Deck 13: Financial Instruments: Long-Term Debt

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

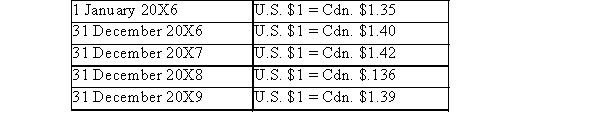

ABC Inc.borrowed funds from its bank.Details are as follows.

Four year term loan, U.S.$500,000

Funds borrowed 1 January 20X6; due 31 December 20X9 Exchange rates: Part A: Based on the above information prepare entries to record receipt of loan proceeds for January 20X6.

Part A: Based on the above information prepare entries to record receipt of loan proceeds for January 20X6.

Part B: Based on the above information prepare entries to record the adjustment to spot rate for December 20X6.

Part C: Based on the above information prepare entries to record adjustment to spot rate December

20X7

Part D: Based on the above information prepare entries to record adjustment to spot rate December 20X8

Part E: Based on the above information prepare entries to record adjustment to spot rate December 20X9

Part F: Based on the above information prepare entries to record repayment of loan December 20X9 Part G: Based on the above information calculate the total accounting recognition of loss.

Four year term loan, U.S.$500,000

Funds borrowed 1 January 20X6; due 31 December 20X9 Exchange rates:

Part A: Based on the above information prepare entries to record receipt of loan proceeds for January 20X6.Part B: Based on the above information prepare entries to record the adjustment to spot rate for December 20X6.

Part C: Based on the above information prepare entries to record adjustment to spot rate December

20X7

Part D: Based on the above information prepare entries to record adjustment to spot rate December 20X8

Part E: Based on the above information prepare entries to record adjustment to spot rate December 20X9

Part F: Based on the above information prepare entries to record repayment of loan December 20X9 Part G: Based on the above information calculate the total accounting recognition of loss.

Question

A company wishes to finance a long-term construction project and in doing so, capitalize the related interest expense.The company requires $2 million in financing.

The company currently has the following debt and equity items on its December 31st, 2019 Balance Sheet: There are 10,000 common shares outstanding which pay an annual dividend of $5 per share.The company can borrow a maximum of $5 million on its unsecured line of credit.

There are 10,000 common shares outstanding which pay an annual dividend of $5 per share.The company can borrow a maximum of $5 million on its unsecured line of credit.

The company's bank has indicated its willingness to extend an additional credit facility in the amount of $1.5 million at an annual rate of 5% as of March 31st, Year 6.These amounts remained outstanding throughout Year 6.

On March 1st, Year 6 the company borrowed $600,000.On April 1st, Year 6, and additional $1.4 million was wired to the company's account, drawn on its new credit facility.

Determine the amount of interest that the company would be able to capitalize as per IFRS for Year

The company currently has the following debt and equity items on its December 31st, 2019 Balance Sheet:

There are 10,000 common shares outstanding which pay an annual dividend of $5 per share.The company can borrow a maximum of $5 million on its unsecured line of credit.The company's bank has indicated its willingness to extend an additional credit facility in the amount of $1.5 million at an annual rate of 5% as of March 31st, Year 6.These amounts remained outstanding throughout Year 6.

On March 1st, Year 6 the company borrowed $600,000.On April 1st, Year 6, and additional $1.4 million was wired to the company's account, drawn on its new credit facility.

Determine the amount of interest that the company would be able to capitalize as per IFRS for Year

Question

Question

Question

Question

Question

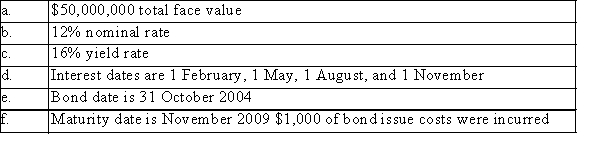

In August 2005, Crown Corporation Inc., a calendar-year corporation that records adjusting entries only once per year, issued bonds with the following characteristics:  Part A: Provide the entries required on 1 August 2007 under the effective interest method of amortization.

Part A: Provide the entries required on 1 August 2007 under the effective interest method of amortization.

Part B: Provide the entries required on 1 August 2007 under the straight line method of amortization.

Part A: Provide the entries required on 1 August 2007 under the effective interest method of amortization.Part B: Provide the entries required on 1 August 2007 under the straight line method of amortization.

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/74

Play

Full screen (f)

Deck 13: Financial Instruments: Long-Term Debt

1

Which of the following is true with respect to bond retirement?

A)On debt retirement all related accounts should be update.

B)Gains and losses on bond retirements may be classified as ordinary gains and losses or unusual gains and losses.

C)If interest rates increase, the issuer can retire bonds at a gain by buying them on the open market.

D)All of these answers are correct.

A)On debt retirement all related accounts should be update.

B)Gains and losses on bond retirements may be classified as ordinary gains and losses or unusual gains and losses.

C)If interest rates increase, the issuer can retire bonds at a gain by buying them on the open market.

D)All of these answers are correct.

D

2

On March 1, 2012, WC issued 10% stated interest rate, 10 year debentures dated January 1, 2012, in the face amount of $1,000,000, with interest payable on January 1 and July 1.The debentures were sold to yield 8% plus accrued interest.How much should WC debit to cash on March 1, 2012, if the bondholders receive their pro-rata share of coupon on that date?

A)$901,967

B)$903,003

C)$1,152,573

D)$1,135,927

A)$901,967

B)$903,003

C)$1,152,573

D)$1,135,927

C

3

The result of an effective interest rate that is higher than the stated rate on a debt security is the:

A)Carrying value of the debt will decrease each interest period.

B)Dollar amount of interest expense reported on the income statement, assuming the interest method is used, will increase each interest period.

C)Cash interest paid on each interest date will be changed.

D)Security will sell at a premium.

A)Carrying value of the debt will decrease each interest period.

B)Dollar amount of interest expense reported on the income statement, assuming the interest method is used, will increase each interest period.

C)Cash interest paid on each interest date will be changed.

D)Security will sell at a premium.

B

4

Which of the following statements is true?

A)If a bond is sold "at a discount," the effective interest rate on the bond is lower than the stated interest rate.

B)Bond price of 98 means that the yield rate is 98% of the stated rate.

C)If a bond is sold "at a premium," the effective interest rate on the bond is higher than the stated interest rate.

D)If a bond is sold between interest dates, it is necessary to record the interest accrued since the last payment date before sale.

A)If a bond is sold "at a discount," the effective interest rate on the bond is lower than the stated interest rate.

B)Bond price of 98 means that the yield rate is 98% of the stated rate.

C)If a bond is sold "at a premium," the effective interest rate on the bond is higher than the stated interest rate.

D)If a bond is sold between interest dates, it is necessary to record the interest accrued since the last payment date before sale.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

5

A firm retired a long-term note by in-substance defeasance.This means that:

A)the creditors have been paid.

B)the debtor has been released of its legal responsibility for all remaining debt payments.

C)the debt is shown as an offset against the assets used to retire the debt, in the debtor's balance sheet.

D)there is only a remote chance that the debtor will be required to make further payments on the liability.

E)the debtor will continue to recognize interest expense on the debt but will make no more payments.

A)the creditors have been paid.

B)the debtor has been released of its legal responsibility for all remaining debt payments.

C)the debt is shown as an offset against the assets used to retire the debt, in the debtor's balance sheet.

D)there is only a remote chance that the debtor will be required to make further payments on the liability.

E)the debtor will continue to recognize interest expense on the debt but will make no more payments.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

6

ER issued for $2,060,000, two thousand of its 9%, $1,000 callable bonds.The bonds are dated January 1, 2019, and mature many years from now.Interest is payable semi-annually on January 1 and July 1.The bonds can be called by the issuer at $102 on any interest payment date after December 31, 2023.The unamortized bond premium was

$28,000 at December 31, 2021, and the market price of the bonds was $99 on this date.In its December 31, 2021, balance sheet, at what amount should GC report the carrying value of the bonds?

A)$2,028,000

B)$2,040,000

C)$2,032,000

D)$1,980,000

E)Cannot answer; the bond term is not given

$28,000 at December 31, 2021, and the market price of the bonds was $99 on this date.In its December 31, 2021, balance sheet, at what amount should GC report the carrying value of the bonds?

A)$2,028,000

B)$2,040,000

C)$2,032,000

D)$1,980,000

E)Cannot answer; the bond term is not given

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

7

When the interest payment dates of a bond are May 31 and November 30, and a bond issue is sold on July 1, the price of the bond will be:

A)Increased by accrued interest from July 1 to November 30.

B)Increased by accrued interest from May 31 to July 1.

C)Decreased by accrued interest from May 31 to July 1.

D)Unaffected by accrued interest.

E)Decreased by accrued interest from July 1 to November 30.

A)Increased by accrued interest from July 1 to November 30.

B)Increased by accrued interest from May 31 to July 1.

C)Decreased by accrued interest from May 31 to July 1.

D)Unaffected by accrued interest.

E)Decreased by accrued interest from July 1 to November 30.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

8

In-substance defeasance is sometimes used as a method of bond retirement.Choose the correct statement about this practice.

A)The firm may invest in any investment-grade debt security to retire the bonds as long as the investment securities are transferred irrevocably to a trustee

B)The process may require the company which issued the bonds to make substantial payments in addition to the investments purchased for the defeasance

C)The bonds are legally retired as a result

D)Neither the assets used to effect the defeasance, nor the bonds themselves, are reported in the balance sheet, even though the bonds remain outstanding

A)The firm may invest in any investment-grade debt security to retire the bonds as long as the investment securities are transferred irrevocably to a trustee

B)The process may require the company which issued the bonds to make substantial payments in addition to the investments purchased for the defeasance

C)The bonds are legally retired as a result

D)Neither the assets used to effect the defeasance, nor the bonds themselves, are reported in the balance sheet, even though the bonds remain outstanding

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

9

VB owes a $200,000, 8%, five-year note payable dated January 1, 2020.It is the end of year 2020, and instead of making the interest payment now due, VB has made arrangements to pay the debt and the 2020 interest payment in four equal instalments based on the same interest rate.The first payment is to be made on January 1, 2021.The amount of the equal annual payments is (rounded to the nearest dollar):

A)$60,384

B)$65,214

C)$54,000

D)$55,912

A)$60,384

B)$65,214

C)$54,000

D)$55,912

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

10

R Company was indebted to A Inc.at January 1, 2014.The note called for a $25,000 payment to be made on December 31, 2014 and also on December 31, 2015.The note was non-interest bearing yet 10% was the prevailing rate at the time the note was issued.What is the book value of the note on R's January 1, 2014 balance sheet (rounded)?

A)$50,000

B)$38,962

C)$47,727

D)$43,388

E)$47,500

A)$50,000

B)$38,962

C)$47,727

D)$43,388

E)$47,500

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

11

Gains or losses from the early extinguishment of debt, if material, should be:

A)recognized as an extraordinary item in the period of extinguishment.

B)amortized over the remaining original life of the extinguished issue.

C)amortized over the life of the new issue.

D)recognized in income as ordinary gains and losses or as unusual items.

A)recognized as an extraordinary item in the period of extinguishment.

B)amortized over the remaining original life of the extinguished issue.

C)amortized over the life of the new issue.

D)recognized in income as ordinary gains and losses or as unusual items.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

12

Straight-line amortization of bond premium or discount:

A)is appropriate for deep discount bonds.

B)is appropriate when the bond term is especially long.

C)Provides the same total amount of interest expense and interest revenue as the effective interest method over the life of the bonds.

D)Provides the same amounts of interest expense and interest revenue each interest period as the effective interest method.

E)Can be used as an optional method of amortization in all situations.

A)is appropriate for deep discount bonds.

B)is appropriate when the bond term is especially long.

C)Provides the same total amount of interest expense and interest revenue as the effective interest method over the life of the bonds.

D)Provides the same amounts of interest expense and interest revenue each interest period as the effective interest method.

E)Can be used as an optional method of amortization in all situations.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

13

When the interest payment dates of a bond are May 31 and November 30, and a bond issue is sold on July 1, the amount of cash received by the issuer will be:

A)Increased by accrued interest from May 31 to July 1.

B)Decreased by accrued interest from July 1 to November 30.

C)Unaffected by accrued interest.

D)Increased by accrued interest from July 1 to November 30.

E)Decreased by accrued interest from May 31 to July 1.

A)Increased by accrued interest from May 31 to July 1.

B)Decreased by accrued interest from July 1 to November 30.

C)Unaffected by accrued interest.

D)Increased by accrued interest from July 1 to November 30.

E)Decreased by accrued interest from May 31 to July 1.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

14

On November 1, 2009, WC purchased CX, 10-year, 7%, bonds with a face value of $100,000 for $96,000.The bonds are intended to be held to maturity.An additional

$2,333 was paid for the accrued interest.Interest is payable semi-annually on January 1 and July 1.The bonds mature on July 1, 2016.WC uses the straight-line method of amortization.Ignoring income taxes, the amount of interest revenue reported in WC's 2019 income statement (year-end December 31)as a result of WC's long-term bond investment in CX was:

A)$1,120

B)$1,267

C)$1,167

D)$1,067

$2,333 was paid for the accrued interest.Interest is payable semi-annually on January 1 and July 1.The bonds mature on July 1, 2016.WC uses the straight-line method of amortization.Ignoring income taxes, the amount of interest revenue reported in WC's 2019 income statement (year-end December 31)as a result of WC's long-term bond investment in CX was:

A)$1,120

B)$1,267

C)$1,167

D)$1,067

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

15

On January 1, 2014, ER signed a $120,000, 10%, three-year, note payable.The proceeds are to be used to purchase a computer and related software for the company.The lending institution advanced proceeds of $115,800 and took a mortgage on the computer.The note is payable in three equal annual instalments starting on December 31, 2014.The effective interest rate to use for this debt is (rounded to the nearest percent; do not interpolate):

A)12%.

B)13%.

C)10%.

D)11%.

A)12%.

B)13%.

C)10%.

D)11%.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

16

AB Company issued a $100,000, 10%, bond at $99.Therefore, the bond:

A)sold at a premium because the $1,000 accrued interest is added to the $100,000 face amount.

B)was sold at a premium because the stated interest rate was higher than the yield rate.

C)sold at a discount because the stated interest rate was lower than the market interest rate.

D)was sold for $100,000 less $1,000 of accrued interest.

A)sold at a premium because the $1,000 accrued interest is added to the $100,000 face amount.

B)was sold at a premium because the stated interest rate was higher than the yield rate.

C)sold at a discount because the stated interest rate was lower than the market interest rate.

D)was sold for $100,000 less $1,000 of accrued interest.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

17

On September 1, 2020, ER issued 11%, 10 year bonds dated June 1, 2020, in the face amount of $140,000, with interest payable July 1 and December 31.The bonds were sold for $140,000.How much should ER debit to cash on September 1, 2020?

A)$142,567

B)$147,700

C)$140,000

D)Cannot be determined from the information given

A)$142,567

B)$147,700

C)$140,000

D)Cannot be determined from the information given

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

18

AB sold its 10-year bond at a discount.In reporting the bonds and the related discount on a balance sheet shortly thereafter, the discount should be:

A)Deducted from the bonds payable.

B)Added to the bonds.

C)Reported as a deferred charge.

D)Recorded as expense in the period of sale.

A)Deducted from the bonds payable.

B)Added to the bonds.

C)Reported as a deferred charge.

D)Recorded as expense in the period of sale.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

19

Bond A and Bond B both have a maturity value of $1,000 and pay annual interest of 9%.The market rate of interest is also 9%.Bond A matures in 4 years and Bond B matures in 5 years.Which of the following is correct?

A)Bond A will sell for more than Bond B.

B)Both bonds sell for the same amount, $1,000.

C)Both bonds sell for more than $1,000.

D)Bond B will sell for more than Bond A.

E)There is not sufficient information to answer the question.

A)Bond A will sell for more than Bond B.

B)Both bonds sell for the same amount, $1,000.

C)Both bonds sell for more than $1,000.

D)Bond B will sell for more than Bond A.

E)There is not sufficient information to answer the question.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

20

ASPE and IFRS differ in their treatment of long-term Bonds Payable in that:

A)The straight-line method may be used under ASPE but not under IFRS.

B)ASPE ignores foreign exchanges gains and losses.

C)IFRS does not account for foreign exchange gains and losses on Bonds Payable.

D)Under IFRS, exchange gains and losses on short-term debt are recorded in the income statement immediately.

A)The straight-line method may be used under ASPE but not under IFRS.

B)ASPE ignores foreign exchanges gains and losses.

C)IFRS does not account for foreign exchange gains and losses on Bonds Payable.

D)Under IFRS, exchange gains and losses on short-term debt are recorded in the income statement immediately.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

21

The stated rate of interest is the interest rate used to determine the amount of cash interest that will be paid on the principal.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

22

The rate of interest specified on the face of the debt is called the:

A)Stated interest rate.

B)Effective interest rate.

C)Market interest rate.

D)Yield interest rate.

A)Stated interest rate.

B)Effective interest rate.

C)Market interest rate.

D)Yield interest rate.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

23

Bonds payable should be reported as a long-term liability in the balance sheet of the issuer at:

A)Current market price.

B)Issue price, excluding any accrued interest at purchase date.

C)lower-of-cost-or-market.

D)Issue price plus any unamortized bond premium or less any unamortized discount.

E)Issue price less any unamortized bond premium or plus any unamortized discount.

A)Current market price.

B)Issue price, excluding any accrued interest at purchase date.

C)lower-of-cost-or-market.

D)Issue price plus any unamortized bond premium or less any unamortized discount.

E)Issue price less any unamortized bond premium or plus any unamortized discount.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

24

KR issued bonds payable with a face amount of $200,000 and a maturity date ten years from date of issuance.If the bonds were issued at a premium, this indicated that:

A)The effective and stated rates of interest were the same.

B)The stated rate of interest exceeded the effective rate of interest.

C)The effective rate of interest exceeded the stated interest rate.

D)No necessary relationship exists between the two rates.

E)The stated interest rate and the market interest rate were the same.

A)The effective and stated rates of interest were the same.

B)The stated rate of interest exceeded the effective rate of interest.

C)The effective rate of interest exceeded the stated interest rate.

D)No necessary relationship exists between the two rates.

E)The stated interest rate and the market interest rate were the same.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

25

JMR bought 15 Z Corporation's $1,000 bonds for $15,270 total, on April 1, 2014, (five years prior to maturity).The bonds pay 8% semi-annual interest on April 1 and October 1.On December 31, 2014, the bonds had a market value of $14,950 (not a permanent decline).JMR purchased these bonds at:

A)Par plus accrued interest.

B)A premium.

C)A discount plus accrued interest.

D)Par.

E)A discount.

A)Par plus accrued interest.

B)A premium.

C)A discount plus accrued interest.

D)Par.

E)A discount.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

26

If a bond was sold at $108, the stated rate of interest was:

A)Equal to market rate.

B)Higher than market rate.

C)Not related to market rate.

D)Lower than market rate.

A)Equal to market rate.

B)Higher than market rate.

C)Not related to market rate.

D)Lower than market rate.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

27

In theory (disregarding any other marketplace variables)the proceeds from the sale of a bond will be equal to:

A)The face amount of the bond plus the present value of the interest payments made during the life of the bond discounted at the prevailing market rate of interest.

B)The present value of the principal amount due at the end of the life of the bond plus the present value of the interest payments made during the life of the bond, each discounted at the prevailing market rate of interest.

C)The present value of the principal amount due at the end of the life of the bond plus the present value of the interest payments made during the life of the bond, each discounted at the stated rate of interest.

D)The sum of the face amount of the bond and the periodic interest payments.

A)The face amount of the bond plus the present value of the interest payments made during the life of the bond discounted at the prevailing market rate of interest.

B)The present value of the principal amount due at the end of the life of the bond plus the present value of the interest payments made during the life of the bond, each discounted at the prevailing market rate of interest.

C)The present value of the principal amount due at the end of the life of the bond plus the present value of the interest payments made during the life of the bond, each discounted at the stated rate of interest.

D)The sum of the face amount of the bond and the periodic interest payments.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

28

All of the following are true with respect to sinking funds except:

A)Once the sinking fund is established, the company has no more responsibility to the debt.

B)A sinking fund is a cash fund that is restricted for retiring the debt of a company.

C)A sinking fund may be handled by a trustee or by the individual company.

D)A sinking fund may make the investment more attractive to investors.

A)Once the sinking fund is established, the company has no more responsibility to the debt.

B)A sinking fund is a cash fund that is restricted for retiring the debt of a company.

C)A sinking fund may be handled by a trustee or by the individual company.

D)A sinking fund may make the investment more attractive to investors.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

29

Which of the following is not one of the conditions that must be met to qualify as extinguishment of debt by in-substance defeasance?

A)Trust must own monetary assets that are essentially risk free.

B)There is a reasonable possibility that the debtor will be called on to make additional payments on the debt.

C)Cash inflows into the trust must approximately coincide with required cash outflows.

D)The qualifying assets must not be used for trustee fees.

A)Trust must own monetary assets that are essentially risk free.

B)There is a reasonable possibility that the debtor will be called on to make additional payments on the debt.

C)Cash inflows into the trust must approximately coincide with required cash outflows.

D)The qualifying assets must not be used for trustee fees.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

30

For bonds payable, the cash interest paid in each interest period is:

A)Not the same amount when the stated and yield interest rates are different.

B)Different depending upon the date of sale.

C)The same amount regardless of whether the bond was sold at par, a discount, or a premium.

D)Dependent on the initial amount of accrued interest.

A)Not the same amount when the stated and yield interest rates are different.

B)Different depending upon the date of sale.

C)The same amount regardless of whether the bond was sold at par, a discount, or a premium.

D)Dependent on the initial amount of accrued interest.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

31

Bonds are said to be redeemable when they can be prematurely retired at the discretion of the issuing company and retractable when they can be prematurely retired at the investor's discretion.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

32

Bonds payable (due 5 years from the balance sheet date)should be classified as follows:

A)A contingent liability.

B)A long-term liability.

C)A current liability.

D)An element of the owners' equity.

A)A contingent liability.

B)A long-term liability.

C)A current liability.

D)An element of the owners' equity.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

33

The rate of interest used to discount the future cash payments on a debt to the cash equivalent borrowed is least likely to be described by which of the following terms:

A)Prevailing interest rate.

B)Effective interest rate.

C)Stated interest rate.

D)Yield interest rate.

A)Prevailing interest rate.

B)Effective interest rate.

C)Stated interest rate.

D)Yield interest rate.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

34

$5,000 (face value)of bonds with a book value of $4,300 was retired 4 years and 9 months prior to maturity.The dollar amount (excluding interest)paid to retire the bonds was $4,700.The entry to record the retirement would include:

A)dr.bonds payable $5,000

B)cr.unusual gain $400

C)dr.bonds payable $4,700

D)cr.cash $4,300

A)dr.bonds payable $5,000

B)cr.unusual gain $400

C)dr.bonds payable $4,700

D)cr.cash $4,300

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

35

A short-term payable may be the current portion of a long-term liability, which arises when the next payment on such a debt will be made out of current assets.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

36

In-substance defeasance means that a debtor irrevocably places cash or other monetary assets in a trust fund to pay interest on an outstanding debt.In such situations, the debt is always recorded as paid when the trust fund is set up (i.e.removed from the books).

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

37

If bonds are issued initially at a discount and the straight-line method of amortization is used for the discount, interest expense in the early years will be:

A)less than if the interest method is used.

B)The same as if the interest method is used.

C)more than if the interest method is used.

D)less than the amount of the interest payments.

A)less than if the interest method is used.

B)The same as if the interest method is used.

C)more than if the interest method is used.

D)less than the amount of the interest payments.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

38

The principal amount of a debt is the cash or cash equivalent amount borrowed.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

39

Transaction costs are deducted from the carrying value of long-term financial liabilities.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

40

There are two methods for amortizing premiums and discounts on the sale of bonds.The differences between the two methods are:

A)There are no differences between the two methods.

B)Both methods charge a constant amount of interest to the financial statements each year; however, the effective interest method charges a larger total amount of interest expense over the life of the bond.

C)The effective interest method charges a different interest expense each year while the straight-line method results in a constant amount of expense each year.

D)None of these answers are correct.

A)There are no differences between the two methods.

B)Both methods charge a constant amount of interest to the financial statements each year; however, the effective interest method charges a larger total amount of interest expense over the life of the bond.

C)The effective interest method charges a different interest expense each year while the straight-line method results in a constant amount of expense each year.

D)None of these answers are correct.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

41

The cost of any equity financing is included when calculating the cost of generalized borrowings.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

42

When the market rate exceeds the stated or nominal rate, a bond's carrying value will be less than its fair value.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

43

Hedging is one method of minimizing foreign exchange risk.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

44

Assume that a company issues bonds at a discount.Under the effective interest method, the company will record progressively less interest expense with the passage of time.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

45

In-substance defeasance leads to the de-recognition of a company's long-term debt.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

46

Debt issue costs on long-term debt are expensed upon issue.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

47

The carrying value of a bond from the issuing corporation's standpoint will always move closer to its face value, regardless of whether the bond is issued at a premium or a discount.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

48

Use of the effective interest method for amortizing bond premiums and discounts is mandatory under IFRS but not under ASPE.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

49

Interest may be recognized on a note even though the note does not explicitly state an interest rate.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

50

Callable bonds are callable at the option of the investor.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

51

The amortization of a bind discount or premium over the life of a bond will be the same under both the straight line and effective interest methods.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

52

A $1,000, 6%, 10-year bond purchased as a long-term investment at an effective rate at 7%, will pay the investor $70 cash interest each year.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

53

The capitalization of borrowing costs is mandatory under both IFRS & ASPE.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

54

Borrowing costs can only be capitalized on non-financial assets.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

55

The present value of any bond payable issued between interest-payment dates will include any interest accrued since the last interest payment date.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

56

An increase in interest rates may make bond defeasance more attractive to the issuing corporation.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

57

Under the effective interest method, interest expense is calculated by multiplying the market interest rate by the carrying value of the bonds.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

58

A company issuing shares to comply with its debt covenants for cash would simultaneously decrease (improve)its debt-to-assets and debt-to equity ratios.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

59

When the maturity date of a bond issue is within one year or the operating cycle (whichever is longer)of the current balance sheet date, the bond liability should be reclassified as a current liability (assuming the payment will be made out of current assets).

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

60

A company enters into a forward exchange contract to hedge its US dollar payable which is due in 90 days.The company committed to purchase sufficient US currency to settle its liability at a rate of $1 US=$1.20 CAD US.The company's year-end falls 30 days before the settlement date.On that date, the forward rate for 30-day settlement contracts was 1 US=$1.22 CAD US.As a result of these facts the company will record a gain on its current year financial statements.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

61

JV issued $10,000, 10% bonds payable (interest payable annually), which mature at the end of six years from issue date.The effective rate of interest at issue date was 12%.The sale price of the bonds was: $ _.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

62

It is often necessary to compute the book value of a bond issue several years into its term.Rather than compute an amortization schedule for the entire term, it is possible to directly compute the net bond liability at any interest date under either the interest method or straight-line method.Assume that $100,000 of 8% bonds were issued to yield 10% on January 1, 2010, the bond date.The bonds pay interest each December 31 and are scheduled to mature in ten years.Answer the following questions without producing an amortization schedule.

(a)What is the book value of the bonds on January 1, 2016 if the firm uses the straight-line method.

(b)What is the book value of the bonds on January 1, 2016 if the firm uses the interest (effective interest)method.

(a)What is the book value of the bonds on January 1, 2016 if the firm uses the straight-line method.

(b)What is the book value of the bonds on January 1, 2016 if the firm uses the interest (effective interest)method.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

63

A firm issued a 16%, $1,000 bond issued and dated Jan.1/2000 maturing Jan.1, 2011 paying interes each June 30 and December 31, and yielding 14%.One bond is used for simplicity.

Required:

(a)Determine the price of the bond

(b)All Year 2000 entries and balance sheet presentations for the bond after each interest date in Yea

A.Show the interest method and straight-line methods in parallel fashion.

Required:

(a)Determine the price of the bond

(b)All Year 2000 entries and balance sheet presentations for the bond after each interest date in Yea

A.Show the interest method and straight-line methods in parallel fashion.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

64

On January 1, 2000, a company purchased a machine (an operational asset)with a list price of

$4,000.$2,000 was paid in cash and a three-year, noninterest-bearing note was signed.The note was for $3,000 and required payment of equal amounts of $1,000 each December 31, 2000, 2001, and 2002.The going rate of interest was 12%.Using this information, complete the following requirements.

(a)Give the entry on January 1, 2000, to record the purchase of the machine (show computations and round to the nearest dollar):

(b)Prepare the related debt amortization schedule.

(c)Give any adjusting entry related to the note payable required for 2001, assuming the accounting period ends March 31.If none is required, state the reason.

(d)Assuming that the accounting period ends March 31 and there were no reversing entries, give the entry to record the annual payment made on December 31, 2001.

$4,000.$2,000 was paid in cash and a three-year, noninterest-bearing note was signed.The note was for $3,000 and required payment of equal amounts of $1,000 each December 31, 2000, 2001, and 2002.The going rate of interest was 12%.Using this information, complete the following requirements.

(a)Give the entry on January 1, 2000, to record the purchase of the machine (show computations and round to the nearest dollar):

(b)Prepare the related debt amortization schedule.

(c)Give any adjusting entry related to the note payable required for 2001, assuming the accounting period ends March 31.If none is required, state the reason.

(d)Assuming that the accounting period ends March 31 and there were no reversing entries, give the entry to record the annual payment made on December 31, 2001.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

65

ABC Inc.borrowed funds from its bank.Details are as follows.

Four year term loan, U.S.$500,000

Funds borrowed 1 January 20X6; due 31 December 20X9 Exchange rates: Part A: Based on the above information prepare entries to record receipt of loan proceeds for January 20X6.

Part B: Based on the above information prepare entries to record the adjustment to spot rate for December 20X6.

Part C: Based on the above information prepare entries to record adjustment to spot rate December

20X7

Part D: Based on the above information prepare entries to record adjustment to spot rate December 20X8

Part E: Based on the above information prepare entries to record adjustment to spot rate December 20X9

Part F: Based on the above information prepare entries to record repayment of loan December 20X9 Part G: Based on the above information calculate the total accounting recognition of loss.

Four year term loan, U.S.$500,000

Funds borrowed 1 January 20X6; due 31 December 20X9 Exchange rates:

Part A: Based on the above information prepare entries to record receipt of loan proceeds for January 20X6.Part B: Based on the above information prepare entries to record the adjustment to spot rate for December 20X6.

Part C: Based on the above information prepare entries to record adjustment to spot rate December

20X7

Part D: Based on the above information prepare entries to record adjustment to spot rate December 20X8

Part E: Based on the above information prepare entries to record adjustment to spot rate December 20X9

Part F: Based on the above information prepare entries to record repayment of loan December 20X9 Part G: Based on the above information calculate the total accounting recognition of loss.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

66

A company wishes to finance a long-term construction project and in doing so, capitalize the related interest expense.The company requires $2 million in financing.

The company currently has the following debt and equity items on its December 31st, 2019 Balance Sheet: There are 10,000 common shares outstanding which pay an annual dividend of $5 per share.The company can borrow a maximum of $5 million on its unsecured line of credit.

The company's bank has indicated its willingness to extend an additional credit facility in the amount of $1.5 million at an annual rate of 5% as of March 31st, Year 6.These amounts remained outstanding throughout Year 6.

On March 1st, Year 6 the company borrowed $600,000.On April 1st, Year 6, and additional $1.4 million was wired to the company's account, drawn on its new credit facility.

Determine the amount of interest that the company would be able to capitalize as per IFRS for Year

The company currently has the following debt and equity items on its December 31st, 2019 Balance Sheet:

There are 10,000 common shares outstanding which pay an annual dividend of $5 per share.The company can borrow a maximum of $5 million on its unsecured line of credit.The company's bank has indicated its willingness to extend an additional credit facility in the amount of $1.5 million at an annual rate of 5% as of March 31st, Year 6.These amounts remained outstanding throughout Year 6.

On March 1st, Year 6 the company borrowed $600,000.On April 1st, Year 6, and additional $1.4 million was wired to the company's account, drawn on its new credit facility.

Determine the amount of interest that the company would be able to capitalize as per IFRS for Year

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

67

AB owes a $100,000, 8%, five-year note payable dated January 1, 2020.It is the end of year 2020, and instead of making the interest payment now due, AB has made arrangements to pay the debt and the 2020 interest payment, in four equal instalments based on the same interest rate.The first payment is to be made on January 1, 2021.The amount of the equal annual payments, rounded to the nearest dollar, is:

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

68

The management of PT authorized an issue of $120,000 bonds payable, 6% (annual interest rate), dated January 1, 2000.The bonds mature on December 31, 2015 (5 years).Interest is payable each June 30 and December 31.The bonds were sold on May 1, 2010, at an effective (yield)rate of 8%.

(a)The bonds were sold at a ________ premium; discount (check one).

(b)Give the entry for PT to record the sale of the bonds on May 1, 2010.Show computations for the issue price.

(a)The bonds were sold at a ________ premium; discount (check one).

(b)Give the entry for PT to record the sale of the bonds on May 1, 2010.Show computations for the issue price.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

69

On September 1, 2015, a company signed a $19,800, one-year, non-interest-bearing note payable and received $18,000 cash.

(a)What was the yield rate of interest? ________

(b)Give the entry required at September 1, 2015, in the accounts of the company (use the net method).

(c)Give the adjusting entry required at the end of the accounting year for the company (December 31 2015).

(d)Give the entry required on the due date, August 31, 2016, assuming no reversing entries were made.

(a)What was the yield rate of interest? ________

(b)Give the entry required at September 1, 2015, in the accounts of the company (use the net method).

(c)Give the adjusting entry required at the end of the accounting year for the company (December 31 2015).

(d)Give the entry required on the due date, August 31, 2016, assuming no reversing entries were made.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

70

On January 1, 1999, a company incurred a debt of $11,663, which is payable in four equal annual instalments of $3,600, starting on December 31, 1999.

(a)The implicit interest rate is % (rounded to the nearest percent).

(b)Give the journal entry to record the second annual payment (on December 31, 2000).

(a)The implicit interest rate is % (rounded to the nearest percent).

(b)Give the journal entry to record the second annual payment (on December 31, 2000).

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

71

In August 2005, Crown Corporation Inc., a calendar-year corporation that records adjusting entries only once per year, issued bonds with the following characteristics: Part A: Provide the entries required on 1 August 2007 under the effective interest method of amortization.

Part B: Provide the entries required on 1 August 2007 under the straight line method of amortization.

Part A: Provide the entries required on 1 August 2007 under the effective interest method of amortization.Part B: Provide the entries required on 1 August 2007 under the straight line method of amortization.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

72

On April 1, 2020, the DEF sold a $2,000,000 bond issue dated January 1, 2020, to yield 9% per annum to maturity.The bonds were to be outstanding for twenty years from January 1, 2020, and the stated rate of interest was 8%.Interest is paid each January 1.

(a)Give the entry to record the purchase of one-fourth of these bonds as a long-term investment by NOP.Assume effective interest amortization and contra/adjunct accounts.

(b)Give the December 31, 2020, adjusting and closing entries for NOP.

(a)Give the entry to record the purchase of one-fourth of these bonds as a long-term investment by NOP.Assume effective interest amortization and contra/adjunct accounts.

(b)Give the December 31, 2020, adjusting and closing entries for NOP.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

73

A firm has two bonds outstanding today, each with: (1)$1,000 face value, (2)a term of 5 years at issuance, (3)3 years remaining to maturity, and (4)10% yield rate at issuance.Bond A is a zero coupon bond; bond B pays 10% annually and just paid interest yesterday.The yield rate today on both bonds is 12%.Which bond has experienced the greatest percentage change in value since issuance?

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

74

On July 1, 2012, RC sold two of its $10,000, 9%, bonds payable at an effective interest rate of 8%.Interest is paid each June 30 and the bond matures in six years on June 30, 2018.Round all amounts to the nearest dollar.

(a)What was the amount of the premium $ ________ or discount $ ?

(b)The income statement for the accounting year ended December 31, 2012, should report interest expense of, assuming:

(1)Straight-line amortization, $ .

(2)Interest-method amortization, $ _.

(a)What was the amount of the premium $ ________ or discount $ ?

(b)The income statement for the accounting year ended December 31, 2012, should report interest expense of, assuming:

(1)Straight-line amortization, $ .

(2)Interest-method amortization, $ _.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 74 flashcards in this deck.