statements.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

41

A company,using a perpetual inventory system,sells goods on credit for $10,000. The applicable PST rate is 5% and the GST rate is 10%. The cost of goods sold was $6,000. Sales taxes are remitted on a monthly basis. Prepare the necessary journal entries for this transaction.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

42

Select transactions and other information pertaining to the Best Place in the World Inc. (BPW)are detailed below.

Facts:

a. BPW is domiciled in Vancouver,British Columbia and all purchases and sales are made in BC.

b. The HST rate in British Columbia is 12%.

c. The balances in BPWs HST recoverable account and HST payable account as at March 31,2012 were $7,000 and $18,000,respectively.

d. BPW uses a perpetual inventory system.

e. Inventory is sold at a 100% mark-up on cost. (Cost of goods sold is 50% of the sales price.)

Select transactions in April 2012:

1. BPW purchased inventory on account at a cost of $17,000 plus HST.

2. BPW purchased equipment on account at a cost of $18,000 plus HST. It paid an additional $600 plus HST for shipping.

3. Cash sales-BPW sold inventory for $45,000 plus HST.

4. Sales on account-BPW sold inventory for $35,000 plus HST.

5. BPW paid the supplier in full for the equipment previously purchased on account.

6. At the end of the month,BPW remitted the net amount of HST owing to the Canada Revenue Agency.

Requirement:

Prepare summary journal entries to record the transactions detailed above.

Facts:

a. BPW is domiciled in Vancouver,British Columbia and all purchases and sales are made in BC.

b. The HST rate in British Columbia is 12%.

c. The balances in BPWs HST recoverable account and HST payable account as at March 31,2012 were $7,000 and $18,000,respectively.

d. BPW uses a perpetual inventory system.

e. Inventory is sold at a 100% mark-up on cost. (Cost of goods sold is 50% of the sales price.)

Select transactions in April 2012:

1. BPW purchased inventory on account at a cost of $17,000 plus HST.

2. BPW purchased equipment on account at a cost of $18,000 plus HST. It paid an additional $600 plus HST for shipping.

3. Cash sales-BPW sold inventory for $45,000 plus HST.

4. Sales on account-BPW sold inventory for $35,000 plus HST.

5. BPW paid the supplier in full for the equipment previously purchased on account.

6. At the end of the month,BPW remitted the net amount of HST owing to the Canada Revenue Agency.

Requirement:

Prepare summary journal entries to record the transactions detailed above.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

43

A company purchased inventory from Europe valued at $100,000 euros. The spot rate at the transaction date was C$1.00 = 0.85 Euro. The spot rate on year end date was C$1.00 = 0.80 Euro. When the company paid the supplier 3 months after year end the spot rate was C$1.00 = 0.90 Euro.

Provide all necessary journal entries. Round all amounts to nearest dollar.

Provide all necessary journal entries. Round all amounts to nearest dollar.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

44

AV Airlines sold a ticket on May 1,2012 for travel on Jun 15,2012 for $1,500. The customer paid at time of booking the flight. Provide the necessary journal entries.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

45

Which statement about sales taxes is correct?

A)The consumer is responsible for remitting the tax to the government.

B)Taxes are uniformly applied to all sale transactions.

C)Businesses can deduct the GST paid from GST collected.

D)The same products that are exempt from GST are exempt from PST.

A)The consumer is responsible for remitting the tax to the government.

B)Taxes are uniformly applied to all sale transactions.

C)Businesses can deduct the GST paid from GST collected.

D)The same products that are exempt from GST are exempt from PST.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

46

On May I,2016,British Columbia Brew Supplies Inc. borrowed USS 180,000 from its bank. British Columbia's year-end is December 31,2016. Exchange rates were as follows:

Requirement:

Prepare the required journal entries to record receipt of the loan proceeds and for any adjustments required at year-end.

Requirement:Prepare the required journal entries to record receipt of the loan proceeds and for any adjustments required at year-end.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

47

Which statement about deferred revenue is correct?

A)Deferred revenue is always a non-current liability.

B)Deferred revenue could arise from loyalty programs.

C)Deferred revenue is measured using expected values.

D)Deferred revenue arises when the goods are shipped.

A)Deferred revenue is always a non-current liability.

B)Deferred revenue could arise from loyalty programs.

C)Deferred revenue is measured using expected values.

D)Deferred revenue arises when the goods are shipped.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

48

A clothing store maintains a loyalty program for its customers. Members receive points for every purchase which do not expire. In fiscal 2012,the store made sales of $1 million and awarded 50,000 points that have a fair value of $50,000. The company estimates that approximately 75% of these points will be redeemed by members. Members redeemed 10,000 points in fiscal 2013.

Provide the necessary journal entries for fiscal 2012 and 2013.

Provide the necessary journal entries for fiscal 2012 and 2013.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

49

In 2017,Johnson's Cycles Inc. sold 5,000 mountain bikes. For the first time,Johnson offered an in-store,no-charge,two-year warranty on each bike sold. Company management estimates that the average cost of providing the warranty is $8 per unit in the first year of coverage and $11 per unit in the second year.

Johnson's warranty-related expenditures totaled $36,500 for labor costs during 2017.

Requirements:

a. Prepare the summary journal entry to recognize Johnson's warranty expense in 2017.

b. Prepare the summary journal entry to recognize the warranty service provided in 2017.

c. Determine the total provision for warranty obligations that will be reported on the company's balance sheet at year-end. Assuming that all sales transactions and warranty service took place on the last day of the year,how much of the warranty obligation will be classified as a current liability? As a non-current liability?

Johnson's warranty-related expenditures totaled $36,500 for labor costs during 2017.

Requirements:

a. Prepare the summary journal entry to recognize Johnson's warranty expense in 2017.

b. Prepare the summary journal entry to recognize the warranty service provided in 2017.

c. Determine the total provision for warranty obligations that will be reported on the company's balance sheet at year-end. Assuming that all sales transactions and warranty service took place on the last day of the year,how much of the warranty obligation will be classified as a current liability? As a non-current liability?

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

50

A company purchases inventory on credit for $40,000. Inventory costing $30,000 is sold on credit for $50,000. The applicable HST rate is 10%. Sales taxes are remitted on a monthly basis. Prepare the necessary journal entries for this transaction.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

51

Which statement about warranties is correct?

A)Warranties sold separately are accounted for under IAS37.

B)Warranties sold separately are accounted for under IAS18.

C)Warranties are financial liabilities and accounted for at fair value.

D)Expected value uses a weighted average of possible outcomes.

A)Warranties sold separately are accounted for under IAS37.

B)Warranties sold separately are accounted for under IAS18.

C)Warranties are financial liabilities and accounted for at fair value.

D)Expected value uses a weighted average of possible outcomes.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

52

Which statement about warranties is correct?

A)Warranties are provisions.

B)Warranties included with the product sold are accounted for under IAS18.

C)Warranties are financial liabilities.

D)Warranties included with the product sold are accounted for under IAS39.

A)Warranties are provisions.

B)Warranties included with the product sold are accounted for under IAS18.

C)Warranties are financial liabilities.

D)Warranties included with the product sold are accounted for under IAS39.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

53

A company purchases inventory on credit for $80,000. Inventory costing $30,000 is sold on credit for $40,000. The applicable HST rate is 10%. Sales taxes are remitted on a monthly basis. Prepare the necessary journal entries for this transaction.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

54

A company,using a perpetual inventory system,sells goods on credit for $10,000. The applicable PST rate is 5% and the cost of goods sold was $6,000. Sales taxes are remitted on a monthly basis. Prepare the necessary journal entries for this transaction.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

55

For the following transaction,provide all of the required journal entries from inception to liquidation. Assume a December 31 year end and that the company does not prepare interim statements. Round all amounts to nearest dollar.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

56

Sales made in fiscal 2012 for $50,000,000 include a 5 year warranty coverage. The estimated cost for warranty is expected to be 2% for the first 4 years and 5% for the last year. Determine how much warranty expense will be recorded in fiscal 2012.

A)1,000,000

B)4,000,000

C)5,000,000

D)6,500,000

A)1,000,000

B)4,000,000

C)5,000,000

D)6,500,000

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

57

A company,using a perpetual inventory system,sells goods on credit for $10,000. The applicable HST rate is 10%. The cost of goods sold was $6,000. Sales taxes are remitted on a monthly basis. Prepare the necessary journal entries for this transaction.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

58

Which statement about deferred revenue is correct?

A)Deferred revenue is a financial liability.

B)Deferred revenue is a non-financial liability.

C)Deferred revenue is a held for trading financial liability.

D)Deferred revenue arises when the contract is signed.

A)Deferred revenue is a financial liability.

B)Deferred revenue is a non-financial liability.

C)Deferred revenue is a held for trading financial liability.

D)Deferred revenue arises when the contract is signed.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

59

Deck Contractors Inc. (DC)enters into a contract to construct six decks adjacent to a commercial building. The purchaser has agreed to pay $8,500 for each deck (total $51,000). The terms of the contract call for a 40% deposit ($3,400 per deck)at time of contract signing and payment of the balance ($5,100 per deck)as each deck is completed.

The contract is signed on October 1,2014. Two decks are completed in 2014 and the balance in 2015. DC has a December 31 year-end. The cost to DC of constructing each deck is $3,400,which it pays in cash.

Requirements:

a. Prepare summary journal entries for 2014 and 2015.

b. What is the balance in the deferred revenue account as at December 31,2014?

The contract is signed on October 1,2014. Two decks are completed in 2014 and the balance in 2015. DC has a December 31 year-end. The cost to DC of constructing each deck is $3,400,which it pays in cash.

Requirements:

a. Prepare summary journal entries for 2014 and 2015.

b. What is the balance in the deferred revenue account as at December 31,2014?

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

60

Which statement about sales taxes is correct?

A)Businesses can recover the PST paid on all of their purchases.

B)Goods purchased for resale are exempt from PST.

C)Businesses remit only the GST collected on sales transactions.

D)The same products that are exempt from HST are exempt from PST.

A)Businesses can recover the PST paid on all of their purchases.

B)Goods purchased for resale are exempt from PST.

C)Businesses remit only the GST collected on sales transactions.

D)The same products that are exempt from HST are exempt from PST.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

61

On January 1,2014 BCL Transmission Services Co. issued a $40,000,non-interest bearing note,due on January 1,2015,in exchange for a custom-built computer system. The fair value of the computer system is not easily determinable. The market rate of interest for similar transactions is 4%. BCL's year-end is December 31.

Requirements:

a. Prepare the journal entry to record the issuance of the note payable.

b. Prepare the journal entry to record the accrual of interest at December 31,2014,assuming that BCL prepares adjusting entries only at year-end.

c. Prepare the journal entry to record the retirement of the note payable on January 1,2015.

Requirements:

a. Prepare the journal entry to record the issuance of the note payable.

b. Prepare the journal entry to record the accrual of interest at December 31,2014,assuming that BCL prepares adjusting entries only at year-end.

c. Prepare the journal entry to record the retirement of the note payable on January 1,2015.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

62

Explain the difference between "probable," "possible," and "remote" under IFRS.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

63

Which statement about contingencies is correct?

A)If the future outcome is possible and reliably measurable,a provision is recorded.

B)If the future outcome is probable and reliably measurable,a provision is recorded.

C)If the future outcome is probable,a provision is recorded even if it is not reliably measurable.

D)If the future outcome is possible,a provision is recorded even if it is not reliably measurable.

A)If the future outcome is possible and reliably measurable,a provision is recorded.

B)If the future outcome is probable and reliably measurable,a provision is recorded.

C)If the future outcome is probable,a provision is recorded even if it is not reliably measurable.

D)If the future outcome is possible,a provision is recorded even if it is not reliably measurable.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

64

It is early in February 2017 and you are conducting the audit of Blast Off Airline's 2016 financial statements. Through discussion with Blast Off's Chief Financial Officer you learn of matters that have not yet been incorporated into the 2016 financial statements:

In July 2016,127 passengers on board Blast Off Airlines Flight 007 were seriously injured when the plane missed the runway on final approach. In January 2017,the injured passengers launched a class action lawsuit against Blast Off seeking damages of $15 million. Blast Off's internal investigation of the incident determined that the pilot was intoxicated during the flight. The company's solicitors suggest that if the matter goes to court,Blast Off will be found liable and ordered to pay the $15 million.

In an attempt to reduce its loss,Blast Off's solicitors made a settlement offer of $10 million to the plaintiffs. The litigants' attorney has not provided a formal response but has indicated that the offer is being seriously considered. Blast Off's lawyers estimate that there is a 90% probability the plaintiffs will accept the offer.

Requirement:

Prepare the journal entries to record the required adjustments for the above event.

In July 2016,127 passengers on board Blast Off Airlines Flight 007 were seriously injured when the plane missed the runway on final approach. In January 2017,the injured passengers launched a class action lawsuit against Blast Off seeking damages of $15 million. Blast Off's internal investigation of the incident determined that the pilot was intoxicated during the flight. The company's solicitors suggest that if the matter goes to court,Blast Off will be found liable and ordered to pay the $15 million.

In an attempt to reduce its loss,Blast Off's solicitors made a settlement offer of $10 million to the plaintiffs. The litigants' attorney has not provided a formal response but has indicated that the offer is being seriously considered. Blast Off's lawyers estimate that there is a 90% probability the plaintiffs will accept the offer.

Requirement:

Prepare the journal entries to record the required adjustments for the above event.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

65

Which statement about contingencies is correct?

A)If the future outcome is possible and reliably measurable,a provision is recorded.

B)If the future outcome is possible,but reliably measurable,no action is required.

C)If the future outcome is possible,but not reliably measurable,no action is required.

D)If the future outcome is possible,but reliably measurable,disclosure is required.

A)If the future outcome is possible and reliably measurable,a provision is recorded.

B)If the future outcome is possible,but reliably measurable,no action is required.

C)If the future outcome is possible,but not reliably measurable,no action is required.

D)If the future outcome is possible,but reliably measurable,disclosure is required.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

66

Which statement about contingent assets is correct?

A)It involves only potential economic outflows of resources.

B)It is a possible asset that depends upon the outcome of a future event.

C)It involves uncertainty about either the timing or amount of payment.

D)It is a condition that depends upon the outcome of a forecasted event.

A)It involves only potential economic outflows of resources.

B)It is a possible asset that depends upon the outcome of a future event.

C)It involves uncertainty about either the timing or amount of payment.

D)It is a condition that depends upon the outcome of a forecasted event.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

67

St. John Laurulry (SJL)recently hired Huck as its payable clerk,a position that has been vacant for two months. While the other accounting staff have taken care of the "must do's," there are a number of transactions that have not yet been recorded.

• Nov. 15,2017-SJL purchases $8,000 supplies inventory on account. The terms offered are 2/10,net 30.

• Nov. 22,2017-SJL purchases 10 washing machines. SJL issues a $3,000 non-interest bearing note payable due on 01/15/18.

• Nov. 28,2017-SJL borrows $131,400 from the bank. SJL signs a demand note for this amount and authorizes the bank to take the interest payments from its bank account. Interest is payable monthly at 10% per annum.

• Dec. 18,2017-SJL purchases $1,000 supplies inventory on account. The terms offered are 2/10,net 30.

• Dec. 21,2017-SJL purchases 15 dryers. SJL issues a $25,000 non-interest bearing note payable due on Dec. 21,2018.

• Dec. 22,2017-Huck pays the Nov. 15,2017 and Dec. 18,2017 invoices.

• Dec. 31,2017-Huck processes the payroll for the month. The gross payroll is $80,000; $2,700 is withheld for the employees' Canada Pension Plan and Employment Insurance premiums.

Other Info

• SJL uses the net method to record accounts payable.

• SJL's year-end is Dec. 31 and interim statements are normally prepared on a monthly basis.

• Due to the vacancy in the accounting department,SJL's latest interim statements are for the period ended Oct. 31,2017. The necessary accruals were made at that time.

• The market rate of interest for SJL's short-term borrowings is 10%.

Requirements:

a. Prepare journal entries to record the documented events and the necessary accruals for the months of November and December. Compute interest accruals based on the number of days,rather than months.

b. Contrast the gross and net methods of accounting for trade payables.

• Nov. 15,2017-SJL purchases $8,000 supplies inventory on account. The terms offered are 2/10,net 30.

• Nov. 22,2017-SJL purchases 10 washing machines. SJL issues a $3,000 non-interest bearing note payable due on 01/15/18.

• Nov. 28,2017-SJL borrows $131,400 from the bank. SJL signs a demand note for this amount and authorizes the bank to take the interest payments from its bank account. Interest is payable monthly at 10% per annum.

• Dec. 18,2017-SJL purchases $1,000 supplies inventory on account. The terms offered are 2/10,net 30.

• Dec. 21,2017-SJL purchases 15 dryers. SJL issues a $25,000 non-interest bearing note payable due on Dec. 21,2018.

• Dec. 22,2017-Huck pays the Nov. 15,2017 and Dec. 18,2017 invoices.

• Dec. 31,2017-Huck processes the payroll for the month. The gross payroll is $80,000; $2,700 is withheld for the employees' Canada Pension Plan and Employment Insurance premiums.

Other Info

• SJL uses the net method to record accounts payable.

• SJL's year-end is Dec. 31 and interim statements are normally prepared on a monthly basis.

• Due to the vacancy in the accounting department,SJL's latest interim statements are for the period ended Oct. 31,2017. The necessary accruals were made at that time.

• The market rate of interest for SJL's short-term borrowings is 10%.

Requirements:

a. Prepare journal entries to record the documented events and the necessary accruals for the months of November and December. Compute interest accruals based on the number of days,rather than months.

b. Contrast the gross and net methods of accounting for trade payables.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

68

It is early in February 2017 and you are conducting the audit of Blast Off Airline's 2016 financial statements. Through discussion with Blast Off's Chief Financial Officer you learn of matters that have not yet been incorporated into the 2016 financial statements:

During 2016,Blast Off began a customer loyalty program. For each aeronautical mile that a passenger travels on a paid flight,the passenger accrues one flight mile. Passengers can redeem accrued flight miles for free air travel. Earned miles do not expire. Blast Off's analysis of its competitors' programs suggests an average redemption rate of 55%. In 2016,Blast Off awarded 50,000,000 flight miles,1,375,000 of which were redeemed. Management estimates the fair value of the flight miles is $540,000.

Requirement:

Prepare the journal entries to record the required adjustments for the above event.

During 2016,Blast Off began a customer loyalty program. For each aeronautical mile that a passenger travels on a paid flight,the passenger accrues one flight mile. Passengers can redeem accrued flight miles for free air travel. Earned miles do not expire. Blast Off's analysis of its competitors' programs suggests an average redemption rate of 55%. In 2016,Blast Off awarded 50,000,000 flight miles,1,375,000 of which were redeemed. Management estimates the fair value of the flight miles is $540,000.

Requirement:

Prepare the journal entries to record the required adjustments for the above event.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

69

GOT Jetski Corp. has sold motorized watercraft for a number of years. GOT includes a three-year warranty on each watercraft they sell. Management estimates that the cost of providing the warranty coverage is 2% of sales in the first year and 3% of sales in each of years two and three. Other facts follow:

• GGT reported a $270,000 provision for warranty payable on its December 31,2012 balance sheet.

• GGT's sales for 2013 totalled $6,000,000 spread evenly through the year.

• The cost to GGT of meeting their warranty claims in 2013 was $480,000; $300,000 for parts and $180,000 for labour.

• GGT's sales for 2014 totalled $6,200,000 spread evenly through the year.

• The cost to GGT of meeting their warranty claims in 2014 was $468,000; $280,800 for parts and $187,200 for labour. Based on recent claims history,GGT revises their 2014 warranty provision to 9% of sales.

Requirements:

a. Prepare summary journal entries to record warranty expense and warranty claims in 2013 and 2014.

b. Determine the provision for warranty payable that GGT will report as a liability on December 31,2014.

• GGT reported a $270,000 provision for warranty payable on its December 31,2012 balance sheet.

• GGT's sales for 2013 totalled $6,000,000 spread evenly through the year.

• The cost to GGT of meeting their warranty claims in 2013 was $480,000; $300,000 for parts and $180,000 for labour.

• GGT's sales for 2014 totalled $6,200,000 spread evenly through the year.

• The cost to GGT of meeting their warranty claims in 2014 was $468,000; $280,800 for parts and $187,200 for labour. Based on recent claims history,GGT revises their 2014 warranty provision to 9% of sales.

Requirements:

a. Prepare summary journal entries to record warranty expense and warranty claims in 2013 and 2014.

b. Determine the provision for warranty payable that GGT will report as a liability on December 31,2014.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

70

Which statement about contingencies is correct?

A)If the future outcome is remote but reliably measurable,a provision is recorded.

B)If the future outcome is remote,but not reliably measurable,disclosure is required.

C)If the future outcome is remote,but not reliably measurable,no action is required.

D)If the future outcome is remote,but reliably measurable,disclosure is required.

A)If the future outcome is remote but reliably measurable,a provision is recorded.

B)If the future outcome is remote,but not reliably measurable,disclosure is required.

C)If the future outcome is remote,but not reliably measurable,no action is required.

D)If the future outcome is remote,but reliably measurable,disclosure is required.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

71

Which statement about contingencies is correct?

A)It involves only potential economic outflows of resources.

B)It is a possible condition that depends upon the outcome of a future event.

C)It involves uncertainty about either the timing or amount of payment.

D)It is an existing condition that depends upon the outcome of a future event.

A)It involves only potential economic outflows of resources.

B)It is a possible condition that depends upon the outcome of a future event.

C)It involves uncertainty about either the timing or amount of payment.

D)It is an existing condition that depends upon the outcome of a future event.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

72

Consider the following independent situations. The underlined entity is the reporting entity.

1. The Supreme Court of Canada ordered a supplier to pay Towna Haring Inc. $500,000 for breach of contract.

2. Iwas Pharmaceuticals Inc. sued Game Day Agencies Ltd. for $8 million alleging patent infringement. While there may be some substance to Iwas's assertion,Game Day's legal counsel estimates that Iwas's likelihood of success is about 30%.

3. Environment Canada sued Foil Fan Isotopes Ltd. for $18 million seeking to recover the costs of cleaning up Foil Fan's accidental discharge of radioactive materials. Foil Fan acknowledges liability but is disputing the amount,claiming that the actual costs are in the range of$9 million to $12 million. Foil Fan's $18 million environmental insurance policy includes a $6 million deductible clause.

Requirement:

a. For each of the situations,indicate whether the appropriate accounting treatment is to:

b. For each situation that requires the recognition of an asset or liability,record the journal entry.

1. The Supreme Court of Canada ordered a supplier to pay Towna Haring Inc. $500,000 for breach of contract.

2. Iwas Pharmaceuticals Inc. sued Game Day Agencies Ltd. for $8 million alleging patent infringement. While there may be some substance to Iwas's assertion,Game Day's legal counsel estimates that Iwas's likelihood of success is about 30%.

3. Environment Canada sued Foil Fan Isotopes Ltd. for $18 million seeking to recover the costs of cleaning up Foil Fan's accidental discharge of radioactive materials. Foil Fan acknowledges liability but is disputing the amount,claiming that the actual costs are in the range of$9 million to $12 million. Foil Fan's $18 million environmental insurance policy includes a $6 million deductible clause.

Requirement:

a. For each of the situations,indicate whether the appropriate accounting treatment is to:

b. For each situation that requires the recognition of an asset or liability,record the journal entry. Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

73

Explain what contingent assets and liabilities are and how these items are accounted for financial reporting purposes.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

74

Which statement about contingencies is correct?

A)If the future outcome is probable and reliably measurable,a provision is recorded.

B)If the future outcome is probable,disclosure is required if it is reliably measurable.

C)If the future outcome is probable,but not reliably measurable,no action is required.

D)If the future outcome is probable,a provision is required,even if it is not reliably measurable,

A)If the future outcome is probable and reliably measurable,a provision is recorded.

B)If the future outcome is probable,disclosure is required if it is reliably measurable.

C)If the future outcome is probable,but not reliably measurable,no action is required.

D)If the future outcome is probable,a provision is required,even if it is not reliably measurable,

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

75

Which statement is correct about provisions,contingent assets and contingent liabilities?

A)Provisions are recorded in the financial statements whereas contingent assets are not recorded.

B)Provisions are recorded in the financial statements whereas contingent liabilities are not recorded.

C)Probable contingent liabilities are recorded at management's best estimates.

D)Probable contingent assets are recorded at management's best estimates.

A)Provisions are recorded in the financial statements whereas contingent assets are not recorded.

B)Provisions are recorded in the financial statements whereas contingent liabilities are not recorded.

C)Probable contingent liabilities are recorded at management's best estimates.

D)Probable contingent assets are recorded at management's best estimates.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

76

LMZ Computer Systems Inc. maintains office equipment under contract. The contracts are for labour only; customers must reimburse LMZ for parts. LMZ's rate schedule follows:

LMZ's 2018 sales of maintenance agreements is set out below:

Requirements:

Assuming that sales occurred evenly through the year:

a. What amount of revenue will LMZ recognize for the year ended December 31,2018?

b. What amount of deferred revenue will LMZ report as a current liability on December 31,2018?

c. What amount of deferred revenue will LMZ report as a non-current liability on December 31,2018?

LMZ's 2018 sales of maintenance agreements is set out below: Requirements:Assuming that sales occurred evenly through the year:

a. What amount of revenue will LMZ recognize for the year ended December 31,2018?

b. What amount of deferred revenue will LMZ report as a current liability on December 31,2018?

c. What amount of deferred revenue will LMZ report as a non-current liability on December 31,2018?

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

77

Which statement about contingent liabilities is correct?

A)It is a possible obligation that arises from past transactions and events.

B)It is an obligation that arises from past transactions and events.

C)It involves uncertainty about either the timing or amount of payment.

D)It is a condition that depends upon the outcome of an anticipated event.

A)It is a possible obligation that arises from past transactions and events.

B)It is an obligation that arises from past transactions and events.

C)It involves uncertainty about either the timing or amount of payment.

D)It is a condition that depends upon the outcome of an anticipated event.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

78

Which statement about contingent liabilities is correct?

A)It is a present obligation that will probably result in the economic outflow of resources.

B)It involves uncertainty about either the timing of payment or the amount of payment.

C)It is an obligation that arises from past transactions and events and can be reliably measured.

D)It is a present obligation that arises from past events but it cannot be reliably measured.

A)It is a present obligation that will probably result in the economic outflow of resources.

B)It involves uncertainty about either the timing of payment or the amount of payment.

C)It is an obligation that arises from past transactions and events and can be reliably measured.

D)It is a present obligation that arises from past events but it cannot be reliably measured.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

79

RJ Magazines sells two-year magazine subscriptions for $108 cash each. The cost of producing and delivering each magazine is $2.75 paid in cash at the time of delivery. RJ's sales activity for the year follows:

Sales activity

• On January 1,2017,RJ sells 22,000 subscriptions.

• On April 1,2017,RJ sells 5,000 subscriptions.

• On November 1,2017,RJ sells 12,000 subscriptions

RJ delivers the magazines at the end of the month and the year-end is December 31.

Requirements:

a. Prepare journal entries to record the subscription sales during the year.

b. Prepare summary journal entries to record the revenue earned during the year and the related expense.

Sales activity

• On January 1,2017,RJ sells 22,000 subscriptions.

• On April 1,2017,RJ sells 5,000 subscriptions.

• On November 1,2017,RJ sells 12,000 subscriptions

RJ delivers the magazines at the end of the month and the year-end is December 31.

Requirements:

a. Prepare journal entries to record the subscription sales during the year.

b. Prepare summary journal entries to record the revenue earned during the year and the related expense.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

80

Which statement is correct about provisions,contingent assets and contingent liabilities?

A)The same probability threshold is used to record contingent liabilities and provisions.

B)The same probability threshold is used to record contingent assets and contingent liabilities.

C)Possible contingent liabilities are recorded.

D)Virtually certain contingent assets are recorded.

A)The same probability threshold is used to record contingent liabilities and provisions.

B)The same probability threshold is used to record contingent assets and contingent liabilities.

C)Possible contingent liabilities are recorded.

D)Virtually certain contingent assets are recorded.

Unlock Deck

Unlock for access to all 90 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 90 flashcards in this deck.