Deck 9: Accounting Changes and Error Analysis

Full screen (f)

Question

Question

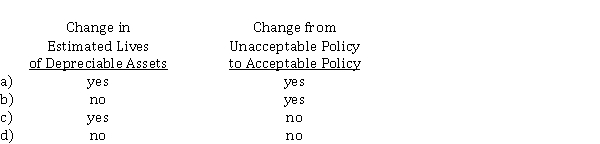

Which of the following should be given retrospective treatment?

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Use the following information for questions *38-*40.

Cheyenne Ltd.'s December 31 year-end financial statements contained the following errors: An insurance premium of $ 3,600 was prepaid in 2019 covering the calendar years 2019, 2020, and 2021. This had been debited to insurance expense. In addition, on December 31, 2020, fully depreciated machinery was sold for $ 1,900 cash, but the sale was not recorded until 2021. There were no other errors during 2020 or 2021 and no corrections have been made for any of the errors. Ignore income tax considerations.

An insurance premium of $ 3,600 was prepaid in 2019 covering the calendar years 2019, 2020, and 2021. This had been debited to insurance expense. In addition, on December 31, 2020, fully depreciated machinery was sold for $ 1,900 cash, but the sale was not recorded until 2021. There were no other errors during 2020 or 2021 and no corrections have been made for any of the errors. Ignore income tax considerations.

A company using a perpetual inventory system neglected to record a purchase of merchandise on account at year end. This merchandise was also omitted from the year-end physical count. How will these errors affect assets, liabilities, and shareholders' equity at year end and net income for the year? Assets Liabilities Shareholders' Equity Net Income

A) no effect understate overstate overstate

B) no effect overstate understate understate

C) understate understate no effect no effect

D) understate no effect understate understate

Cheyenne Ltd.'s December 31 year-end financial statements contained the following errors:

An insurance premium of $ 3,600 was prepaid in 2019 covering the calendar years 2019, 2020, and 2021. This had been debited to insurance expense. In addition, on December 31, 2020, fully depreciated machinery was sold for $ 1,900 cash, but the sale was not recorded until 2021. There were no other errors during 2020 or 2021 and no corrections have been made for any of the errors. Ignore income tax considerations.A company using a perpetual inventory system neglected to record a purchase of merchandise on account at year end. This merchandise was also omitted from the year-end physical count. How will these errors affect assets, liabilities, and shareholders' equity at year end and net income for the year? Assets Liabilities Shareholders' Equity Net Income

A) no effect understate overstate overstate

B) no effect overstate understate understate

C) understate understate no effect no effect

D) understate no effect understate understate

Question

Use the following information for questions *38-*40.

Cheyenne Ltd.'s December 31 year-end financial statements contained the following errors: An insurance premium of $ 3,600 was prepaid in 2019 covering the calendar years 2019, 2020, and 2021. This had been debited to insurance expense. In addition, on December 31, 2020, fully depreciated machinery was sold for $ 1,900 cash, but the sale was not recorded until 2021. There were no other errors during 2020 or 2021 and no corrections have been made for any of the errors. Ignore income tax considerations.

MissTake Corp. is a small private corporation that does not prepare comparative statements. At the end of their 2020 fiscal year, it was discovered that the 2019 depreciation expense on their computer equipment had been incorrectly debited to maintenance expense. How should MissTake deal with this situation?

A) Prepare an adjusting entry to debit depreciation expense and credit maintenance expense.

B) Prepare an adjusting entry to debit retained earnings and credit maintenance expense.

C) Restate their 2019 financial statements.

D) Ignore it.

Cheyenne Ltd.'s December 31 year-end financial statements contained the following errors:

An insurance premium of $ 3,600 was prepaid in 2019 covering the calendar years 2019, 2020, and 2021. This had been debited to insurance expense. In addition, on December 31, 2020, fully depreciated machinery was sold for $ 1,900 cash, but the sale was not recorded until 2021. There were no other errors during 2020 or 2021 and no corrections have been made for any of the errors. Ignore income tax considerations.MissTake Corp. is a small private corporation that does not prepare comparative statements. At the end of their 2020 fiscal year, it was discovered that the 2019 depreciation expense on their computer equipment had been incorrectly debited to maintenance expense. How should MissTake deal with this situation?

A) Prepare an adjusting entry to debit depreciation expense and credit maintenance expense.

B) Prepare an adjusting entry to debit retained earnings and credit maintenance expense.

C) Restate their 2019 financial statements.

D) Ignore it.

Question

Question

Randall Corp. began operations on January 1, 2019, and uses FIFO to cost its inventory. Management is contemplating a change to the average cost method and is interested in determining what effect such a change will have on pre-tax income. Accordingly, the following information has been developed:  Based upon the above information, a change to the average cost method in 2020 would result in pre-tax income for 2020 of

Based upon the above information, a change to the average cost method in 2020 would result in pre-tax income for 2020 of

A) $ 790,000.

B) $ 860,000.

C) $ 940,000.

D) $ 980,000.

Based upon the above information, a change to the average cost method in 2020 would result in pre-tax income for 2020 ofA) $ 790,000.

B) $ 860,000.

C) $ 940,000.

D) $ 980,000.

Question

Use the following information for questions *38-*40.

Cheyenne Ltd.'s December 31 year-end financial statements contained the following errors: An insurance premium of $ 3,600 was prepaid in 2019 covering the calendar years 2019, 2020, and 2021. This had been debited to insurance expense. In addition, on December 31, 2020, fully depreciated machinery was sold for $ 1,900 cash, but the sale was not recorded until 2021. There were no other errors during 2020 or 2021 and no corrections have been made for any of the errors. Ignore income tax considerations.

Counterbalancing errors do NOT include

A) errors that correct themselves in two years.

B) errors that correct themselves in three or more years.

C) an understatement of ending inventory.

D) an overstatement of unearned revenue.

Cheyenne Ltd.'s December 31 year-end financial statements contained the following errors:

An insurance premium of $ 3,600 was prepaid in 2019 covering the calendar years 2019, 2020, and 2021. This had been debited to insurance expense. In addition, on December 31, 2020, fully depreciated machinery was sold for $ 1,900 cash, but the sale was not recorded until 2021. There were no other errors during 2020 or 2021 and no corrections have been made for any of the errors. Ignore income tax considerations.Counterbalancing errors do NOT include

A) errors that correct themselves in two years.

B) errors that correct themselves in three or more years.

C) an understatement of ending inventory.

D) an overstatement of unearned revenue.

Question

Use the following information for questions *38-*40.

Cheyenne Ltd.'s December 31 year-end financial statements contained the following errors: An insurance premium of $ 3,600 was prepaid in 2019 covering the calendar years 2019, 2020, and 2021. This had been debited to insurance expense. In addition, on December 31, 2020, fully depreciated machinery was sold for $ 1,900 cash, but the sale was not recorded until 2021. There were no other errors during 2020 or 2021 and no corrections have been made for any of the errors. Ignore income tax considerations.

On December 31, 2020, the bookkeeper at Thrush Corp. did not record special insurance costs that had been incurred (but not yet paid), related to a building that Thrush Corp. is constructing. What is the effect of the omission on accrued liabilities and retained earnings in the December 31, 2020 statement of financial position?

Cheyenne Ltd.'s December 31 year-end financial statements contained the following errors:

An insurance premium of $ 3,600 was prepaid in 2019 covering the calendar years 2019, 2020, and 2021. This had been debited to insurance expense. In addition, on December 31, 2020, fully depreciated machinery was sold for $ 1,900 cash, but the sale was not recorded until 2021. There were no other errors during 2020 or 2021 and no corrections have been made for any of the errors. Ignore income tax considerations.On December 31, 2020, the bookkeeper at Thrush Corp. did not record special insurance costs that had been incurred (but not yet paid), related to a building that Thrush Corp. is constructing. What is the effect of the omission on accrued liabilities and retained earnings in the December 31, 2020 statement of financial position?

Question

Question

Question

Question

Question

Use the following information for questions *38-*40.

Cheyenne Ltd.'s December 31 year-end financial statements contained the following errors: An insurance premium of $ 3,600 was prepaid in 2019 covering the calendar years 2019, 2020, and 2021. This had been debited to insurance expense. In addition, on December 31, 2020, fully depreciated machinery was sold for $ 1,900 cash, but the sale was not recorded until 2021. There were no other errors during 2020 or 2021 and no corrections have been made for any of the errors. Ignore income tax considerations.

What is the total net effect of the errors on Cheyenne's 2020 net income?

A) Net income understated by $ 2,900

B) Net income overstated by $ 1,500

C) Net income overstated by $ 2,600

D) Net income overstated by $ 3,000

Cheyenne Ltd.'s December 31 year-end financial statements contained the following errors:

An insurance premium of $ 3,600 was prepaid in 2019 covering the calendar years 2019, 2020, and 2021. This had been debited to insurance expense. In addition, on December 31, 2020, fully depreciated machinery was sold for $ 1,900 cash, but the sale was not recorded until 2021. There were no other errors during 2020 or 2021 and no corrections have been made for any of the errors. Ignore income tax considerations.What is the total net effect of the errors on Cheyenne's 2020 net income?

A) Net income understated by $ 2,900

B) Net income overstated by $ 1,500

C) Net income overstated by $ 2,600

D) Net income overstated by $ 3,000

Question

Question

Use the following information for questions *38-*40.

Cheyenne Ltd.'s December 31 year-end financial statements contained the following errors: An insurance premium of $ 3,600 was prepaid in 2019 covering the calendar years 2019, 2020, and 2021. This had been debited to insurance expense. In addition, on December 31, 2020, fully depreciated machinery was sold for $ 1,900 cash, but the sale was not recorded until 2021. There were no other errors during 2020 or 2021 and no corrections have been made for any of the errors. Ignore income tax considerations.

What is the total effect of the errors on the balance of Cheyenne's retained earnings at December 31, 2020?

A) Retained earnings understated by $ 2,000

B) Retained earnings understated by $ 900

C) Retained earnings understated by $ 500

D) Retained earnings overstated by $ 700

Cheyenne Ltd.'s December 31 year-end financial statements contained the following errors:

An insurance premium of $ 3,600 was prepaid in 2019 covering the calendar years 2019, 2020, and 2021. This had been debited to insurance expense. In addition, on December 31, 2020, fully depreciated machinery was sold for $ 1,900 cash, but the sale was not recorded until 2021. There were no other errors during 2020 or 2021 and no corrections have been made for any of the errors. Ignore income tax considerations.What is the total effect of the errors on the balance of Cheyenne's retained earnings at December 31, 2020?

A) Retained earnings understated by $ 2,000

B) Retained earnings understated by $ 900

C) Retained earnings understated by $ 500

D) Retained earnings overstated by $ 700

Question

Question

Question

Question

Question

Use the following information for questions *38-*40.

Cheyenne Ltd.'s December 31 year-end financial statements contained the following errors: An insurance premium of $ 3,600 was prepaid in 2019 covering the calendar years 2019, 2020, and 2021. This had been debited to insurance expense. In addition, on December 31, 2020, fully depreciated machinery was sold for $ 1,900 cash, but the sale was not recorded until 2021. There were no other errors during 2020 or 2021 and no corrections have been made for any of the errors. Ignore income tax considerations.

What is the total net effect of the errors on the amount of Cheyenne's working capital at December 31, 2020?

A) Working capital overstated by $ 1,000

B) Working capital overstated by $ 300

C) Working capital understated by $ 900

D) Working capital understated by $ 2,400

Cheyenne Ltd.'s December 31 year-end financial statements contained the following errors:

An insurance premium of $ 3,600 was prepaid in 2019 covering the calendar years 2019, 2020, and 2021. This had been debited to insurance expense. In addition, on December 31, 2020, fully depreciated machinery was sold for $ 1,900 cash, but the sale was not recorded until 2021. There were no other errors during 2020 or 2021 and no corrections have been made for any of the errors. Ignore income tax considerations.What is the total net effect of the errors on the amount of Cheyenne's working capital at December 31, 2020?

A) Working capital overstated by $ 1,000

B) Working capital overstated by $ 300

C) Working capital understated by $ 900

D) Working capital understated by $ 2,400

Question

Question

Question

Question

Question

Use the following information for questions *38-*40.

Cheyenne Ltd.'s December 31 year-end financial statements contained the following errors: An insurance premium of $ 3,600 was prepaid in 2019 covering the calendar years 2019, 2020, and 2021. This had been debited to insurance expense. In addition, on December 31, 2020, fully depreciated machinery was sold for $ 1,900 cash, but the sale was not recorded until 2021. There were no other errors during 2020 or 2021 and no corrections have been made for any of the errors. Ignore income tax considerations.

At December 31, 2020, Grant Corp.'s auditor discovered the following errors:

1) Accrued salaries payable of $ 11,000 were NOT recorded at December 31, 2019.

2) Office supplies on hand of $ 5,000 at December 31, 2020 had been treated as expense instead of supplies inventory.

Neither of these errors was discovered nor corrected. The effect of these two errors would cause

A) 2020 net income to be understated $ 16,000 and December 31, 2020 retained earnings to be understated $ 5,000.

B) 2019 net income and December 31, 2019 retained earnings to be understated $ 11,000 each.

C) 2019 net income to be overstated $ 6,000 and 2020 net income to be understated $ 5,000.

D) 2020 net income and December 31, 2020 retained earnings to be understated $ 5,000 each.

Cheyenne Ltd.'s December 31 year-end financial statements contained the following errors:

An insurance premium of $ 3,600 was prepaid in 2019 covering the calendar years 2019, 2020, and 2021. This had been debited to insurance expense. In addition, on December 31, 2020, fully depreciated machinery was sold for $ 1,900 cash, but the sale was not recorded until 2021. There were no other errors during 2020 or 2021 and no corrections have been made for any of the errors. Ignore income tax considerations.At December 31, 2020, Grant Corp.'s auditor discovered the following errors:

1) Accrued salaries payable of $ 11,000 were NOT recorded at December 31, 2019.

2) Office supplies on hand of $ 5,000 at December 31, 2020 had been treated as expense instead of supplies inventory.

Neither of these errors was discovered nor corrected. The effect of these two errors would cause

A) 2020 net income to be understated $ 16,000 and December 31, 2020 retained earnings to be understated $ 5,000.

B) 2019 net income and December 31, 2019 retained earnings to be understated $ 11,000 each.

C) 2019 net income to be overstated $ 6,000 and 2020 net income to be understated $ 5,000.

D) 2020 net income and December 31, 2020 retained earnings to be understated $ 5,000 each.

Question

Question

Eagle Corp. is a calendar-year corporation whose financial statements for 2019 and 2020 included errors as follows:  Assume that purchases were recorded correctly and that no correcting entries were made at December 31, 2019 or December 31, 2020. Ignoring income taxes, by how much should Eagle's retained earnings be retrospectively adjusted at January 1, 2021?

Assume that purchases were recorded correctly and that no correcting entries were made at December 31, 2019 or December 31, 2020. Ignoring income taxes, by how much should Eagle's retained earnings be retrospectively adjusted at January 1, 2021?

A) $ 32,000 increase

B) $ 8,000 increase

C) $ 4,000 decrease

D) $ 2,000 increase

Assume that purchases were recorded correctly and that no correcting entries were made at December 31, 2019 or December 31, 2020. Ignoring income taxes, by how much should Eagle's retained earnings be retrospectively adjusted at January 1, 2021?A) $ 32,000 increase

B) $ 8,000 increase

C) $ 4,000 decrease

D) $ 2,000 increase

Question

Question

Question

Effects of errors on net income

Hummingbird Corp. began operations on January 1, 2019. Financial statements for 2019 and 2020 contained the following errors: In addition, on December 26, 2020, fully depreciated equipment was sold for $ 19,000, but the sale was not recorded until 2021. No corrections have been made for any of the errors.

In addition, on December 26, 2020, fully depreciated equipment was sold for $ 19,000, but the sale was not recorded until 2021. No corrections have been made for any of the errors.

Instructions

Ignoring income tax, show your calculation of the total effect of the errors on 2020 net income.

Hummingbird Corp. began operations on January 1, 2019. Financial statements for 2019 and 2020 contained the following errors:

In addition, on December 26, 2020, fully depreciated equipment was sold for $ 19,000, but the sale was not recorded until 2021. No corrections have been made for any of the errors.Instructions

Ignoring income tax, show your calculation of the total effect of the errors on 2020 net income.

Question

Question

Use the following information for questions *42-*44.

Fairfax Inc. began operations on January 1, 2019. Financial statements for 2019 and 2020 contained the following errors: In addition, on December 31, 2020 fully depreciated equipment was sold for $ 7,200, but the sale was NOT recorded until 2021. No corrections have been made for any of the errors. Ignore income tax considerations.

In addition, on December 31, 2020 fully depreciated equipment was sold for $ 7,200, but the sale was NOT recorded until 2021. No corrections have been made for any of the errors. Ignore income tax considerations.

The total effect of the errors on Fairfax's retained earnings at December 31, 2020 is that the balance is understated by

A) $ 82,200.

B) $ 67,200.

C) $ 46,200.

D) $ 34,200.

Fairfax Inc. began operations on January 1, 2019. Financial statements for 2019 and 2020 contained the following errors:

In addition, on December 31, 2020 fully depreciated equipment was sold for $ 7,200, but the sale was NOT recorded until 2021. No corrections have been made for any of the errors. Ignore income tax considerations.The total effect of the errors on Fairfax's retained earnings at December 31, 2020 is that the balance is understated by

A) $ 82,200.

B) $ 67,200.

C) $ 46,200.

D) $ 34,200.

Question

Question

Question

Question

Question

Effects of errors on financial statements

Show how the following independent errors will affect net income on the income statement and the shareholders' equity section of the statement of financial position (SFP) using the symbol + (plus) for overstated, - (minus) for understated, and 0 (zero) for no effect.

1. Ending 2019 inventory overstated

2. Failure to accrue 2019 interest revenue

3. A capital expenditure for factory equipment (useful life, 5 years) was charged to expense in error in 2019

4. Failure to accrue 2019 wages

5. Ending inventory in 2019 understated

6. Overstated 2019 depreciation expense; 2020 expense correct

Show how the following independent errors will affect net income on the income statement and the shareholders' equity section of the statement of financial position (SFP) using the symbol + (plus) for overstated, - (minus) for understated, and 0 (zero) for no effect.

1. Ending 2019 inventory overstated

2. Failure to accrue 2019 interest revenue

3. A capital expenditure for factory equipment (useful life, 5 years) was charged to expense in error in 2019

4. Failure to accrue 2019 wages

5. Ending inventory in 2019 understated

6. Overstated 2019 depreciation expense; 2020 expense correct

Question

Use the following information for questions *42-*44.

Fairfax Inc. began operations on January 1, 2019. Financial statements for 2019 and 2020 contained the following errors: In addition, on December 31, 2020 fully depreciated equipment was sold for $ 7,200, but the sale was NOT recorded until 2021. No corrections have been made for any of the errors. Ignore income tax considerations.

The total effect of the errors on Fairfax's working capital at December 31, 2020 is that working capital is understated by

A) $ 100,200.

B) $ 79,200.

C) $ 46,200.

D) $ 31,200.

Fairfax Inc. began operations on January 1, 2019. Financial statements for 2019 and 2020 contained the following errors:

In addition, on December 31, 2020 fully depreciated equipment was sold for $ 7,200, but the sale was NOT recorded until 2021. No corrections have been made for any of the errors. Ignore income tax considerations.The total effect of the errors on Fairfax's working capital at December 31, 2020 is that working capital is understated by

A) $ 100,200.

B) $ 79,200.

C) $ 46,200.

D) $ 31,200.

Question

Use the following information for questions *42-*44.

Fairfax Inc. began operations on January 1, 2019. Financial statements for 2019 and 2020 contained the following errors: In addition, on December 31, 2020 fully depreciated equipment was sold for $ 7,200, but the sale was NOT recorded until 2021. No corrections have been made for any of the errors. Ignore income tax considerations.

The total effect of the errors on Fairfax's 2020 net income is

A) understated by $ 94,200.

B) understated by $ 61,200.

C) overstated by $ 28,800.

D) overstated by $ 49,800.

Fairfax Inc. began operations on January 1, 2019. Financial statements for 2019 and 2020 contained the following errors:

In addition, on December 31, 2020 fully depreciated equipment was sold for $ 7,200, but the sale was NOT recorded until 2021. No corrections have been made for any of the errors. Ignore income tax considerations.The total effect of the errors on Fairfax's 2020 net income is

A) understated by $ 94,200.

B) understated by $ 61,200.

C) overstated by $ 28,800.

D) overstated by $ 49,800.

Question

Question

Correction of errors in prior years

Goldfinch Inc. reported net incomes for the last three years as follows: In reviewing the accounts in 2021 (after the books for the prior year had been closed), you find that the following errors have been made:

In reviewing the accounts in 2021 (after the books for the prior year had been closed), you find that the following errors have been made:  Instructions

Instructions

a) Calculate corrected net incomes for 2018, 2019, and 2020.

b) Prepare the entry required in 2021 to correct the books. Ignore income taxes.

Show any calculations.

Goldfinch Inc. reported net incomes for the last three years as follows:

In reviewing the accounts in 2021 (after the books for the prior year had been closed), you find that the following errors have been made: Instructions a) Calculate corrected net incomes for 2018, 2019, and 2020.

b) Prepare the entry required in 2021 to correct the books. Ignore income taxes.

Show any calculations.

Question

Question

Question

Accounting for accounting changes and error corrections

Parrot Corp. reported net incomes for the last three years as follows: During the 2020 year-end audit, the following items come to your attention:

During the 2020 year-end audit, the following items come to your attention:

1. Parrot bought a truck on January 1, 2017 for $ 98,000 cash, with an $ 8,000 estimated residual value and a six-year life. The company debited an expense account for the entire cost of the asset. Parrot uses straight-line depreciation for all trucks.

2. During 2020, Parrot changed from straight-line depreciation for its cement plant to double declining balance. The following calculations present depreciation on both bases: The net income for 2020 was calculated using the double declining balance method.

The net income for 2020 was calculated using the double declining balance method.

3. In reviewing its provision for uncollectible accounts during 2020, the corporation has determined that 1% is the appropriate amount of bad debt expense to be charged to operations. The company had used 1/2 of 1% as its rate in 2019 and 2018 when the expense had been $ 9,000 and $ 6,000, respectively. Parrot recorded bad debt expense using the new rate for 2020. If they had used the old rate, they would have recorded $ 3,000 less bad debt expense on December 31, 2020.

Instructions (Ignore all income tax effects)

a) Prepare the general journal entry required to correct the books for the item 1 situation (only) of this problem, assuming that the books have not been closed for 2020.

b) Present comparative income statement data for the years 2018 to 2020, starting with income before the cumulative effect of any accounting changes.

c) Assume that the beginning retained earnings balance (unadjusted) for 2018 was $ 630,000. At what adjusted amount should the beginning retained earnings balance for 2018 be shown, assuming that comparative financial statements were prepared?

d) Assume that the beginning retained earnings balance (unadjusted) for 2020 is $ 900,000 and that comparative financial statements are not prepared. At what adjusted amount should this beginning retained earnings balance be shown?

Parrot Corp. reported net incomes for the last three years as follows:

During the 2020 year-end audit, the following items come to your attention:1. Parrot bought a truck on January 1, 2017 for $ 98,000 cash, with an $ 8,000 estimated residual value and a six-year life. The company debited an expense account for the entire cost of the asset. Parrot uses straight-line depreciation for all trucks.

2. During 2020, Parrot changed from straight-line depreciation for its cement plant to double declining balance. The following calculations present depreciation on both bases:

The net income for 2020 was calculated using the double declining balance method.3. In reviewing its provision for uncollectible accounts during 2020, the corporation has determined that 1% is the appropriate amount of bad debt expense to be charged to operations. The company had used 1/2 of 1% as its rate in 2019 and 2018 when the expense had been $ 9,000 and $ 6,000, respectively. Parrot recorded bad debt expense using the new rate for 2020. If they had used the old rate, they would have recorded $ 3,000 less bad debt expense on December 31, 2020.

Instructions (Ignore all income tax effects)

a) Prepare the general journal entry required to correct the books for the item 1 situation (only) of this problem, assuming that the books have not been closed for 2020.

b) Present comparative income statement data for the years 2018 to 2020, starting with income before the cumulative effect of any accounting changes.

c) Assume that the beginning retained earnings balance (unadjusted) for 2018 was $ 630,000. At what adjusted amount should the beginning retained earnings balance for 2018 be shown, assuming that comparative financial statements were prepared?

d) Assume that the beginning retained earnings balance (unadjusted) for 2020 is $ 900,000 and that comparative financial statements are not prepared. At what adjusted amount should this beginning retained earnings balance be shown?

Question

*Error corrections and adjustments

The controller for Stork Corp. is concerned about certain business transactions that the company experienced during 2020. The controller, after discussing these matters with various individuals, has come to you for advice. The transactions at issue are presented below:

1. The company has decided to switch from the direct write-off method for accounting for bad debts to the percentage-of-sales approach. Assume that Stork has recognized bad debt expense as the receivables have actually become uncollectible in the following way: The controller estimates that an additional $ 21,800 in bad debts will be written off in 2021: $ 3,800 applicable to 2019 sales and $ 18,000 to 2020 sales.

The controller estimates that an additional $ 21,800 in bad debts will be written off in 2021: $ 3,800 applicable to 2019 sales and $ 18,000 to 2020 sales.

2. Inventory has been shipped on consignment. These transactions have been recorded as ordinary sales and billed as such (on account). At December 31, 2020, inventory billed and in the hands of consignees amounted to $ 160,000. The percentage markup on selling price is 20%. Assume that the consigned inventory is sold the following year. The company uses the perpetual inventory system.

3. During 2020, Stork sold $ 300,000 worth of goods on the instalment basis. The cost of sales associated with these instalment sales is $ 225,000. The company inadvertently handled these sales and related costs as part of their regular sales transactions. Cash of $ 86,000, including a down payment of $ 30,000, was collected on these instalment sales during 2020. Due to questionable collectability, the instalment method was considered appropriate.

Instructions

a) Assume that Stork Corp. reported pre-tax income of $ 500,000 for 2020. Present a schedule showing the corrected pre-tax income after the above transactions are taken into account. Ignore income tax effects.

b) Prepare the correcting journal entries required at December 31, 2020, assuming that the books have been closed.

The controller for Stork Corp. is concerned about certain business transactions that the company experienced during 2020. The controller, after discussing these matters with various individuals, has come to you for advice. The transactions at issue are presented below:

1. The company has decided to switch from the direct write-off method for accounting for bad debts to the percentage-of-sales approach. Assume that Stork has recognized bad debt expense as the receivables have actually become uncollectible in the following way:

The controller estimates that an additional $ 21,800 in bad debts will be written off in 2021: $ 3,800 applicable to 2019 sales and $ 18,000 to 2020 sales.2. Inventory has been shipped on consignment. These transactions have been recorded as ordinary sales and billed as such (on account). At December 31, 2020, inventory billed and in the hands of consignees amounted to $ 160,000. The percentage markup on selling price is 20%. Assume that the consigned inventory is sold the following year. The company uses the perpetual inventory system.

3. During 2020, Stork sold $ 300,000 worth of goods on the instalment basis. The cost of sales associated with these instalment sales is $ 225,000. The company inadvertently handled these sales and related costs as part of their regular sales transactions. Cash of $ 86,000, including a down payment of $ 30,000, was collected on these instalment sales during 2020. Due to questionable collectability, the instalment method was considered appropriate.

Instructions

a) Assume that Stork Corp. reported pre-tax income of $ 500,000 for 2020. Present a schedule showing the corrected pre-tax income after the above transactions are taken into account. Ignore income tax effects.

b) Prepare the correcting journal entries required at December 31, 2020, assuming that the books have been closed.

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/65

Play

Full screen (f)

Deck 9: Accounting Changes and Error Analysis

1

Accounting for a retrospective change requires

A) reissuing all prior financial statements affected by the change.

B) adjusting the ending balance of retained earnings for the current year.

C) reporting the "catch-up" adjustment on the current income statement.

D) adjusting the opening balance of each affected component of equity for the current year.

A) reissuing all prior financial statements affected by the change.

B) adjusting the ending balance of retained earnings for the current year.

C) reporting the "catch-up" adjustment on the current income statement.

D) adjusting the opening balance of each affected component of equity for the current year.

D

2

Which of the following should be given retrospective treatment?

B

3

Which of the following is NOT considered a change in accounting policy?

A) change in depreciation method

B) change from FIFO to weighted average cost

C) initial adoption of a new accounting standard

D) change in accounting for a defined benefit pension plan from deferral and amortization to immediate recognition

A) change in depreciation method

B) change from FIFO to weighted average cost

C) initial adoption of a new accounting standard

D) change in accounting for a defined benefit pension plan from deferral and amortization to immediate recognition

A

4

Which of the following is NOT considered to be an accounting error?

A) changing from the cash basis to the accrual basis

B) expensing the cost of a new machine

C) changing depreciation methods from declining balance to straight line

D) failing to accrue wages payable at year end

A) changing from the cash basis to the accrual basis

B) expensing the cost of a new machine

C) changing depreciation methods from declining balance to straight line

D) failing to accrue wages payable at year end

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

5

Which of the following is (are) the proper time period(s) to record the effects of a change in accounting estimate?

A) retrospectively only

B) current period and prospectively

C) current period and retrospectively

D) current period only

A) retrospectively only

B) current period and prospectively

C) current period and retrospectively

D) current period only

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

6

One condition required by IFRS is that a voluntary change in accounting policy must result in information that is

A) more reliable than before.

B) more reliable, but equally as relevant as before.

C) both more reliable and more relevant.

D) more relevant, but equally as reliable as before.

A) more reliable than before.

B) more reliable, but equally as relevant as before.

C) both more reliable and more relevant.

D) more relevant, but equally as reliable as before.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

7

Which of the following is NOT considered to be an accounting change?

A) change in accounting estimate

B) change in the composition of the board of directors

C) change in accounting policy

D) correction of a prior period error

A) change in accounting estimate

B) change in the composition of the board of directors

C) change in accounting policy

D) correction of a prior period error

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

8

Which of the following statements is correct?

A) Changes in accounting policy are always handled in the current or prospective period.

B) Prior year statements should always be restated for changes in accounting estimates.

C) A change from the deferral and amortization method to the immediate recognition method of accounting for defined benefit pension plans should be treated as a change in accounting policy.

D) Correction of prior period error should be presented as an adjustment on the current income statement.

A) Changes in accounting policy are always handled in the current or prospective period.

B) Prior year statements should always be restated for changes in accounting estimates.

C) A change from the deferral and amortization method to the immediate recognition method of accounting for defined benefit pension plans should be treated as a change in accounting policy.

D) Correction of prior period error should be presented as an adjustment on the current income statement.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

9

An example of a correction of an error in previously issued financial statements is a change

A) from the FIFO method of inventory valuation to the average cost method.

B) in the service life of plant assets, based on changes in the economic environment.

C) from the cash basis of accounting to the accrual basis of accounting.

D) in the tax assessment related to a prior period.

A) from the FIFO method of inventory valuation to the average cost method.

B) in the service life of plant assets, based on changes in the economic environment.

C) from the cash basis of accounting to the accrual basis of accounting.

D) in the tax assessment related to a prior period.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

10

Stockton Ltd. changed its inventory system from FIFO to average cost. What type of accounting change does this represent?

A) A change in accounting estimate for which the financial statements for the prior periods included for comparative purposes do not need to be restated.

B) A change in accounting policy for which the financial statements for prior periods included for comparative purposes do not need to be restated.

C) A change in accounting policy for which the financial statements for prior periods included for comparative purposes should be restated.

D) A change in accounting estimate for which the financial statements for prior periods included for comparative purposes should be restated.

A) A change in accounting estimate for which the financial statements for the prior periods included for comparative purposes do not need to be restated.

B) A change in accounting policy for which the financial statements for prior periods included for comparative purposes do not need to be restated.

C) A change in accounting policy for which the financial statements for prior periods included for comparative purposes should be restated.

D) A change in accounting estimate for which the financial statements for prior periods included for comparative purposes should be restated.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

11

Retrospective application is required for all

A) errors and non-mandated policy changes.

B) changes in estimates and non-mandated policy changes.

C) errors and changes in estimates.

D) changes in estimates.

A) errors and non-mandated policy changes.

B) changes in estimates and non-mandated policy changes.

C) errors and changes in estimates.

D) changes in estimates.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

12

For accounting changes, which of the following is NOT allowed?

A) To use retrospective application for an accounting policy change without restatement, if restatement is impractical.

B) To net accounting errors for disclosure purposes.

C) To use prospective application for an accounting policy change, if allowed in the transition policy.

D) To use prospective application for a change in estimate.

A) To use retrospective application for an accounting policy change without restatement, if restatement is impractical.

B) To net accounting errors for disclosure purposes.

C) To use prospective application for an accounting policy change, if allowed in the transition policy.

D) To use prospective application for a change in estimate.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

13

Which of the following alternative accounting methods is(are) allowed by ASPE and IFRS for reporting accounting changes?

A) prospective and retrospective

B) current and retrospective

C) current and prospective

D) retrospective only

A) prospective and retrospective

B) current and retrospective

C) current and prospective

D) retrospective only

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

14

The underlying principle of the retrospective application method is to

A) apply changes currently and in the future.

B) present all comparative periods as if the new accounting policy had always been used.

C) make assumptions about what management's intent was in prior years.

D) disclose all mistakes made in the past.

A) apply changes currently and in the future.

B) present all comparative periods as if the new accounting policy had always been used.

C) make assumptions about what management's intent was in prior years.

D) disclose all mistakes made in the past.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

15

A publicly accountable enterprise changes from straight-line depreciation to double declining balance. Management feels that this will result in equally reliable and more relevant information; thus it will be treated as a change in accounting policy. The entry to record this change should include a

A) debit to Accumulated Depreciation.

B) credit to Other Comprehensive Income.

C) credit to Deferred Tax Asset.

D) debit to Deferred Tax Liability.

A) debit to Accumulated Depreciation.

B) credit to Other Comprehensive Income.

C) credit to Deferred Tax Asset.

D) debit to Deferred Tax Liability.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

16

When an entity is first transitioning to IFRS, any adjustments required to bring GAAP measures in line with IFRS

A) are recognized directly in other comprehensive income.

B) are recognized directly in retained earnings.

C) must be accounted for by prospective application.

D) are ignored.

A) are recognized directly in other comprehensive income.

B) are recognized directly in retained earnings.

C) must be accounted for by prospective application.

D) are ignored.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

17

When a company decides to switch from deferring development costs to expensing them immediately, this change should probably be treated as a

A) change in accounting policy.

B) change in accounting estimate.

C) prior period adjustment.

D) correction of an error.

A) change in accounting policy.

B) change in accounting estimate.

C) prior period adjustment.

D) correction of an error.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

18

Which type of accounting change may be accounted for in current and future periods only?

A) change in accounting estimate

B) change in inventory costing method

C) change in accounting policy

D) correction of an error

A) change in accounting estimate

B) change in inventory costing method

C) change in accounting policy

D) correction of an error

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

19

Under IFRS, which of the following disclosures is NOT required for the correction of an accounting error?

A) the amount of the correction made to each affected financial statement item for each prior period presented

B) the nature of the error

C) who was responsible for the error

D) the effect of the correction on both basic and diluted earnings per share for each prior period presented

A) the amount of the correction made to each affected financial statement item for each prior period presented

B) the nature of the error

C) who was responsible for the error

D) the effect of the correction on both basic and diluted earnings per share for each prior period presented

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

20

Which of the following is NOT considered to be a change in accounting policy?

A) changing from weighted average to FIFO for valuing inventories

B) initial adoption of a new accounting standard

C) reclassifying items on the financial statements of prior periods to make the statements more comparable

D) changing from the cost basis to the fair value model for measuring investments

A) changing from weighted average to FIFO for valuing inventories

B) initial adoption of a new accounting standard

C) reclassifying items on the financial statements of prior periods to make the statements more comparable

D) changing from the cost basis to the fair value model for measuring investments

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

21

Use the following information for questions 30-31.

Major Corp. purchased a machine on January 1, 2017, for $ 900,000. The machine is being depreciated on a straight-line basis, using an estimated useful life of six years and no residual value. On January 1, 2020, Major determined, as a result of additional information, that the machine had an estimated useful life of eight years from the date of acquisition with no residual value. An accounting change was made in 2020 to reflect this additional information.

What is the amount of depreciation expense on this machine that should be reported in Major's income statement for calendar 2020?

A) $ 225,000

B) $ 180,000

C) $ 112,500

D) $ 90,000

Major Corp. purchased a machine on January 1, 2017, for $ 900,000. The machine is being depreciated on a straight-line basis, using an estimated useful life of six years and no residual value. On January 1, 2020, Major determined, as a result of additional information, that the machine had an estimated useful life of eight years from the date of acquisition with no residual value. An accounting change was made in 2020 to reflect this additional information.

What is the amount of depreciation expense on this machine that should be reported in Major's income statement for calendar 2020?

A) $ 225,000

B) $ 180,000

C) $ 112,500

D) $ 90,000

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

22

On January 1, 2020, Miner Corp. changed its inventory costing from FIFO to average cost for financial statement and income tax purposes, to make their reporting as reliable and more relevant. The change resulted in a $ 600,000 increase in the beginning inventory at January 1, 2020. Assume a 30% income tax rate. The cumulative effect of this accounting change should be reported by Chickadee in its 2020

A) Retained earnings statement as a $ 420,000 addition to the beginning balance.

B) Income statement as $ 420,000 other comprehensive income.

C) Retained earnings statement as a $ 600,000 addition to the beginning balance.

D) Income statement as a $ 600,000 cumulative effect of accounting change.

A) Retained earnings statement as a $ 420,000 addition to the beginning balance.

B) Income statement as $ 420,000 other comprehensive income.

C) Retained earnings statement as a $ 600,000 addition to the beginning balance.

D) Income statement as a $ 600,000 cumulative effect of accounting change.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

23

Use the following information for questions *38-*40.

Cheyenne Ltd.'s December 31 year-end financial statements contained the following errors: An insurance premium of $ 3,600 was prepaid in 2019 covering the calendar years 2019, 2020, and 2021. This had been debited to insurance expense. In addition, on December 31, 2020, fully depreciated machinery was sold for $ 1,900 cash, but the sale was not recorded until 2021. There were no other errors during 2020 or 2021 and no corrections have been made for any of the errors. Ignore income tax considerations.

A company using a perpetual inventory system neglected to record a purchase of merchandise on account at year end. This merchandise was also omitted from the year-end physical count. How will these errors affect assets, liabilities, and shareholders' equity at year end and net income for the year? Assets Liabilities Shareholders' Equity Net Income

A) no effect understate overstate overstate

B) no effect overstate understate understate

C) understate understate no effect no effect

D) understate no effect understate understate

Cheyenne Ltd.'s December 31 year-end financial statements contained the following errors:

An insurance premium of $ 3,600 was prepaid in 2019 covering the calendar years 2019, 2020, and 2021. This had been debited to insurance expense. In addition, on December 31, 2020, fully depreciated machinery was sold for $ 1,900 cash, but the sale was not recorded until 2021. There were no other errors during 2020 or 2021 and no corrections have been made for any of the errors. Ignore income tax considerations.A company using a perpetual inventory system neglected to record a purchase of merchandise on account at year end. This merchandise was also omitted from the year-end physical count. How will these errors affect assets, liabilities, and shareholders' equity at year end and net income for the year? Assets Liabilities Shareholders' Equity Net Income

A) no effect understate overstate overstate

B) no effect overstate understate understate

C) understate understate no effect no effect

D) understate no effect understate understate

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

24

Use the following information for questions *38-*40.

Cheyenne Ltd.'s December 31 year-end financial statements contained the following errors: An insurance premium of $ 3,600 was prepaid in 2019 covering the calendar years 2019, 2020, and 2021. This had been debited to insurance expense. In addition, on December 31, 2020, fully depreciated machinery was sold for $ 1,900 cash, but the sale was not recorded until 2021. There were no other errors during 2020 or 2021 and no corrections have been made for any of the errors. Ignore income tax considerations.

MissTake Corp. is a small private corporation that does not prepare comparative statements. At the end of their 2020 fiscal year, it was discovered that the 2019 depreciation expense on their computer equipment had been incorrectly debited to maintenance expense. How should MissTake deal with this situation?

A) Prepare an adjusting entry to debit depreciation expense and credit maintenance expense.

B) Prepare an adjusting entry to debit retained earnings and credit maintenance expense.

C) Restate their 2019 financial statements.

D) Ignore it.

Cheyenne Ltd.'s December 31 year-end financial statements contained the following errors:

An insurance premium of $ 3,600 was prepaid in 2019 covering the calendar years 2019, 2020, and 2021. This had been debited to insurance expense. In addition, on December 31, 2020, fully depreciated machinery was sold for $ 1,900 cash, but the sale was not recorded until 2021. There were no other errors during 2020 or 2021 and no corrections have been made for any of the errors. Ignore income tax considerations.MissTake Corp. is a small private corporation that does not prepare comparative statements. At the end of their 2020 fiscal year, it was discovered that the 2019 depreciation expense on their computer equipment had been incorrectly debited to maintenance expense. How should MissTake deal with this situation?

A) Prepare an adjusting entry to debit depreciation expense and credit maintenance expense.

B) Prepare an adjusting entry to debit retained earnings and credit maintenance expense.

C) Restate their 2019 financial statements.

D) Ignore it.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

25

On January 1, 2017, Casino Inc. purchased a machine for $ 300,000. The machine has an estimated five year life, and no residual value. Double declining balance depreciation has been used for financial statement reporting and CCA for income tax reporting. Effective January 1, 2020, Casino decided to change to straight-line depreciation for this machine, and treated the change as a change in accounting policy. For calendar 2020, Casino's pre-tax income before depreciation on this asset is $ 250,000. Their income tax rate has been 30% for many years. What net income should Casino report for calendar 2020?

A) $ 190,000

B) $ 171,640

C) $ 133,000

D) $ 91,000

A) $ 190,000

B) $ 171,640

C) $ 133,000

D) $ 91,000

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

26

Randall Corp. began operations on January 1, 2019, and uses FIFO to cost its inventory. Management is contemplating a change to the average cost method and is interested in determining what effect such a change will have on pre-tax income. Accordingly, the following information has been developed: Based upon the above information, a change to the average cost method in 2020 would result in pre-tax income for 2020 of

A) $ 790,000.

B) $ 860,000.

C) $ 940,000.

D) $ 980,000.

Based upon the above information, a change to the average cost method in 2020 would result in pre-tax income for 2020 ofA) $ 790,000.

B) $ 860,000.

C) $ 940,000.

D) $ 980,000.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

27

Use the following information for questions *38-*40.

Cheyenne Ltd.'s December 31 year-end financial statements contained the following errors: An insurance premium of $ 3,600 was prepaid in 2019 covering the calendar years 2019, 2020, and 2021. This had been debited to insurance expense. In addition, on December 31, 2020, fully depreciated machinery was sold for $ 1,900 cash, but the sale was not recorded until 2021. There were no other errors during 2020 or 2021 and no corrections have been made for any of the errors. Ignore income tax considerations.

Counterbalancing errors do NOT include

A) errors that correct themselves in two years.

B) errors that correct themselves in three or more years.

C) an understatement of ending inventory.

D) an overstatement of unearned revenue.

Cheyenne Ltd.'s December 31 year-end financial statements contained the following errors:

An insurance premium of $ 3,600 was prepaid in 2019 covering the calendar years 2019, 2020, and 2021. This had been debited to insurance expense. In addition, on December 31, 2020, fully depreciated machinery was sold for $ 1,900 cash, but the sale was not recorded until 2021. There were no other errors during 2020 or 2021 and no corrections have been made for any of the errors. Ignore income tax considerations.Counterbalancing errors do NOT include

A) errors that correct themselves in two years.

B) errors that correct themselves in three or more years.

C) an understatement of ending inventory.

D) an overstatement of unearned revenue.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

28

Use the following information for questions *38-*40.

Cheyenne Ltd.'s December 31 year-end financial statements contained the following errors: An insurance premium of $ 3,600 was prepaid in 2019 covering the calendar years 2019, 2020, and 2021. This had been debited to insurance expense. In addition, on December 31, 2020, fully depreciated machinery was sold for $ 1,900 cash, but the sale was not recorded until 2021. There were no other errors during 2020 or 2021 and no corrections have been made for any of the errors. Ignore income tax considerations.

On December 31, 2020, the bookkeeper at Thrush Corp. did not record special insurance costs that had been incurred (but not yet paid), related to a building that Thrush Corp. is constructing. What is the effect of the omission on accrued liabilities and retained earnings in the December 31, 2020 statement of financial position?

Cheyenne Ltd.'s December 31 year-end financial statements contained the following errors:

An insurance premium of $ 3,600 was prepaid in 2019 covering the calendar years 2019, 2020, and 2021. This had been debited to insurance expense. In addition, on December 31, 2020, fully depreciated machinery was sold for $ 1,900 cash, but the sale was not recorded until 2021. There were no other errors during 2020 or 2021 and no corrections have been made for any of the errors. Ignore income tax considerations.On December 31, 2020, the bookkeeper at Thrush Corp. did not record special insurance costs that had been incurred (but not yet paid), related to a building that Thrush Corp. is constructing. What is the effect of the omission on accrued liabilities and retained earnings in the December 31, 2020 statement of financial position?

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

29

The service life of a building that has been depreciated for 30 years of an originally estimated 50-year life (no residual value) has been revised to an estimated remaining life of 10 years. Based on this information, the accountant should

A) continue to depreciate the building over the original 50-year life.

B) depreciate the remaining book value over the remaining life of the asset.

C) adjust accumulated depreciation to its appropriate balance through net income, based on a 40-year life, and then depreciate the adjusted book value as though the estimated life had always been 40 years.

D) adjust accumulated depreciation to its appropriate balance through retained earnings, based on a 40-year life, and then depreciate the adjusted book value as though the estimated life had always been 40 years.

A) continue to depreciate the building over the original 50-year life.

B) depreciate the remaining book value over the remaining life of the asset.

C) adjust accumulated depreciation to its appropriate balance through net income, based on a 40-year life, and then depreciate the adjusted book value as though the estimated life had always been 40 years.

D) adjust accumulated depreciation to its appropriate balance through retained earnings, based on a 40-year life, and then depreciate the adjusted book value as though the estimated life had always been 40 years.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

30

On January 1, 2020, Bluebird Ltd. changed its inventory valuation method from weighted-average cost to FIFO for financial statement and income tax purposes, to make their reporting as reliable and more relevant. The change resulted in a $ 900,000 increase in the beginning inventory at January 1, 2020. Assume a 25% income tax rate. The cumulative effect of this accounting change reported for the year ended December 31, 2020 is

A) $ 0.

B) $ 225,000.

C) $ 675,000.

D) $ 900,000.

A) $ 0.

B) $ 225,000.

C) $ 675,000.

D) $ 900,000.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

31

Use the following information for questions 25-26.

On January 2, 2018, Moose Corp. purchased machinery for $ 270,000. The entire cost was incorrectly recorded as an expense. The machinery has a nine-year life and a $ 18,000 residual value. Beaver uses straight-line depreciation for all its plant assets. The error was not discovered until May 1, 2020, and the appropriate corrections were made. Ignore income tax considerations.

Moose's income statement for the year ended December 31, 2020 would show the cumulative effect of this error in the amount of:

A) $ 0.

B) $ 186,000.

C) $ 214,000.

D) $ 242,000.

On January 2, 2018, Moose Corp. purchased machinery for $ 270,000. The entire cost was incorrectly recorded as an expense. The machinery has a nine-year life and a $ 18,000 residual value. Beaver uses straight-line depreciation for all its plant assets. The error was not discovered until May 1, 2020, and the appropriate corrections were made. Ignore income tax considerations.

Moose's income statement for the year ended December 31, 2020 would show the cumulative effect of this error in the amount of:

A) $ 0.

B) $ 186,000.

C) $ 214,000.

D) $ 242,000.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

32

On January 1, 2017, Wren Corp. purchased a patent for $ 238,000. The patent is being amortized straight-line with no residual value over its remaining legal life of 15 years. At the beginning of 2020, however, Wren determined that the economic benefits of the patent would not last longer than ten years from the date of acquisition. What amount should be reported in the 2020 of financial position for the patent, net of accumulated amortization, at December 31, 2020?

A) $ 142,800

B) $ 163,200

C) $ 168,000

D) $ 174,550

A) $ 142,800

B) $ 163,200

C) $ 168,000

D) $ 174,550

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

33

Use the following information for questions *38-*40.

Cheyenne Ltd.'s December 31 year-end financial statements contained the following errors: An insurance premium of $ 3,600 was prepaid in 2019 covering the calendar years 2019, 2020, and 2021. This had been debited to insurance expense. In addition, on December 31, 2020, fully depreciated machinery was sold for $ 1,900 cash, but the sale was not recorded until 2021. There were no other errors during 2020 or 2021 and no corrections have been made for any of the errors. Ignore income tax considerations.

What is the total net effect of the errors on Cheyenne's 2020 net income?

A) Net income understated by $ 2,900

B) Net income overstated by $ 1,500

C) Net income overstated by $ 2,600

D) Net income overstated by $ 3,000

Cheyenne Ltd.'s December 31 year-end financial statements contained the following errors:

An insurance premium of $ 3,600 was prepaid in 2019 covering the calendar years 2019, 2020, and 2021. This had been debited to insurance expense. In addition, on December 31, 2020, fully depreciated machinery was sold for $ 1,900 cash, but the sale was not recorded until 2021. There were no other errors during 2020 or 2021 and no corrections have been made for any of the errors. Ignore income tax considerations.What is the total net effect of the errors on Cheyenne's 2020 net income?

A) Net income understated by $ 2,900

B) Net income overstated by $ 1,500

C) Net income overstated by $ 2,600

D) Net income overstated by $ 3,000

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

34

On January 1, 2016, Manchester Ltd. purchased a machine for $ 495,000 and depreciated it using the straight-line method with an estimated useful life of eight years with no residual value. On January 1, 2019, Plover determined that the machine had a useful life of only six years from the date of acquisition, but will have a residual value of $ 45,000. An accounting change was made in 2019 to reflect these additional facts. At December 31, 2020, the accumulated depreciation account for this machine should have a balance of

A) $ 273,750.

B) $ 281,250.

C) $ 361,875.

D) $ 375,000.

A) $ 273,750.

B) $ 281,250.

C) $ 361,875.

D) $ 375,000.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

35

Use the following information for questions *38-*40.

Cheyenne Ltd.'s December 31 year-end financial statements contained the following errors: An insurance premium of $ 3,600 was prepaid in 2019 covering the calendar years 2019, 2020, and 2021. This had been debited to insurance expense. In addition, on December 31, 2020, fully depreciated machinery was sold for $ 1,900 cash, but the sale was not recorded until 2021. There were no other errors during 2020 or 2021 and no corrections have been made for any of the errors. Ignore income tax considerations.

What is the total effect of the errors on the balance of Cheyenne's retained earnings at December 31, 2020?

A) Retained earnings understated by $ 2,000

B) Retained earnings understated by $ 900

C) Retained earnings understated by $ 500

D) Retained earnings overstated by $ 700

Cheyenne Ltd.'s December 31 year-end financial statements contained the following errors:

An insurance premium of $ 3,600 was prepaid in 2019 covering the calendar years 2019, 2020, and 2021. This had been debited to insurance expense. In addition, on December 31, 2020, fully depreciated machinery was sold for $ 1,900 cash, but the sale was not recorded until 2021. There were no other errors during 2020 or 2021 and no corrections have been made for any of the errors. Ignore income tax considerations.What is the total effect of the errors on the balance of Cheyenne's retained earnings at December 31, 2020?

A) Retained earnings understated by $ 2,000

B) Retained earnings understated by $ 900

C) Retained earnings understated by $ 500

D) Retained earnings overstated by $ 700

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

36

Use the following information for questions 30-31.

Major Corp. purchased a machine on January 1, 2017, for $ 900,000. The machine is being depreciated on a straight-line basis, using an estimated useful life of six years and no residual value. On January 1, 2020, Major determined, as a result of additional information, that the machine had an estimated useful life of eight years from the date of acquisition with no residual value. An accounting change was made in 2020 to reflect this additional information.

Assuming that the direct effects of this change are limited to the effect on depreciation and the related tax provision, and that the income tax rate for all years since the machine was purchased was 30%, what should be reported in the income statement for calendar 2020 as the cumulative effect on prior years of changing the estimated useful life of the machine?

A) $ 0

B) $ 60,000

C) $ 90,000

D) $ 315,000

Major Corp. purchased a machine on January 1, 2017, for $ 900,000. The machine is being depreciated on a straight-line basis, using an estimated useful life of six years and no residual value. On January 1, 2020, Major determined, as a result of additional information, that the machine had an estimated useful life of eight years from the date of acquisition with no residual value. An accounting change was made in 2020 to reflect this additional information.

Assuming that the direct effects of this change are limited to the effect on depreciation and the related tax provision, and that the income tax rate for all years since the machine was purchased was 30%, what should be reported in the income statement for calendar 2020 as the cumulative effect on prior years of changing the estimated useful life of the machine?

A) $ 0

B) $ 60,000

C) $ 90,000

D) $ 315,000

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

37

On January 1, 2017, Cumberland Ltd. bought machinery for $ 750,000. They used straight-line depreciation for this machinery, over an estimated useful life of ten years, with no residual value. At the beginning of 2020, Detroit decided the estimated useful life of this machinery was only eight years (from the date of acquisition), still with no residual value. For calendar 2020, the depreciation expense for this machinery is

A) $ 75,000.

B) $ 65,625.

C) $ 105,000.

D) $ 93,750.

A) $ 75,000.

B) $ 65,625.

C) $ 105,000.

D) $ 93,750.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

38

Use the following information for questions 25-26.

On January 2, 2018, Moose Corp. purchased machinery for $ 270,000. The entire cost was incorrectly recorded as an expense. The machinery has a nine-year life and a $ 18,000 residual value. Beaver uses straight-line depreciation for all its plant assets. The error was not discovered until May 1, 2020, and the appropriate corrections were made. Ignore income tax considerations.

Before the corrections were made, retained earnings was understated by

A) $ 270,000.

B) $ 242,000.

C) $ 214,000.

D) $ 186,000.

On January 2, 2018, Moose Corp. purchased machinery for $ 270,000. The entire cost was incorrectly recorded as an expense. The machinery has a nine-year life and a $ 18,000 residual value. Beaver uses straight-line depreciation for all its plant assets. The error was not discovered until May 1, 2020, and the appropriate corrections were made. Ignore income tax considerations.

Before the corrections were made, retained earnings was understated by

A) $ 270,000.

B) $ 242,000.

C) $ 214,000.

D) $ 186,000.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

39

On January 1, 2017, Missoula Corporation bought machinery for $ 800,000. They used double declining balance depreciation for this asset, with an estimated life of eight years, and an estimated $ 200,000 residual value. At the beginning of 2020, Missoula decided to change to the straight-line method of depreciation for this equipment, and treated the change as a change in estimate. For calendar 2020, the depreciation expense for this machinery is

A) $ 100,000.

B) $ 92,500.

C) $ 75,050.

D) $ 27,500.

A) $ 100,000.

B) $ 92,500.

C) $ 75,050.

D) $ 27,500.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

40

Use the following information for questions *38-*40.

Cheyenne Ltd.'s December 31 year-end financial statements contained the following errors: An insurance premium of $ 3,600 was prepaid in 2019 covering the calendar years 2019, 2020, and 2021. This had been debited to insurance expense. In addition, on December 31, 2020, fully depreciated machinery was sold for $ 1,900 cash, but the sale was not recorded until 2021. There were no other errors during 2020 or 2021 and no corrections have been made for any of the errors. Ignore income tax considerations.

What is the total net effect of the errors on the amount of Cheyenne's working capital at December 31, 2020?

A) Working capital overstated by $ 1,000

B) Working capital overstated by $ 300

C) Working capital understated by $ 900

D) Working capital understated by $ 2,400

Cheyenne Ltd.'s December 31 year-end financial statements contained the following errors:

An insurance premium of $ 3,600 was prepaid in 2019 covering the calendar years 2019, 2020, and 2021. This had been debited to insurance expense. In addition, on December 31, 2020, fully depreciated machinery was sold for $ 1,900 cash, but the sale was not recorded until 2021. There were no other errors during 2020 or 2021 and no corrections have been made for any of the errors. Ignore income tax considerations.What is the total net effect of the errors on the amount of Cheyenne's working capital at December 31, 2020?

A) Working capital overstated by $ 1,000

B) Working capital overstated by $ 300

C) Working capital understated by $ 900

D) Working capital understated by $ 2,400

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

41

Explain the circumstances in which an accounting policy can be changed under IFRS versus ASPE.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

42

Provide and explain four reasons why companies may prefer/choose certain accounting methods and procedures over others.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

43

Economic reasons for changing accounting policies

Discuss possible economic reasons why companies may choose to change accounting policies.

Discuss possible economic reasons why companies may choose to change accounting policies.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

44

*Non-counterbalancing error correction

Turkey Corp. bought a machine on January 3, 2018 for $ 275,000. It had a $ 15,000 estimated residual value and a ten-year life. The corporation uses straight-line depreciation. An expense account was debited in error on the purchase date, but this was not discovered until late 2020.

Instructions

Prepare the correcting entry or entries related to the machine for 2020. Ignore income tax effects.

Turkey Corp. bought a machine on January 3, 2018 for $ 275,000. It had a $ 15,000 estimated residual value and a ten-year life. The corporation uses straight-line depreciation. An expense account was debited in error on the purchase date, but this was not discovered until late 2020.

Instructions

Prepare the correcting entry or entries related to the machine for 2020. Ignore income tax effects.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

45

Use the following information for questions *38-*40.

Cheyenne Ltd.'s December 31 year-end financial statements contained the following errors: An insurance premium of $ 3,600 was prepaid in 2019 covering the calendar years 2019, 2020, and 2021. This had been debited to insurance expense. In addition, on December 31, 2020, fully depreciated machinery was sold for $ 1,900 cash, but the sale was not recorded until 2021. There were no other errors during 2020 or 2021 and no corrections have been made for any of the errors. Ignore income tax considerations.

At December 31, 2020, Grant Corp.'s auditor discovered the following errors:

1) Accrued salaries payable of $ 11,000 were NOT recorded at December 31, 2019.

2) Office supplies on hand of $ 5,000 at December 31, 2020 had been treated as expense instead of supplies inventory.

Neither of these errors was discovered nor corrected. The effect of these two errors would cause

A) 2020 net income to be understated $ 16,000 and December 31, 2020 retained earnings to be understated $ 5,000.

B) 2019 net income and December 31, 2019 retained earnings to be understated $ 11,000 each.

C) 2019 net income to be overstated $ 6,000 and 2020 net income to be understated $ 5,000.

D) 2020 net income and December 31, 2020 retained earnings to be understated $ 5,000 each.

Cheyenne Ltd.'s December 31 year-end financial statements contained the following errors: