Deck 10: Fundamentals of Cost Management

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

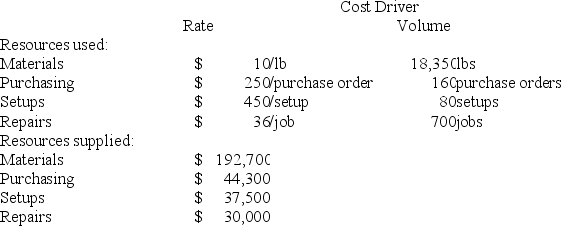

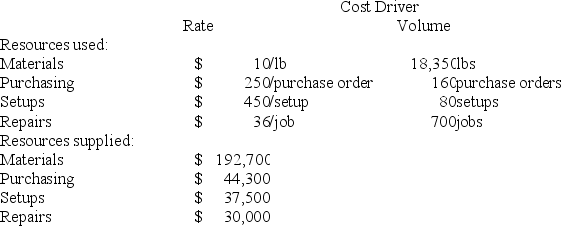

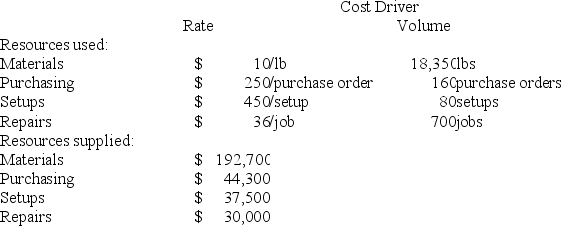

Question

Question

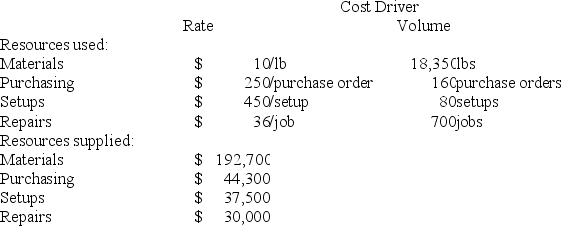

South Beach Industries reports the following information about resources. At the beginning of the year, South Beach estimated it would spend $180,000 for materials, $42,000 for purchasing, $35,000 for setups, and $36,000 for repairs.

-

The unused resource capacity for materials for South Beach is:

A) $12,700.

B) $3,500.

C) $19,270.

D) $9,200.

-

The unused resource capacity for materials for South Beach is:

A) $12,700.

B) $3,500.

C) $19,270.

D) $9,200.

Question

Question

Question

Question

Question

South Beach Industries reports the following information about resources. At the beginning of the year, South Beach estimated it would spend $180,000 for materials, $42,000 for purchasing, $35,000 for setups, and $36,000 for repairs.

-

The unused resource capacity for purchasing for South Beach is:

A) $5,538.

B) $2,000.

C) $4,300.

D) $2,300.

-

The unused resource capacity for purchasing for South Beach is:

A) $5,538.

B) $2,000.

C) $4,300.

D) $2,300.

Question

Question

Question

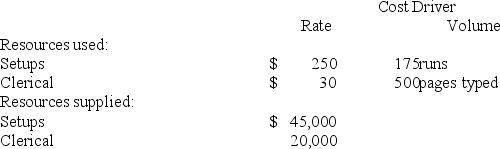

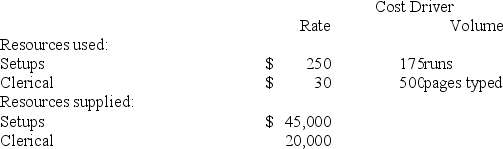

Macon Publishing reports the following information about resources. At the beginning of the year, Macon estimated it would spend $42,000 for setups and $21,000 for clerical.

-

The unused resource capacity for setups for Macon Publishing is:

A) $1,250.

B) $3,000.

C) $1,750.

D) $5,000.

-

The unused resource capacity for setups for Macon Publishing is:

A) $1,250.

B) $3,000.

C) $1,750.

D) $5,000.

Question

South Beach Industries reports the following information about resources. At the beginning of the year, South Beach estimated it would spend $180,000 for materials, $42,000 for purchasing, $35,000 for setups, and $36,000 for repairs.

-

The unused resource capacity for setups for South Beach is:

A) $2,500.

B) $1,080.

C) $1,500.

D) $1,000.

-

The unused resource capacity for setups for South Beach is:

A) $2,500.

B) $1,080.

C) $1,500.

D) $1,000.

Question

Question

Question

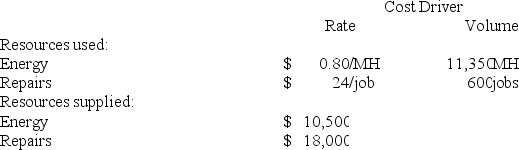

South Beach Industries reports the following information about resources. At the beginning of the year, South Beach estimated it would spend $180,000 for materials, $42,000 for purchasing, $35,000 for setups, and $36,000 for repairs.

-

The unused resource capacity for repairs for South Beach is:

A) $4,800.

B) $10,800.

C) $6,000.

D) $3,600.

-

The unused resource capacity for repairs for South Beach is:

A) $4,800.

B) $10,800.

C) $6,000.

D) $3,600.

Question

Question

Question

Question

Question

Question

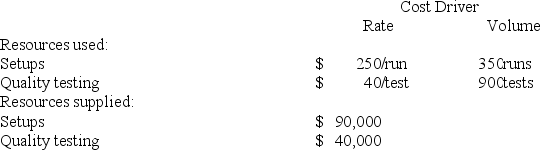

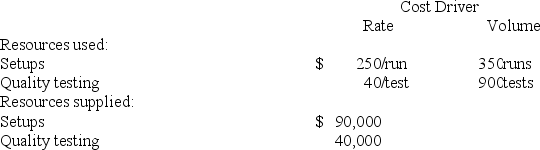

Denim Products reports the following information about resources. At the beginning of the year, Denim estimated it would spend $84,000 for setups and $41,000 for quality testing.

-

The unused resource capacity for setups for Denim Products is:

A) $6,000.

B) $2,500.

C) $1,000.

D) $3,500.

-

The unused resource capacity for setups for Denim Products is:

A) $6,000.

B) $2,500.

C) $1,000.

D) $3,500.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Macon Publishing reports the following information about resources. At the beginning of the year, Macon estimated it would spend $42,000 for setups and $21,000 for clerical.

-

The unused resource capacity for clerical for Macon Publishing is:

A) $5,000.

B) $1,000.

C) $6,000.

D) $1,260.

-

The unused resource capacity for clerical for Macon Publishing is:

A) $5,000.

B) $1,000.

C) $6,000.

D) $1,260.

Question

Question

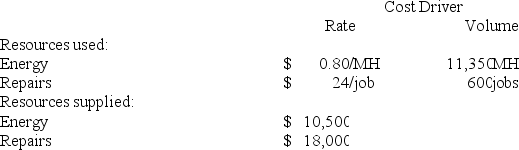

Scallon Products reports the following information about resources. At the beginning of the year, Scallon estimated it would spend $8,000 for energy and $12,000 for repairs.

-

The unused resource capacity for energy for Scallon Products is:

A) $8,000.

B) $1,080.

C) $1,420.

D) $2,500.

-

The unused resource capacity for energy for Scallon Products is:

A) $8,000.

B) $1,080.

C) $1,420.

D) $2,500.

Question

Scallon Products reports the following information about resources. At the beginning of the year, Scallon estimated it would spend $8,000 for energy and $12,000 for repairs.

-

The unused resource capacity for repairs for Scallon Products is:

A) $2,400.

B) $12,000.

C) $6,000.

D) $3,600.

-

The unused resource capacity for repairs for Scallon Products is:

A) $2,400.

B) $12,000.

C) $6,000.

D) $3,600.

Question

Question

Question

Denim Products reports the following information about resources. At the beginning of the year, Denim estimated it would spend $84,000 for setups and $41,000 for quality testing.

-

The unused resource capacity for quality testing for Denim Products is:

A) $4,000.

B) $2,000.

C) $1,000.

D) $5,000.

-

The unused resource capacity for quality testing for Denim Products is:

A) $4,000.

B) $2,000.

C) $1,000.

D) $5,000.

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/144

Play

Full screen (f)

Deck 10: Fundamentals of Cost Management

1

Managerial decisions based on activity-based costing (ABC) information affect only volume-related, batch-related, and product-related costs.

False

2

A cost of quality system is based on the trade-off between incurring costs to meet product (or service) specifications and the costs of failing to meet those specifications.

True

3

Internal failure costs include materials wasted in the production process and correcting products before they are sold.

True

4

Activity-based cost management (ABCM) can be used for managerial decision-making in service, merchandising, and manufacturing companies.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

5

Quality can be defined as the degree to which a product or service performs as it was designed to do.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

6

Unused capacity costs incurred for the benefit of a company's customers (e.g., meet seasonal demands) should be assigned to the customers that require (use) the excess capacity.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

7

Storing materials, work-in-process items, and finished goods in inventory are essential, value-added activities in most companies.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

8

Activity-based cost management (ABCM) uses the information provided by activity-based costing (ABC) to identify ways to improve operations.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

9

In activity-based costing, the cost driver rate is computed by dividing the total cost per activity by the estimated number of units produced.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

10

Tangible customer expectations include how the product's salespeople treat customers and the time required to deliver the product to the customer.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

11

The basic concepts involved in activity-based costing (ABC) can be used to determine customer profitability as well as product costs.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

12

The difference between the resources used and the resources supplied is called unused resource capacity in a typical activity-based cost management (ABCM) system.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

13

In general, managerial decisions affecting capacity-related costs and activities also affect volume-level, batch-level, and product-level cost and activities.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

14

Unused resource capacity plus the amount of the resources used is equal to the amount of resources supplied.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

15

In general, the unit-level (or volume-related) costs in an activity-based costing (ABC) system are variable costs.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

16

Activity-based costing (ABC) techniques used to evaluate customer profitability can also be applied to evaluating suppliers.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

17

Theoretical capacity is the long-run expected volume based on reasonably attainable working conditions.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

18

In general, decreasing (or eliminating) the resources committed to nonvalue-added activities will decrease customer response time.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

19

Theoretical capacity is the amount of production possible assuming expected downtime for scheduled maintenance, normal breaks, and vacations.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

20

In general, the capacity-related costs in an activity-based costing (ABC) system are variable costs.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

21

Fence Industries is preparing its annual profit plan. As part of its analysis of the profitability of its customers, management estimates that the $12,000 for sales support should be assigned to the individual customers from the information given as follows:

-

What is the amount of the sales support costs that should be allocated to Customer B, assuming Fence uses purchases orders to compute activity-based costs?

A) $2,400.

B) $4,000.

C) $8,000.

D) $9,600.

-

What is the amount of the sales support costs that should be allocated to Customer B, assuming Fence uses purchases orders to compute activity-based costs?

A) $2,400.

B) $4,000.

C) $8,000.

D) $9,600.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

22

In an activity-based costing (ABC) system, cost reduction is accomplished by identifying and eliminating: (CPA adapted)

A.

B.

C.

D.

A) Option A.

B) Option B.

C) Option C.

D) Option D.

A.

B.

C.

D.

A) Option A.

B) Option B.

C) Option C.

D) Option D.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

23

Which of the following is a value-added activity?

A) Storing items.

B) Moving items.

C) Waiting for work.

D) Assembling items.

A) Storing items.

B) Moving items.

C) Waiting for work.

D) Assembling items.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

24

Which of the following is not true of process reengineering?

A) It is the changing of operational processes to improve performance.

B) It often takes place after examining ABC data to determine opportunities for improvement.

C) It involves identifying what the customer wants or expects from the firm's products or services.

D) It is the sixth, and final, step of ABCM activity analysis.

A) It is the changing of operational processes to improve performance.

B) It often takes place after examining ABC data to determine opportunities for improvement.

C) It involves identifying what the customer wants or expects from the firm's products or services.

D) It is the sixth, and final, step of ABCM activity analysis.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

25

Which of the following items would be classified as a batch-related cost in an activity-based cost management (ABCM) system?

A) Indirect labor.

B) Production supervisor's salary.

C) Depreciation on factory building.

D) Machinery set-up costs.

A) Indirect labor.

B) Production supervisor's salary.

C) Depreciation on factory building.

D) Machinery set-up costs.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

26

Activity-based cost management (ABCM) can best be defined as:

A) a cost system using multiple departmental overhead rates.

B) the use of cost information gathered using activity-based costing (ABC).

C) a quality-control system focusing on eliminating errors and mistakes.

D) an incentive system for a company's key decision-makers.

A) a cost system using multiple departmental overhead rates.

B) the use of cost information gathered using activity-based costing (ABC).

C) a quality-control system focusing on eliminating errors and mistakes.

D) an incentive system for a company's key decision-makers.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

27

Barter Company's cost management and product costing procedures follow activity-based costing (ABC) principles. Activities have been identified and classified as being either value-added or nonvalue-added for each product. Which of the following activities, used in Barter's production process, is nonvalue-added? (CPA adapted)

A) Drill press activity.

B) Heat treatment activity.

C) Design engineering activity.

D) Raw materials storage activity.

A) Drill press activity.

B) Heat treatment activity.

C) Design engineering activity.

D) Raw materials storage activity.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

28

Activity analysis is one of the first stages in implementing activity-based cost management (ABCM). Which of the following steps in activity analysis is usually performed first?

A) Classify all activities as value-added or nonvalue-added.

B) Chart, from start to finish, the activities used to complete the product or service.

C) Identify the process objectives that are defined by what the customer wants or expects from the process.

D) Continuously improve the efficiency of all value-added activities and develop plans to eliminate or reduce nonvalue-added ones.

A) Classify all activities as value-added or nonvalue-added.

B) Chart, from start to finish, the activities used to complete the product or service.

C) Identify the process objectives that are defined by what the customer wants or expects from the process.

D) Continuously improve the efficiency of all value-added activities and develop plans to eliminate or reduce nonvalue-added ones.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

29

McArthur Company has gathered the following data related to its production process of two of its products for the week ended April 30:

The costs above that appear to be allocated rather than traced are:

A) Unit-related material costs.

B) Variable conversion costs.

C) Indirect manufacturing costs only.

D) All indirect costs.

The costs above that appear to be allocated rather than traced are:

A) Unit-related material costs.

B) Variable conversion costs.

C) Indirect manufacturing costs only.

D) All indirect costs.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

30

Which of the following activities is most likely to be classified as value-added for a merchandise company?

A) Purchasing.

B) Waiting.

C) Receiving.

D) Setting up.

A) Purchasing.

B) Waiting.

C) Receiving.

D) Setting up.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

31

Which of the following statements about activity-based costing (ABC) is not true? (CIA adapted)

A) In ABC, cost drivers are used to link costs to products.

B) ABC is useful for assigning marketing and distribution costs.

C) ABC differs from traditional costing systems in that products are not cross-subsidized.

D) ABC is more likely to result in major differences from traditional costing systems if the firm manufactures only one product rather than multiple products.

A) In ABC, cost drivers are used to link costs to products.

B) ABC is useful for assigning marketing and distribution costs.

C) ABC differs from traditional costing systems in that products are not cross-subsidized.

D) ABC is more likely to result in major differences from traditional costing systems if the firm manufactures only one product rather than multiple products.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

32

Which of the following items would not be used as the cost driver for a volume-related cost in an activity-based cost management (ABCM) system?

A) Direct labor hours.

B) Machine hours.

C) Units produced.

D) Square footage.

A) Direct labor hours.

B) Machine hours.

C) Units produced.

D) Square footage.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

33

Which of the following activities is most likely to be classified as value-added for a manufacturing company?

A) Storing.

B) Ordering.

C) Inspecting.

D) Assembling.

A) Storing.

B) Ordering.

C) Inspecting.

D) Assembling.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

34

Activity analysis is an important approach to operations control and the successful implementation of activity-based cost management (ABCM). Which of the following procedures is not part of activity analysis?

A) Chart, from start to finish, the activities used to complete the product or service.

B) Classify all activities as either value-added or nonvalue-added activities.

C) Identify the process objectives as defined by what the customer desires from the process.

D) Compute the predetermined rate per activity by dividing the total cost pool by the total cost drivers.

A) Chart, from start to finish, the activities used to complete the product or service.

B) Classify all activities as either value-added or nonvalue-added activities.

C) Identify the process objectives as defined by what the customer desires from the process.

D) Compute the predetermined rate per activity by dividing the total cost pool by the total cost drivers.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

35

Fence Industries is preparing its annual profit plan. As part of its analysis of the profitability of its customers, management estimates that the $12,000 for sales support should be assigned to the individual customers from the information given as follows:

-

What is the amount of the sales support costs that should be allocated to Customer A, assuming Fence uses purchases orders to compute activity-based costs?

A) $2,400.

B) $4,000.

C) $8,000.

D) $9,600.

-

What is the amount of the sales support costs that should be allocated to Customer A, assuming Fence uses purchases orders to compute activity-based costs?

A) $2,400.

B) $4,000.

C) $8,000.

D) $9,600.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

36

In an activity-based cost management (ABCM) system, facility-related costs are those that are incurred to:

A) sustain the company's marketing program.

B) maintain the plant's production capacity.

C) support the research and development process.

D) cause a change in the engineering plans for a product.

A) sustain the company's marketing program.

B) maintain the plant's production capacity.

C) support the research and development process.

D) cause a change in the engineering plans for a product.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

37

Fence Industries is preparing its annual profit plan. As part of its analysis of the profitability of its customers, management estimates that the $12,000 for sales support should be assigned to the individual customers from the information given as follows:

-

What is the amount of the sales support costs that should be allocated to Customer B, assuming Fence uses units purchased to compute activity-based costs?

A) $2,400.

B) $4,000.

C) $8,000.

D) $9,600.

-

What is the amount of the sales support costs that should be allocated to Customer B, assuming Fence uses units purchased to compute activity-based costs?

A) $2,400.

B) $4,000.

C) $8,000.

D) $9,600.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

38

Which of the following items would be classified as a volume-related cost in an activity-based cost management (ABCM) system?

A) Indirect materials.

B) Production supervisor's salary.

C) Depreciation on factory building.

D) Research and development.

A) Indirect materials.

B) Production supervisor's salary.

C) Depreciation on factory building.

D) Research and development.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

39

Which of the following items would be classified as a product-related cost in an activity-based cost management (ABCM) system?

A) Change order to meet a new customer's specification.

B) Movement of materials for products in production.

C) Long-term lease payments for factory equipment.

D) Insurance and property taxes on factory building.

A) Change order to meet a new customer's specification.

B) Movement of materials for products in production.

C) Long-term lease payments for factory equipment.

D) Insurance and property taxes on factory building.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

40

Fence Industries is preparing its annual profit plan. As part of its analysis of the profitability of its customers, management estimates that the $12,000 for sales support should be assigned to the individual customers from the information given as follows:

-

What is the amount of the sales support costs that should be allocated to Customer A assuming Fence uses units purchased to compute activity-based costs?

A) $2,400.

B) $4,000.

C) $8,000.

D) $9,600.

-

What is the amount of the sales support costs that should be allocated to Customer A assuming Fence uses units purchased to compute activity-based costs?

A) $2,400.

B) $4,000.

C) $8,000.

D) $9,600.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

41

Express Travel decides to price delivery service according to the results of a recent activity-based costing (ABC) study. The study indicates Express Travel should charge $16 per order, 1% of annual order value for general delivery costs, $2.50 per item, and $45 for delivery.

A year later, Express Travel collected the following information for three of its customers:

-

What are the total delivery costs charged to Customer C during the year?

A) $16,863.

B) $20,000.

C) $31,272.

D) $32,272.

A year later, Express Travel collected the following information for three of its customers:

-

What are the total delivery costs charged to Customer C during the year?

A) $16,863.

B) $20,000.

C) $31,272.

D) $32,272.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

42

Crafter Lumber Supply noticed a recent decline in the amount of purchases from a key customer. Worried that other customers might also reduce their purchases, Crafter's management decided to evaluate the cost of its delivery service. Which of the following cost drivers is more appropriate for general administrative costs of the Delivery Department?

A) Number of different items ordered.

B) Value of each order.

C) Total number of items in each order.

D) Number of deliveries made.

A) Number of different items ordered.

B) Value of each order.

C) Total number of items in each order.

D) Number of deliveries made.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

43

Benton Company is preparing its annual profit plan. As part of its analysis of the cost of its purchasing activity, management estimates that the $48,000 for purchasing support should be assigned to the individual vendors from the information given as follows:

-

What is the amount of the purchasing costs that should be allocated to Vendor B, assuming Benton uses purchases orders to compute activity-based costs?

A) $9,600.

B) $16,000.

C) $32,000.

D) $38,400.

-

What is the amount of the purchasing costs that should be allocated to Vendor B, assuming Benton uses purchases orders to compute activity-based costs?

A) $9,600.

B) $16,000.

C) $32,000.

D) $38,400.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

44

Benton Company is preparing its annual profit plan. As part of its analysis of the cost of its purchasing activity, management estimates that the $48,000 for purchasing support should be assigned to the individual vendors from the information given as follows:

-

What is the amount of the purchasing costs that should be allocated to Vendor A, assuming Benton uses purchases orders to compute activity-based costs?

A) $9,600.

B) $16,000.

C) $32,000.

D) $38,400.

-

What is the amount of the purchasing costs that should be allocated to Vendor A, assuming Benton uses purchases orders to compute activity-based costs?

A) $9,600.

B) $16,000.

C) $32,000.

D) $38,400.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

45

Express Travel decides to price delivery services according to the results of a recent activity-based costing (ABC) study. The study indicates Express Travel should charge $16 per order, 1% of annual order value for general delivery costs, $2.50 per item, and $45 for delivery.

A year later, Express Travel collected the following information for three of its customers:

-

What are the total delivery costs charged to Customer B during the year?

A) $13,490.

B) $11,378.

C) $10,800.

D) $10,578.

A year later, Express Travel collected the following information for three of its customers:

-

What are the total delivery costs charged to Customer B during the year?

A) $13,490.

B) $11,378.

C) $10,800.

D) $10,578.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

46

South Beach Industries reports the following information about resources. At the beginning of the year, South Beach estimated it would spend $180,000 for materials, $42,000 for purchasing, $35,000 for setups, and $36,000 for repairs.

-

The unused resource capacity for materials for South Beach is:

A) $12,700.

B) $3,500.

C) $19,270.

D) $9,200.

-

The unused resource capacity for materials for South Beach is:

A) $12,700.

B) $3,500.

C) $19,270.

D) $9,200.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

47

Benton Company is preparing its annual profit plan. As part of its analysis of the cost of its purchasing activity, management estimates that the $48,000 for purchasing support should be assigned to the individual vendors from the information given as follows:

-

What is the amount of the purchasing costs that should be allocated to Vendor B, assuming Benton uses units purchased to compute activity-based costs?

A) $9,600.

B) $16,000.

C) $32,000.

D) $38,400.

-

What is the amount of the purchasing costs that should be allocated to Vendor B, assuming Benton uses units purchased to compute activity-based costs?

A) $9,600.

B) $16,000.

C) $32,000.

D) $38,400.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

48

Benton Company is preparing its annual profit plan. As part of its analysis of the cost of its purchasing activity, management estimates that the $48,000 for purchasing support should be assigned to the individual vendors from the information given as follows:

-

What is the amount of the purchasing costs that should be allocated to Vendor B, assuming Benton uses number of shipments received to compute activity-based costs?

A) $9,000.

B) $16,000.

C) $32,000.

D) $39,000.

-

What is the amount of the purchasing costs that should be allocated to Vendor B, assuming Benton uses number of shipments received to compute activity-based costs?

A) $9,000.

B) $16,000.

C) $32,000.

D) $39,000.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

49

The amount of resources used in an activity-based costing (ABC) system for a specific activity is computed by multiplying the:

A) cost driver rate by the actual cost driver volume.

B) cost driver rate by the planned cost driver volume.

C) overhead rate by the actual cost driver volume.

D) overhead rate by the planned cost driver volume.

A) cost driver rate by the actual cost driver volume.

B) cost driver rate by the planned cost driver volume.

C) overhead rate by the actual cost driver volume.

D) overhead rate by the planned cost driver volume.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

50

Express Travel decides to price delivery services according to the results of a recent activity-based costing (ABC) study. The study indicates Express Travel should charge $16 per order, 1% of annual order value for general delivery costs, $2.50 per item, and $45 for delivery.

A year later, Express Travel collected the following information for three of its customers:

-

What are the total delivery costs charged to Customer A during the year?

A) $5,738.

B) $6,650.

C) $6,938.

D) $20,235.

A year later, Express Travel collected the following information for three of its customers:

-

What are the total delivery costs charged to Customer A during the year?

A) $5,738.

B) $6,650.

C) $6,938.

D) $20,235.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

51

South Beach Industries reports the following information about resources. At the beginning of the year, South Beach estimated it would spend $180,000 for materials, $42,000 for purchasing, $35,000 for setups, and $36,000 for repairs.

-

The unused resource capacity for purchasing for South Beach is:

A) $5,538.

B) $2,000.

C) $4,300.

D) $2,300.

-

The unused resource capacity for purchasing for South Beach is:

A) $5,538.

B) $2,000.

C) $4,300.

D) $2,300.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

52

Benton Company is preparing its annual profit plan. As part of its analysis of the cost of its purchasing activity, management estimates that the $48,000 for purchasing support should be assigned to the individual vendors from the information given as follows:

What is the amount of the purchasing costs that should be allocated to Vendor A, assuming Benton uses units purchased to compute activity-based costs?

A) $9,600.

B) $16,000.

C) $32,000.

D) $38,400.

What is the amount of the purchasing costs that should be allocated to Vendor A, assuming Benton uses units purchased to compute activity-based costs?

A) $9,600.

B) $16,000.

C) $32,000.

D) $38,400.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

53

Republic Industries decides to price delivery services according to the results of a recent activity-based costing (ABC) study. The study indicates Republic should charge $8 per order, 2% of annual order value for general delivery costs, $1.25 per item, and $30 for delivery.

A year later, Republic collected the following information for two of its best customers:

-

What are the total delivery costs charged to Customer C during the year?

A) $5,344.

B) $5,364.

C) $6,900.

D) $6,964.

A year later, Republic collected the following information for two of its best customers:

-

What are the total delivery costs charged to Customer C during the year?

A) $5,344.

B) $5,364.

C) $6,900.

D) $6,964.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

54

Macon Publishing reports the following information about resources. At the beginning of the year, Macon estimated it would spend $42,000 for setups and $21,000 for clerical.

-

The unused resource capacity for setups for Macon Publishing is:

A) $1,250.

B) $3,000.

C) $1,750.

D) $5,000.

-

The unused resource capacity for setups for Macon Publishing is:

A) $1,250.

B) $3,000.

C) $1,750.

D) $5,000.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

55

South Beach Industries reports the following information about resources. At the beginning of the year, South Beach estimated it would spend $180,000 for materials, $42,000 for purchasing, $35,000 for setups, and $36,000 for repairs.

-

The unused resource capacity for setups for South Beach is:

A) $2,500.

B) $1,080.

C) $1,500.

D) $1,000.

-

The unused resource capacity for setups for South Beach is:

A) $2,500.

B) $1,080.

C) $1,500.

D) $1,000.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

56

Republic Industries decides to price delivery services according to the results of a recent activity-based costing (ABC) study. The study indicates Republic should charge $8 per order, 2% of annual order value for general delivery costs, $1.25 per item, and $30 for delivery.

A year later, Republic collected the following information for two of its best customers:

-

What are the total delivery costs charged to Customer D during the year?

A) $5,344.

B) $5,364.

C) $6,900.

D) $6,964.

A year later, Republic collected the following information for two of its best customers:

-

What are the total delivery costs charged to Customer D during the year?

A) $5,344.

B) $5,364.

C) $6,900.

D) $6,964.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

57

Activity-based costing (ABC) information cannot be used by managerial decision-makers to evaluate the:

A) profitability of a customer.

B) market potential of a product.

C) cost of using a particular supplier.

D) whether to continue providing a service.

A) profitability of a customer.

B) market potential of a product.

C) cost of using a particular supplier.

D) whether to continue providing a service.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

58

South Beach Industries reports the following information about resources. At the beginning of the year, South Beach estimated it would spend $180,000 for materials, $42,000 for purchasing, $35,000 for setups, and $36,000 for repairs.

-

The unused resource capacity for repairs for South Beach is:

A) $4,800.

B) $10,800.

C) $6,000.

D) $3,600.

-

The unused resource capacity for repairs for South Beach is:

A) $4,800.

B) $10,800.

C) $6,000.

D) $3,600.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

59

The unused resource capacity is the difference between the resources supplied and the resources:

A) purchased.

B) wasted.

C) used.

D) on hand.

A) purchased.

B) wasted.

C) used.

D) on hand.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

60

Benton Company is preparing its annual profit plan. As part of its analysis of the cost of its purchasing activity, management estimates that the $48,000 for purchasing support should be assigned to the individual vendors from the information given as follows:

-

What is the amount of the purchasing costs that should be allocated to Vendor A, assuming Benton uses number of shipments received to compute activity-based costs?

A) $9,000.

B) $16,000.

C) $32,000.

D) $39,000.

-

What is the amount of the purchasing costs that should be allocated to Vendor A, assuming Benton uses number of shipments received to compute activity-based costs?

A) $9,000.

B) $16,000.

C) $32,000.

D) $39,000.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

61

Water Industries' quality control report for August contains the following items:

-

What would be the total of the appraisal costs on the August quality control report for Water Industries?

A) $7,000.

B) $11,000.

C) $12,000.

D) $15,000.

-

What would be the total of the appraisal costs on the August quality control report for Water Industries?

A) $7,000.

B) $11,000.

C) $12,000.

D) $15,000.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

62

Which of the following is not an explanation of why a company would operate at less than theoretical capacity?

A) Scheduled maintenance of equipment.

B) Breakdowns in equipment.

C) Customer demand is less than anticipated.

D) Customer demand is more than anticipated.

A) Scheduled maintenance of equipment.

B) Breakdowns in equipment.

C) Customer demand is less than anticipated.

D) Customer demand is more than anticipated.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

63

Water Industries' quality control report for August contains the following items:

-

What would be the total of the prevention costs on the August quality control report for Water Industries?

A) $5,000.

B) $7,000.

C) $11,000.

D) $15,000.

-

What would be the total of the prevention costs on the August quality control report for Water Industries?

A) $5,000.

B) $7,000.

C) $11,000.

D) $15,000.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

64

Denim Products reports the following information about resources. At the beginning of the year, Denim estimated it would spend $84,000 for setups and $41,000 for quality testing.

-

The unused resource capacity for setups for Denim Products is:

A) $6,000.

B) $2,500.

C) $1,000.

D) $3,500.

-

The unused resource capacity for setups for Denim Products is:

A) $6,000.

B) $2,500.

C) $1,000.

D) $3,500.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

65

Which of the following is not an example of an external failure cost?

A) Accepting company liability resulting from product failure.

B) Experiencing decreasing sales as a result of poor-quality products.

C) Repairing or replacing defective products after they've been sold.

D) Testing products in use at the customer's site.

A) Accepting company liability resulting from product failure.

B) Experiencing decreasing sales as a result of poor-quality products.

C) Repairing or replacing defective products after they've been sold.

D) Testing products in use at the customer's site.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

66

Which of the following statements regarding quality costs is(are) false?

(A) In a cost of quality system, internal and external failure costs are called conformance costs.

(B) Prevention costs are costs incurred to detect individual units of product that do not conform to its specifications.

A) Only A is false.

B) Only B is false.

C) Both of these are false.

D) Neither of these is false.

(A) In a cost of quality system, internal and external failure costs are called conformance costs.

(B) Prevention costs are costs incurred to detect individual units of product that do not conform to its specifications.

A) Only A is false.

B) Only B is false.

C) Both of these are false.

D) Neither of these is false.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

67

The degree to which a good or service meets specifications is called:

A) conformance to specifications.

B) customer quality demands.

C) a conformance cost.

D) a compliance cost.

A) conformance to specifications.

B) customer quality demands.

C) a conformance cost.

D) a compliance cost.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

68

Which of the following statement is(are) true?

(A) Unused capacity costs incurred for the benefit of a company's customers (e.g., meet seasonal demands) should be assigned to the customers that require (use) the excess capacity.

(B) In general, managerial decisions affecting capacity-related costs and activities also affect volume-related, batch-related, and product-related cost and activities.

A) Only A is true.

B) Only B is true.

C) Both of these are true.

D) Neither of these is true.

(A) Unused capacity costs incurred for the benefit of a company's customers (e.g., meet seasonal demands) should be assigned to the customers that require (use) the excess capacity.

(B) In general, managerial decisions affecting capacity-related costs and activities also affect volume-related, batch-related, and product-related cost and activities.

A) Only A is true.

B) Only B is true.

C) Both of these are true.

D) Neither of these is true.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

69

A company has high winter demand and low summer demand for its services. The cost of the unused summer capacity should be allocated:

A) to an account called Idle Capacity.

B) evenly to all customers.

C) only to the winter customers.

D) only to the summer customers.

A) to an account called Idle Capacity.

B) evenly to all customers.

C) only to the winter customers.

D) only to the summer customers.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

70

Which of the following statements is(are) true?

(A) Theoretical capacity is the long-run expected volume based on reasonably attainable working conditions.

(B) The cost of excess capacity is allocated to individual cost objects using the cost driver rate.

A) Only A is true.

B) Only B is true.

C) Both of these are true.

D) Neither of these is true.

(A) Theoretical capacity is the long-run expected volume based on reasonably attainable working conditions.

(B) The cost of excess capacity is allocated to individual cost objects using the cost driver rate.

A) Only A is true.

B) Only B is true.

C) Both of these are true.

D) Neither of these is true.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

71

Which of the following is an example of a prevention cost?

A) Machine inspection.

B) Warranty repairs.

C) Field testing.

D) Marketing costs.

A) Machine inspection.

B) Warranty repairs.

C) Field testing.

D) Marketing costs.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

72

Which of the following is an example of an internal failure cost?

A) Training employees to improve quality.

B) Designing products to reduce production problems.

C) Correcting product defects before they are sold.

D) Inspecting the production process as it occurs.

A) Training employees to improve quality.

B) Designing products to reduce production problems.

C) Correcting product defects before they are sold.

D) Inspecting the production process as it occurs.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

73

Which of the following items is included in almost all quality control systems?

A) Quality-related waiting time.

B) Quality planning and analysis.

C) Excess or obsolete inventory.

D) Quality-related overtime.

A) Quality-related waiting time.

B) Quality planning and analysis.

C) Excess or obsolete inventory.

D) Quality-related overtime.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

74

Macon Publishing reports the following information about resources. At the beginning of the year, Macon estimated it would spend $42,000 for setups and $21,000 for clerical.

-

The unused resource capacity for clerical for Macon Publishing is:

A) $5,000.

B) $1,000.

C) $6,000.

D) $1,260.

-

The unused resource capacity for clerical for Macon Publishing is:

A) $5,000.

B) $1,000.

C) $6,000.

D) $1,260.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

75

Which of the following is not an example of a prevention cost?

A) Training employees to improve quality.

B) Designing products to reduce production problems.

C) Correcting product defects before they are sold.

D) Inspecting the production process as it occurs.

A) Training employees to improve quality.

B) Designing products to reduce production problems.

C) Correcting product defects before they are sold.

D) Inspecting the production process as it occurs.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

76

Scallon Products reports the following information about resources. At the beginning of the year, Scallon estimated it would spend $8,000 for energy and $12,000 for repairs.

-

The unused resource capacity for energy for Scallon Products is:

A) $8,000.

B) $1,080.

C) $1,420.

D) $2,500.

-

The unused resource capacity for energy for Scallon Products is:

A) $8,000.

B) $1,080.

C) $1,420.

D) $2,500.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

77

Scallon Products reports the following information about resources. At the beginning of the year, Scallon estimated it would spend $8,000 for energy and $12,000 for repairs.

-

The unused resource capacity for repairs for Scallon Products is:

A) $2,400.

B) $12,000.

C) $6,000.

D) $3,600.

-

The unused resource capacity for repairs for Scallon Products is:

A) $2,400.

B) $12,000.

C) $6,000.

D) $3,600.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

78

Which of the following statements regarding the trade-off between conformance and nonconformance costs is(are) false?

(A) The optimal level for a company's quality control program occurs when its conformance costs equal its nonconformance costs.

(B) There is an inverse relationship between the costs spent on nonconformance costs and the level of quality achieved.

A) Only A is false.

B) Only B is false.

C) Both of these are false.

D) Neither of these is false.

(A) The optimal level for a company's quality control program occurs when its conformance costs equal its nonconformance costs.

(B) There is an inverse relationship between the costs spent on nonconformance costs and the level of quality achieved.

A) Only A is false.

B) Only B is false.

C) Both of these are false.

D) Neither of these is false.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

79

The amount of production possible under normal working conditions, including planned downtime and scheduled vacations, is called:

A) actual capacity.

B) normal capacity.

C) practical capacity.

D) theoretical capacity.

A) actual capacity.

B) normal capacity.

C) practical capacity.

D) theoretical capacity.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

80

Denim Products reports the following information about resources. At the beginning of the year, Denim estimated it would spend $84,000 for setups and $41,000 for quality testing.

-

The unused resource capacity for quality testing for Denim Products is:

A) $4,000.

B) $2,000.

C) $1,000.

D) $5,000.

-

The unused resource capacity for quality testing for Denim Products is:

A) $4,000.

B) $2,000.

C) $1,000.

D) $5,000.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 144 flashcards in this deck.