Deck 4: Accounting for Governmental Operating Activities-Illustrative Transactions and Financial Statements

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

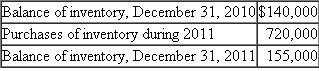

Adjusting Entries for Inventory of Supplies.The Village of Baxter uses the purchases method of accounting for its inventories of supplies in the General Fund.GASB standards, however, require that the consumption method be used for the government-wide financial statements.Because its computer system is very limited, the Village uses a periodic inventory system, adjusting inventory balances based on a physical inventory of supplies at year-end.When supplies are received during the year, the Village records expenditures and expenses in the general journals of the General Fund and governmental activities, respectively.The Village's inventory records showed the following information for the fiscal year ending December 31, 2011:

Required

Required

a.Provide the required adjusting entries at the end of 2011, assuming that the December 31, 2011, balance of Inventory of Supplies has been confirmed by physical count.Make entries in the general journals of both the General Fund (omitting subsidiary detail) and governmental activities at the government- wide level.

b.Assume that the General Fund uses the consumption method for reporting inventories of supplies rather than the purchases method.Make the required adjusting entries for the General Fund and governmental activities at the government-wide level.

Required a.Provide the required adjusting entries at the end of 2011, assuming that the December 31, 2011, balance of Inventory of Supplies has been confirmed by physical count.Make entries in the general journals of both the General Fund (omitting subsidiary detail) and governmental activities at the government- wide level.

b.Assume that the General Fund uses the consumption method for reporting inventories of supplies rather than the purchases method.Make the required adjusting entries for the General Fund and governmental activities at the government-wide level.

Question

Question

Question

Question

Question

Question

Question

Question

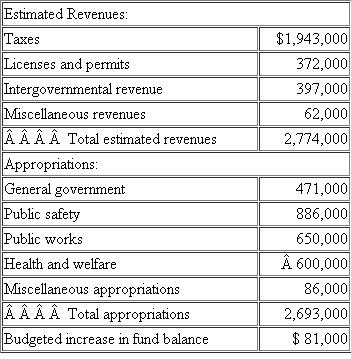

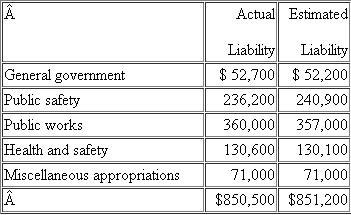

Transactions and Budgetary Comparison Schedule.The following transactions occurred during the 2011 fiscal year for the City of Fayette.For budgetary purposes, the city reports encumbrances in the Expenditures section of its budgetary comparison schedule for the General Fund but excludes expenditures chargeable to a prior year's appropriation.

1.The budget prepared for the fiscal year 2011 was as follows:

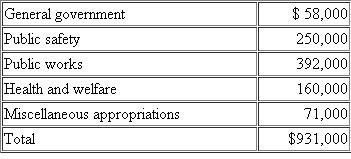

2.Encumbrances issued against the appropriations during the year were as follows:

2.Encumbrances issued against the appropriations during the year were as follows:

3.The current year's tax levy of $2,005,000 was recorded; uncollectibles were estimated as $65,000.

3.The current year's tax levy of $2,005,000 was recorded; uncollectibles were estimated as $65,000.

4.Tax collections from prior years' levies totaled $132,000; collections of the current year's levy totaled $1,459,000.

5.Personnel costs during the year were charged to the following appropriations in the amounts indicated.Encumbrances were not recorded for personnel costs.Since no liabilities currently exist for withholdings, you may ignore any FICA or federal or state income tax withholdings.( Note: Expenditures charged to Miscellaneous Appropriations should be treated as General Government expenses in the governmental activities general journal at the government-wide level.) 6.Invoices for all items ordered during the prior year were received and approved for payment in the amount of $14,470.Encumbrances had been recorded in the prior year for these items in the amount of $14,000.The amount chargeable to each year's appropriations should be charged to the Public Safety appropriation.

6.Invoices for all items ordered during the prior year were received and approved for payment in the amount of $14,470.Encumbrances had been recorded in the prior year for these items in the amount of $14,000.The amount chargeable to each year's appropriations should be charged to the Public Safety appropriation.

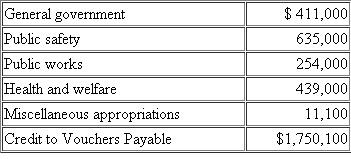

7.Invoices were received and approved for payment for items ordered in documents recorded as encumbrances in Transaction (2) of this problem.The following appropriations were affected.

8.Revenue other than taxes collected during the year consisted of licenses and permits, $373,000; intergovernmental revenue, $400,000; and $66,000 of miscellaneous revenues.For purposes of accounting for these revenues at the government-wide level, the intergovernmental revenues were operating grants and contributions for the Public Safety function.Miscellaneous revenues are not identifiable with any function and therefore are recorded as General Revenues at the government-wide level.

8.Revenue other than taxes collected during the year consisted of licenses and permits, $373,000; intergovernmental revenue, $400,000; and $66,000 of miscellaneous revenues.For purposes of accounting for these revenues at the government-wide level, the intergovernmental revenues were operating grants and contributions for the Public Safety function.Miscellaneous revenues are not identifiable with any function and therefore are recorded as General Revenues at the government-wide level.

9.Payments on Vouchers Payable totaled $2,505,000.

Additional information follows: The General Fund Fund Balance account had a credit balance of $82,900 as of December 31, 2010; no entries have been made in the Fund Balance account during 2011.

Required

a.Record the preceding transactions in general journal form for fiscal year 2011 in both the General Fund and governmental activities general journals.

b.Prepare a budgetary comparison schedule for the General Fund of the City of Fayette for the fiscal year ending December 31, 2011, as shown in Illustration 4-7.Do not prepare a government-wide statement of activities since other governmental funds would affect that statement.

1.The budget prepared for the fiscal year 2011 was as follows:

2.Encumbrances issued against the appropriations during the year were as follows: 3.The current year's tax levy of $2,005,000 was recorded; uncollectibles were estimated as $65,000.4.Tax collections from prior years' levies totaled $132,000; collections of the current year's levy totaled $1,459,000.

5.Personnel costs during the year were charged to the following appropriations in the amounts indicated.Encumbrances were not recorded for personnel costs.Since no liabilities currently exist for withholdings, you may ignore any FICA or federal or state income tax withholdings.( Note: Expenditures charged to Miscellaneous Appropriations should be treated as General Government expenses in the governmental activities general journal at the government-wide level.)

6.Invoices for all items ordered during the prior year were received and approved for payment in the amount of $14,470.Encumbrances had been recorded in the prior year for these items in the amount of $14,000.The amount chargeable to each year's appropriations should be charged to the Public Safety appropriation.7.Invoices were received and approved for payment for items ordered in documents recorded as encumbrances in Transaction (2) of this problem.The following appropriations were affected.

8.Revenue other than taxes collected during the year consisted of licenses and permits, $373,000; intergovernmental revenue, $400,000; and $66,000 of miscellaneous revenues.For purposes of accounting for these revenues at the government-wide level, the intergovernmental revenues were operating grants and contributions for the Public Safety function.Miscellaneous revenues are not identifiable with any function and therefore are recorded as General Revenues at the government-wide level.9.Payments on Vouchers Payable totaled $2,505,000.

Additional information follows: The General Fund Fund Balance account had a credit balance of $82,900 as of December 31, 2010; no entries have been made in the Fund Balance account during 2011.

Required

a.Record the preceding transactions in general journal form for fiscal year 2011 in both the General Fund and governmental activities general journals.

b.Prepare a budgetary comparison schedule for the General Fund of the City of Fayette for the fiscal year ending December 31, 2011, as shown in Illustration 4-7.Do not prepare a government-wide statement of activities since other governmental funds would affect that statement.

Question

Question

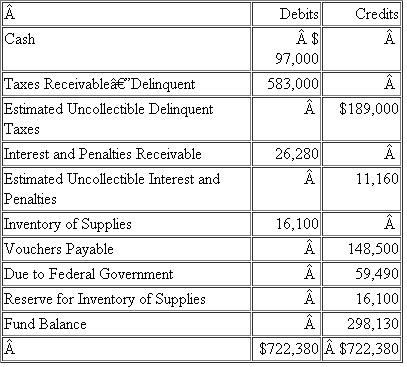

Operating Transactions, Special Topics, and Financial Statements.The City of Ashland's General Fund had the following post-closing trial balance at April 30, 2010, the end of its fiscal year:

During the year ended April 30, 2011, the following transactions, in summary form, with subsidiary ledger detail omitted, occurred:

During the year ended April 30, 2011, the following transactions, in summary form, with subsidiary ledger detail omitted, occurred:

1.The budget for FY 2011 provided for General Fund estimated revenues totaling $3,140,000 and appropriations totaling $3,100,000.

2.The city council authorized temporary borrowing of $300,000 in the form of a 120-day tax anticipation note.The loan was obtained from a local bank at a discount of 6 percent per annum (debit Expenditures for discount).

3.The property tax levy for FY 2011 was recorded.Net assessed valuation of taxable property for the year was $43,000,000, and the tax rate was $5 per $100.It was estimated that 4 percent of the levy would be uncollectible.

4.Purchase orders and contracts were issued to vendors and others in the amount of $2,059,000.

5.The County Board of Review discovered unassessed properties with a total taxable value of $500,000.The owners of these properties were charged with taxes at the city's General Fund rate of $5 per $100 assessed value.(You need not adjust the Estimated Uncollectible Current Taxes account.)6.$1,961,000 of current taxes, $383,270 of delinquent taxes, and $20,570 of interest and penalties were collected.

7.Additional interest and penalties on delinquent taxes were accrued in the amount of $38,430, of which 30 percent was estimated to be uncollectible.

8.Because of a change in state law, the city was notified that it will receive $80,000 less in intergovernmental revenues than was budgeted.

9.Total payroll during the year was $819,490.Of that amount, $62,690 was withheld for employees' FICA tax liability, $103,710 for employees' federal income tax liability, and $34,400 for state taxes; the balance was paid to employees in cash.

10.The employer's FICA tax liability was recorded for $62,690.

11.Revenues from sources other than taxes were collected in the amount of $946,700.

12.Amounts due the federal government as of April 30, 2011, and amounts due for FICA taxes, and state and federal withholding taxes during the year were vouchered.

13.Purchase orders and contracts encumbered in the amount of $1,988,040 were filled at a net cost of $1,987,570, which was vouchered.

14.Vouchers payable totaling $2,301,660 were paid after deducting a credit for purchases discount of $8,030 (credit Expenditures).

15.The tax anticipation note of $300,000 was repaid.

16.All unpaid current year's property taxes became delinquent.The balances of the current tax receivables and related uncollectibles were transferred to delinquent accounts.

17.A physical inventory of materials and supplies at April 30, 2011, showed a total of $19,100.Inventory is recorded using the purchases method in the General Fund; the consumption method is used at the government-wide level.

Required

a.Record in general journal form the effect of the above transactions on the General Fund and governmental activities for the year ended April 30, 2011.Do not record subsidiary ledger debits and credits.

b.Record in general journal form entries to close the budgetary and operating statement accounts.

c.Prepare a General Fund balance sheet as of April 30, 2011.

d.Prepare a statement of revenues, expenditures, and changes in fund balance for the year ended April 30, 2011.Do not prepare the government-wide financial statements.

During the year ended April 30, 2011, the following transactions, in summary form, with subsidiary ledger detail omitted, occurred:1.The budget for FY 2011 provided for General Fund estimated revenues totaling $3,140,000 and appropriations totaling $3,100,000.

2.The city council authorized temporary borrowing of $300,000 in the form of a 120-day tax anticipation note.The loan was obtained from a local bank at a discount of 6 percent per annum (debit Expenditures for discount).

3.The property tax levy for FY 2011 was recorded.Net assessed valuation of taxable property for the year was $43,000,000, and the tax rate was $5 per $100.It was estimated that 4 percent of the levy would be uncollectible.

4.Purchase orders and contracts were issued to vendors and others in the amount of $2,059,000.

5.The County Board of Review discovered unassessed properties with a total taxable value of $500,000.The owners of these properties were charged with taxes at the city's General Fund rate of $5 per $100 assessed value.(You need not adjust the Estimated Uncollectible Current Taxes account.)6.$1,961,000 of current taxes, $383,270 of delinquent taxes, and $20,570 of interest and penalties were collected.

7.Additional interest and penalties on delinquent taxes were accrued in the amount of $38,430, of which 30 percent was estimated to be uncollectible.

8.Because of a change in state law, the city was notified that it will receive $80,000 less in intergovernmental revenues than was budgeted.

9.Total payroll during the year was $819,490.Of that amount, $62,690 was withheld for employees' FICA tax liability, $103,710 for employees' federal income tax liability, and $34,400 for state taxes; the balance was paid to employees in cash.

10.The employer's FICA tax liability was recorded for $62,690.

11.Revenues from sources other than taxes were collected in the amount of $946,700.

12.Amounts due the federal government as of April 30, 2011, and amounts due for FICA taxes, and state and federal withholding taxes during the year were vouchered.

13.Purchase orders and contracts encumbered in the amount of $1,988,040 were filled at a net cost of $1,987,570, which was vouchered.

14.Vouchers payable totaling $2,301,660 were paid after deducting a credit for purchases discount of $8,030 (credit Expenditures).

15.The tax anticipation note of $300,000 was repaid.

16.All unpaid current year's property taxes became delinquent.The balances of the current tax receivables and related uncollectibles were transferred to delinquent accounts.

17.A physical inventory of materials and supplies at April 30, 2011, showed a total of $19,100.Inventory is recorded using the purchases method in the General Fund; the consumption method is used at the government-wide level.

Required

a.Record in general journal form the effect of the above transactions on the General Fund and governmental activities for the year ended April 30, 2011.Do not record subsidiary ledger debits and credits.

b.Record in general journal form entries to close the budgetary and operating statement accounts.

c.Prepare a General Fund balance sheet as of April 30, 2011.

d.Prepare a statement of revenues, expenditures, and changes in fund balance for the year ended April 30, 2011.Do not prepare the government-wide financial statements.

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/25

Play

Full screen (f)

Deck 4: Accounting for Governmental Operating Activities-Illustrative Transactions and Financial Statements

1

Explain why some transactions for governmental activities at the government wide level are reported differently than transactions for the General Fund.Give some examples of transactions that would be recorded in the general journals of ( a ) only the General Fund, ( b ) only governmental activities at the government-wide level, and ( c ) both.

Governmental funds:

The funds of the government focus on the flow of the current financial resources.It includes assets and liabilities.The capital assets and noncurrent liabilities will not be recorded in the governmental funds.The basis of accounting for the governmental funds is modified accrual.

Determine how the decline in value of property affects the property tax levy:

A decline in the value of the property will raise the property tax levy.Property tax levy is based on the value of the property in the market.If the value of the project declines, the government has to made change in the levy rate.

If there is no change in the levy rate even after the fall in the value of the property, it will make the tax collections fall dramatically.Thus, the government will be forced to raise the property tax levy to make the tax collection more stable.

Conclusion:

Property tax levy is a levy that the owner pays on the property.The tax levy will be labeled by the governing authority in which the property or assets is located.

The funds of the government focus on the flow of the current financial resources.It includes assets and liabilities.The capital assets and noncurrent liabilities will not be recorded in the governmental funds.The basis of accounting for the governmental funds is modified accrual.

Determine how the decline in value of property affects the property tax levy:

A decline in the value of the property will raise the property tax levy.Property tax levy is based on the value of the property in the market.If the value of the project declines, the government has to made change in the levy rate.

If there is no change in the levy rate even after the fall in the value of the property, it will make the tax collections fall dramatically.Thus, the government will be forced to raise the property tax levy to make the tax collection more stable.

Conclusion:

Property tax levy is a levy that the owner pays on the property.The tax levy will be labeled by the governing authority in which the property or assets is located.

2

Analyzing Results of Operations.Using either a city's own Web site or the GASBS 34 link of the GASB's Web site, download either the city's entire comprehensive annual financial report (CAFR) or, if possible, just the portion of the CAFR that contains the basic financial statements.Print a copy of the government-wide statement of activities and a copy of the statement of revenues, expenditures, and changes in fund balances-governmental funds, along with the reconciliation between these two statements, and respond to the requirements below.

The city manager is concerned that some recently elected members of the city council will get a mixed message since the change in net assets reported for governmental activities is noticeably different from the change in fund balances reported on the governmental funds statement of revenues, expenditures, and changes in fund balances.The city manager has requested that you, in your role as finance director, explain to the city council in clear, easy-to-understand terms for which purposes each operating statement is intended and how and why the operating results differ.

Required

a.Examine the two operating statements in detail, paying particular attention to the lines on which changes in net assets and changes in fund balances are reported and develop a list of reasons why the two numbers are not the same.

b.Prepare a succinct and understandable explanation of the results of operations of this government from the perspective of each operating statement, in terms that a non-accountant council member would be able to understand.

The city manager is concerned that some recently elected members of the city council will get a mixed message since the change in net assets reported for governmental activities is noticeably different from the change in fund balances reported on the governmental funds statement of revenues, expenditures, and changes in fund balances.The city manager has requested that you, in your role as finance director, explain to the city council in clear, easy-to-understand terms for which purposes each operating statement is intended and how and why the operating results differ.

Required

a.Examine the two operating statements in detail, paying particular attention to the lines on which changes in net assets and changes in fund balances are reported and develop a list of reasons why the two numbers are not the same.

b.Prepare a succinct and understandable explanation of the results of operations of this government from the perspective of each operating statement, in terms that a non-accountant council member would be able to understand.

a.Students will examine different governments, but in all cases there should be a significant difference between the change in the total fund balances of governmental funds and the change in net assets of governmental activities. A simple evaluation of a positive change or increase is that it represents "good news" while a decrease in fund balances or net assets represents "bad news." This initial assessment should always be qualified until further analysis is done to determine whether the government had planned for that outcome. Changes in net assets at the government-wide level will include depreciation of general capital assets and amortization of bond discounts and premiums. Changes in the fund balances of governmental funds will include new acquisitions of capital assets that have been recorded as expenditures for the current year (as well as sales of capital assets), and proceeds of bond issuances. In addition, the net revenue of certain internal service fund (ISF) activity will be reflected in governmental activities net assets, but not governmental funds fund balances, as the ISF is a proprietary fund.

b.Encourage students to examine the Reconciliation of the Statement of Revenues, Expenditures, and Changes in Fund Balances-Governmental Funds to the Statement of Activities (see Illustration A1-6). They should recast the information in this statement in "plain English" to be included in their memo. The nature of the story to be told is that the government is accountable for spending within its legal authorization as presented in the budget, and governmental fund financial statements are designed to show this fiscal accountability. On the other hand, government managers are also accountable for the operations of the government with a view toward the government as a whole and its long-term financial condition, and the government-wide statements are designed to meet this need.

b.Encourage students to examine the Reconciliation of the Statement of Revenues, Expenditures, and Changes in Fund Balances-Governmental Funds to the Statement of Activities (see Illustration A1-6). They should recast the information in this statement in "plain English" to be included in their memo. The nature of the story to be told is that the government is accountable for spending within its legal authorization as presented in the budget, and governmental fund financial statements are designed to show this fiscal accountability. On the other hand, government managers are also accountable for the operations of the government with a view toward the government as a whole and its long-term financial condition, and the government-wide statements are designed to meet this need.

3

Examine the CAFR.Utilizing the comprehensive annual financial report obtained for Exercise 1-1, follow these instructions.

a.Governmental Activities, Government-wide Level.Answer the following questions.(1) Are governmental activities reported in a separate column from business-type activities in the two government-wide financial statements (2) Are assets and liabilities reported either in the relative order of their liquidity or on a classified basis on the statement of net assets (3) Is information on expenses for governmental activities presented at least at the functional level of detail (4) Are program revenues segregated into ( a ) charges for services, ( b ) operating grants and contributions, and ( c ) capital grants and contributions on the statement of activities

b.General Fund.Answer the following questions.(1) What statements and schedules pertaining to the General Fund are presented (2) In what respects (headings, arrangements, items included, etc.) do they seem similar to the year-end statements illustrated or described in the text (3) In what respects do they differ (4) What purpose is each statement and schedule intended to serve (5) How well, in your reasoned opinion, does each statement and schedule accomplish its intended purpose (6) Are any noncurrent or nonliquid assets included in the General Fund balance sheet If so, are they offset by "Reserve" accounts in the Fund Equity section (7) Are any noncurrent liabilities included in the General Fund balance sheet If so, describe them.(8) Are revenue classifications sufficiently detailed to be meaningful (9) Has the government refrained from reporting expenses rather than expenditures

c.Special Revenue Funds.Answer the following questions.(1) What statements and schedules pertaining to the special revenue funds are presented (2) Are these only combining statements, or are there also statements for individual special revenue funds (3) Are expenditures classified by character (i.e., current, intergovernmental, capital outlay, and debt service) (4) Are current expenditures further categorized at least by function

d.Examine Again.Refer to part b.Answer each question again, now from the perspective of the special revenue funds.Review your answers to Exercises 1-1, 2-1, and 3-1 in light of your study of Chapter 4.If you now believe your earlier answers were not entirely correct, change them to conform with your present understanding of GASB financial reporting standards.

a.Governmental Activities, Government-wide Level.Answer the following questions.(1) Are governmental activities reported in a separate column from business-type activities in the two government-wide financial statements (2) Are assets and liabilities reported either in the relative order of their liquidity or on a classified basis on the statement of net assets (3) Is information on expenses for governmental activities presented at least at the functional level of detail (4) Are program revenues segregated into ( a ) charges for services, ( b ) operating grants and contributions, and ( c ) capital grants and contributions on the statement of activities

b.General Fund.Answer the following questions.(1) What statements and schedules pertaining to the General Fund are presented (2) In what respects (headings, arrangements, items included, etc.) do they seem similar to the year-end statements illustrated or described in the text (3) In what respects do they differ (4) What purpose is each statement and schedule intended to serve (5) How well, in your reasoned opinion, does each statement and schedule accomplish its intended purpose (6) Are any noncurrent or nonliquid assets included in the General Fund balance sheet If so, are they offset by "Reserve" accounts in the Fund Equity section (7) Are any noncurrent liabilities included in the General Fund balance sheet If so, describe them.(8) Are revenue classifications sufficiently detailed to be meaningful (9) Has the government refrained from reporting expenses rather than expenditures

c.Special Revenue Funds.Answer the following questions.(1) What statements and schedules pertaining to the special revenue funds are presented (2) Are these only combining statements, or are there also statements for individual special revenue funds (3) Are expenditures classified by character (i.e., current, intergovernmental, capital outlay, and debt service) (4) Are current expenditures further categorized at least by function

d.Examine Again.Refer to part b.Answer each question again, now from the perspective of the special revenue funds.Review your answers to Exercises 1-1, 2-1, and 3-1 in light of your study of Chapter 4.If you now believe your earlier answers were not entirely correct, change them to conform with your present understanding of GASB financial reporting standards.

The answers will differ from student to student, since each has a different annual report. The instructor may wish to have copies made of good examples of statements, charts, graphs, informative schedules, and tables.Some class discussion of the different presentations found by students is worthwhile. As a suggestion, you may ask students to carefully review the government-wide statement of net assets and statement of activities and comment on the usefulness of those two statements.

4

In what ways does the government-wide statement of net assets differ from the balance sheet for governmental funds

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

5

Policy Issues Relating to Property Taxes.Property owners in Trevor City were shocked when they recently received notice that assessed valuations on their homes had increased by an average 35 percent, based on a triennial reassessment by the County Board of Equalization.Like many homeowners in the city, you have often complained about the high property taxes in Trevor City, and now you are outraged that your taxes will apparently increase another 35 percent in the coming year.

After stewing all weekend about the unreasonable increase in assessed valuation, you decide to visit the county tax assessor on Monday to find out why your assessed valuation has increased so rapidly.When you finally reach the counter, the customer service representative explains that reassessment considers such factors as actual property sales in particular neighborhoods, trends in building costs, and home improvements.He also explains that heavy demand for both new and previously owned homes has skyrocketed in the Trevor City area in recent years.Moreover, you learn that the reassessment on your home is only average, with some being higher and some lower.Although this information calms you down somewhat, you ask: "But how can we possibly afford a 35 percent increase in our taxes next year " The representative explains that actual tax rates are set by each jurisdiction having taxing authority over particular properties (in your case, these are the county government, Trevor City, the Trevor City Independent School District, the Trevor City Library, and the Trevor City Redevelopment Authority), so he cannot say how much property taxes will actually increase.

Required

a.When you have regained your composure, prepare a brief written analysis objectively evaluating the probability that your property taxes will actually increase by 35 percent next year.In doing so, consider factors that you feel may mitigate against such a large increase.What would have to happen to the tax rates for your taxes to remain at their current level or increase only slightly

b.Put yourself in the position of the city manager of Trevor City.Does she view the rapid growth in property values as a windfall for the city What are the potential economic and political risks involved with a hot real estate market such as Trevor City is experiencing

After stewing all weekend about the unreasonable increase in assessed valuation, you decide to visit the county tax assessor on Monday to find out why your assessed valuation has increased so rapidly.When you finally reach the counter, the customer service representative explains that reassessment considers such factors as actual property sales in particular neighborhoods, trends in building costs, and home improvements.He also explains that heavy demand for both new and previously owned homes has skyrocketed in the Trevor City area in recent years.Moreover, you learn that the reassessment on your home is only average, with some being higher and some lower.Although this information calms you down somewhat, you ask: "But how can we possibly afford a 35 percent increase in our taxes next year " The representative explains that actual tax rates are set by each jurisdiction having taxing authority over particular properties (in your case, these are the county government, Trevor City, the Trevor City Independent School District, the Trevor City Library, and the Trevor City Redevelopment Authority), so he cannot say how much property taxes will actually increase.

Required

a.When you have regained your composure, prepare a brief written analysis objectively evaluating the probability that your property taxes will actually increase by 35 percent next year.In doing so, consider factors that you feel may mitigate against such a large increase.What would have to happen to the tax rates for your taxes to remain at their current level or increase only slightly

b.Put yourself in the position of the city manager of Trevor City.Does she view the rapid growth in property values as a windfall for the city What are the potential economic and political risks involved with a hot real estate market such as Trevor City is experiencing

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

6

Multiple Choice.Choose the best answer. 1.When equipment was purchased with General Fund resources, which of the following accounts would have been debited in the General Fund

A)Expenditures.

B)Equipment.

C)Encumbrances.

D)No entry should be made in the General Fund.

2)The City of Marshall uses the purchases method for recording its inventory of supplies in the General Fund.Rather than using a perpetual inventory system, inventories are updated at year-end based on a physical count.Physical inventories were $85,000 and $75,000 at December 31, 2010 and 2011, respectively.The adjusting journal entry on December 31, 2011, will include a:

A)Debit to Inventory of Supplies for $75,000.

B)Debit to Expenditures for $10,000.

C)Credit to Inventory of Supplies for $10,000.

D)Credit to Expenditures for $10,000.

3)Goods for which a purchase order had been placed at an estimated cost of $1,000 were received at an actual cost of $985.The journal entry in the General Fund to record the receipt of the goods will include a:

A)Debit to Reserve for Encumbrances for $1,000.

B)Credit to Vouchers Payable for $985.

C)Debit to Expenditures for $985.

D)All of the above are correct.

4)The City of Fenton levied $3,000,000 of General Fund property taxes for the fiscal year ending December 31, 2011, with an estimated uncollectible amount of $200,000.During 2011 and January and February of 2012, $2,500,000 of the levy is expected to be collected; however, $300,000 of the levy is not expected to be collected until after February 2012.The amount of property tax revenues to be recognized in FY 2011 is:

A)$3,000,000 in governmental activities at the government-wide level and $2,800,000 in the General Fund.

B)$2,800,000 in governmental activities at the government-wide level and $2,500,000 in the General Fund.

C)$2,500,000 in governmental activities at the government-wide level and $2,800,000 in the General Fund.

D)$2,500,000 in governmental activities at the government-wide level and $2,500,000 in the General Fund.

5)Which of the following items would be reported as a program revenue on the government-wide statement of activities

A)Sales taxes.

B)Interest and penalties on taxes.

C)Unrestricted federal grants.

D)Fines and forfeits.

6)Internal exchange transactions in which a governmental fund receives goods or services from an enterprise fund are:

A)Reported as expenditures by the governmental fund and as revenues by the enterprise fund.

B)Reported as interfund transfers out by the governmental fund and as interfund transfers in by the internal service fund.

C)Reported as expenses by governmental funds and as revenues by the enterprise fund.

D)Either a or b, depending on local policy.

7)Which of the following revenues would be classified as an imposed nonex-change revenue

A)Sales taxes.

B)Federal and state grants.

C)Property taxes.

D)Income taxes.

8)Which of the following transactions is reported on the government-wide financial statements

A)An interfund loan from the General Fund to a special revenue fund.

B)Equipment used by the General Fund is transferred to an internal service fund that predominantly serves departments that are engaged in governmental activities.

C)The City Airport Fund, an enterprise fund, transfers a portion of boarding fees charged to passengers to the General Fund.

D)An interfund transfer is made between the General Fund and the Debt Service Fund.

9)A special revenue fund that administers a program funded by a reimbursement- type (expenditure-driven) federal grant should recognize revenue:

A)When notified of grant approval.

B)When qualifying expenditures have been made.

C)When cash is received.

D)When the special revenue fund has paid for all of the services it has provided.

10)A city received a $1,000,000 cash contribution under a trust agreement in which investment earnings (but not the principal amount) can be used to maintain the city cemetery.This contribution should be recorded in a (an):

A)Fiduciary fund.

B)Permanent fund.

C)Special revenue fund.

D)Internal service fund.

A)Expenditures.

B)Equipment.

C)Encumbrances.

D)No entry should be made in the General Fund.

2)The City of Marshall uses the purchases method for recording its inventory of supplies in the General Fund.Rather than using a perpetual inventory system, inventories are updated at year-end based on a physical count.Physical inventories were $85,000 and $75,000 at December 31, 2010 and 2011, respectively.The adjusting journal entry on December 31, 2011, will include a:

A)Debit to Inventory of Supplies for $75,000.

B)Debit to Expenditures for $10,000.

C)Credit to Inventory of Supplies for $10,000.

D)Credit to Expenditures for $10,000.

3)Goods for which a purchase order had been placed at an estimated cost of $1,000 were received at an actual cost of $985.The journal entry in the General Fund to record the receipt of the goods will include a:

A)Debit to Reserve for Encumbrances for $1,000.

B)Credit to Vouchers Payable for $985.

C)Debit to Expenditures for $985.

D)All of the above are correct.

4)The City of Fenton levied $3,000,000 of General Fund property taxes for the fiscal year ending December 31, 2011, with an estimated uncollectible amount of $200,000.During 2011 and January and February of 2012, $2,500,000 of the levy is expected to be collected; however, $300,000 of the levy is not expected to be collected until after February 2012.The amount of property tax revenues to be recognized in FY 2011 is:

A)$3,000,000 in governmental activities at the government-wide level and $2,800,000 in the General Fund.

B)$2,800,000 in governmental activities at the government-wide level and $2,500,000 in the General Fund.

C)$2,500,000 in governmental activities at the government-wide level and $2,800,000 in the General Fund.

D)$2,500,000 in governmental activities at the government-wide level and $2,500,000 in the General Fund.

5)Which of the following items would be reported as a program revenue on the government-wide statement of activities

A)Sales taxes.

B)Interest and penalties on taxes.

C)Unrestricted federal grants.

D)Fines and forfeits.

6)Internal exchange transactions in which a governmental fund receives goods or services from an enterprise fund are:

A)Reported as expenditures by the governmental fund and as revenues by the enterprise fund.

B)Reported as interfund transfers out by the governmental fund and as interfund transfers in by the internal service fund.

C)Reported as expenses by governmental funds and as revenues by the enterprise fund.

D)Either a or b, depending on local policy.

7)Which of the following revenues would be classified as an imposed nonex-change revenue

A)Sales taxes.

B)Federal and state grants.

C)Property taxes.

D)Income taxes.

8)Which of the following transactions is reported on the government-wide financial statements

A)An interfund loan from the General Fund to a special revenue fund.

B)Equipment used by the General Fund is transferred to an internal service fund that predominantly serves departments that are engaged in governmental activities.

C)The City Airport Fund, an enterprise fund, transfers a portion of boarding fees charged to passengers to the General Fund.

D)An interfund transfer is made between the General Fund and the Debt Service Fund.

9)A special revenue fund that administers a program funded by a reimbursement- type (expenditure-driven) federal grant should recognize revenue:

A)When notified of grant approval.

B)When qualifying expenditures have been made.

C)When cash is received.

D)When the special revenue fund has paid for all of the services it has provided.

10)A city received a $1,000,000 cash contribution under a trust agreement in which investment earnings (but not the principal amount) can be used to maintain the city cemetery.This contribution should be recorded in a (an):

A)Fiduciary fund.

B)Permanent fund.

C)Special revenue fund.

D)Internal service fund.

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

7

How does the use of encumbrance procedures improve budgetary control over expenditures

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

8

Reporting Internal Service Fund Financial Information at the Government - wide Level.During the current fiscal year, the City of Manchester created a Printing and Sign Fund (an internal service fund) to provide custom printing and signage for city departments, predominantly those financed by the General Fund.As this is the city's first internal service fund, finance officials are uncertain how to account for the activities of the Printing and Sign Fund at the government-wide level.After much discussion, they have approached you, the audit manager, with the following questions:

1.In governmental activities at the government-wide level, should expenses for printing and signage within the various functions be the amount billed to departments or the Printing and Sign Fund's cost to provide the printing and signage service Please explain.

2.What about the Printing and Sign Fund's operating revenues from billings to departments Should these revenues be reported as program revenues, specifically, as charges for services of the functions receiving the services Why or why not

3.The Printing and Sign Fund obtains about 10 percent of its revenues from the City Electric, Sewage, and Water Fund, an enterprise fund.Should the financial information related to these transactions be reported in the Business-type Activities column of the government-wide financial statements, rather than the Governmental Activities column Please explain in detail.

Required

a.Evaluate these questions and provide the city's finance director with a written response to each question.

b.How would your response to question 3 differ if the Printing and Sign Fund provided 60 percent of its total services to the enterprise fund

1.In governmental activities at the government-wide level, should expenses for printing and signage within the various functions be the amount billed to departments or the Printing and Sign Fund's cost to provide the printing and signage service Please explain.

2.What about the Printing and Sign Fund's operating revenues from billings to departments Should these revenues be reported as program revenues, specifically, as charges for services of the functions receiving the services Why or why not

3.The Printing and Sign Fund obtains about 10 percent of its revenues from the City Electric, Sewage, and Water Fund, an enterprise fund.Should the financial information related to these transactions be reported in the Business-type Activities column of the government-wide financial statements, rather than the Governmental Activities column Please explain in detail.

Required

a.Evaluate these questions and provide the city's finance director with a written response to each question.

b.How would your response to question 3 differ if the Printing and Sign Fund provided 60 percent of its total services to the enterprise fund

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

9

Calculating Required Tax Anticipation Financing and Recording Issuance of Tax Anticipation Notes.The City of Perrin collects its annual property taxes late in its fiscal year.Consequently, each year it must finance part of its operating budget using tax anticipation notes.The notes are repaid upon collection of property taxes.On April 1, 2011, the City estimated that it will require $2,470,000 to finance governmental activities for the remainder of the 2011 fiscal year.On that date, it had $740,000 of cash on hand and $830,000 of current liabilities.Collections for the remainder of FY 2011 from revenues other than current property taxes and from delinquent property taxes, including interest and penalties, were estimated at $1,100,000.

Required

a.Calculate the estimated amount of tax anticipation financing that will be required for the remainder of FY 2011.Show work in good form.

b.Assume that on April 2, 2011, the City of Perrin borrowed the amount calculated in part a by signing tax anticipation notes bearing 5 percent per annum to a local bank.Record the issuance of the tax anticipation notes in the general journals of the General Fund and governmental activities at the government-wide level.

c.By October 1, 2011, the City had collected a sufficient amount of current property taxes to repay the tax anticipation notes with interest.Record the repayment of the tax anticipation notes and interest in the general journals of the General Fund and governmental activities at the government-wide level.

Required

a.Calculate the estimated amount of tax anticipation financing that will be required for the remainder of FY 2011.Show work in good form.

b.Assume that on April 2, 2011, the City of Perrin borrowed the amount calculated in part a by signing tax anticipation notes bearing 5 percent per annum to a local bank.Record the issuance of the tax anticipation notes in the general journals of the General Fund and governmental activities at the government-wide level.

c.By October 1, 2011, the City had collected a sufficient amount of current property taxes to repay the tax anticipation notes with interest.Record the repayment of the tax anticipation notes and interest in the general journals of the General Fund and governmental activities at the government-wide level.

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

10

If the General Fund of a certain city needs $6,720,000 of revenue from property taxes to finance estimated expenditures of the next fiscal year and historical experience indicates that 4 percent of the gross levy will not be collected, what should be the amount of the gross levy for property taxes Show all computations in good form.

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

11

Reporting Multipurpose Grant Transactions in the Funds and Government- wide Financial Statements of Local Government Recipients.In this case, local governments receive reimbursements from the state government's Department of Social Services Teen Assistance Program for expenditures incurred in conducting an array of locally administered programs that benefit troubled teens.The state program provides reimbursement up to a maximum amount based on grant applications submitted annually by each local government and provides notification of the amounts approved prior to the grant year.Each local government determines which kinds of teen programs and what mix of services are most appropriate for its community.Reimbursements are made only after services have been provided and documented claims for reimbursements have been submitted to the state.GASB standards relevant to this grant state:

Multipurpose grants (those that provide financing from more than one program) should be reported as program revenue if the amounts restricted to each program are specifically identified in the grant award or grant agreement.Multipurpose grants that do not provide for specific identification of the programs and amounts should be reported as general revenues.

Required

a.In which fiscal year(s) should the grant be reported on the fund and government- wide financial statements of the local governments receiving the grant reimbursements Please explain your answer.

b.How should the grant be reported on the fund and government-wide financial statements Please explain your answer.

Multipurpose grants (those that provide financing from more than one program) should be reported as program revenue if the amounts restricted to each program are specifically identified in the grant award or grant agreement.Multipurpose grants that do not provide for specific identification of the programs and amounts should be reported as general revenues.

Required

a.In which fiscal year(s) should the grant be reported on the fund and government- wide financial statements of the local governments receiving the grant reimbursements Please explain your answer.

b.How should the grant be reported on the fund and government-wide financial statements Please explain your answer.

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

12

Property Tax Calculations and Journal Entries.The Village of Darby's budget calls for property tax revenues for the fiscal year ending December 31, 2011, of $2,660,000.Village records indicate that, on average, 2 percent of taxes levied are not collected.The county tax assessor has assessed the value of taxable property located in the village at $135,714,300.

Required

a.Calculate to the nearest penny what tax rate per $100 of assessed valuation is required to generate a tax levy that will produce the required amount of revenue for the year.

b.Record the tax levy for 2011 in the General Fund.(Ignore subsidiary detail and entries at the government-wide level.)c.By December 31, 2011, $2,540,000 of the current property tax levy had been collected.Record the amounts collected and reclassify the uncollected amount as delinquent.Interest and penalties of 6 percent were immediately due on the delinquent taxes, but the finance director estimates that 10 percent will not be collectible.Record the interest and penalties receivable.(Round all amounts to the nearest dollar.)

Required

a.Calculate to the nearest penny what tax rate per $100 of assessed valuation is required to generate a tax levy that will produce the required amount of revenue for the year.

b.Record the tax levy for 2011 in the General Fund.(Ignore subsidiary detail and entries at the government-wide level.)c.By December 31, 2011, $2,540,000 of the current property tax levy had been collected.Record the amounts collected and reclassify the uncollected amount as delinquent.Interest and penalties of 6 percent were immediately due on the delinquent taxes, but the finance director estimates that 10 percent will not be collectible.Record the interest and penalties receivable.(Round all amounts to the nearest dollar.)

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

13

"Actual revenues and expenditures reported on a budget and actual comparison schedule should be prepared on the same basis as budgeted revenues and expenditures, even if a cash basis is used." Do you agree with this statement Why or why not

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

14

Adjusting Entries for Inventory of Supplies.The Village of Baxter uses the purchases method of accounting for its inventories of supplies in the General Fund.GASB standards, however, require that the consumption method be used for the government-wide financial statements.Because its computer system is very limited, the Village uses a periodic inventory system, adjusting inventory balances based on a physical inventory of supplies at year-end.When supplies are received during the year, the Village records expenditures and expenses in the general journals of the General Fund and governmental activities, respectively.The Village's inventory records showed the following information for the fiscal year ending December 31, 2011:

Required

a.Provide the required adjusting entries at the end of 2011, assuming that the December 31, 2011, balance of Inventory of Supplies has been confirmed by physical count.Make entries in the general journals of both the General Fund (omitting subsidiary detail) and governmental activities at the government- wide level.

b.Assume that the General Fund uses the consumption method for reporting inventories of supplies rather than the purchases method.Make the required adjusting entries for the General Fund and governmental activities at the government-wide level.

Required a.Provide the required adjusting entries at the end of 2011, assuming that the December 31, 2011, balance of Inventory of Supplies has been confirmed by physical count.Make entries in the general journals of both the General Fund (omitting subsidiary detail) and governmental activities at the government- wide level.

b.Assume that the General Fund uses the consumption method for reporting inventories of supplies rather than the purchases method.Make the required adjusting entries for the General Fund and governmental activities at the government-wide level.

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

15

Explain why expenses reported on the government-wide statement of activities for supplies used in conducting governmental activities may differ in amounts from expenditures for the same supplies reported on the statement of revenues, expenditures, and changes in fund balances for governmental funds.

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

16

Special Revenue Fund, Voluntary Nonexchange Transactions.The City of Eldon applied for a competitive grant from the state government for park improvements such as upgrading hiking trails and bike paths.On May 1, 2011, the City was notified that it had been awarded a grant of $200,000 for the program, to be received in two installments on July 1, 2011, and July 1, 2012.The grant stipulates that $100,000 is for use in each of the city's fiscal years ending June 30, 2012, and June 30, 2013.Any amounts not expended during FY 2012 can be carried over for use in FY 2013.During FY 2012, the city expended $90,000 for park improvements from grant resources.

Required

For the special revenue fund, provide the appropriate journal entries, if any, that would be made for the following:

1.May 1, 2011, notification of grant approval.

2.July 1, 2011, receipt of first installment of the grant.

3.During FY 2011 to record expenditures under the grant.

4.July 1, 2012.

Required

For the special revenue fund, provide the appropriate journal entries, if any, that would be made for the following:

1.May 1, 2011, notification of grant approval.

2.July 1, 2011, receipt of first installment of the grant.

3.During FY 2011 to record expenditures under the grant.

4.July 1, 2012.

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

17

Explain the primary differences between ad valorem taxes, such as property taxes, and other taxes that generate derived tax revenues, such as sales and income taxes.How does accounting differ between these classes of taxes

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

18

Closing Journal Entries.At the end of a fiscal year, budgetary and operating statement control accounts in the general ledger of the General Fund of Dade City had the following balances: Appropriations, $6,224,000; Estimated Other Financing Uses, $2,776,000; Estimated Revenues, $7,997,000; Encumbrances, $0; Expenditures, $6,192,000; Other Financing Uses, $2,770,000; and Revenues, $7,980,000.Appropriations included the authorization to order a certain item at a cost not to exceed $65,000; this was not ordered during the year because it will not be available until late in the following year.

Required

Show in general journal form the entry needed to close all of the preceding accounts that should be closed as of the end of the fiscal year.

Required

Show in general journal form the entry needed to close all of the preceding accounts that should be closed as of the end of the fiscal year.

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

19

If interim financial reporting to external parties is not required, why should a government bother to prepare interim financial statements and schedules Give some examples of interim financial statements or schedules that a government should consider for internal management use.

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

20

Interfund and Interactivity Transactions.The following transactions affected various funds and activities of the City of Atwater.

1.The Fire Department, a governmental activity, purchased $100,000 of water from the Water Utility Fund, a business-type activity.

2.The Municipal Golf Course, an enterprise fund, reimbursed the General Fund $1,000 for office supplies that the General Fund had purchased on its behalf and that were used in the course of the fiscal year.

3.The General Fund made a long-term loan in the amount of $50,000 to the Central Stores Fund, an internal service fund that services city departments.

4.The General Fund paid its annual contribution of $80,000 to the debt service fund for interest and principal on general obligation bonds due during the year.

5.The $5,000 balance in the capital projects fund at the completion of construction of a new City Hall was transferred to the General Fund.

Required

a.Make the required journal entries in the general journal of the General Fund and any other fund(s) affected by the interfund transactions described.Also make entries in the governmental activities journal for any transaction(s) affecting a governmental fund.Do not make entries in the subsidiary ledgers.

b.Why is it unnecessary to make entries in a business-type activities journal for any transaction(s) affecting proprietary funds Are internal service funds any different

1.The Fire Department, a governmental activity, purchased $100,000 of water from the Water Utility Fund, a business-type activity.

2.The Municipal Golf Course, an enterprise fund, reimbursed the General Fund $1,000 for office supplies that the General Fund had purchased on its behalf and that were used in the course of the fiscal year.

3.The General Fund made a long-term loan in the amount of $50,000 to the Central Stores Fund, an internal service fund that services city departments.

4.The General Fund paid its annual contribution of $80,000 to the debt service fund for interest and principal on general obligation bonds due during the year.

5.The $5,000 balance in the capital projects fund at the completion of construction of a new City Hall was transferred to the General Fund.

Required

a.Make the required journal entries in the general journal of the General Fund and any other fund(s) affected by the interfund transactions described.Also make entries in the governmental activities journal for any transaction(s) affecting a governmental fund.Do not make entries in the subsidiary ledgers.

b.Why is it unnecessary to make entries in a business-type activities journal for any transaction(s) affecting proprietary funds Are internal service funds any different

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

21

How does a permanent fund differ from public-purpose trusts that are reported in special revenue funds How does it differ from private-purpose trust funds

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

22

Transactions and Budgetary Comparison Schedule.The following transactions occurred during the 2011 fiscal year for the City of Fayette.For budgetary purposes, the city reports encumbrances in the Expenditures section of its budgetary comparison schedule for the General Fund but excludes expenditures chargeable to a prior year's appropriation.

1.The budget prepared for the fiscal year 2011 was as follows:

2.Encumbrances issued against the appropriations during the year were as follows:

3.The current year's tax levy of $2,005,000 was recorded; uncollectibles were estimated as $65,000.

4.Tax collections from prior years' levies totaled $132,000; collections of the current year's levy totaled $1,459,000.

5.Personnel costs during the year were charged to the following appropriations in the amounts indicated.Encumbrances were not recorded for personnel costs.Since no liabilities currently exist for withholdings, you may ignore any FICA or federal or state income tax withholdings.( Note: Expenditures charged to Miscellaneous Appropriations should be treated as General Government expenses in the governmental activities general journal at the government-wide level.) 6.Invoices for all items ordered during the prior year were received and approved for payment in the amount of $14,470.Encumbrances had been recorded in the prior year for these items in the amount of $14,000.The amount chargeable to each year's appropriations should be charged to the Public Safety appropriation.

7.Invoices were received and approved for payment for items ordered in documents recorded as encumbrances in Transaction (2) of this problem.The following appropriations were affected.

8.Revenue other than taxes collected during the year consisted of licenses and permits, $373,000; intergovernmental revenue, $400,000; and $66,000 of miscellaneous revenues.For purposes of accounting for these revenues at the government-wide level, the intergovernmental revenues were operating grants and contributions for the Public Safety function.Miscellaneous revenues are not identifiable with any function and therefore are recorded as General Revenues at the government-wide level.

9.Payments on Vouchers Payable totaled $2,505,000.

Additional information follows: The General Fund Fund Balance account had a credit balance of $82,900 as of December 31, 2010; no entries have been made in the Fund Balance account during 2011.

Required

a.Record the preceding transactions in general journal form for fiscal year 2011 in both the General Fund and governmental activities general journals.

b.Prepare a budgetary comparison schedule for the General Fund of the City of Fayette for the fiscal year ending December 31, 2011, as shown in Illustration 4-7.Do not prepare a government-wide statement of activities since other governmental funds would affect that statement.

1.The budget prepared for the fiscal year 2011 was as follows:

2.Encumbrances issued against the appropriations during the year were as follows: 3.The current year's tax levy of $2,005,000 was recorded; uncollectibles were estimated as $65,000.4.Tax collections from prior years' levies totaled $132,000; collections of the current year's levy totaled $1,459,000.

5.Personnel costs during the year were charged to the following appropriations in the amounts indicated.Encumbrances were not recorded for personnel costs.Since no liabilities currently exist for withholdings, you may ignore any FICA or federal or state income tax withholdings.( Note: Expenditures charged to Miscellaneous Appropriations should be treated as General Government expenses in the governmental activities general journal at the government-wide level.)

6.Invoices for all items ordered during the prior year were received and approved for payment in the amount of $14,470.Encumbrances had been recorded in the prior year for these items in the amount of $14,000.The amount chargeable to each year's appropriations should be charged to the Public Safety appropriation.7.Invoices were received and approved for payment for items ordered in documents recorded as encumbrances in Transaction (2) of this problem.The following appropriations were affected.

8.Revenue other than taxes collected during the year consisted of licenses and permits, $373,000; intergovernmental revenue, $400,000; and $66,000 of miscellaneous revenues.For purposes of accounting for these revenues at the government-wide level, the intergovernmental revenues were operating grants and contributions for the Public Safety function.Miscellaneous revenues are not identifiable with any function and therefore are recorded as General Revenues at the government-wide level.9.Payments on Vouchers Payable totaled $2,505,000.

Additional information follows: The General Fund Fund Balance account had a credit balance of $82,900 as of December 31, 2010; no entries have been made in the Fund Balance account during 2011.

Required

a.Record the preceding transactions in general journal form for fiscal year 2011 in both the General Fund and governmental activities general journals.

b.Prepare a budgetary comparison schedule for the General Fund of the City of Fayette for the fiscal year ending December 31, 2011, as shown in Illustration 4-7.Do not prepare a government-wide statement of activities since other governmental funds would affect that statement.

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

23

Name the four classes of nonexchange transactions defined by GASB standards and explain the revenue and expenditure/expense recognition rules applicable to each class.

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

24

Operating Transactions, Special Topics, and Financial Statements.The City of Ashland's General Fund had the following post-closing trial balance at April 30, 2010, the end of its fiscal year:

During the year ended April 30, 2011, the following transactions, in summary form, with subsidiary ledger detail omitted, occurred:

1.The budget for FY 2011 provided for General Fund estimated revenues totaling $3,140,000 and appropriations totaling $3,100,000.

2.The city council authorized temporary borrowing of $300,000 in the form of a 120-day tax anticipation note.The loan was obtained from a local bank at a discount of 6 percent per annum (debit Expenditures for discount).

3.The property tax levy for FY 2011 was recorded.Net assessed valuation of taxable property for the year was $43,000,000, and the tax rate was $5 per $100.It was estimated that 4 percent of the levy would be uncollectible.

4.Purchase orders and contracts were issued to vendors and others in the amount of $2,059,000.

5.The County Board of Review discovered unassessed properties with a total taxable value of $500,000.The owners of these properties were charged with taxes at the city's General Fund rate of $5 per $100 assessed value.(You need not adjust the Estimated Uncollectible Current Taxes account.)6.$1,961,000 of current taxes, $383,270 of delinquent taxes, and $20,570 of interest and penalties were collected.

7.Additional interest and penalties on delinquent taxes were accrued in the amount of $38,430, of which 30 percent was estimated to be uncollectible.

8.Because of a change in state law, the city was notified that it will receive $80,000 less in intergovernmental revenues than was budgeted.

9.Total payroll during the year was $819,490.Of that amount, $62,690 was withheld for employees' FICA tax liability, $103,710 for employees' federal income tax liability, and $34,400 for state taxes; the balance was paid to employees in cash.

10.The employer's FICA tax liability was recorded for $62,690.

11.Revenues from sources other than taxes were collected in the amount of $946,700.

12.Amounts due the federal government as of April 30, 2011, and amounts due for FICA taxes, and state and federal withholding taxes during the year were vouchered.

13.Purchase orders and contracts encumbered in the amount of $1,988,040 were filled at a net cost of $1,987,570, which was vouchered.

14.Vouchers payable totaling $2,301,660 were paid after deducting a credit for purchases discount of $8,030 (credit Expenditures).

15.The tax anticipation note of $300,000 was repaid.

16.All unpaid current year's property taxes became delinquent.The balances of the current tax receivables and related uncollectibles were transferred to delinquent accounts.

17.A physical inventory of materials and supplies at April 30, 2011, showed a total of $19,100.Inventory is recorded using the purchases method in the General Fund; the consumption method is used at the government-wide level.

Required

a.Record in general journal form the effect of the above transactions on the General Fund and governmental activities for the year ended April 30, 2011.Do not record subsidiary ledger debits and credits.

b.Record in general journal form entries to close the budgetary and operating statement accounts.

c.Prepare a General Fund balance sheet as of April 30, 2011.

d.Prepare a statement of revenues, expenditures, and changes in fund balance for the year ended April 30, 2011.Do not prepare the government-wide financial statements.

During the year ended April 30, 2011, the following transactions, in summary form, with subsidiary ledger detail omitted, occurred:1.The budget for FY 2011 provided for General Fund estimated revenues totaling $3,140,000 and appropriations totaling $3,100,000.

2.The city council authorized temporary borrowing of $300,000 in the form of a 120-day tax anticipation note.The loan was obtained from a local bank at a discount of 6 percent per annum (debit Expenditures for discount).

3.The property tax levy for FY 2011 was recorded.Net assessed valuation of taxable property for the year was $43,000,000, and the tax rate was $5 per $100.It was estimated that 4 percent of the levy would be uncollectible.

4.Purchase orders and contracts were issued to vendors and others in the amount of $2,059,000.

5.The County Board of Review discovered unassessed properties with a total taxable value of $500,000.The owners of these properties were charged with taxes at the city's General Fund rate of $5 per $100 assessed value.(You need not adjust the Estimated Uncollectible Current Taxes account.)6.$1,961,000 of current taxes, $383,270 of delinquent taxes, and $20,570 of interest and penalties were collected.

7.Additional interest and penalties on delinquent taxes were accrued in the amount of $38,430, of which 30 percent was estimated to be uncollectible.

8.Because of a change in state law, the city was notified that it will receive $80,000 less in intergovernmental revenues than was budgeted.

9.Total payroll during the year was $819,490.Of that amount, $62,690 was withheld for employees' FICA tax liability, $103,710 for employees' federal income tax liability, and $34,400 for state taxes; the balance was paid to employees in cash.

10.The employer's FICA tax liability was recorded for $62,690.

11.Revenues from sources other than taxes were collected in the amount of $946,700.

12.Amounts due the federal government as of April 30, 2011, and amounts due for FICA taxes, and state and federal withholding taxes during the year were vouchered.

13.Purchase orders and contracts encumbered in the amount of $1,988,040 were filled at a net cost of $1,987,570, which was vouchered.

14.Vouchers payable totaling $2,301,660 were paid after deducting a credit for purchases discount of $8,030 (credit Expenditures).

15.The tax anticipation note of $300,000 was repaid.

16.All unpaid current year's property taxes became delinquent.The balances of the current tax receivables and related uncollectibles were transferred to delinquent accounts.

17.A physical inventory of materials and supplies at April 30, 2011, showed a total of $19,100.Inventory is recorded using the purchases method in the General Fund; the consumption method is used at the government-wide level.

Required

a.Record in general journal form the effect of the above transactions on the General Fund and governmental activities for the year ended April 30, 2011.Do not record subsidiary ledger debits and credits.

b.Record in general journal form entries to close the budgetary and operating statement accounts.

c.Prepare a General Fund balance sheet as of April 30, 2011.

d.Prepare a statement of revenues, expenditures, and changes in fund balance for the year ended April 30, 2011.Do not prepare the government-wide financial statements.

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

25

Permanent Fund and Related Special Revenue Fund Transactions.Annabelle

Benton, great-granddaughter of the founder of the Town of Benton, made a cash contribution in the amount of $500,00 to be held as an endowment.To account for this endowment, the town has created the Alex Benton Park Endowment Fund.Under terms of the agreement, the town must invest and conserve the principal amount of the contribution in perpetuity.Earnings, measured on the accrual basis, must be used to maintain Alex Benton Park in an "attractive manner." All changes in fair value are treated as adjustments of fund balance of the permanent fund and do not affect earnings.Earnings are transferred periodically to the Alex Benton Park Maintenance Fund, a special revenue fund.Information pertaining to transactions of the endowment and special revenue funds for the fiscal year ended June 30, 2011, follows:

1.The contribution of $500,000 was received and recorded on December 31, 2010.

2.On December 31, 2010, bonds having a face value of $400,000 were purchased for $406,300, plus three months of accrued interest of $6,000.A certificate of deposit with a face and fair value of $70,000 was also purchased on this date.The bonds mature on October 1, 2019 (105 months from date of purchase), and pay interest of 6 percent per annum semiannually on April 1 and October 1.The certificate of deposit pays interest of 4 percent per annum payable on March 31, June 30, September 30, and December 31.

3.On January 2, 2011, the town council approved a budget for the Alex Ben- ton Park Maintenance Fund, which included estimated revenues of $13,400 and appropriations of $13,000.

4.On March 31, 2011, interest on the certificate of deposit was received by the endowment fund and transferred to the Alex Benton Park Maintenance Fund.

5.The April 1, 2011, bond interest was received by the endowment fund and transferred to the Alex Benton Park Maintenance Fund.

6.On June 30, 2011, interest on the certificate of deposit was received and transferred to the Alex Benton Park Maintenance Fund.

7.For the year ended June 30, 2011, maintenance expenditures from the Alex Benton Park Maintenance Fund amounted to $2,700 for materials and contractual services and $10,150 for wages and salaries.All expenditures were paid in cash except for $430 of vouchers payable as of June 30, 2011.Inventories of materials and supplies are deemed immaterial in amount.

8.On June 30, 2011, bonds with face value of $100,000 were sold for $102,000 plus accrued interest of $1,500.On the same date, 2,000 shares of ABC Corporation's stock were purchased at $52 per share.

Required

a.Prepare in general journal form the entries required in the Alex Benton Park Endowment Fund to record the transactions occurring during the fiscal year ending June 30, 2011, including all appropriate adjusting and closing entries.( Note: Ignore related entries in the governmental activities journal at the government-wide level.)b.Prepare in general journal form the entries required in the Alex Benton Park Maintenance Fund to record Transactions 1-8.

c.Prepare the following financial statements:

(1) A balance sheet for both the Alex Benton Park Endowment Fund and the Alex Benton Park Maintenance Fund as of June 30, 2011.

(2) A statement of revenues, expenditures, and changes in fund balance for both the Alex Benton Park Endowment Fund and the Alex Benton Park Maintenance Fund for the year ended June 30, 2011.