Deck 12: General Equilibrium and the Efficiency of Perfect Competition

Full screen (f)

Question

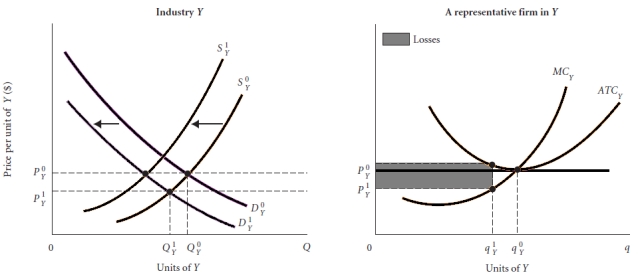

Use Figure 12.1 to answer the following question. Assume that this industry is currently enjoying normal economic profit and for whatever reason there is an increase in demand for the goods produced by this industry. Using general equilibrium analysis explain what will happen both in this industry and in industry Y which is perceived by consumers as being a product that is a substitute for product X.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

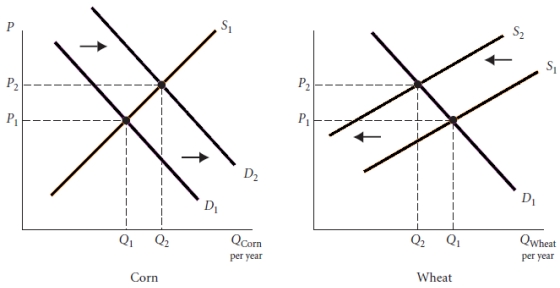

Assume that a farmer could just as easily plan corn as well as wheat. Explain what would happen using a supply and demand graph for both markets if suddenly there was a sustained increase in the demand for corn.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/44

Play

Full screen (f)

Deck 12: General Equilibrium and the Efficiency of Perfect Competition

1

Use Figure 12.1 to answer the following question. Assume that this industry is currently enjoying normal economic profit and for whatever reason there is an increase in demand for the goods produced by this industry. Using general equilibrium analysis explain what will happen both in this industry and in industry Y which is perceived by consumers as being a product that is a substitute for product X.

Initially, demand for X shifts from to This shift pushes the price of X up to creating profits. Demand for Y shifts down from to pushing the price of Y down to and creating losses. Firms have an incentive to leave sector Y and an incentive to enter sector X. Exiting sector Y shifts supply in that industry to raising price and eliminating losses. Entry shifts supply in X to S1 thus reducing and eliminating profits.

2

What does it mean for an industry to be considered an increasing cost industry?

An increasing cost industry is one where resource prices rise as the size of the industry expands.

3

What is efficiency?

Efficiency is the condition in which the economy is producing what people want at the least possible cost.

4

Why are perfectly competitive markets considered efficient?

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

5

In the early years of software development the industry had to train its own workers in developing code to build software applications. It was a very costly undertaking as software firms had to shoulder most of the training costs. However, over time the industry began to experience decreasing costs. How and why did this transformation take place?

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

6

Comment on the following statement: "Input and output markets should be considered separately because they operate independently of one another."

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

7

Comment on the following statement. "Once general equilibrium is achieved this will result in a long-run equilibrium as well."

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

8

How is it that economists can claim that perfectly competitive markets give people what they want?

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

9

What assumptions lead to the conclusion that final products are distributed efficiently among households?

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

10

Explain the difference between partial equilibrium analysis and general equilibrium analysis.

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

11

What assumptions lead to the conclusion that that the allocation of resources among firms is efficient.

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

12

What is partial equilibrium analysis?

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

13

Assume that the economy has two sectors, milk and orange juice, and that both sectors are initially in long-run competitive equilibrium. Milk and orange juice are substitute goods. Trace the effects of a change in preferences that increases the demand for orange juice.

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

14

What three decisions do firms make simultaneously?

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

15

Assume that a farmer could just as easily plan corn as well as wheat. Explain what would happen using a supply and demand graph for both markets if suddenly there was a sustained increase in the demand for corn.

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

16

The text asserts that the allocation of resources among firms is efficient. What assumptions must hold for this to be true?

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

17

Why is it difficult to determine whether an industry is operating efficiently when there is rapid technological process underway?

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

18

If all the assumptions of perfect competition hold, the result is an efficient, or Pareto optimal, allocation of resources. What is necessary to prove this?

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

19

Would the housing industry be characterized as an increasing, decreasing or a constant-cost industry? Explain your position.

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

20

What is general equilibrium?

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

21

A firm produces an output level at which price is greater than marginal cost. Explain why this is inefficient.

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

22

Antitrust cases that are brought to the courts by the Justice Department typically rely on perfect competition as a benchmark for lawyers to determine whether a firm is competitive or monopolistic. Why is this a troublesome criterion to use in prosecuting such cases?

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

23

Assume there is a toll bridge that is built by a private firm. It's been determined by cost accountants that the marginal cost that each automobile imposes is close to zero. If the bridge cost $1 million to build and 250,000 automobiles cross it each day what is the price that would be necessary for the firm to charge in order to achieve the key efficiency criteria of perfect competition? How might this be a problem for this private bridge company?

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

24

Is it theoretically possible for general equilibrium to be attained? Is it likely that general equilibrium will be attained? Explain.

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

25

Why does the model of perfect competition imply that firms will produce the products that households want the most?

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

26

Why does the model of perfect competition imply that there will be an efficient allocation of resources among firms?

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

27

Why does an efficient distribution of outputs among households occur in perfectly competitive markets?

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

28

Create an example of a Pareto efficient trade. Make sure that you explain why such a trade is Pareto efficient.

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

29

What condition must be satisfied so that society is producing the efficient mix of output? Why does this condition guarantee efficiency?

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

30

What is Pareto optimality?

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

31

If the economy were truly made of industries that fit the textbook definition of perfect competition what do you expect would be a major disadvantage of this from the consumer's perspective?

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

32

Use the three basic questions to describe why perfect competition is efficient.

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

33

When parents inoculate their children from communicable diseases prior to sending them off to school they not only provide their own children a benefit but also bestow a benefit on every other student at the school. There are now fewer students who can pass on these types of diseases. However, parents are not likely to take into account the fact that their actions create this external benefit. Therefore, economists argue that the market on its own may not provide for the optimal level of inoculations. What methods might work to get parents to take into account the external benefit when deciding whether to inoculate their children?

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

34

What three assumptions must hold for the allocation of resources among firms to be efficient?

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

35

Create an example of a trade that is not Pareto efficient. Make sure that you explain why such a trade is not Pareto efficient.

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

36

What are the three basic economic questions that must be answered by all societies?

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

37

Define public goods. Give an example of a public good. Explain why private firms will not generally produce public goods.

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

38

Students arriving late to class are a potential negative externality because their tardiness may interrupt the instructor and distract students. Can you think of any way in which this externality could be curbed? That is, can you think of any methods that could be employed to internalize this negative externality?

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

39

How is a potentially efficient change different from a Pareto optimal change?

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

40

Do the assumptions of the perfectly competitive model describe all real-world markets? Explain.

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

41

What is meant by market failure?

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

42

Explain the condition where society would be better off when more of a good is produced.

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

43

What is imperfect competition?

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

44

Define "externality." Give an example of an external cost. Explain why resources will not be allocated efficiently if externalities are present. How can the problem of externalities be addressed?

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 44 flashcards in this deck.