Deck 14: Non-Current Liabilities

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

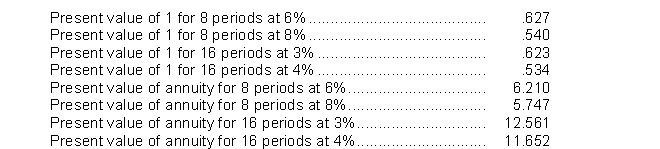

Use the following information for questions.issued eight-year bonds with a face value of $1,000,000 and a stated interest rate of 6%, payable semiannually on June 30 and December 31.The bonds were sold to yield 8%.Table values are:

The present value of the interest is

A)$344,820.

B)$349,560.

C)$372,600.

D)$376,830.

The present value of the interest is

A)$344,820.

B)$349,560.

C)$372,600.

D)$376,830.

Question

Use the following information for questions.issued eight-year bonds with a face value of $1,000,000 and a stated interest rate of 6%, payable semiannually on June 30 and December 31.The bonds were sold to yield 8%.Table values are:

Downing Company issues $5,000,000, 6%, 5-year bonds dated January 1, 2010 on January 1, 2010.The bonds pay interest semiannually on June 30 and December 31.The bonds are issued to yield 5%.What are the proceeds from the bond issue?

A)$5,000,000

B)$5,216,494

C)$5,218,809

D)$5,217,308

Downing Company issues $5,000,000, 6%, 5-year bonds dated January 1, 2010 on January 1, 2010.The bonds pay interest semiannually on June 30 and December 31.The bonds are issued to yield 5%.What are the proceeds from the bond issue?

A)$5,000,000

B)$5,216,494

C)$5,218,809

D)$5,217,308

Question

Question

Question

Question

Question

Question

Use the following information for questions.issued eight-year bonds with a face value of $1,000,000 and a stated interest rate of 6%, payable semiannually on June 30 and December 31.The bonds were sold to yield 8%.Table values are:

The issue price of the bonds is

A)$883,560.

B)$884,820.

C)$889,560.

D)$999,600.

The issue price of the bonds is

A)$883,560.

B)$884,820.

C)$889,560.

D)$999,600.

Question

Question

Question

Question

Question

Question

Use the following information for questions.issued eight-year bonds with a face value of $1,000,000 and a stated interest rate of 6%, payable semiannually on June 30 and December 31.The bonds were sold to yield 8%.Table values are:

Feller Company issues $20,000,000 of 10-year, 9% bonds on March 1, 2010 at 97 plus accrued interest.The bonds are dated January 1, 2010, and pay interest on June 30 and December 31.What is the total cash received on the issue date?

A)$19,400,000

B)$20,450,000

C)$19,700,000

D)$19,100,000

Feller Company issues $20,000,000 of 10-year, 9% bonds on March 1, 2010 at 97 plus accrued interest.The bonds are dated January 1, 2010, and pay interest on June 30 and December 31.What is the total cash received on the issue date?

A)$19,400,000

B)$20,450,000

C)$19,700,000

D)$19,100,000

Question

Question

Question

Use the following information for questions.issued eight-year bonds with a face value of $1,000,000 and a stated interest rate of 6%, payable semiannually on June 30 and December 31.The bonds were sold to yield 8%.Table values are:

The present value of the principal is

A)$534,000.

B)$540,000.

C)$623,000.

D)$627,000.

The present value of the principal is

A)$534,000.

B)$540,000.

C)$623,000.

D)$627,000.

Question

Question

Question

Question

Question

Question

Question

Question

Use the following information for questions.issued eight-year bonds with a face value of $1,000,000 and a stated interest rate of 6%, payable semiannually on June 30 and December 31.The bonds were sold to yield 8%.Table values are:

Everhart Company issues $10,000,000, 6%, 5-year bonds dated January 1, 2010 on January 1, 2010.The bonds pays interest semiannually on June 30 and December 31.The bonds are issued to yield 5%.What are the proceeds from the bond issue?

A)$10,000,000

B)$10,432,988

C)$10,437,618

D)$10,434,616

Everhart Company issues $10,000,000, 6%, 5-year bonds dated January 1, 2010 on January 1, 2010.The bonds pays interest semiannually on June 30 and December 31.The bonds are issued to yield 5%.What are the proceeds from the bond issue?

A)$10,000,000

B)$10,432,988

C)$10,437,618

D)$10,434,616

Question

Question

Question

Question

Question

Question

Question

Use the following information for questions.issued eight-year bonds with a face value of $1,000,000 and a stated interest rate of 6%, payable semiannually on June 30 and December 31.The bonds were sold to yield 8%.Table values are:

Farmer Company issues $10,000,000 of 10-year, 9% bonds on March 1, 2010 at 97 plus accrued interest.The bonds are dated January 1, 2010, and pay interest on June 30 and December 31.What is the total cash received on the issue date?

A)$9,700,000

B)$10,225,000

C)$9,850,000

D)$9,550,000

Farmer Company issues $10,000,000 of 10-year, 9% bonds on March 1, 2010 at 97 plus accrued interest.The bonds are dated January 1, 2010, and pay interest on June 30 and December 31.What is the total cash received on the issue date?

A)$9,700,000

B)$10,225,000

C)$9,850,000

D)$9,550,000

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/108

Play

Full screen (f)

Deck 14: Non-Current Liabilities

1

When bonds are issued at a discount, the bonds payable account is credited for the proceeds from the issue.

True

2

The cash paid for interest will always be greater than interest expense when using effective-interest amortization for a bond.

False

3

If the market rate is greater than the stated rate, bonds will be sold at a premium.

False

4

When bonds are issued at a premium, the bonds payable account is credited for the face amount.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

5

The semi-annual interest payment on a 6.5% HK$10,000,000 bond is HK$650,000.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

6

Bond issues that mature in installments are called serial bonds.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

7

The interest rate written in the terms of the bond indenture is called the effective yield or market rate.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

8

A bond may only be issued on an interest payment date.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

9

The process of interest-rate approximation is called imputation, and the resulting interest rate is called an imputed interest rate.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

10

The stated rate is the same as the coupon rate.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

11

If a long-term note payable has a stated interest rate, that rate should be considered to be the effective rate.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

12

The journal entry to record amortization of bond discount includes a debit to the bonds payable account.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

13

The proceeds of a bond with a face amount of ¥100,000,000 which sells at 98 will be ¥98,000,000.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

14

At any point during the term of the bond, the balance in the bonds payable account should be the carrying value of the bond.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

15

The proceeds of a bond with a face amount of ¥100,000,000 which sells at 102 will be ¥100,200,000.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

16

Amortization of bond premium reduces the balance in bonds payable.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

17

Amortization of a premium increases bond interest expense, while amortization of a discount decreases bond interest expense.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

18

A mortgage bond is referred to as a debenture bond.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

19

When a zero-interest bearing note is issued, the note payable account will be credited for the present value of the maturity value.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

20

Companies usually make bond interest payments semiannually, although the interest rate is generally expressed as an annual rate.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

21

The covenants and other terms of the agreement between the issuer of bonds and the lender are set forth in the

A)bond indenture.

B)bond debenture.

C)registered bond.

D)bond coupon.

A)bond indenture.

B)bond debenture.

C)registered bond.

D)bond coupon.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

22

The rate of interest actually earned by bondholders is called the

A)stated rate.

B)yield rate.

C)effective rate.

D)effective yield or market rate.

A)stated rate.

B)yield rate.

C)effective rate.

D)effective yield or market rate.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

23

Under the effective-interest method of bond discount or premium amortization, the periodic interest expense is equal to

A)the stated (nominal) rate of interest multiplied by the face value of the bonds.

B)the market rate of interest multiplied by the face value of the bonds.

C)the stated rate multiplied by the beginning-of-period carrying amount of the bonds.

D)the market rate multiplied by the beginning-of-period carrying amount of the bonds.

A)the stated (nominal) rate of interest multiplied by the face value of the bonds.

B)the market rate of interest multiplied by the face value of the bonds.

C)the stated rate multiplied by the beginning-of-period carrying amount of the bonds.

D)the market rate multiplied by the beginning-of-period carrying amount of the bonds.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

24

Off-balance-sheet financing is an attempt to borrow monies in such a way to minimize the reporting of debt on the balance sheet.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

25

Under IFRS, subsidiaries in which the parent company holds a less than 50 percent interest do not have to be included in consolidated financial statements.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

26

Debt issuance costs are recorded as an asset and amortized to expense over the life of the bond.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

27

The interest rate written in the terms of the bond indenture is known as the

A)coupon rate.

B)nominal rate.

C)stated rate.

D)coupon rate, nominal rate, or stated rate.

A)coupon rate.

B)nominal rate.

C)stated rate.

D)coupon rate, nominal rate, or stated rate.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

28

Use the following information for questions.issued $100,000 of ten-year, 10% bonds that pay interest semiannually.The bonds are sold to yield 8%.

One step in calculating the issue price of the bonds is to multiply the principal by the table value for

A)10 periods and 10% from the present value of 1 table.

B)20 periods and 5% from the present value of 1 table.

C)10 periods and 8% from the present value of 1 table.

D)20 periods and 4% from the present value of 1 table.

One step in calculating the issue price of the bonds is to multiply the principal by the table value for

A)10 periods and 10% from the present value of 1 table.

B)20 periods and 5% from the present value of 1 table.

C)10 periods and 8% from the present value of 1 table.

D)20 periods and 4% from the present value of 1 table.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

29

When the effective-interest method is used to amortize bond premium or discount, the periodic amortization will

A)increase if the bonds were issued at a discount.

B)decrease if the bonds were issued at a premium.

C)increase if the bonds were issued at a premium.

D)increase if the bonds were issued at either a discount or a premium.

A)increase if the bonds were issued at a discount.

B)decrease if the bonds were issued at a premium.

C)increase if the bonds were issued at a premium.

D)increase if the bonds were issued at either a discount or a premium.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

30

When the interest payment dates of a bond are May 1 and November 1, and a bond issue is sold on June 1, the amount of cash received by the issuer will be

A)decreased by accrued interest from June 1 to November 1.

B)decreased by accrued interest from May 1 to June 1.

C)increased by accrued interest from June 1 to November 1.

D)increased by accrued interest from May 1 to June 1.

A)decreased by accrued interest from June 1 to November 1.

B)decreased by accrued interest from May 1 to June 1.

C)increased by accrued interest from June 1 to November 1.

D)increased by accrued interest from May 1 to June 1.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

31

The times interest earned ratio is computed by dividing income before interest expense by interest expense.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

32

IFRS recognition criteria for environment liabilities are more stringent than that of US GAAP.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

33

The debt to total assets ratio will go up if an equal amount of assets and liabilities are added to the balance sheet.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

34

Use the following information for questions.issued $100,000 of ten-year, 10% bonds that pay interest semiannually.The bonds are sold to yield 8%.

Another step in calculating the issue price of the bonds is to

A)multiply $10,000 by the table value for 10 periods and 10% from the present value of an annuity table.

B)multiply $10,000 by the table value for 20 periods and 5% from the present value of an annuity table.

C)multiply $10,000 by the table value for 20 periods and 4% from the present value of an annuity table.

D)none of these.

Another step in calculating the issue price of the bonds is to

A)multiply $10,000 by the table value for 10 periods and 10% from the present value of an annuity table.

B)multiply $10,000 by the table value for 20 periods and 5% from the present value of an annuity table.

C)multiply $10,000 by the table value for 20 periods and 4% from the present value of an annuity table.

D)none of these.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

35

If a company plans to retire long-term debt from a bond retirement fund, it should report the debt as current.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

36

Reich, Inc.issued bonds with a maturity amount of $200,000 and a maturity ten years from date of issue.If the bonds were issued at a premium, this indicates that

A)the effective yield or market rate of interest exceeded the stated (nominal) rate.

B)the nominal rate of interest exceeded the market rate.

C)the market and nominal rates coincided.

D)no necessary relationship exists between the two rates.

A)the effective yield or market rate of interest exceeded the stated (nominal) rate.

B)the nominal rate of interest exceeded the market rate.

C)the market and nominal rates coincided.

D)no necessary relationship exists between the two rates.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

37

The replacement of an existing bond issue with a new one is called refunding.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

38

Amortization of the discount on a zero-interest bearing note decreases the balance in notes payable.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

39

If bonds are issued between interest dates, the entry on the books of the issuing corporation could include a

A)debit to Interest Payable.

B)credit to Interest Receivable.

C)credit to Interest Expense.

D)credit to Unearned Interest.

A)debit to Interest Payable.

B)credit to Interest Receivable.

C)credit to Interest Expense.

D)credit to Unearned Interest.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

40

The IASB's position is that fair value measurement for financial liabilities is more relevant and understandable than amortized cost.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

41

Use the following information for questions.issued eight-year bonds with a face value of $1,000,000 and a stated interest rate of 6%, payable semiannually on June 30 and December 31.The bonds were sold to yield 8%.Table values are:

The present value of the interest is

A)$344,820.

B)$349,560.

C)$372,600.

D)$376,830.

The present value of the interest is

A)$344,820.

B)$349,560.

C)$372,600.

D)$376,830.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

42

Use the following information for questions.issued eight-year bonds with a face value of $1,000,000 and a stated interest rate of 6%, payable semiannually on June 30 and December 31.The bonds were sold to yield 8%.Table values are:

Downing Company issues $5,000,000, 6%, 5-year bonds dated January 1, 2010 on January 1, 2010.The bonds pay interest semiannually on June 30 and December 31.The bonds are issued to yield 5%.What are the proceeds from the bond issue?

A)$5,000,000

B)$5,216,494

C)$5,218,809

D)$5,217,308

Downing Company issues $5,000,000, 6%, 5-year bonds dated January 1, 2010 on January 1, 2010.The bonds pay interest semiannually on June 30 and December 31.The bonds are issued to yield 5%.What are the proceeds from the bond issue?

A)$5,000,000

B)$5,216,494

C)$5,218,809

D)$5,217,308

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

43

A discount on notes payable is charged to interest expense

A)equally over the life of the note.

B)only in the year the note is issued.

C)using the effective-interest method.

D)only in the year the note matures.

A)equally over the life of the note.

B)only in the year the note is issued.

C)using the effective-interest method.

D)only in the year the note matures.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

44

The times interest earned ratio is computed by dividing

A)net income by interest expense.

B)income before taxes by interest expense.

C)income before income taxes and interest expense by interest expense.

D)net income and interest expense by interest expense.

A)net income by interest expense.

B)income before taxes by interest expense.

C)income before income taxes and interest expense by interest expense.

D)net income and interest expense by interest expense.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

45

Which of the following must be disclosed relative to long-term debt maturities and sinking fund requirements?

A)The present value of future payments for sinking fund requirements and long-term debt maturities during each of the next five years.

B)The present value of scheduled interest payments on long-term debt during each of the next five years.

C)The amount of scheduled interest payments on long-term debt during each of the next five years.

D)The amount of future payments for sinking fund requirements and long-term debt maturities during each of the next five years.

A)The present value of future payments for sinking fund requirements and long-term debt maturities during each of the next five years.

B)The present value of scheduled interest payments on long-term debt during each of the next five years.

C)The amount of scheduled interest payments on long-term debt during each of the next five years.

D)The amount of future payments for sinking fund requirements and long-term debt maturities during each of the next five years.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

46

In a debt settlement in which the debt is continued with modified terms, a gain should be recognized at the date of settlement whenever the

A)carrying amount of the debt is less than the total future cash flows.

B)carrying amount of the debt is greater than the present value of the future cash flows.

C)present value of the debt is less than the present value of the future cash flows.

D)present value of the debt is greater than the present value of the future cash flows.

A)carrying amount of the debt is less than the total future cash flows.

B)carrying amount of the debt is greater than the present value of the future cash flows.

C)present value of the debt is less than the present value of the future cash flows.

D)present value of the debt is greater than the present value of the future cash flows.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

47

In a debt extinguishment in which the debt is continued with modified terms and the carrying value of the debt is more than the fair value of the debt,

A)a loss should be recognized by the debtor.

B)a new effective-interest rate must be computed.

C)a gain should be recognized by the debtor.

D)no interest expense should be recognized in the future.

A)a loss should be recognized by the debtor.

B)a new effective-interest rate must be computed.

C)a gain should be recognized by the debtor.

D)no interest expense should be recognized in the future.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

48

Use the following information for questions.issued eight-year bonds with a face value of $1,000,000 and a stated interest rate of 6%, payable semiannually on June 30 and December 31.The bonds were sold to yield 8%.Table values are:

The issue price of the bonds is

A)$883,560.

B)$884,820.

C)$889,560.

D)$999,600.

The issue price of the bonds is

A)$883,560.

B)$884,820.

C)$889,560.

D)$999,600.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

49

All of the following are differences between IFRS and U.S.GAAP in according for liabilities except:

A)When a bond is issued at a discount, U.S.GAAP records the discount in a separate contra-liability account.IFRS records the bond net of the discount.

B)Under IFRS, bond issuance costs reduces the carrying value of the debt.Under U.S.GAAP, these costs are recorded as an asset and amortized to expense over the term of the bond.

C)U.S.GAAP, but not IFRS uses the term "troubled debt restructurings."

D)U.S.GAAP, but not IFRS uses the term "provisions" for contingent liabilities which are accrued.

A)When a bond is issued at a discount, U.S.GAAP records the discount in a separate contra-liability account.IFRS records the bond net of the discount.

B)Under IFRS, bond issuance costs reduces the carrying value of the debt.Under U.S.GAAP, these costs are recorded as an asset and amortized to expense over the term of the bond.

C)U.S.GAAP, but not IFRS uses the term "troubled debt restructurings."

D)U.S.GAAP, but not IFRS uses the term "provisions" for contingent liabilities which are accrued.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

50

Bond issuance costs, including the printing costs and legal fees associated with the issuance, should be

A)expensed in the period when the debt is issued.

B)recorded as a reduction in the carrying value of bonds payable.

C)accumulated in a deferred charge account and amortized over the life of the bonds.

D)reported as an expense in the period the bonds mature or are retired.

A)expensed in the period when the debt is issued.

B)recorded as a reduction in the carrying value of bonds payable.

C)accumulated in a deferred charge account and amortized over the life of the bonds.

D)reported as an expense in the period the bonds mature or are retired.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

51

In a debt extinguishment in which the debt is settled by a transfer of assets with a fair value less than the carrying amount of the debt, the debtor would recognize

A)no gain or loss on the settlement.

B)a gain on the settlement.

C)a loss on the settlement.

D)none of these.

A)no gain or loss on the settlement.

B)a gain on the settlement.

C)a loss on the settlement.

D)none of these.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

52

When a note payable is exchanged for property, goods, or services, the stated interest rate is presumed to be fair unless

A)no interest rate is stated.

B)the stated interest rate is unreasonable.

C)the stated face amount of the note is materially different from the current cash sales price for similar items or from current fair value of the note.

D)any of these.

A)no interest rate is stated.

B)the stated interest rate is unreasonable.

C)the stated face amount of the note is materially different from the current cash sales price for similar items or from current fair value of the note.

D)any of these.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

53

The debt to total assets ratio is computed by dividing

A)current liabilities by total assets.

B)long-term liabilities by total assets.

C)total liabilities by total assets.

D)total assets by total liabilities.

A)current liabilities by total assets.

B)long-term liabilities by total assets.

C)total liabilities by total assets.

D)total assets by total liabilities.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

54

Use the following information for questions.issued eight-year bonds with a face value of $1,000,000 and a stated interest rate of 6%, payable semiannually on June 30 and December 31.The bonds were sold to yield 8%.Table values are:

Feller Company issues $20,000,000 of 10-year, 9% bonds on March 1, 2010 at 97 plus accrued interest.The bonds are dated January 1, 2010, and pay interest on June 30 and December 31.What is the total cash received on the issue date?

A)$19,400,000

B)$20,450,000

C)$19,700,000

D)$19,100,000

Feller Company issues $20,000,000 of 10-year, 9% bonds on March 1, 2010 at 97 plus accrued interest.The bonds are dated January 1, 2010, and pay interest on June 30 and December 31.What is the total cash received on the issue date?

A)$19,400,000

B)$20,450,000

C)$19,700,000

D)$19,100,000

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

55

When a note payable is issued for property, goods, or services, the present value of the note is measured by

A)the fair value of the property, goods, or services.

B)the fair value of the note.

C)using an imputed interest rate to discount all future payments on the note.

D)any of these.

A)the fair value of the property, goods, or services.

B)the fair value of the note.

C)using an imputed interest rate to discount all future payments on the note.

D)any of these.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

56

Note disclosures for long-term debt generally include all of the following except

A)assets pledged as security.

B)call provisions and conversion privileges.

C)restrictions imposed by the creditor.

D)names of specific creditors.

A)assets pledged as security.

B)call provisions and conversion privileges.

C)restrictions imposed by the creditor.

D)names of specific creditors.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

57

Use the following information for questions.issued eight-year bonds with a face value of $1,000,000 and a stated interest rate of 6%, payable semiannually on June 30 and December 31.The bonds were sold to yield 8%.Table values are:

The present value of the principal is

A)$534,000.

B)$540,000.

C)$623,000.

D)$627,000.

The present value of the principal is

A)$534,000.

B)$540,000.

C)$623,000.

D)$627,000.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

58

The amortization of a premium on bonds payable

A)decreases the balance of the bonds payable account.

B)increases the amount of interest expense reported.

C)decreases the carrying amount of the bond.

D)increases the cash payment to bondholders.

A)decreases the balance of the bonds payable account.

B)increases the amount of interest expense reported.

C)decreases the carrying amount of the bond.

D)increases the cash payment to bondholders.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

59

The printing costs and legal fees associated with the issuance of bonds should

A)be expensed when incurred.

B)be reported as a deduction from the face amount of bonds payable.

C)be recorded as a reduction of the bond issue amount and then amortized over the life of the bonds.

D)not be reported as an expense until the period the bonds mature or are retired.

A)be expensed when incurred.

B)be reported as a deduction from the face amount of bonds payable.

C)be recorded as a reduction of the bond issue amount and then amortized over the life of the bonds.

D)not be reported as an expense until the period the bonds mature or are retired.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

60

Which of the following is not a difference between IFRS and U.S.GAAP in according for non-current liabilities?

A)Non-current liabilities follow current liabilities on the statement of financial position under U.S.GAAP, but precede current liabilities under IFRS.

B)The criteria for recognizing environment liabilities is more stringent under U.S.GAAP compared to IFRS.

C)Bond issuance costs are recorded as a reduction of the carrying value of the debt under U.S.GAAP but are recorded as an asset and amortized to expense over the term of the debt under IFRS.

D)Under U.S.GAAP, bonds payable is recorded at the face amount and any premium or discount is recorded in a separate account.Under IFRS, bonds payable is recorded at the carrying value so no separate premium or discount accounts are used.

A)Non-current liabilities follow current liabilities on the statement of financial position under U.S.GAAP, but precede current liabilities under IFRS.

B)The criteria for recognizing environment liabilities is more stringent under U.S.GAAP compared to IFRS.

C)Bond issuance costs are recorded as a reduction of the carrying value of the debt under U.S.GAAP but are recorded as an asset and amortized to expense over the term of the debt under IFRS.

D)Under U.S.GAAP, bonds payable is recorded at the face amount and any premium or discount is recorded in a separate account.Under IFRS, bonds payable is recorded at the carrying value so no separate premium or discount accounts are used.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

61

A company issues $20,000,000, 7.8%, 20-year bonds to yield 8% on January 1, 2010.Interest is paid on June 30 and December 31.The proceeds from the bonds are $19,604,145.Using effective-interest amortization, what will the carrying value of the bonds be on the December 31, 2010 statement of financial position?

A)$19,612,643

B)$20,000,000

C)$19,625,125

D)$19,608,310

A)$19,612,643

B)$20,000,000

C)$19,625,125

D)$19,608,310

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

62

On January 2, 2010, a calendar-year corporation sold 8% bonds with a face value of $600,000.These bonds mature in five years, and interest is paid semiannually on June 30 and December 31.The bonds were sold for $553,600 to yield 10%.Using the effective-interest method of computing interest, how much should be charged to interest expense in 2010?

A)$48,000.

B)$55,360.

C)$55,544.

D)$60,000.

A)$48,000.

B)$55,360.

C)$55,544.

D)$60,000.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

63

At the beginning of 2010, Winston Corporation issued 10% bonds with a face value of $600,000.These bonds mature in five years, and interest is paid semiannually on June 30 and December 31.The bonds were sold for $555,840 to yield 12%.Winston uses a calendar-year reporting period.Using the effective-interest method of amortization, what amount of interest expense should be reported for 2010? (Round your answer to the nearest dollar.)

A)$66,500

B)$66,700

C)$66,901

D)$68,832

A)$66,500

B)$66,700

C)$66,901

D)$68,832

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

64

The following information applies to both questions

On October 1, 2010 Bartley Corporation issued 5%, 10-year bonds with a face value of $500,000 at 108 (a 4% yield).Interest is paid on October 1 and April 1, with any premiums or discounts amortized on an effective-interest basis.

The entry to record the issuance of the bonds would include a

A)credit of $12,500 to interest Payable.

B)credit of $540,000 to Bonds Payable.

C)credit of $500,000 to Bonds Payable.

D)debit of $40,000 to Bonds Payable.

On October 1, 2010 Bartley Corporation issued 5%, 10-year bonds with a face value of $500,000 at 108 (a 4% yield).Interest is paid on October 1 and April 1, with any premiums or discounts amortized on an effective-interest basis.

The entry to record the issuance of the bonds would include a

A)credit of $12,500 to interest Payable.

B)credit of $540,000 to Bonds Payable.

C)credit of $500,000 to Bonds Payable.

D)debit of $40,000 to Bonds Payable.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

65

Use the following information for questions.issued eight-year bonds with a face value of $1,000,000 and a stated interest rate of 6%, payable semiannually on June 30 and December 31.The bonds were sold to yield 8%.Table values are:

Everhart Company issues $10,000,000, 6%, 5-year bonds dated January 1, 2010 on January 1, 2010.The bonds pays interest semiannually on June 30 and December 31.The bonds are issued to yield 5%.What are the proceeds from the bond issue?

A)$10,000,000

B)$10,432,988

C)$10,437,618

D)$10,434,616

Everhart Company issues $10,000,000, 6%, 5-year bonds dated January 1, 2010 on January 1, 2010.The bonds pays interest semiannually on June 30 and December 31.The bonds are issued to yield 5%.What are the proceeds from the bond issue?

A)$10,000,000

B)$10,432,988

C)$10,437,618

D)$10,434,616

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

66

A company issues $5,000,000, 7.8%, 20-year bonds to yield 8% on January 1, 2010.Interest is paid on June 30 and December 31.The proceeds from the bonds are $4,901,036.Using effective-interest amortization, what will the carrying value of the bonds be on the December 31, 2010 statement of financial position?

A)$4,903,160

B)$5,000,000

C)$4,906,281

D)$4,902,077

A)$4,903,160

B)$5,000,000

C)$4,906,281

D)$4,902,077

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

67

At the beginning of 2010, Wallace Corporation issued 10% bonds with a face value of $900,000.These bonds mature in the five years, and interest is paid semiannually on June 30 and December 31.The bonds were sold for $833,760 to yield 12%.Wallace uses a calendar-year reporting period.Using the effective-interest method of amortization, what amount of interest expense should be reported for 2010? (Round your answer to the nearest dollar.)

A)$103,248

B)$100,353

C)$100,050

D)$99,750

A)$103,248

B)$100,353

C)$100,050

D)$99,750

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

68

Bangalor Company issues Rs10,000,000, 8%, 10-year bonds at 96.5 on July 1, 2011.Interest is paid on July 1 and January 1.The journal entry to record the issuance will include

A)a debit to cash for Rs10,000,000

B)a credit to cash for Rs9,650,000

C)a debit to discount on bonds payable for Rs350,000

D)a credit to bonds payable for Rs9,650,000

A)a debit to cash for Rs10,000,000

B)a credit to cash for Rs9,650,000

C)a debit to discount on bonds payable for Rs350,000

D)a credit to bonds payable for Rs9,650,000

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

69

Franzia Company issues €10,000,000, 7.8%, 20-year bonds to yield 8% on July 1, 2011.Interest is paid on July 1 and January 1.The proceeds from the bonds are €9,802,073.What amount of interest expense will be reported on the 2012 income statement?

A)€392,083

B)€780,000

C)€784,249

D)€784,419

A)€392,083

B)€780,000

C)€784,249

D)€784,419

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

70

On January 1, 2011, Chang Company sold HK$10,000,000 of its 10%, bonds for HK$8,852,960, a yield of 12%.Interest is payable semiannually on January 1 and July1.The June 30, 2011 entry to record the first interest payment will include

A)a debit to Bonds Payable for HK$531,178.

B)a credit to Bonds Payable for HK$1,062,355.

C)a debit to Cash for HK$600,000.

D)a credit to Interest Expense for HK$442,648.

A)a debit to Bonds Payable for HK$531,178.

B)a credit to Bonds Payable for HK$1,062,355.

C)a debit to Cash for HK$600,000.

D)a credit to Interest Expense for HK$442,648.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

71

A company issues $5,000,000, 7.8%, 20-year bonds to yield 8% on January 1, 2010.Interest is paid on June 30 and December 31.The proceeds from the bonds are $4,901,036.Using effective-interest amortization, how much interest expense will be recognized in 2010?

A)$195,000

B)$390,000

C)$392,124

D)$392,083

A)$195,000

B)$390,000

C)$392,124

D)$392,083

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

72

Use the following information for questions.issued eight-year bonds with a face value of $1,000,000 and a stated interest rate of 6%, payable semiannually on June 30 and December 31.The bonds were sold to yield 8%.Table values are:

Farmer Company issues $10,000,000 of 10-year, 9% bonds on March 1, 2010 at 97 plus accrued interest.The bonds are dated January 1, 2010, and pay interest on June 30 and December 31.What is the total cash received on the issue date?

A)$9,700,000

B)$10,225,000

C)$9,850,000

D)$9,550,000

Farmer Company issues $10,000,000 of 10-year, 9% bonds on March 1, 2010 at 97 plus accrued interest.The bonds are dated January 1, 2010, and pay interest on June 30 and December 31.What is the total cash received on the issue date?

A)$9,700,000

B)$10,225,000

C)$9,850,000

D)$9,550,000

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

73

Franzia Company issues €10,000,000, 7.8%, 20-year bonds to yield 8% on July 1, 2011.Interest is paid on July 1 and January 1.The proceeds from the bonds are $9,604,145.The balance reported in the bonds payable account on the December 31, 2011 statement of financial position?

A)€9,802,073

B)€9,804,156

C)€9,806,322

D)€10,000,000

A)€9,802,073

B)€9,804,156

C)€9,806,322

D)€10,000,000

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

74

A company issues $20,000,000, 7.8%, 20-year bonds to yield 8% on January 1, 2010.Interest is paid on June 30 and December 31.The proceeds from the bonds are $19,604,145.Using effective-interest amortization, how much interest expense will be recognized in 2010?

A)$780,000

B)$1,560,000

C)$1,568,498

D)$1,568,332

A)$780,000

B)$1,560,000

C)$1,568,498

D)$1,568,332

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

75

The following information applies to both questions

On October 1, 2010 Macklin Corporation issued 5%, 10-year bonds with a face value of $1,000,000 at 108 (a 4% yield).Interest is paid on October 1 and April 1, with any premiums or discounts amortized on an effective-interest basis.

The entry to record the issuance of the bonds would include a credit of

A)$25,000 to interest Payable.

B)$80,000 to Bonds Payable.

C)$1,000,000 to Bonds Payable.

D)$1,080,000 to Bonds Payable.

On October 1, 2010 Macklin Corporation issued 5%, 10-year bonds with a face value of $1,000,000 at 108 (a 4% yield).Interest is paid on October 1 and April 1, with any premiums or discounts amortized on an effective-interest basis.

The entry to record the issuance of the bonds would include a credit of

A)$25,000 to interest Payable.

B)$80,000 to Bonds Payable.

C)$1,000,000 to Bonds Payable.

D)$1,080,000 to Bonds Payable.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

76

On January 1, Martinez Inc.issued $3,000,000, 11% bonds for $3,195,000.The market rate of interest for these bonds is 10%.Interest is payable annually on December 31.Martinez uses the effective-interest method of amortizing bond premium.At the end of the first year, Martinez should report bonds payable of:

A)$3,185,130

B)$3,184,500

C)$3,173,550

D)$3,165,000

A)$3,185,130

B)$3,184,500

C)$3,173,550

D)$3,165,000

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

77

The following information applies to both questions

On October 1, 2010 Bartley Corporation issued 5%, 10-year bonds with a face value of $500,000 at 108 (a 4% yield).Interest is paid on October 1 and April 1, with any premiums or discounts amortized on an effective-interest basis.

Bond interest expense reported on the December 31, 2010 income statement of Bartley Corporation would be

A)$6,750

B)$10,800

C)$5,400

D)$6,250

On October 1, 2010 Bartley Corporation issued 5%, 10-year bonds with a face value of $500,000 at 108 (a 4% yield).Interest is paid on October 1 and April 1, with any premiums or discounts amortized on an effective-interest basis.

Bond interest expense reported on the December 31, 2010 income statement of Bartley Corporation would be

A)$6,750

B)$10,800

C)$5,400

D)$6,250

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

78

On January 1, 2010, Huber Co.sold 12% bonds with a face value of $600,000.The bonds mature in five years, and interest is paid semiannually on June 30 and December 31.The bonds were sold for $646,200 to yield 10%.Using the effective-interest method of amortization, interest expense for 2010 is

A)$60,000.

B)$64,436.

C)$64,620.

D)$72,000.

A)$60,000.

B)$64,436.

C)$64,620.

D)$72,000.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

79

On January 1, Patterson Inc.issued $5,000,000, 9% bonds for $4,695,000.The market rate of interest for these bonds is 10%.Interest is payable annually on December 31.Patterson uses the effective-interest method of amortizing bond discount.At the end of the first year, Patterson should report bonds payable of

A)$4,725,500.

B)$4,714,500.

C)$258,050.

D)$4,745,000.

A)$4,725,500.

B)$4,714,500.

C)$258,050.

D)$4,745,000.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

80

The following information applies to both questions

On October 1, 2010 Macklin Corporation issued 5%, 10-year bonds with a face value of $1,000,000 at 108 (a 4% yield).Interest is paid on October 1 and April 1, with any premiums or discounts amortized on an effective-interest basis.

Bond interest expense reported on the December 31, 2010 income statement of Macklin Corporation would be

A)$10,800

B)$12,500

C)$13,500

D)$21,600

On October 1, 2010 Macklin Corporation issued 5%, 10-year bonds with a face value of $1,000,000 at 108 (a 4% yield).Interest is paid on October 1 and April 1, with any premiums or discounts amortized on an effective-interest basis.

Bond interest expense reported on the December 31, 2010 income statement of Macklin Corporation would be

A)$10,800

B)$12,500

C)$13,500

D)$21,600

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 108 flashcards in this deck.