Deck 6: Elimination of Unrealized Profit on Intercompany Sales of Inventory

Full screen (f)

Question

Question

Use the following information for Questions 17 & 18:

P Company owns an 80% interest in S Company.During 2014, S sells merchandise to P for $200,000 at a profit of $40,000.On December 31, 2014, 50% of this merchandise is included in P's inventory.Income statements for P and S are summarized below:

Noncontrolling interest in income for 2014 is:

A)$4,000.

B)$19,200.

C)$20,000.

D)$24,000.

P Company owns an 80% interest in S Company.During 2014, S sells merchandise to P for $200,000 at a profit of $40,000.On December 31, 2014, 50% of this merchandise is included in P's inventory.Income statements for P and S are summarized below:

Noncontrolling interest in income for 2014 is:

A)$4,000.

B)$19,200.

C)$20,000.

D)$24,000.

Question

Question

Question

Question

Use the following information for Questions 15 & 16:

P Company regularly sells merchandise to its 80%-owned subsidiary, S Corporation.In 2013, P sold merchandise that cost $240,000 to S for $300,000.Half of this merchandise remained in S's December 31, 2013 inventory.During 2014, P sold merchandise that cost $375,000 to S for $468,000.Forty percent of this merchandise inventory remained in S's December 31, 2014 inventory.Selected income statement information for the two affiliates for the year 2014 is as follows:

Consolidated sales revenue for P and Subsidiary for 2014 are:

A)$2,907,000.

B)$3,000,000.

C)$3,205,500.

D)$3,375,000.

P Company regularly sells merchandise to its 80%-owned subsidiary, S Corporation.In 2013, P sold merchandise that cost $240,000 to S for $300,000.Half of this merchandise remained in S's December 31, 2013 inventory.During 2014, P sold merchandise that cost $375,000 to S for $468,000.Forty percent of this merchandise inventory remained in S's December 31, 2014 inventory.Selected income statement information for the two affiliates for the year 2014 is as follows:

Consolidated sales revenue for P and Subsidiary for 2014 are:

A)$2,907,000.

B)$3,000,000.

C)$3,205,500.

D)$3,375,000.

Question

Question

Question

Question

Question

Use the following information for Questions 15 & 16:

P Company regularly sells merchandise to its 80%-owned subsidiary, S Corporation.In 2013, P sold merchandise that cost $240,000 to S for $300,000.Half of this merchandise remained in S's December 31, 2013 inventory.During 2014, P sold merchandise that cost $375,000 to S for $468,000.Forty percent of this merchandise inventory remained in S's December 31, 2014 inventory.Selected income statement information for the two affiliates for the year 2014 is as follows:

Consolidated cost of goods sold for P Company and Subsidiary for 2014 are:

A)$2,260,500.

B)$2,268,000.

C)$2,276,700.

D)$2,737,500.

P Company regularly sells merchandise to its 80%-owned subsidiary, S Corporation.In 2013, P sold merchandise that cost $240,000 to S for $300,000.Half of this merchandise remained in S's December 31, 2013 inventory.During 2014, P sold merchandise that cost $375,000 to S for $468,000.Forty percent of this merchandise inventory remained in S's December 31, 2014 inventory.Selected income statement information for the two affiliates for the year 2014 is as follows:

Consolidated cost of goods sold for P Company and Subsidiary for 2014 are:

A)$2,260,500.

B)$2,268,000.

C)$2,276,700.

D)$2,737,500.

Question

Question

Use the following information for Questions 17 & 18:

P Company owns an 80% interest in S Company.During 2014, S sells merchandise to P for $200,000 at a profit of $40,000.On December 31, 2014, 50% of this merchandise is included in P's inventory.Income statements for P and S are summarized below:

Controlling interest in consolidated net income for 2014 is:

A)$300,000.

B)$380,000.

C)$396,000.

D)$420,000.

P Company owns an 80% interest in S Company.During 2014, S sells merchandise to P for $200,000 at a profit of $40,000.On December 31, 2014, 50% of this merchandise is included in P's inventory.Income statements for P and S are summarized below:

Controlling interest in consolidated net income for 2014 is:

A)$300,000.

B)$380,000.

C)$396,000.

D)$420,000.

Question

Question

Question

Question

Question

Question

Question

Question

Use the following information for Questions 24 & 25:

P Company owns an 80% interest in S Company.During 2014, S sells merchandise to P for $150,000 at a profit of $30,000.On December 31, 2014, 50% of this merchandise is included in P's inventory.Income statements for P and S are summarized below:

Controlling interest in consolidated net income for 2014 is:

A)$225,000.

B)$285,000.

C)$297,000.

D)$315,000.

P Company owns an 80% interest in S Company.During 2014, S sells merchandise to P for $150,000 at a profit of $30,000.On December 31, 2014, 50% of this merchandise is included in P's inventory.Income statements for P and S are summarized below:

Controlling interest in consolidated net income for 2014 is:

A)$225,000.

B)$285,000.

C)$297,000.

D)$315,000.

Question

Question

Question

On January 1, 2014, Pharma Company purchased a 90% interest in Sandy Company for $2,800,000.At that time, Sandy had $1,840,000 of common stock and $360,000 of retained earnings.The difference between implied and book value was allocated to the following assets of Sandy Company:

The plant and equipment had a 10-year remaining useful life on January 1, 2014.

During 2014, Pharma sold merchandise to Sandy at a 20% markup above cost.At December 31, 2014, Sandy still had $180,000 of merchandise in its inventory that it had purchased from Pharma.In 2014, Pharma reported net income from independent operations of $1,600,000, while Sandy reported net income of $600,000.

Required:

A.Prepare the workpaper entry to allocate, amortize, and depreciate the difference between implied and book value for 2014.

B.Calculate controlling interest in consolidated net income for 2014.

The plant and equipment had a 10-year remaining useful life on January 1, 2014.

During 2014, Pharma sold merchandise to Sandy at a 20% markup above cost.At December 31, 2014, Sandy still had $180,000 of merchandise in its inventory that it had purchased from Pharma.In 2014, Pharma reported net income from independent operations of $1,600,000, while Sandy reported net income of $600,000.

Required:

A.Prepare the workpaper entry to allocate, amortize, and depreciate the difference between implied and book value for 2014.

B.Calculate controlling interest in consolidated net income for 2014.

Question

Question

Question

Question

Use the following information for Questions 22 & 23:

P Company regularly sells merchandise to its 80%-owned subsidiary, S Corporation.In 2013, P sold merchandise that cost $192,000 to S for $240,000.Half of this merchandise remained in S's December 31, 2013 inventory.During 2014, P sold merchandise that cost $300,000 to S for $375,000.Forty percent of this merchandise inventory remained in S's December 31, 2014 inventory.Selected income statement information for the two affiliates for the year 2014 is as follows:

Consolidated cost of goods sold for P Company and Subsidiary for 2014 are:

A)$1,809,000.

B)$1,815,000.

C)$1,821,000.

D)$2,190,000.

P Company regularly sells merchandise to its 80%-owned subsidiary, S Corporation.In 2013, P sold merchandise that cost $192,000 to S for $240,000.Half of this merchandise remained in S's December 31, 2013 inventory.During 2014, P sold merchandise that cost $300,000 to S for $375,000.Forty percent of this merchandise inventory remained in S's December 31, 2014 inventory.Selected income statement information for the two affiliates for the year 2014 is as follows:

Consolidated cost of goods sold for P Company and Subsidiary for 2014 are:

A)$1,809,000.

B)$1,815,000.

C)$1,821,000.

D)$2,190,000.

Question

The following balances were taken from the records of S Company:

P Company owns 80% of the common stock of S Company.During 2014, P Company purchased merchandise from S Company for $4,000,000.S Company sells merchandise to P Company at cost plus 25% of cost.On December 31, 2014, merchandise purchased from S Company for $1,250,000 remains in the inventory of P Company.On January 1, 2014, P Company's inventory contained merchandise purchased from S Company for $525,000.The affiliated companies file a consolidated income tax return.There was no difference between the implied value and the book value of net assets acquired.

Required:

A.Prepare all workpaper entries necessitated by the intercompany sales of merchandise.

B.Compute noncontrolling interest in consolidated income for 2014.

C.Compute noncontrolling interest in consolidated net assets on December 31, 2014.

P Company owns 80% of the common stock of S Company.During 2014, P Company purchased merchandise from S Company for $4,000,000.S Company sells merchandise to P Company at cost plus 25% of cost.On December 31, 2014, merchandise purchased from S Company for $1,250,000 remains in the inventory of P Company.On January 1, 2014, P Company's inventory contained merchandise purchased from S Company for $525,000.The affiliated companies file a consolidated income tax return.There was no difference between the implied value and the book value of net assets acquired.

Required:

A.Prepare all workpaper entries necessitated by the intercompany sales of merchandise.

B.Compute noncontrolling interest in consolidated income for 2014.

C.Compute noncontrolling interest in consolidated net assets on December 31, 2014.

Question

Question

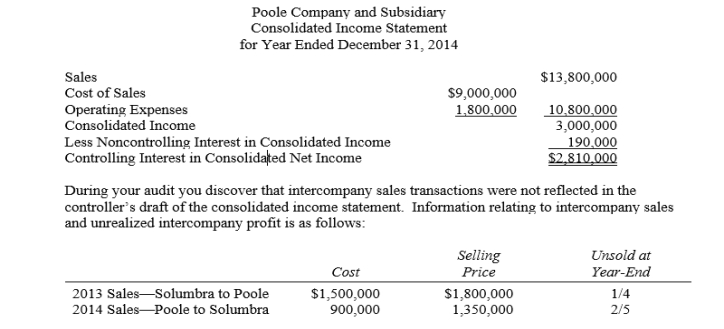

Poole Company owns a 90% interest in Solumbra Company.The consolidated income statement drafted by the controller of Poole Company appeared as follows:

Required:

Prepare a corrected consolidated income statement for Poole Company and Slocum Company for the year ended December 31, 2014.

Required:

Prepare a corrected consolidated income statement for Poole Company and Slocum Company for the year ended December 31, 2014.

Question

Question

Use the following information for Questions 22 & 23:

P Company regularly sells merchandise to its 80%-owned subsidiary, S Corporation.In 2013, P sold merchandise that cost $192,000 to S for $240,000.Half of this merchandise remained in S's December 31, 2013 inventory.During 2014, P sold merchandise that cost $300,000 to S for $375,000.Forty percent of this merchandise inventory remained in S's December 31, 2014 inventory.Selected income statement information for the two affiliates for the year 2014 is as follows:

Consolidated sales revenue for P and Subsidiary for 2014 are:

A)$2,325,000.

B)$2,400,000.

C)$2,565,000.

D)$2,700,000.

P Company regularly sells merchandise to its 80%-owned subsidiary, S Corporation.In 2013, P sold merchandise that cost $192,000 to S for $240,000.Half of this merchandise remained in S's December 31, 2013 inventory.During 2014, P sold merchandise that cost $300,000 to S for $375,000.Forty percent of this merchandise inventory remained in S's December 31, 2014 inventory.Selected income statement information for the two affiliates for the year 2014 is as follows:

Consolidated sales revenue for P and Subsidiary for 2014 are:

A)$2,325,000.

B)$2,400,000.

C)$2,565,000.

D)$2,700,000.

Question

Question

Question

Use the following information for Questions 24 & 25:

P Company owns an 80% interest in S Company.During 2014, S sells merchandise to P for $150,000 at a profit of $30,000.On December 31, 2014, 50% of this merchandise is included in P's inventory.Income statements for P and S are summarized below:

Noncontrolling interest in income for 2014 is:

A)$3,000.

B)$14,400.

C)$15,000.

D)$18,000.

P Company owns an 80% interest in S Company.During 2014, S sells merchandise to P for $150,000 at a profit of $30,000.On December 31, 2014, 50% of this merchandise is included in P's inventory.Income statements for P and S are summarized below:

Noncontrolling interest in income for 2014 is:

A)$3,000.

B)$14,400.

C)$15,000.

D)$18,000.

Question

Question

Question

Question

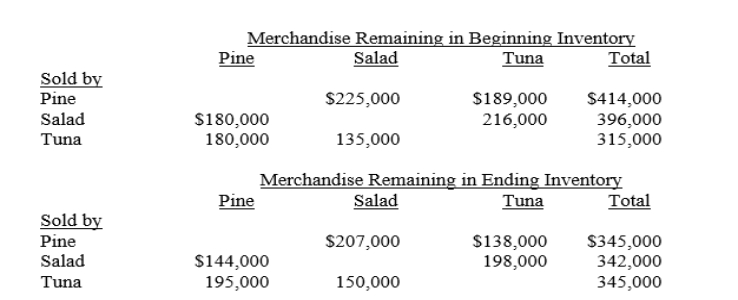

Pine Company owns an 80% interest in Salad Company and a 90% interest in Tuna Company.During 2013 and 2014, intercompany sales of merchandise were made by all three companies.Total sales amounted to $2,400,000 in 2013, and $2,700,000 in 2014.The companies sold their merchandise at the following percentages above cost.

Pine 15%

Salad 20%

Tuna 25%

The amount of merchandise remaining in the 2014 beginning and ending inventories of the companies from these intercompany sales is shown below.

Reported net incomes (from independent operations including sales to affiliates) of Pine, Salad, and Tuna for 2014 were $3,600,000, $1,500,000, and $2,400,000, respectively.

Required:

A.Calculate the amount noncontrolling interest to be deducted from consolidated income in the consolidated income statement for 2014.

B.Calculate the controlling interest in consolidated net income for 2014.

Pine 15%

Salad 20%

Tuna 25%

The amount of merchandise remaining in the 2014 beginning and ending inventories of the companies from these intercompany sales is shown below.

Reported net incomes (from independent operations including sales to affiliates) of Pine, Salad, and Tuna for 2014 were $3,600,000, $1,500,000, and $2,400,000, respectively.

Required:

A.Calculate the amount noncontrolling interest to be deducted from consolidated income in the consolidated income statement for 2014.

B.Calculate the controlling interest in consolidated net income for 2014.

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/40

Play

Full screen (f)

Deck 6: Elimination of Unrealized Profit on Intercompany Sales of Inventory

1

P Company sold merchandise costing $240,000 to S Company (90% owned) for $300,000.At the end of the current year, one-third of the merchandise remains in S Company's inventory.Applying the lower-of- cost-or-market rule, S Company wrote this inventory down to $92,000.What amount of intercompany profit should be eliminated on the consolidated statements workpaper?

A)$20,000.

B)$18,000.

C)$12,000.

D)$10,800.

A)$20,000.

B)$18,000.

C)$12,000.

D)$10,800.

C

2

Use the following information for Questions 17 & 18:

P Company owns an 80% interest in S Company.During 2014, S sells merchandise to P for $200,000 at a profit of $40,000.On December 31, 2014, 50% of this merchandise is included in P's inventory.Income statements for P and S are summarized below:

Noncontrolling interest in income for 2014 is:

A)$4,000.

B)$19,200.

C)$20,000.

D)$24,000.

P Company owns an 80% interest in S Company.During 2014, S sells merchandise to P for $200,000 at a profit of $40,000.On December 31, 2014, 50% of this merchandise is included in P's inventory.Income statements for P and S are summarized below:

Noncontrolling interest in income for 2014 is:

A)$4,000.

B)$19,200.

C)$20,000.

D)$24,000.

C

3

The material sale of inventory items by a parent company to an affiliated company:

A)enters the consolidated revenue computation only if the transfer was the result of arm's length bargaining.

B)affects consolidated net income under a periodic inventory system but not under a perpetual inventory system.

C)does not result in consolidated income until the merchandise is sold to outside parties.

D)does not require a working paper adjustment if the merchandise was transferred at cost.

A)enters the consolidated revenue computation only if the transfer was the result of arm's length bargaining.

B)affects consolidated net income under a periodic inventory system but not under a perpetual inventory system.

C)does not result in consolidated income until the merchandise is sold to outside parties.

D)does not require a working paper adjustment if the merchandise was transferred at cost.

C

4

Pruitt Company owns 80% of Stoney Company's common stock.During 2014, Stoney sold $400,000 of merchandise to Pruitt.At December 31, 2014, one-fourth of the merchandise remained in Pruitt's inventory.In 2014, gross profit percentages were 25% for Pruitt and 30% for Stoney.The amount of unrealized intercompany profit that should be eliminated in the consolidated statements is

A)$80,000.

B)$24,000.

C)$30,000.

D)$25,000.

A)$80,000.

B)$24,000.

C)$30,000.

D)$25,000.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

5

Polly, Inc.owns 80% of Saffron, Inc.During 2014, Polly sold goods with a 40% gross profit to Saffron.Saffron sold all of these goods in 2014.For 2014 consolidated financial statements, how should the summation of Polly and Saffron income statement items be adjusted?

A)Sales and cost of goods sold should be reduced by the intercompany sales.

B)Sales and cost of goods sold should be reduced by 80% of the intercompany sales.

C)Net income should be reduced by 80% of the gross profit on intercompany sales.

D)No adjustment is necessary.

A)Sales and cost of goods sold should be reduced by the intercompany sales.

B)Sales and cost of goods sold should be reduced by 80% of the intercompany sales.

C)Net income should be reduced by 80% of the gross profit on intercompany sales.

D)No adjustment is necessary.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

6

Use the following information for Questions 15 & 16:

P Company regularly sells merchandise to its 80%-owned subsidiary, S Corporation.In 2013, P sold merchandise that cost $240,000 to S for $300,000.Half of this merchandise remained in S's December 31, 2013 inventory.During 2014, P sold merchandise that cost $375,000 to S for $468,000.Forty percent of this merchandise inventory remained in S's December 31, 2014 inventory.Selected income statement information for the two affiliates for the year 2014 is as follows:

Consolidated sales revenue for P and Subsidiary for 2014 are:

A)$2,907,000.

B)$3,000,000.

C)$3,205,500.

D)$3,375,000.

P Company regularly sells merchandise to its 80%-owned subsidiary, S Corporation.In 2013, P sold merchandise that cost $240,000 to S for $300,000.Half of this merchandise remained in S's December 31, 2013 inventory.During 2014, P sold merchandise that cost $375,000 to S for $468,000.Forty percent of this merchandise inventory remained in S's December 31, 2014 inventory.Selected income statement information for the two affiliates for the year 2014 is as follows:

Consolidated sales revenue for P and Subsidiary for 2014 are:

A)$2,907,000.

B)$3,000,000.

C)$3,205,500.

D)$3,375,000.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

7

The noncontrolling interest's share of the selling affiliate's profit on intercompany sales is considered to be realized under

A)partial elimination.

B)total elimination.

C)100% elimination.

D)both total and 100% elimination.

A)partial elimination.

B)total elimination.

C)100% elimination.

D)both total and 100% elimination.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

8

The workpaper entry in the year of sale to eliminate unrealized intercompany profit in ending inventory includes a

A)credit to Ending Inventory (Cost of Sales).

B)credit to Sales.

C)debit to Ending Inventory (Cost of Sales).

D)debit to Inventory - Balance Sheet.

A)credit to Ending Inventory (Cost of Sales).

B)credit to Sales.

C)debit to Ending Inventory (Cost of Sales).

D)debit to Inventory - Balance Sheet.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

9

The noncontrolling interest in consolidated income when the selling affiliate is an 80% owned subsidiary is calculated by multiplying the noncontrolling minoritydelete minority ownership percentage by the subsidiary's reported net income

A)plus unrealized profit in ending inventory less unrealized profit in beginning inventory.

B)plus realized profit in ending inventory less realized profit in beginning inventory.

C)less unrealized profit in ending inventory plus realized profit in beginning inventory.

D)less realized profit in ending inventory plus realized profit in beginning inventory.

A)plus unrealized profit in ending inventory less unrealized profit in beginning inventory.

B)plus realized profit in ending inventory less realized profit in beginning inventory.

C)less unrealized profit in ending inventory plus realized profit in beginning inventory.

D)less realized profit in ending inventory plus realized profit in beginning inventory.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

10

Petunia Company acquired an 80% interest in Shaman Company in 201320132013 just once.In 2014 and 2015, Sutton reported net income of $400,000 and $480,000, respectively.During 2014, Shaman sold $80,000 of merchandise to Petunia for a $20,000 profit.Petunia sold the merchandise to outsiders during 2015 for $140,000.For consolidation purposes, what is the noncontrolling interest's share of Shaman's 2014 and 2015 net income?

A)$90,000 and $96,000.

B)$100,000 and $76,000.

C)$84,000 and $92,000.

D)$76,000 and $100,000.

A)$90,000 and $96,000.

B)$100,000 and $76,000.

C)$84,000 and $92,000.

D)$76,000 and $100,000.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

11

Use the following information for Questions 15 & 16:

P Company regularly sells merchandise to its 80%-owned subsidiary, S Corporation.In 2013, P sold merchandise that cost $240,000 to S for $300,000.Half of this merchandise remained in S's December 31, 2013 inventory.During 2014, P sold merchandise that cost $375,000 to S for $468,000.Forty percent of this merchandise inventory remained in S's December 31, 2014 inventory.Selected income statement information for the two affiliates for the year 2014 is as follows:

Consolidated cost of goods sold for P Company and Subsidiary for 2014 are:

A)$2,260,500.

B)$2,268,000.

C)$2,276,700.

D)$2,737,500.

P Company regularly sells merchandise to its 80%-owned subsidiary, S Corporation.In 2013, P sold merchandise that cost $240,000 to S for $300,000.Half of this merchandise remained in S's December 31, 2013 inventory.During 2014, P sold merchandise that cost $375,000 to S for $468,000.Forty percent of this merchandise inventory remained in S's December 31, 2014 inventory.Selected income statement information for the two affiliates for the year 2014 is as follows:

Consolidated cost of goods sold for P Company and Subsidiary for 2014 are:

A)$2,260,500.

B)$2,268,000.

C)$2,276,700.

D)$2,737,500.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

12

In determining controlling interest in consolidated income in the consolidated financial statements, unrealized intercompany profit on inventory acquired by a parent from its subsidiary should:

A)not be eliminated.

B)be eliminated in full.

C)be eliminated to the extent of the parent company's controlling interest in the subsidiary.

D)be eliminated to the extent of the noncontrolling interest in the subsidiary.

A)not be eliminated.

B)be eliminated in full.

C)be eliminated to the extent of the parent company's controlling interest in the subsidiary.

D)be eliminated to the extent of the noncontrolling interest in the subsidiary.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

13

Use the following information for Questions 17 & 18:

P Company owns an 80% interest in S Company.During 2014, S sells merchandise to P for $200,000 at a profit of $40,000.On December 31, 2014, 50% of this merchandise is included in P's inventory.Income statements for P and S are summarized below:

Controlling interest in consolidated net income for 2014 is:

A)$300,000.

B)$380,000.

C)$396,000.

D)$420,000.

P Company owns an 80% interest in S Company.During 2014, S sells merchandise to P for $200,000 at a profit of $40,000.On December 31, 2014, 50% of this merchandise is included in P's inventory.Income statements for P and S are summarized below:

Controlling interest in consolidated net income for 2014 is:

A)$300,000.

B)$380,000.

C)$396,000.

D)$420,000.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

14

A parent company regularly sells merchandise to its 80%-owned subsidiary.Which of the following statements describes the computation of noncontrolling interest income?

A)the subsidiary's net income times 20%.

B)(the subsidiary's net income x 20%) + unrealized profits in the beginning inventory - unrealized profits in the ending inventory.

C)(the subsidiary's net income + unrealized profits in the beginning inventory - unrealized profits in the ending inventory) × 20%.

D)(the subsidiary's net income + unrealized profits in the ending inventory - unrealized profits in the beginning inventory) × 20%.

A)the subsidiary's net income times 20%.

B)(the subsidiary's net income x 20%) + unrealized profits in the beginning inventory - unrealized profits in the ending inventory.

C)(the subsidiary's net income + unrealized profits in the beginning inventory - unrealized profits in the ending inventory) × 20%.

D)(the subsidiary's net income + unrealized profits in the ending inventory - unrealized profits in the beginning inventory) × 20%.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

15

Failure to eliminate intercompany sales would result in an overstatement of consolidated

A)net income.

B)gross profit.

C)cost of sales.

D)all of these.

A)net income.

B)gross profit.

C)cost of sales.

D)all of these.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

16

P Corporation acquired a 60% interest in S Corporation on January 1, 2014, at book value equal to fair value.During 2014, P sold merchandise that cost $135,000 to S for $189,000.One-third of this merchandise remained in S's inventory at December 31, 2014.S reported net income of $120,000 for 2014.P's income from S for 2014 is:

A)$36,000.

B)$50,400.

C)$54,000.

D)$61,200.

A)$36,000.

B)$50,400.

C)$54,000.

D)$61,200.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

17

P Corporation acquired a 60% interest in S Corporation on January 1, 2014, at book value equal to fair value.During 2014, P sold merchandise that cost $225,000 to S for $315,000.One-third of this merchandise remained in S's inventory at December 31, 2014.S reported net income of $200,000 for 2014.P's income from S for 2014 is:

A)$60,000.

B)$90,000.

C)$120,000.

D)$102,000.

A)$60,000.

B)$90,000.

C)$120,000.

D)$102,000.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

18

A 90% owned subsidiary sold merchandise at a profit to its parent company near the end of 2013.Under the partial equity method, the workpaper entry in 2014 to recognize the intercompany profit in beginning inventory realized during 2014 includes a debit to

A)Retained Earnings - P.

B)Noncontrolling interest.

C)Cost of Sales.

D)both Retained Earnings - P and Noncontrolling Interest.

A)Retained Earnings - P.

B)Noncontrolling interest.

C)Cost of Sales.

D)both Retained Earnings - P and Noncontrolling Interest.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

19

Sales from one subsidiary to another are called

A)downstream sales.

B)upstream sales.

C)intersubsidiary sales.

D)horizontal sales.

A)downstream sales.

B)upstream sales.

C)intersubsidiary sales.

D)horizontal sales.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

20

Noncontrolling interest in consolidated income is never affected by

A)upstream sales.

B)downstream sales.

C)horizontal sales.

D)Noncontrolling interest is affected by all sales.

A)upstream sales.

B)downstream sales.

C)horizontal sales.

D)Noncontrolling interest is affected by all sales.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

21

Use the following information for Questions 24 & 25:

P Company owns an 80% interest in S Company.During 2014, S sells merchandise to P for $150,000 at a profit of $30,000.On December 31, 2014, 50% of this merchandise is included in P's inventory.Income statements for P and S are summarized below:

Controlling interest in consolidated net income for 2014 is:

A)$225,000.

B)$285,000.

C)$297,000.

D)$315,000.

P Company owns an 80% interest in S Company.During 2014, S sells merchandise to P for $150,000 at a profit of $30,000.On December 31, 2014, 50% of this merchandise is included in P's inventory.Income statements for P and S are summarized below:

Controlling interest in consolidated net income for 2014 is:

A)$225,000.

B)$285,000.

C)$297,000.

D)$315,000.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

22

What is the essential procedural difference between workpaper eliminating entries for unrealized intercompany profit made when the selling affiliate is a less than wholly owned subsidiary and those made when the selling affiliate is the parent company or a wholly owned subsidiary?

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

23

Define the controlling interest in consolidated net income using the t-account or analytical approach.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

24

On January 1, 2014, Pharma Company purchased a 90% interest in Sandy Company for $2,800,000.At that time, Sandy had $1,840,000 of common stock and $360,000 of retained earnings.The difference between implied and book value was allocated to the following assets of Sandy Company:

The plant and equipment had a 10-year remaining useful life on January 1, 2014.

During 2014, Pharma sold merchandise to Sandy at a 20% markup above cost.At December 31, 2014, Sandy still had $180,000 of merchandise in its inventory that it had purchased from Pharma.In 2014, Pharma reported net income from independent operations of $1,600,000, while Sandy reported net income of $600,000.

Required:

A.Prepare the workpaper entry to allocate, amortize, and depreciate the difference between implied and book value for 2014.

B.Calculate controlling interest in consolidated net income for 2014.

The plant and equipment had a 10-year remaining useful life on January 1, 2014.

During 2014, Pharma sold merchandise to Sandy at a 20% markup above cost.At December 31, 2014, Sandy still had $180,000 of merchandise in its inventory that it had purchased from Pharma.In 2014, Pharma reported net income from independent operations of $1,600,000, while Sandy reported net income of $600,000.

Required:

A.Prepare the workpaper entry to allocate, amortize, and depreciate the difference between implied and book value for 2014.

B.Calculate controlling interest in consolidated net income for 2014.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

25

Are the adjustments to the noncontrolling interest for the effects of intercompany profit eliminations illustrated in this text necessary for fair presentation in accordance with generally accepted accounting principles? Explain.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

26

Does the elimination of the effects of intercompany sales of merchandise always affect the amount of reported consolidated net income? Explain.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

27

Puma Company owns 80% of the common stock of Smarte Company.Puma sells merchandise to Smarte at 20% above cost.During 2014 and 2015, intercompany sales amounted to $1,080,000 and $1,200,000 respectively.At the end of 2014, Smarte had one-fifth of the goods purchased that year from Puma in its ending inventory.Smarte's 2015 ending inventory contained one-fourth of that year's purchases from Puma.There were no intercompany sales prior to 2014.

Puma reported net income from its own operations of $720,000 in 2014 and $760,000 in 2015.Smarte reported net income of $400,000 in 2014 and $460,000 in 2015.Neither company declared dividends in either year.

Required:

A.Prepare in general journal form all entries necessary on the consolidated statements workpapers to eliminate the effects of the intercompany sales for both 2014 and 2015.

B.Calculate controlling interest in consolidated net income for 2015.

Puma reported net income from its own operations of $720,000 in 2014 and $760,000 in 2015.Smarte reported net income of $400,000 in 2014 and $460,000 in 2015.Neither company declared dividends in either year.

Required:

A.Prepare in general journal form all entries necessary on the consolidated statements workpapers to eliminate the effects of the intercompany sales for both 2014 and 2015.

B.Calculate controlling interest in consolidated net income for 2015.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

28

Use the following information for Questions 22 & 23:

P Company regularly sells merchandise to its 80%-owned subsidiary, S Corporation.In 2013, P sold merchandise that cost $192,000 to S for $240,000.Half of this merchandise remained in S's December 31, 2013 inventory.During 2014, P sold merchandise that cost $300,000 to S for $375,000.Forty percent of this merchandise inventory remained in S's December 31, 2014 inventory.Selected income statement information for the two affiliates for the year 2014 is as follows:

Consolidated cost of goods sold for P Company and Subsidiary for 2014 are:

A)$1,809,000.

B)$1,815,000.

C)$1,821,000.

D)$2,190,000.

P Company regularly sells merchandise to its 80%-owned subsidiary, S Corporation.In 2013, P sold merchandise that cost $192,000 to S for $240,000.Half of this merchandise remained in S's December 31, 2013 inventory.During 2014, P sold merchandise that cost $300,000 to S for $375,000.Forty percent of this merchandise inventory remained in S's December 31, 2014 inventory.Selected income statement information for the two affiliates for the year 2014 is as follows:

Consolidated cost of goods sold for P Company and Subsidiary for 2014 are:

A)$1,809,000.

B)$1,815,000.

C)$1,821,000.

D)$2,190,000.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

29

The following balances were taken from the records of S Company:

P Company owns 80% of the common stock of S Company.During 2014, P Company purchased merchandise from S Company for $4,000,000.S Company sells merchandise to P Company at cost plus 25% of cost.On December 31, 2014, merchandise purchased from S Company for $1,250,000 remains in the inventory of P Company.On January 1, 2014, P Company's inventory contained merchandise purchased from S Company for $525,000.The affiliated companies file a consolidated income tax return.There was no difference between the implied value and the book value of net assets acquired.

Required:

A.Prepare all workpaper entries necessitated by the intercompany sales of merchandise.

B.Compute noncontrolling interest in consolidated income for 2014.

C.Compute noncontrolling interest in consolidated net assets on December 31, 2014.

P Company owns 80% of the common stock of S Company.During 2014, P Company purchased merchandise from S Company for $4,000,000.S Company sells merchandise to P Company at cost plus 25% of cost.On December 31, 2014, merchandise purchased from S Company for $1,250,000 remains in the inventory of P Company.On January 1, 2014, P Company's inventory contained merchandise purchased from S Company for $525,000.The affiliated companies file a consolidated income tax return.There was no difference between the implied value and the book value of net assets acquired.

Required:

A.Prepare all workpaper entries necessitated by the intercompany sales of merchandise.

B.Compute noncontrolling interest in consolidated income for 2014.

C.Compute noncontrolling interest in consolidated net assets on December 31, 2014.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

30

P Company sells inventory costing $100,000 to its subsidiary, S Company, for $150,000.At the end of the current year, one-half of the goods re-mainsremains in S Company's inventory.Applying the lower of cost or market rule, S Company writes down this inventory to $60,000.What amount of intercompany profit should be eliminated on the consolidated statements workpaper?

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

31

Poole Company owns a 90% interest in Solumbra Company.The consolidated income statement drafted by the controller of Poole Company appeared as follows:

Required:

Prepare a corrected consolidated income statement for Poole Company and Slocum Company for the year ended December 31, 2014.

Required:

Prepare a corrected consolidated income statement for Poole Company and Slocum Company for the year ended December 31, 2014.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

32

Determination of the noncontrolling interest in consolidated net income differs depending on whether intercompany sales are downstream or upstream.Explain the difference in calculating noncontrolling interest for downstream and upstream sales.

Questions from the Textbook

Questions from the Textbook

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

33

Use the following information for Questions 22 & 23:

P Company regularly sells merchandise to its 80%-owned subsidiary, S Corporation.In 2013, P sold merchandise that cost $192,000 to S for $240,000.Half of this merchandise remained in S's December 31, 2013 inventory.During 2014, P sold merchandise that cost $300,000 to S for $375,000.Forty percent of this merchandise inventory remained in S's December 31, 2014 inventory.Selected income statement information for the two affiliates for the year 2014 is as follows:

Consolidated sales revenue for P and Subsidiary for 2014 are:

A)$2,325,000.

B)$2,400,000.

C)$2,565,000.

D)$2,700,000.

P Company regularly sells merchandise to its 80%-owned subsidiary, S Corporation.In 2013, P sold merchandise that cost $192,000 to S for $240,000.Half of this merchandise remained in S's December 31, 2013 inventory.During 2014, P sold merchandise that cost $300,000 to S for $375,000.Forty percent of this merchandise inventory remained in S's December 31, 2014 inventory.Selected income statement information for the two affiliates for the year 2014 is as follows:

Consolidated sales revenue for P and Subsidiary for 2014 are:

A)$2,325,000.

B)$2,400,000.

C)$2,565,000.

D)$2,700,000.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

34

Why are adjustments made to the calculation of the noncontrolling interest for the effects of intercompany profit in upstream but not in down-stream sales?

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

35

Past and proposed GAAP agree that unrealized intercompany profit should not be included in consolidated net income or assets.Briefly explain the preferred approach of eliminating intercompany profit.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

36

Use the following information for Questions 24 & 25:

P Company owns an 80% interest in S Company.During 2014, S sells merchandise to P for $150,000 at a profit of $30,000.On December 31, 2014, 50% of this merchandise is included in P's inventory.Income statements for P and S are summarized below:

Noncontrolling interest in income for 2014 is:

A)$3,000.

B)$14,400.

C)$15,000.

D)$18,000.

P Company owns an 80% interest in S Company.During 2014, S sells merchandise to P for $150,000 at a profit of $30,000.On December 31, 2014, 50% of this merchandise is included in P's inventory.Income statements for P and S are summarized below:

Noncontrolling interest in income for 2014 is:

A)$3,000.

B)$14,400.

C)$15,000.

D)$18,000.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

37

What procedure is used in the consolidated statements workpaper to adjust the noncontrolling interest in consolidated net assets at the be-ginningbeginning of the year for the effects of intercompany profits?

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

38

Pinta Company owns 90% of the common stock of Simplex Company.Simplex Company sells merchandise to Pinta Company at 25% above cost.During 2013 and 2014 such sales amounted to $800,000 and $1,020,000, respectively.At the end of each year, Pinta Company had in its inventory one-fourth of the amount of goods purchased from Simplex Company during that year.Pinta Company reported income of $1,500,000 from its independent operations in 2013 and $1,720,000 in 2014.Simplex Company reported net income of $600,000 in each year and did not declare any dividends in either year.There were no intercompany sales prior to 2013.

Required:

A.Prepare, in general journal form, all entries necessary on the 2014 consolidated statements workpaper to eliminate the effects of intercompany sales.

B.Calculate the amount of noncontrolling interest to be deducted from consolidated income in the consolidated income statement in 2014.

C.Calculate controlling interest in consolidated net income for 2014.

Required:

A.Prepare, in general journal form, all entries necessary on the 2014 consolidated statements workpaper to eliminate the effects of intercompany sales.

B.Calculate the amount of noncontrolling interest to be deducted from consolidated income in the consolidated income statement in 2014.

C.Calculate controlling interest in consolidated net income for 2014.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

39

Why is the gross profit on intercompany sales, rather than profit after deducting selling and administrative expenses, ordinarily eliminated from consolidated inventory balances?

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

40

Pine Company owns an 80% interest in Salad Company and a 90% interest in Tuna Company.During 2013 and 2014, intercompany sales of merchandise were made by all three companies.Total sales amounted to $2,400,000 in 2013, and $2,700,000 in 2014.The companies sold their merchandise at the following percentages above cost.

Pine 15%

Salad 20%

Tuna 25%

The amount of merchandise remaining in the 2014 beginning and ending inventories of the companies from these intercompany sales is shown below.

Reported net incomes (from independent operations including sales to affiliates) of Pine, Salad, and Tuna for 2014 were $3,600,000, $1,500,000, and $2,400,000, respectively.

Required:

A.Calculate the amount noncontrolling interest to be deducted from consolidated income in the consolidated income statement for 2014.

B.Calculate the controlling interest in consolidated net income for 2014.

Pine 15%

Salad 20%

Tuna 25%

The amount of merchandise remaining in the 2014 beginning and ending inventories of the companies from these intercompany sales is shown below.

Reported net incomes (from independent operations including sales to affiliates) of Pine, Salad, and Tuna for 2014 were $3,600,000, $1,500,000, and $2,400,000, respectively.

Required:

A.Calculate the amount noncontrolling interest to be deducted from consolidated income in the consolidated income statement for 2014.

B.Calculate the controlling interest in consolidated net income for 2014.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 40 flashcards in this deck.