Deck 14: Long-Term Financial Liabilities

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Use the following information for questions.

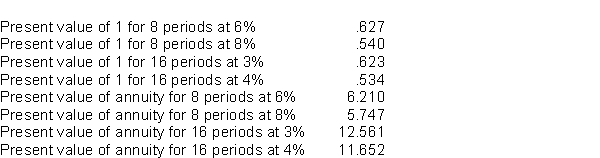

On January 1, 2017, Satin Corp.issued eight-year, 6% bonds with a face value of $500,000, with interest payable semi-annually on June 30 and December 31.The bonds were sold to yield 8%.Table values are:

The present value of the principal is

A)$267,000.

B)$270,000.

C)$311,500.

D)$313,500.

On January 1, 2017, Satin Corp.issued eight-year, 6% bonds with a face value of $500,000, with interest payable semi-annually on June 30 and December 31.The bonds were sold to yield 8%.Table values are:

The present value of the principal is

A)$267,000.

B)$270,000.

C)$311,500.

D)$313,500.

Question

Question

Question

Question

Question

Question

Use the following information for questions.

On January 1, 2017, Satin Corp.issued eight-year, 6% bonds with a face value of $500,000, with interest payable semi-annually on June 30 and December 31.The bonds were sold to yield 8%.Table values are:

The issue price of the bonds is

A)$441,780.

B)$442,410.

C)$444,780.

D)$499,800.

On January 1, 2017, Satin Corp.issued eight-year, 6% bonds with a face value of $500,000, with interest payable semi-annually on June 30 and December 31.The bonds were sold to yield 8%.Table values are:

The issue price of the bonds is

A)$441,780.

B)$442,410.

C)$444,780.

D)$499,800.

Question

Question

Question

Question

Use the following information for questions.

On January 1, 2017, Satin Corp.issued eight-year, 6% bonds with a face value of $500,000, with interest payable semi-annually on June 30 and December 31.The bonds were sold to yield 8%.Table values are:

The present value of the interest is

A)$172,410.

B)$174,780.

C)$186,300.

D)$188,415.

On January 1, 2017, Satin Corp.issued eight-year, 6% bonds with a face value of $500,000, with interest payable semi-annually on June 30 and December 31.The bonds were sold to yield 8%.Table values are:

The present value of the interest is

A)$172,410.

B)$174,780.

C)$186,300.

D)$188,415.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Continental Company's 2017 financial statements contain the following selected data:  Continental's times interest earned for 2017 is

Continental's times interest earned for 2017 is

A)8 times.

B)11 times.

C)12 times.

D)13 times.

Continental's times interest earned for 2017 isA)8 times.

B)11 times.

C)12 times.

D)13 times.

Question

Pineapple owes Dole a $600,000, 12%, three-year note dated December 31, 2015.Pineapple has been experiencing financial difficulties, and still owes accrued interest of $72,000 on this note at December 31, 2017.Under a troubled debt restructuring, on December 31, 2017, Dole agrees to settle the note plus the accrued interest for land that Pineapple owns, which has a fair value of $540,000.Pineapple's original cost of the land is $435,000.Ignoring income taxes, on its 2017 income statement, what should Pineapple report as a result of the troubled debt restructuring?

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/62

Play

Full screen (f)

Deck 14: Long-Term Financial Liabilities

1

If bonds are issued between interest dates, the entry on the books of the issuing corporation could include a

A)debit to Interest Payable.

B)credit to Interest Receivable.

C)credit to Interest Expense.

D)credit to Unearned Interest.

A)debit to Interest Payable.

B)credit to Interest Receivable.

C)credit to Interest Expense.

D)credit to Unearned Interest.

C

2

If bonds are initially sold at a discount and the straight-line method of amortization is used, interest expense in the earlier years will be

A)higher than it would have been had the effective-interest method of amortization been used.

B)less than it would have been had the effective-interest method of amortization been used.

C)the same as it would have been had the effective-interest method of amortization been used.

D)less than the stated rate of interest.

A)higher than it would have been had the effective-interest method of amortization been used.

B)less than it would have been had the effective-interest method of amortization been used.

C)the same as it would have been had the effective-interest method of amortization been used.

D)less than the stated rate of interest.

A

3

Restrictions included in restricted covenants do NOT generally include

A)working capital restrictions.

B)limits on executive compensation.

C)dividend restrictions.

D)limitations on incurring additional debt.

A)working capital restrictions.

B)limits on executive compensation.

C)dividend restrictions.

D)limitations on incurring additional debt.

B

4

A ten-year bond was issued in 2017 at a discount with a call provision to retire the bonds.When the bond issuer exercised the call provision on an interest date in 2016, the carrying value of the bond was less than the call price.The amount of bond liability removed from the accounts in 2019 would be the

A)call price.

B)maturity value.

C)carrying value.

D)face amount plus unamortized discount.

A)call price.

B)maturity value.

C)carrying value.

D)face amount plus unamortized discount.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

5

Bonds frequently used by schools and municipalities that mature in instalments are called

A)convertible bonds.

B)revenue bonds.

C)serial bonds.

D)callable bonds.

A)convertible bonds.

B)revenue bonds.

C)serial bonds.

D)callable bonds.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

6

If a long-term note is issued with zero interest or for non-monetary consideration,

A)the debtor must first try to value the non-monetary asset(s)involved in the transaction.

B)a reasonable interest rate must be imputed.

C)the debtor always tries to create a gain with such a transaction.

D)the note is a non-monetary liability.

A)the debtor must first try to value the non-monetary asset(s)involved in the transaction.

B)a reasonable interest rate must be imputed.

C)the debtor always tries to create a gain with such a transaction.

D)the note is a non-monetary liability.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

7

Using the effective-interest method of bond discount or premium amortization, the periodic interest expense is equal to the

A)stated rate multiplied by the face value of the bonds.

B)market rate multiplied by the beginning-of-period carrying value of the bonds.

C)stated rate multiplied by the beginning-of-period carrying value of the bonds.

D)market rate multiplied by the face value of the bonds.

A)stated rate multiplied by the face value of the bonds.

B)market rate multiplied by the beginning-of-period carrying value of the bonds.

C)stated rate multiplied by the beginning-of-period carrying value of the bonds.

D)market rate multiplied by the face value of the bonds.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

8

When a note payable is issued for property, goods, or services, the present value of the note should preferably be measured by

A)the present value of the property, goods or services.

B)the fair value of the property, goods, or services.

C)the fair value of the debt instrument.

D)the present value of the debt instrument.

A)the present value of the property, goods or services.

B)the fair value of the property, goods, or services.

C)the fair value of the debt instrument.

D)the present value of the debt instrument.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

9

How should a long-term bond initially be valued?

A)at the future value of the future cash flows

B)at the present value of the future cash flows

C)at the present value of the interest to be paid

D)at the maturity value of the bond

A)at the future value of the future cash flows

B)at the present value of the future cash flows

C)at the present value of the interest to be paid

D)at the maturity value of the bond

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

10

A contract representing the covenants and other terms of the agreement between the issuer of bonds and the lender is known as a

A)bond debenture.

B)long-term note payable.

C)registered bond.

D)bond indenture.

A)bond debenture.

B)long-term note payable.

C)registered bond.

D)bond indenture.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

11

When valuing financial instruments at fair value (the fair value option),

A)ASPE allows this option only for certain financial instruments.

B)IFRS allows this for all financial instruments.

C)IFRS requires that this option be used only where fair value does not result in more relevant information.

D)IFRS requires that non-performance risk be included in the fair value measurement.

A)ASPE allows this option only for certain financial instruments.

B)IFRS allows this for all financial instruments.

C)IFRS requires that this option be used only where fair value does not result in more relevant information.

D)IFRS requires that non-performance risk be included in the fair value measurement.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

12

When the interest payment dates of a bond are May 1 and November 1, and a bond issue is sold on June 1, the amount of cash received by the issuer will be

A)decreased by accrued interest from June 1 to November 1.

B)decreased by accrued interest from May 1 to June 1.

C)increased by accrued interest from June 1 to November 1.

D)increased by accrued interest from May 1 to June 1.

A)decreased by accrued interest from June 1 to November 1.

B)decreased by accrued interest from May 1 to June 1.

C)increased by accrued interest from June 1 to November 1.

D)increased by accrued interest from May 1 to June 1.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

13

When the effective-interest method is used to amortize bond premium or discount, the periodic amortization will

A)increase if the bonds were issued at a discount.

B)decrease if the bonds were issued at a premium.

C)increase if the bonds were issued at a premium.

D)increase if the bonds were issued at either a discount or a premium.

A)increase if the bonds were issued at a discount.

B)decrease if the bonds were issued at a premium.

C)increase if the bonds were issued at a premium.

D)increase if the bonds were issued at either a discount or a premium.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

14

The rate of interest actually earned by bondholders is called the

A)stated rate.

B)coupon rate.

C)dividend rate.

D)effective yield or market rate.

A)stated rate.

B)coupon rate.

C)dividend rate.

D)effective yield or market rate.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

15

Which of the following is NOT generally classified as a long-term liability?

A)stock dividends distributable

B)pension liabilities

C)mortgages payable

D)lease liabilities

A)stock dividends distributable

B)pension liabilities

C)mortgages payable

D)lease liabilities

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

16

Mars Corp.issued ten-year bonds with a maturity value of $400,000.If the bonds were issued at a premium, this indicates that

A)the market rate was higher than the stated rate.

B)the stated rate was higher than the market rate.

C)the market and stated rates were the same.

D)no relationship exists between the two rates.

A)the market rate was higher than the stated rate.

B)the stated rate was higher than the market rate.

C)the market and stated rates were the same.

D)no relationship exists between the two rates.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

17

A bond's face value is also called

A)the par value or the present value.

B)the principal amount or the present value.

C)the future value or the maturity value.

D)the par value or the maturity value.

A)the par value or the present value.

B)the principal amount or the present value.

C)the future value or the maturity value.

D)the par value or the maturity value.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

18

In a troubled debt restructuring in which the debt is continued with modified terms and the carrying amount of the debt is less than the total future cash flows,

A)an extraordinary gain should be recognized by the debtor.

B)a gain should be recognized by the debtor.

C)a new effective-interest rate must be calculated.

D)no interest expense or revenue should be recognized in the future.

A)an extraordinary gain should be recognized by the debtor.

B)a gain should be recognized by the debtor.

C)a new effective-interest rate must be calculated.

D)no interest expense or revenue should be recognized in the future.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

19

If a debt refunding is viewed as a modification or renegotiation, then

A)a new effective-interest rate is calculated.

B)a gain or loss is recorded.

C)there is no change in the accounting for the debt.

D)the old debt is derecognized.

A)a new effective-interest rate is calculated.

B)a gain or loss is recorded.

C)there is no change in the accounting for the debt.

D)the old debt is derecognized.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

20

The term used for bonds that are backed by collateral is

A)convertible bonds.

B)debenture bonds.

C)secured bonds.

D)callable bonds.

A)convertible bonds.

B)debenture bonds.

C)secured bonds.

D)callable bonds.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

21

Note disclosures for long-term debt generally include all of the following EXCEPT

A)assets pledged as security.

B)names of specific creditors.

C)restrictions imposed by creditors.

D)call provisions and conversion privileges.

A)assets pledged as security.

B)names of specific creditors.

C)restrictions imposed by creditors.

D)call provisions and conversion privileges.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

22

Which of the following statements is true?

A)Refinanced long-term debt may be reported as long-term rather than current if the refinancing has been completed before the date of the financial statements, according to ASPE; and before the date of the issue of the financial statements, according to IFRS.

B)Refinanced long-term debt may be reported as long-term rather than current if the refinancing has been completed before the date of the financial statements, according to IFRS; and before the date of the issue of the financial statements, according to ASPE.

C)Refinanced long-term debt may be reported as long-term rather than current if the refinancing has been completed before the date of the financial statements, according to IFRS and ASPE.

D)Refinanced long-term debt may be reported as long-term rather than current if the refinancing has been completed before the issue of the financial statements, according to IFRS and ASPE.

A)Refinanced long-term debt may be reported as long-term rather than current if the refinancing has been completed before the date of the financial statements, according to ASPE; and before the date of the issue of the financial statements, according to IFRS.

B)Refinanced long-term debt may be reported as long-term rather than current if the refinancing has been completed before the date of the financial statements, according to IFRS; and before the date of the issue of the financial statements, according to ASPE.

C)Refinanced long-term debt may be reported as long-term rather than current if the refinancing has been completed before the date of the financial statements, according to IFRS and ASPE.

D)Refinanced long-term debt may be reported as long-term rather than current if the refinancing has been completed before the issue of the financial statements, according to IFRS and ASPE.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

23

The times interest earned ratio is calculated by dividing

A)net income by interest expense.

B)income before taxes by interest expense.

C)income before income taxes and interest expense by interest expense.

D)net income and interest expense by interest expense.

A)net income by interest expense.

B)income before taxes by interest expense.

C)income before income taxes and interest expense by interest expense.

D)net income and interest expense by interest expense.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

24

The times interest earned ratio measures

A)the amount of interest expense related to long-term debt.

B)the percentage of total assets financed by creditors.

C)the profitability of an enterprise.

D)an enterprise's ability to meet interest payments as they come due.

A)the amount of interest expense related to long-term debt.

B)the percentage of total assets financed by creditors.

C)the profitability of an enterprise.

D)an enterprise's ability to meet interest payments as they come due.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

25

A troubled debt restructuring will generally result in a

A)loss by the debtor and a gain by the creditor.

B)loss by both the debtor and the creditor.

C)gain by both the debtor and the creditor.

D)gain by the debtor and a loss by the creditor.

A)loss by the debtor and a gain by the creditor.

B)loss by both the debtor and the creditor.

C)gain by both the debtor and the creditor.

D)gain by the debtor and a loss by the creditor.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

26

Which of the following statements is correct?

A)IFRS requires the effective-interest method to be used to amortize bond premiums and discounts; ASPE permits either the effective-interest method or the straight-line method.

B)ASPE requires the effective-interest method to be used to amortize bond premiums and discounts; IFRS permits either the effective-interest method or the straight-line method.

C)Both IFRS and ASPE require the effective-interest method to be used to amortize bond premiums and discounts.

D)Both IFRS and ASPE permit either the effective-interest method or the straight-line method to be used to amortize bond premiums and discounts.

A)IFRS requires the effective-interest method to be used to amortize bond premiums and discounts; ASPE permits either the effective-interest method or the straight-line method.

B)ASPE requires the effective-interest method to be used to amortize bond premiums and discounts; IFRS permits either the effective-interest method or the straight-line method.

C)Both IFRS and ASPE require the effective-interest method to be used to amortize bond premiums and discounts.

D)Both IFRS and ASPE permit either the effective-interest method or the straight-line method to be used to amortize bond premiums and discounts.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

27

Use the following information for questions.

On January 1, 2017, Satin Corp.issued eight-year, 6% bonds with a face value of $500,000, with interest payable semi-annually on June 30 and December 31.The bonds were sold to yield 8%.Table values are:

The present value of the principal is

A)$267,000.

B)$270,000.

C)$311,500.

D)$313,500.

On January 1, 2017, Satin Corp.issued eight-year, 6% bonds with a face value of $500,000, with interest payable semi-annually on June 30 and December 31.The bonds were sold to yield 8%.Table values are:

The present value of the principal is

A)$267,000.

B)$270,000.

C)$311,500.

D)$313,500.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

28

In a troubled debt restructuring in which the debt is settled by a transfer of assets with a fair market value less the carrying amount of the debt, the debtor would

A)not recognize a gain or loss on the settlement.

B)recognize a gain on the settlement.

C)recognize a loss on the settlement.

D)only record a memo in the general ledger.

A)not recognize a gain or loss on the settlement.

B)recognize a gain on the settlement.

C)recognize a loss on the settlement.

D)only record a memo in the general ledger.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

29

Which of the following is a required disclosure with respect to liabilities?

A)who the creditors are and how much is owed to each

B)payment terms for trade accounts payable

C)future payments and maturity amounts for each of the next ten years

D)details of assets pledged as collateral

A)who the creditors are and how much is owed to each

B)payment terms for trade accounts payable

C)future payments and maturity amounts for each of the next ten years

D)details of assets pledged as collateral

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

30

Which of the following arrangements would NOT represent a possible example of "off-balance-sheet financing"?

A)non-consolidated subsidiaries

B)variable interest entities

C)operating leases

D)capital or financing leases

A)non-consolidated subsidiaries

B)variable interest entities

C)operating leases

D)capital or financing leases

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

31

On January 1, 2017, Lace Ltd.sold five year, 12% bonds with a face value of $500,000.Interest will be paid semi-annually on June 30 and December 31.The bonds were sold for $538,500 to yield 10%.Using the effective-interest method of amortization of bond discount or premium, interest expense for 2017 is

A)$50,000.

B)$53,696.

C)$53,850.

D)$60,000.

A)$50,000.

B)$53,696.

C)$53,850.

D)$60,000.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

32

Which of the following is NOT a required disclosure with respect to liabilities?

A)maturity dates and interest rates for each outstanding bond issue

B)payment terms for trade accounts payable

C)future payments and maturity amounts for each of the next five years

D)details of assets pledged as collateral

A)maturity dates and interest rates for each outstanding bond issue

B)payment terms for trade accounts payable

C)future payments and maturity amounts for each of the next five years

D)details of assets pledged as collateral

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

33

Use the following information for questions.

On January 1, 2017, Satin Corp.issued eight-year, 6% bonds with a face value of $500,000, with interest payable semi-annually on June 30 and December 31.The bonds were sold to yield 8%.Table values are:

The issue price of the bonds is

A)$441,780.

B)$442,410.

C)$444,780.

D)$499,800.

On January 1, 2017, Satin Corp.issued eight-year, 6% bonds with a face value of $500,000, with interest payable semi-annually on June 30 and December 31.The bonds were sold to yield 8%.Table values are:

The issue price of the bonds is

A)$441,780.

B)$442,410.

C)$444,780.

D)$499,800.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

34

Complex financial instruments make the distinction between debt and equity

A)easier to define.

B)harder to define.

C)less important.

D)irrelevant.

A)easier to define.

B)harder to define.

C)less important.

D)irrelevant.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

35

How should long-term debt be reported if it matures within one year and the company has arranged, before its current year end, to convert the debt into shares?

A)as non-current and accompanied with a note explaining the method to be used in its liquidation

B)in a special section between liabilities and shareholders' equity

C)as non-current

D)as a current liability

A)as non-current and accompanied with a note explaining the method to be used in its liquidation

B)in a special section between liabilities and shareholders' equity

C)as non-current

D)as a current liability

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

36

The debt to total assets ratio is calculated by dividing

A)total liabilities by total assets.

B)long-term liabilities by total assets.

C)current liabilities by total assets.

D)total assets by total liabilities.

A)total liabilities by total assets.

B)long-term liabilities by total assets.

C)current liabilities by total assets.

D)total assets by total liabilities.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

37

Use the following information for questions.

On January 1, 2017, Satin Corp.issued eight-year, 6% bonds with a face value of $500,000, with interest payable semi-annually on June 30 and December 31.The bonds were sold to yield 8%.Table values are:

The present value of the interest is

A)$172,410.

B)$174,780.

C)$186,300.

D)$188,415.

On January 1, 2017, Satin Corp.issued eight-year, 6% bonds with a face value of $500,000, with interest payable semi-annually on June 30 and December 31.The bonds were sold to yield 8%.Table values are:

The present value of the interest is

A)$172,410.

B)$174,780.

C)$186,300.

D)$188,415.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

38

In a troubled debt restructuring in which the debt is continued with modified terms and the carrying amount of the debt is less than the total future cash flows, the creditor should

A)calculate a new effective-interest rate.

B)not recognize a loss.

C)calculate its loss using the historical effective rate of the loan.

D)calculate its loss using the current effective rate of the loan.

A)calculate a new effective-interest rate.

B)not recognize a loss.

C)calculate its loss using the historical effective rate of the loan.

D)calculate its loss using the current effective rate of the loan.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

39

When the debtor sets aside money in a trust such that the investment and any return will be sufficient to pay the principal and the interest to the creditor, but the creditor does NOT release the company from the primary obligation to settle the debt, this type of arrangement is known as

A)in substance defeasance.

B)in substance refunding.

C)substantive repayment.

D)legal defeasance.

A)in substance defeasance.

B)in substance refunding.

C)substantive repayment.

D)legal defeasance.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

40

The debt to total assets earned ratio measures

A)the amount of debt related to interest expense.

B)the percentage of total assets financed by creditors.

C)the likelihood an enterprise will default on its obligations.

D)the profitability of an enterprise.

A)the amount of debt related to interest expense.

B)the percentage of total assets financed by creditors.

C)the likelihood an enterprise will default on its obligations.

D)the profitability of an enterprise.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

41

The December 31, 2017, statement of financial position of Cotton Corporation includes the following:

9% bonds payable due December 31, 2023 $718,900

The bonds have a face value of $700,000, and were issued on December 31, 2016, at 103, with interest payable on July 1 and December 31 of each year.Cotton uses straight-line amortization to amortize bond premium or discount.On March 1, 2018, Cotton retired $280,000 of these bonds at 98 plus accrued interest.Ignoring income taxes, what should Cotton record as a gain on retirement of these bonds?

A)$ 7,560

B)$13,020

C)$13,160

D)$14,000

9% bonds payable due December 31, 2023 $718,900

The bonds have a face value of $700,000, and were issued on December 31, 2016, at 103, with interest payable on July 1 and December 31 of each year.Cotton uses straight-line amortization to amortize bond premium or discount.On March 1, 2018, Cotton retired $280,000 of these bonds at 98 plus accrued interest.Ignoring income taxes, what should Cotton record as a gain on retirement of these bonds?

A)$ 7,560

B)$13,020

C)$13,160

D)$14,000

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

42

On July 1, 2017, Salmon Corp.issued $600,000, 8% bonds at 99 plus accrued interest.The bonds are dated April 1, 2017 and mature on April 1, 2027.Interest is payable semi-annually on April 1 and October 1.How much did Salmon receive from the bond issuance?

A)$594,000

B)$600,000

C)$606,000

D)$602,000

A)$594,000

B)$600,000

C)$606,000

D)$602,000

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

43

On July 1, 2017, Pike Inc.issued $500,000, 9% bonds, which mature on July 1, 2027.The bonds were issued for $469,500 to yield 10%.Pike uses the effective-interest method of amortizing bond discount.Interest is payable annually on June 30.At June 30, 2019, the adjusted balance in the Bonds Payable account should be

A)$500,000.

B)$493,900.

C)$473,595.

D)$471,450.

A)$500,000.

B)$493,900.

C)$473,595.

D)$471,450.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

44

Suede Corp.called an outstanding bond obligation four years before maturity.At that time there was an unamortized discount of $150,000.To extinguish this debt, Suede had to pay a call premium of $75,000.Ignoring income tax considerations, how should these amounts be treated for accounting purposes?

A)Amortize $225,000 over four years.

B)Record a $225,000 loss in the year of extinguishment.

C)Record a $75,000 loss in the year of extinguishment and amortize $150,000 over four years.

D)Either amortize $225,000 over four years or record a $225,000 loss immediately, whichever management selects.

A)Amortize $225,000 over four years.

B)Record a $225,000 loss in the year of extinguishment.

C)Record a $75,000 loss in the year of extinguishment and amortize $150,000 over four years.

D)Either amortize $225,000 over four years or record a $225,000 loss immediately, whichever management selects.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

45

Use the following information for questions.

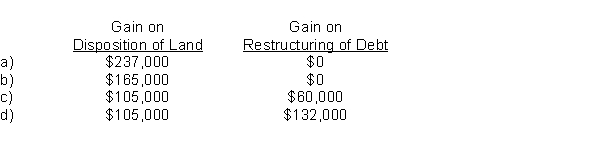

On December 31, 2017, Diaz Corp.is in financial difficulty and cannot pay a $900,000 note with $90,000 accrued interest payable to Cameron Ltd., which is now due.Cameron agrees to accept from Diaz equipment that has a fair value of $435,000, an original cost of $720,000, and accumulated depreciation of $345,000.Cameron also forgives the accrued interest, extends the maturity date to December 31, 2020, reduces the face amount of the note to $375,000, and reduces the interest rate to 6%, with interest payable at the end of each year.

Diaz should record interest expense for 2020 of

A)$0.

B)$22,500.

C)$45,000.

D)$67,500.

On December 31, 2017, Diaz Corp.is in financial difficulty and cannot pay a $900,000 note with $90,000 accrued interest payable to Cameron Ltd., which is now due.Cameron agrees to accept from Diaz equipment that has a fair value of $435,000, an original cost of $720,000, and accumulated depreciation of $345,000.Cameron also forgives the accrued interest, extends the maturity date to December 31, 2020, reduces the face amount of the note to $375,000, and reduces the interest rate to 6%, with interest payable at the end of each year.

Diaz should record interest expense for 2020 of

A)$0.

B)$22,500.

C)$45,000.

D)$67,500.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

46

On January 1, 2017, Trout Corp.sold $500,000, 10% bonds for $442,648 to yield 12%.Interest is payable semi-annually on January 1 and July 1.Trout uses the effective-interest method of amortizing bond discount.What amount should Trout report as interest expense for the six months ended June 30, 2017?

A)$30,000

B)$26,559

C)$25,000

D)$22,133

A)$30,000

B)$26,559

C)$25,000

D)$22,133

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

47

On January 1, 2017, Varden Ltd.issued $4,000,000, 10% bonds, which mature on January 1, 2027.The bonds were issued for $4,540,000 to yield 8%.Varden uses the effective-interest method of amortizing bond premium.Interest is payable annually on December 31.At December 31, 2017, the adjusted balance in the Bonds Payable account should be

A)$4,540,000.

B)$4,503,200.

C)$4,486,000.

D)$4,000,000.

A)$4,540,000.

B)$4,503,200.

C)$4,486,000.

D)$4,000,000.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

48

On January 2, 2017, Muslin Ltd.sold five year, 8% bonds with a face value of $900,000.Interest will be paid semi-annually on June 30 and December 31.The bonds were sold for $830,400 to yield 10%.Using the effective-interest method of amortization of bond discount or premium, interest expense for 2017 is

A)$72,000.

B)$83,040.

C)$83,316.

D)$90,000.

A)$72,000.

B)$83,040.

C)$83,316.

D)$90,000.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

49

On January 1, 2017, Bass Inc.redeemed its 15-year, $900,000 par value bonds at 102.They were originally issued on January 1, 2005 at 98 with a maturity date of January 1, 2020.Bass amortizes bond discounts and premiums using the straight-line method.Ignoring income taxes, what amount of loss should Bass recognize on the redemption of these bonds?

A)$32,400

B)$21,600

C)$18,000

D)$14,400

A)$32,400

B)$21,600

C)$18,000

D)$14,400

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

50

On January 1, 2017, Alvin Corp.sold property to Marvin Ltd., for which Alvin had originally paid $570,000.There was no established exchange price for this property.Marvin gave Alvin a $900,000, zero-interest-bearing note, payable in three equal annual instalments of $300,000, with the first payment due December 31, 2017.The note also has no ready market.The market rate of interest for a note of this type is 10%.The present value of a $900,000 note payable in three equal annual instalments of $300,000 at 10% is $746,056.To the nearest dollar, and using the effective-interest method, how much interest revenue should Alvin recognize in 2017?

A)$ 0

B)$30,000

C)$74,606

D)$90,000

A)$ 0

B)$30,000

C)$74,606

D)$90,000

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

51

On July 1, 2017, Tilapia Corp.had outstanding 8%, $1,000,000, 10-year bonds maturing on June 30, 2027.Interest is payable semi-annually on June 30 and December 31.Assume all appropriate entries had been prepared and posted at June 30, 2018.The carrying value of the bond at June 30, 2018 was $965,000.At this time, Tilapia purchased all the bonds at 94 and retired them.What is the gain or loss on this early extinguishment of debt?

A)$60,000 gain

B)$35,000 loss

C)$25,000 gain

D)$25,000 loss

A)$60,000 gain

B)$35,000 loss

C)$25,000 gain

D)$25,000 loss

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

52

Use the following information for questions.

On December 31, 2017, Diaz Corp.is in financial difficulty and cannot pay a $900,000 note with $90,000 accrued interest payable to Cameron Ltd., which is now due.Cameron agrees to accept from Diaz equipment that has a fair value of $435,000, an original cost of $720,000, and accumulated depreciation of $345,000.Cameron also forgives the accrued interest, extends the maturity date to December 31, 2020, reduces the face amount of the note to $375,000, and reduces the interest rate to 6%, with interest payable at the end of each year.

Diaz should recognize a gain on the partial settlement and restructure of the debt of

A)$0.

B)$22,500.

C)$112,500.

D)$180,000.

On December 31, 2017, Diaz Corp.is in financial difficulty and cannot pay a $900,000 note with $90,000 accrued interest payable to Cameron Ltd., which is now due.Cameron agrees to accept from Diaz equipment that has a fair value of $435,000, an original cost of $720,000, and accumulated depreciation of $345,000.Cameron also forgives the accrued interest, extends the maturity date to December 31, 2020, reduces the face amount of the note to $375,000, and reduces the interest rate to 6%, with interest payable at the end of each year.

Diaz should recognize a gain on the partial settlement and restructure of the debt of

A)$0.

B)$22,500.

C)$112,500.

D)$180,000.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

53

At December 31, 2017, the 10% bonds payable of Paisley Inc.had a carrying value of $760,000.The bonds, which had a face value of $800,000, were issued at a discount to yield 12%.The amortization of the bond discount had been recorded using the effective-interest method.Interest was being paid on January 1 and July 1 of each year.The July 1, 2018 interest payment and discount amortization had been correctly recorded.On July 2, 2018, Paisley retired the bonds at 102.Ignoring income taxes, what is the loss that should be recorded on the early retirement of the bonds?

A)$16,000

B)$44,800

C)$50,400

D)$56,000

A)$16,000

B)$44,800

C)$50,400

D)$56,000

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

54

At December 31, 2017, the 12% bonds payable of Leather Corp.had a carrying value of $312,000.The bonds, which had a face value of $300,000, were issued at a premium to yield 10%.Leather uses the effective-interest method of amortization of bond premium.Interest is paid on June 30 and December 31.On June 30, 2018, Leather retired the bonds at 104 plus accrued interest.The loss on retirement, ignoring taxes, is

A)$ 0.

B)$ 2,400.

C)$ 3,720.

D)$12,000.

A)$ 0.

B)$ 2,400.

C)$ 3,720.

D)$12,000.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

55

On its December 31, 2017 statement of financial position, Codfish Ltd.reported bonds payable of $1,000,000.The bonds had been issued at par.On January 2, 2018, Codfish retired one half of the outstanding bonds at 103 plus a call premium of $35,000.Ignoring income taxes, what amount should Codfish report on its 2018 income statement as loss on extinguishment of debt?

A)$50,000

B)$35,000

C)$15,000

D)$0

A)$50,000

B)$35,000

C)$15,000

D)$0

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

56

On January 1, 2017, Halibut Corp.issued $1,000,000, 10% bonds for $1,040,000.These bonds were to mature on January 1, 2027 but were callable at 101 any time after December 31, 2017.Interest was payable semi-annually on July 1 and January 1.On July 1, 2022, Halibut called all of the bonds and retired them.Bond premium was amortized on a straight-line basis.Ignoring income taxes, Halibut's gain or loss in 2022 on this early extinguishment of debt was

A)$8,000 loss.

B)$8,000 gain.

C)$10,000 loss.

D)$12,000 gain.

A)$8,000 loss.

B)$8,000 gain.

C)$10,000 loss.

D)$12,000 gain.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

57

On January 1, 2017, Susan Hong lent $60,104 to Ben Bachu.A zero-interest-bearing note (face amount, $80,000)was exchanged solely for cash; no other rights or privileges were exchanged.The note is to be repaid on December 31, 2019.The market rate of interest for a loan of this type is 10%.To the nearest dollar, and using the effective-interest method, how much interest revenue should Ms.Hong recognize in 2017?

A)$ 6,010

B)$ 8,000

C)$18,030

D)$24,000

A)$ 6,010

B)$ 8,000

C)$18,030

D)$24,000

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

58

Use the following information for questions.

On December 31, 2017, Diaz Corp.is in financial difficulty and cannot pay a $900,000 note with $90,000 accrued interest payable to Cameron Ltd., which is now due.Cameron agrees to accept from Diaz equipment that has a fair value of $435,000, an original cost of $720,000, and accumulated depreciation of $345,000.Cameron also forgives the accrued interest, extends the maturity date to December 31, 2020, reduces the face amount of the note to $375,000, and reduces the interest rate to 6%, with interest payable at the end of each year.

Diaz should recognize a gain or loss on the transfer of the equipment of

A)$0.

B)$60,000 gain.

C)$90,000 gain.

D)$285,000 loss.

On December 31, 2017, Diaz Corp.is in financial difficulty and cannot pay a $900,000 note with $90,000 accrued interest payable to Cameron Ltd., which is now due.Cameron agrees to accept from Diaz equipment that has a fair value of $435,000, an original cost of $720,000, and accumulated depreciation of $345,000.Cameron also forgives the accrued interest, extends the maturity date to December 31, 2020, reduces the face amount of the note to $375,000, and reduces the interest rate to 6%, with interest payable at the end of each year.

Diaz should recognize a gain or loss on the transfer of the equipment of

A)$0.

B)$60,000 gain.

C)$90,000 gain.

D)$285,000 loss.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

59

On January 1, 2017, Linen Corp.issued $450,000 (face value), 10%, ten-year bonds at 103.The bonds are callable at 105.Linen has recorded amortization of the bond premium by the straight-line method.On December 31, 2023, Linen repurchased $100,000 of the bonds in the open market at 96.Bond interest expense and premium amortization have been recorded for 2023.Ignoring income taxes, what is the loss or gain arising from this reacquisition?

A)a gain of $4,900

B)a loss of $4,900

C)a gain of $6,100

D)a loss of $6,100

A)a gain of $4,900

B)a loss of $4,900

C)a gain of $6,100

D)a loss of $6,100

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

60

On January 1, 2017, Queen Ltd.sold property to King Company.There was no established exchange price for the property, and King gave Queen a $3,000,000, zero-interest-bearing note payable in five equal annual instalments of $600,000, with the first payment due December 31, 2017.The market rate of interest for a note of this type is 9%.The present value of the note at 9% was $2,333,791 at January 1, 2017.What should be the balance of the Note Payable to Queen Ltd.account on King's December 31, 2017 adjusted trial balance, assuming that the note is recorded at net and the effective-interest method is used? (Round to the nearest dollar, if necessary.)

A)$1,943,832

B)$2,333,791

C)$2,400,000

D)$3,000,000

A)$1,943,832

B)$2,333,791

C)$2,400,000

D)$3,000,000

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

61

Continental Company's 2017 financial statements contain the following selected data: Continental's times interest earned for 2017 is

A)8 times.

B)11 times.

C)12 times.

D)13 times.

Continental's times interest earned for 2017 isA)8 times.

B)11 times.

C)12 times.

D)13 times.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

62

Pineapple owes Dole a $600,000, 12%, three-year note dated December 31, 2015.Pineapple has been experiencing financial difficulties, and still owes accrued interest of $72,000 on this note at December 31, 2017.Under a troubled debt restructuring, on December 31, 2017, Dole agrees to settle the note plus the accrued interest for land that Pineapple owns, which has a fair value of $540,000.Pineapple's original cost of the land is $435,000.Ignoring income taxes, on its 2017 income statement, what should Pineapple report as a result of the troubled debt restructuring?

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 62 flashcards in this deck.