Deck 7: Real Estate as an Investment: Some Background Information

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

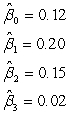

Suppose you regress a time-series of appraisal-based index periodic returns onto both contemporaneous and lagged securities market returns that do not suffer from lagging or measurement errors. That is, you perform the following regression, where rM,t is the accurate market return in period t and r*t is the appraisal-based real estate return in period t:

The resulting contemporaneous and lagged beta values are:

The resulting contemporaneous and lagged beta values are:

What is your best estimate of the true long-run beta between real estate and the securities market index?

What is your best estimate of the true long-run beta between real estate and the securities market index?

.

The resulting contemporaneous and lagged beta values are: What is your best estimate of the true long-run beta between real estate and the securities market index?.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

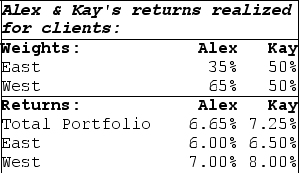

Alex and Kay are two retail property investment managers hired one year ago by two different investors. In both cases the managers were free to use their own judgment regarding geographical allocation between properties in the East versus West of the country. Kay allocated her capital equally between the two regions, while Alex placed 65% of his capital in the Western region. After one year their respective total returns were as depicted in the table below. As you can see, Kay beat Alex by 60 basis-points in her total portfolio performance for the year.

How would you attribute this 60 basis-point differential between pure allocation performance, pure selection performance, and a combined interaction effect, if you wanted to compute an unconditional performance attribution that was independent of the order of computation? Note: This is equivalent to taking Alex as the benchmark against which Kay's performance is being compared.)

How would you attribute this 60 basis-point differential between pure allocation performance, pure selection performance, and a combined interaction effect, if you wanted to compute an unconditional performance attribution that was independent of the order of computation? Note: This is equivalent to taking Alex as the benchmark against which Kay's performance is being compared.)

How would you attribute this 60 basis-point differential between pure allocation performance, pure selection performance, and a combined interaction effect, if you wanted to compute an unconditional performance attribution that was independent of the order of computation? Note: This is equivalent to taking Alex as the benchmark against which Kay's performance is being compared.) Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/25

Play

Full screen (f)

Deck 7: Real Estate as an Investment: Some Background Information

1

Consider two portfolios. Portfolio A has an expected return of 12% and volatility of 11%. Portfolio B has expected return of 9% and volatility of 6%. The interest rate on a riskfree investment is 6% which can be held either long or short). Which of these two risky portfolios is definitely not on the efficient frontier? Show your work for full credit.)

Portfolio A's Sharpe Ratio is 9%-6%)/6% = 0.5. Portfolio B's Sharpe Ratio is 12%-6%)/11% = 0.55. Thus, Portfolio A can possibly be the Sharpe-Maximizing Portfolio its Sharpe Ratio is as high as B's). Thus, Portfolio A can possibly be on the efficient frontier.

2

Regarding time-series second moments of periodic investment returns data, relevant to portfolio investment analysis:

A) An asset's own return variance measures the asset's total risk and its covariance with a portfolio measures its potential contribution to the risk in that portfolio.

B) An asset's covariance with the investor's portfolio measures the asset's total risk and its own return variance measures its potential contribution to the risk in that portfolio.

C) An asset's own return variance represents the systematic component of risk that cannot be diversified away.

D) Investor's should not care about an asset's covariance because it represents the component of risk that cannot be diversified away.

A) An asset's own return variance measures the asset's total risk and its covariance with a portfolio measures its potential contribution to the risk in that portfolio.

B) An asset's covariance with the investor's portfolio measures the asset's total risk and its own return variance measures its potential contribution to the risk in that portfolio.

C) An asset's own return variance represents the systematic component of risk that cannot be diversified away.

D) Investor's should not care about an asset's covariance because it represents the component of risk that cannot be diversified away.

A

3

According to Portfolio Theory if you do not want to bear much risk:

A) Don't invest in risky assets.

B) Buy a diversified mixture of risky assets and lever your investment by borrowing.

C) Buy a diversified mixture of risky assets and also invest in Government bonds.

D) Invest only in efficient markets.

A) Don't invest in risky assets.

B) Buy a diversified mixture of risky assets and lever your investment by borrowing.

C) Buy a diversified mixture of risky assets and also invest in Government bonds.

D) Invest only in efficient markets.

C

4

Suppose the riskfree rate is 3% and the market risk premium is 6% and a certain asset has a beta of 0.5. The asset in question is expected to produce a perpetuity of net cash flow to its investors equal to $1,000,000 per year. Suppose the CAPM is "true", and disequilibrium in asset market prices does not endure beyond i.e., "gets corrected" within) one year. Should you buy this asset if you can get it for a current price of $15,000,000? What would be the NPV of such an acquisition, and what would be the minimum expected return on a one-year investment in this asset at that price, and how much of that return if any) would be considered "super-normal" i.e., more than what is warranted by the amount of risk in the investment)?

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

5

The traditional "complaint" about applying the CAPM to real estate is:

A) Real estate's classical CAPM "beta" with respect to the stock market is nearly zero, yet real estate seems to command a significant ex ante return risk premium.

B) Real estate's classical CAPM "beta" with respect to the stock market is very high, yet real estate seems to provide a very low ex post return risk premium.

C) Real estate has a moderate "beta" and a moderate ex ante return risk premium, even though it should be a low risk asset class.

D) Real estate seems to perform differently than other small cap assets regarding the Fama-French factors.

A) Real estate's classical CAPM "beta" with respect to the stock market is nearly zero, yet real estate seems to command a significant ex ante return risk premium.

B) Real estate's classical CAPM "beta" with respect to the stock market is very high, yet real estate seems to provide a very low ex post return risk premium.

C) Real estate has a moderate "beta" and a moderate ex ante return risk premium, even though it should be a low risk asset class.

D) Real estate seems to perform differently than other small cap assets regarding the Fama-French factors.

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

6

In portfolio theory, what is the definition of an "optimal" portfolio of risky assets if we assume that no such thing as a riskless asset exists? That is, what are the characteristics that define, or the criteria that determine, such a portfolio?) Now answer this same question under the assumption that there does exist a riskless asset and state how you could identify the optimal portfolio. Be complete, defining any specialized terms you employ.

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

7

Which of the following is true about analytical tools useful in "strategic" long horizon, big picture) and "tactical" shorter horizon, more specific) investment policy analysis for portfolio management?

A) Modern portfolio theory MPT) is most useful for strategic analysis and equilibrium asset price modeling such as the CAPM) is most useful for tactical analysis.

B) Modern portfolio theory MPT) is most useful for tactical analysis and equilibrium asset price modeling such as the CAPM) is most useful for strategic analysis.

C) Both models are equally useful at both levels.

D) Neither theory is very useful at either level.

A) Modern portfolio theory MPT) is most useful for strategic analysis and equilibrium asset price modeling such as the CAPM) is most useful for tactical analysis.

B) Modern portfolio theory MPT) is most useful for tactical analysis and equilibrium asset price modeling such as the CAPM) is most useful for strategic analysis.

C) Both models are equally useful at both levels.

D) Neither theory is very useful at either level.

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

8

Suppose you regress a time-series of appraisal-based index periodic returns onto both contemporaneous and lagged securities market returns that do not suffer from lagging or measurement errors. That is, you perform the following regression, where rM,t is the accurate market return in period t and r*t is the appraisal-based real estate return in period t:

The resulting contemporaneous and lagged beta values are:

What is your best estimate of the true long-run beta between real estate and the securities market index?

.

The resulting contemporaneous and lagged beta values are: What is your best estimate of the true long-run beta between real estate and the securities market index?.

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

9

In a world where riskless borrowing or lending is possible at 6%, if the expected return to the optimal risky asset portfolio is 12%, and you want a target return of 15%, what must you do?

A) Borrow an amount equal to 25% of your wealth and put 125% of your wealth in the risky portfolio.

B) Borrow an amount equal to 50% of your wealth and put 150% of your wealth in the risky portfolio.

C) Invest half your wealth in the risky portfolio and the other half in bonds.

D) Invest 75% of your wealth in risky assets and 25% in bonds.

A) Borrow an amount equal to 25% of your wealth and put 125% of your wealth in the risky portfolio.

B) Borrow an amount equal to 50% of your wealth and put 150% of your wealth in the risky portfolio.

C) Invest half your wealth in the risky portfolio and the other half in bonds.

D) Invest 75% of your wealth in risky assets and 25% in bonds.

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

10

If the riskfree interest rate is 5%, the market price of risk is 6%, and the beta is 0.5, then, according to the classical single-factor CAPM, what is the equilibrium expected total return for investment in the asset in question?

A) 3%

B) 6%

C) 8%

D) 11%

E) 17%

A) 3%

B) 6%

C) 8%

D) 11%

E) 17%

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

11

What is the CAPM's basic treatment of idiosyncratic risk?

A) It is the most important factor in the model

B) It is irrelevant because it can be diversified away

C) It is somewhat important, but not as important as systematic risk

D) It is a primary indicator of future returns

A) It is the most important factor in the model

B) It is irrelevant because it can be diversified away

C) It is somewhat important, but not as important as systematic risk

D) It is a primary indicator of future returns

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

12

What is the main value or usefulness of real estate in the portfolio on the asset side of the balance sheet, and what is its main value or usefulness in dealing with the liability side of the balance sheet, for a typical pension fund?

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

13

If real estate has an expected return of 10% and stocks have an expected return of 15% then what would be the expected return of a portfolio consisting of 80% real estate and 20% stocks?

A) 11%

B) 12%

C) 13%

D) 14%

A) 11%

B) 12%

C) 13%

D) 14%

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

14

REITs use a metric similar to NOI for individual properties) of which they must distribute at least 90% as dividends to qualify as a REIT. What is this measure?

A) FFO

B) FAD

C) GAGR

D) CPC

A) FFO

B) FAD

C) GAGR

D) CPC

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

15

If an asset has expected return 12%, standard deviation 10%, and T-Bills return is 8%, then its "Sharpe Ratio" is:

A) 0

B) 1.200

C) 0.667

D) 0.400

A) 0

B) 1.200

C) 0.667

D) 0.400

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

16

Suppose REIT share prices have plunged 25% in the past year. Then it is reasonable to expect:

A) REIT prices will certainly rise substantially next year.

B) REIT prices will certainly fall substantially next year.

C) Unsecuritized property prices will probably rise in the upcoming year.

D) Unsecuritized property prices will probably fall in the upcoming year.

A) REIT prices will certainly rise substantially next year.

B) REIT prices will certainly fall substantially next year.

C) Unsecuritized property prices will probably rise in the upcoming year.

D) Unsecuritized property prices will probably fall in the upcoming year.

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

17

If the expected return to a risky portfolio is 12% with standard deviation 10%, and if the return to the riskless asset is 7%, then the expected return and Volatility for a portfolio consisting of 1/2) riskless bonds and 1/2) the risky portfolio would be:

A) 7% return, 10% Volatility

B) 9.5% return, 5% Volatility

C) 9.5% return, 10% Volatility

D) 10% return, 10% Volatility

E) Cannot be computed with the information given.

A) 7% return, 10% Volatility

B) 9.5% return, 5% Volatility

C) 9.5% return, 10% Volatility

D) 10% return, 10% Volatility

E) Cannot be computed with the information given.

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

18

According to Portfolio Theory all the following statements are true when there is a riskless asset except:

A) The optimal risky asset portfolio maximizes the Sharpe Measure.

B) The optimal risky asset portfolio minimizes the risk per unit of return risk premium.

C) The optimal risky asset portfolio should be bought even by investors who do not want to bear much risk.

D) The optimal risky asset portfolio should always be mixed with investments in riskless bonds.

A) The optimal risky asset portfolio maximizes the Sharpe Measure.

B) The optimal risky asset portfolio minimizes the risk per unit of return risk premium.

C) The optimal risky asset portfolio should be bought even by investors who do not want to bear much risk.

D) The optimal risky asset portfolio should always be mixed with investments in riskless bonds.

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

19

REITs don't have to pay corporate income taxes, but in return they face what major restriction?

A) They have to hold at least 50% of their assets in government bonds.

B) They have to sell any properties they develop within four years of the date of completion of construction.

C) Their directors must agree not to accept invitations to spend the night in the White House, except under a Republican administration.

D) They have to pay out 90% or more of their annual taxable income in dividends.

A) They have to hold at least 50% of their assets in government bonds.

B) They have to sell any properties they develop within four years of the date of completion of construction.

C) Their directors must agree not to accept invitations to spend the night in the White House, except under a Republican administration.

D) They have to pay out 90% or more of their annual taxable income in dividends.

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

20

If A and B are two risky assets that are less than perfectly correlated, and P is a portfolio with 1/2 its value in A and 1/2 its value in B, then:

A) Volatility of P = 1/2)Volatility of A) + 1/2)Volatility of B)

B) Volatility of P > 1/2)Volatility of A) + 1/2)Volatility of B)

C) Volatility of P < 1/2)Volatility of A) + 1/2)Volatility of B)

D) Volatility of P = 1/4)Volatility of A)*Volatility of B)

A) Volatility of P = 1/2)Volatility of A) + 1/2)Volatility of B)

B) Volatility of P > 1/2)Volatility of A) + 1/2)Volatility of B)

C) Volatility of P < 1/2)Volatility of A) + 1/2)Volatility of B)

D) Volatility of P = 1/4)Volatility of A)*Volatility of B)

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

21

Describe the implications for asset market efficiency and investment return behavior associated with:

a) Zero autocorrelation in periodic returns series;

b) Positive autocorrelation in periodic returns series;

c) Negative autocorrelation in periodic returns series.

a) Zero autocorrelation in periodic returns series;

b) Positive autocorrelation in periodic returns series;

c) Negative autocorrelation in periodic returns series.

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

22

Suppose REIT prices have risen strongly for two consecutive years. It is reasonable to expect:

A) REIT prices will certainly rise substantially next year.

B) REIT prices will certainly fall substantially next year.

C) Property market prices will probably rise in the upcoming year.

D) Property market prices will probably fall in the upcoming year.

A) REIT prices will certainly rise substantially next year.

B) REIT prices will certainly fall substantially next year.

C) Property market prices will probably rise in the upcoming year.

D) Property market prices will probably fall in the upcoming year.

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

23

What is meant by the term "umbrella partnership REIT" or "UPREIT")?

A) A REIT that invests primarily in Seattle.

B) A REIT that invests in low-risk properties, saving for a "rainy day".

C) A REIT that owns property equity directly.

D) A REIT that owns property only indirectly, through its holdings in a partnership.

A) A REIT that invests primarily in Seattle.

B) A REIT that invests in low-risk properties, saving for a "rainy day".

C) A REIT that owns property equity directly.

D) A REIT that owns property only indirectly, through its holdings in a partnership.

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

24

Alex and Kay are two retail property investment managers hired one year ago by two different investors. In both cases the managers were free to use their own judgment regarding geographical allocation between properties in the East versus West of the country. Kay allocated her capital equally between the two regions, while Alex placed 65% of his capital in the Western region. After one year their respective total returns were as depicted in the table below. As you can see, Kay beat Alex by 60 basis-points in her total portfolio performance for the year.

How would you attribute this 60 basis-point differential between pure allocation performance, pure selection performance, and a combined interaction effect, if you wanted to compute an unconditional performance attribution that was independent of the order of computation? Note: This is equivalent to taking Alex as the benchmark against which Kay's performance is being compared.)

How would you attribute this 60 basis-point differential between pure allocation performance, pure selection performance, and a combined interaction effect, if you wanted to compute an unconditional performance attribution that was independent of the order of computation? Note: This is equivalent to taking Alex as the benchmark against which Kay's performance is being compared.) Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

25

Describe the "non-normal" risk that is not rigorously modeled by modern portfolio theory.

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 25 flashcards in this deck.