Deck 4: Quality and Standards of Assurance Engagements

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

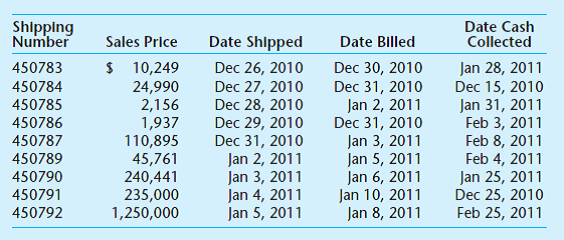

Cutoff tests. While performing a sales cutoff test for your audit client, you review all shipping documents for five days before and five days after year-end. All sales are on credit and are sent FOB shipping point. Cost of goods sold is 75% of sales revenue. You are using the shipping log for the ten-day time period of the test. Test results follow.

a. Identify by shipping number the sales that the company has recorded as sales revenue at December 31, 2010.

b. Identify by shipping number the sales that should have been recorded as sales revenue at December 31, 2010.

c. Prepare the adjusting entry needed to correct the sales revenue and inventory at December 31, 2010.

d. Prepare the journal entries needed to record the sale represented by shipping document 450784, including the cash collection and the revenue recognition.

e. What accounting rule should the company use to recognize revenue

f. How is the company currently recognizing revenue

g. What questions should you ask the client to clarify the evidence you have gathered during this audit test

a. Identify by shipping number the sales that the company has recorded as sales revenue at December 31, 2010.

b. Identify by shipping number the sales that should have been recorded as sales revenue at December 31, 2010.

c. Prepare the adjusting entry needed to correct the sales revenue and inventory at December 31, 2010.

d. Prepare the journal entries needed to record the sale represented by shipping document 450784, including the cash collection and the revenue recognition.

e. What accounting rule should the company use to recognize revenue

f. How is the company currently recognizing revenue

g. What questions should you ask the client to clarify the evidence you have gathered during this audit test

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

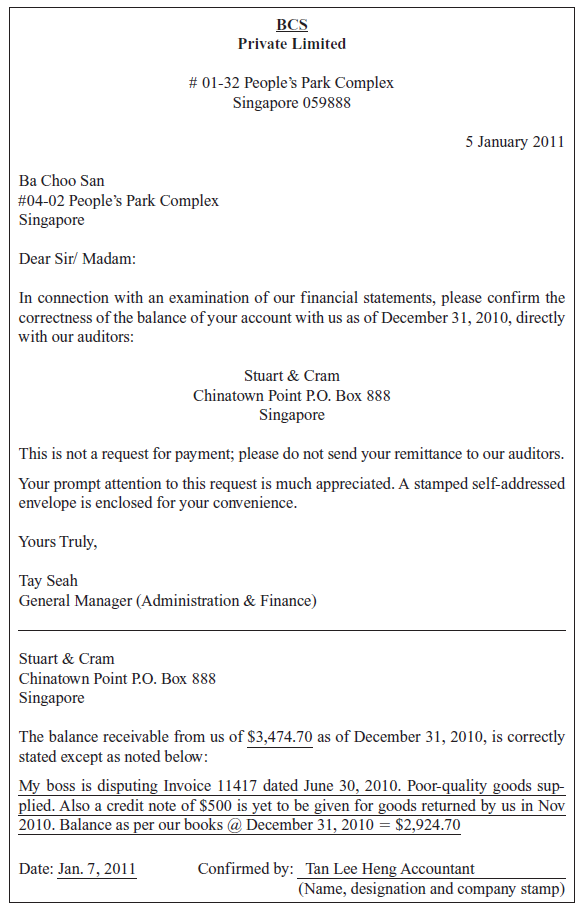

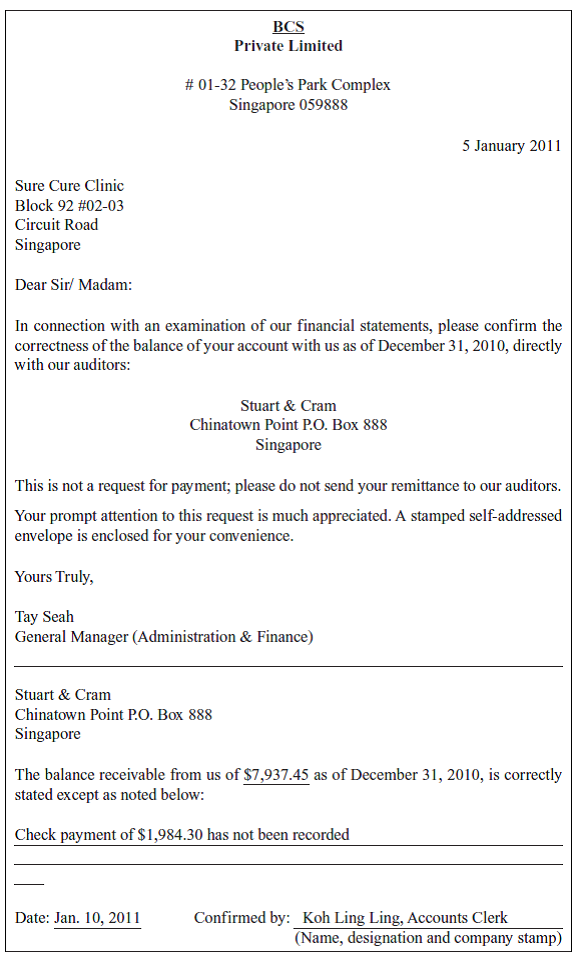

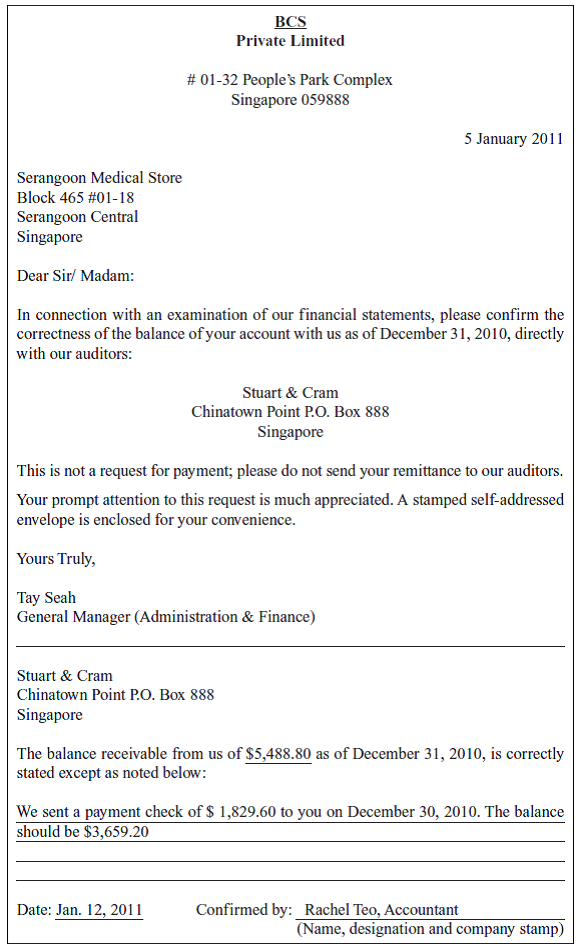

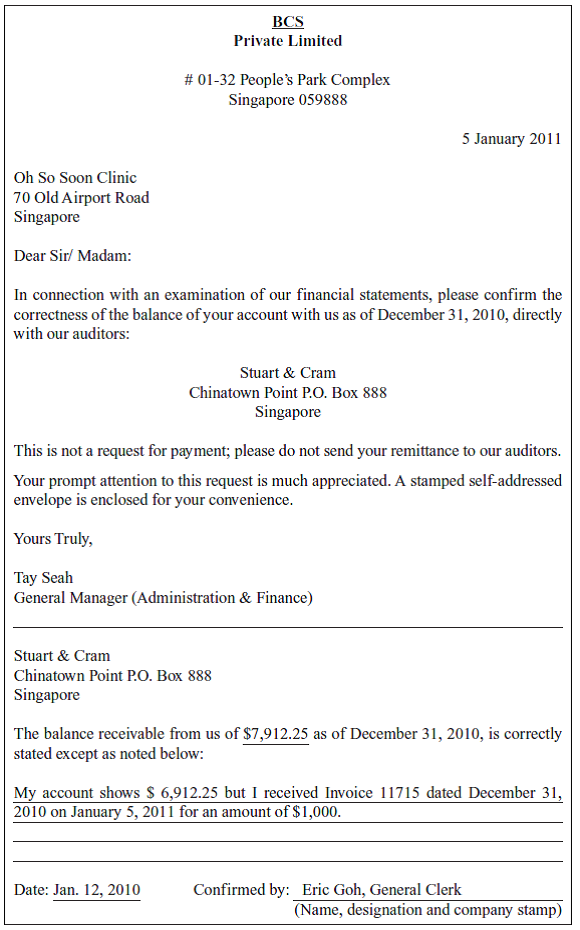

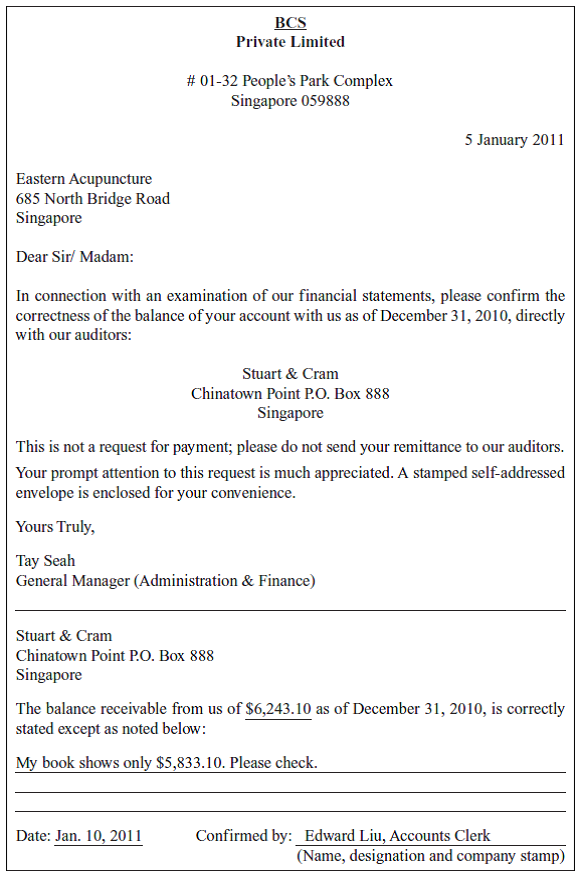

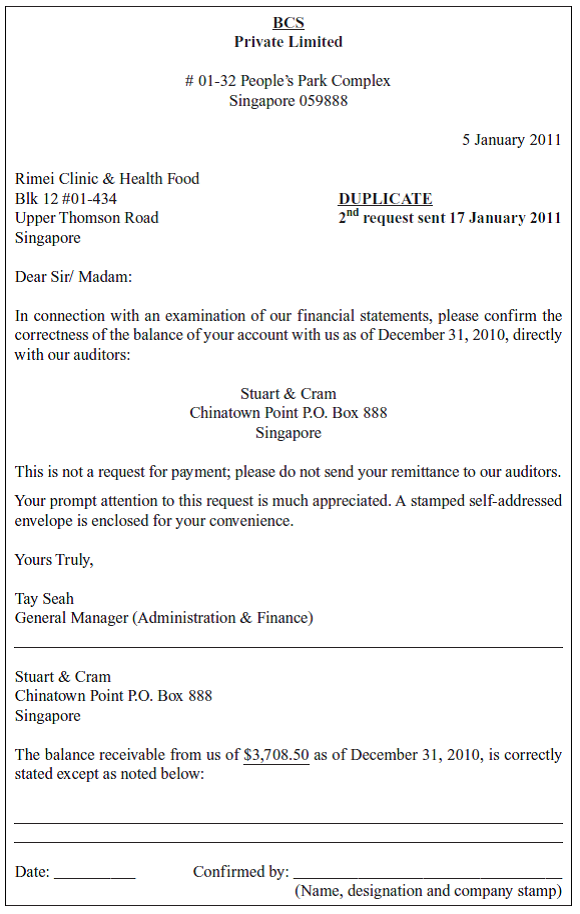

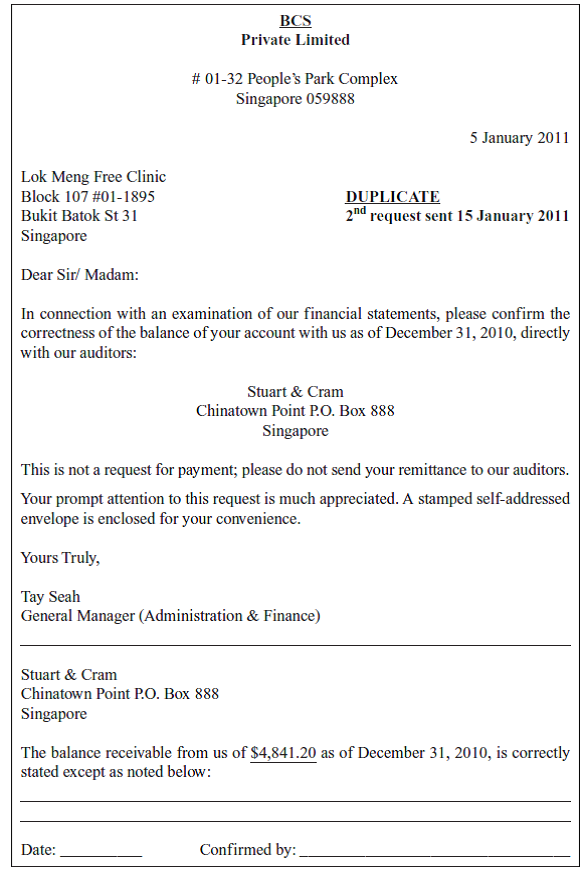

Substantive test of balances. Refer to Appendix A for five replies from customers of BCS Inc. in response to the receivables confirmation conducted by Stuart Cram, the BCS auditor and a copy of two letters for which replies have not yet been received.

a. For each reply, explain what you think has happened, how you would verify your explanation, and whether the reply represents a misstatement in the BCS accounts. If so, prepare the adjusting entry.

b. For the two nonreplies, explain what other method the auditor could use to obtain some assurance on the balances involved.

a. For each reply, explain what you think has happened, how you would verify your explanation, and whether the reply represents a misstatement in the BCS accounts. If so, prepare the adjusting entry.

b. For the two nonreplies, explain what other method the auditor could use to obtain some assurance on the balances involved.

Question

Question

Question

Question

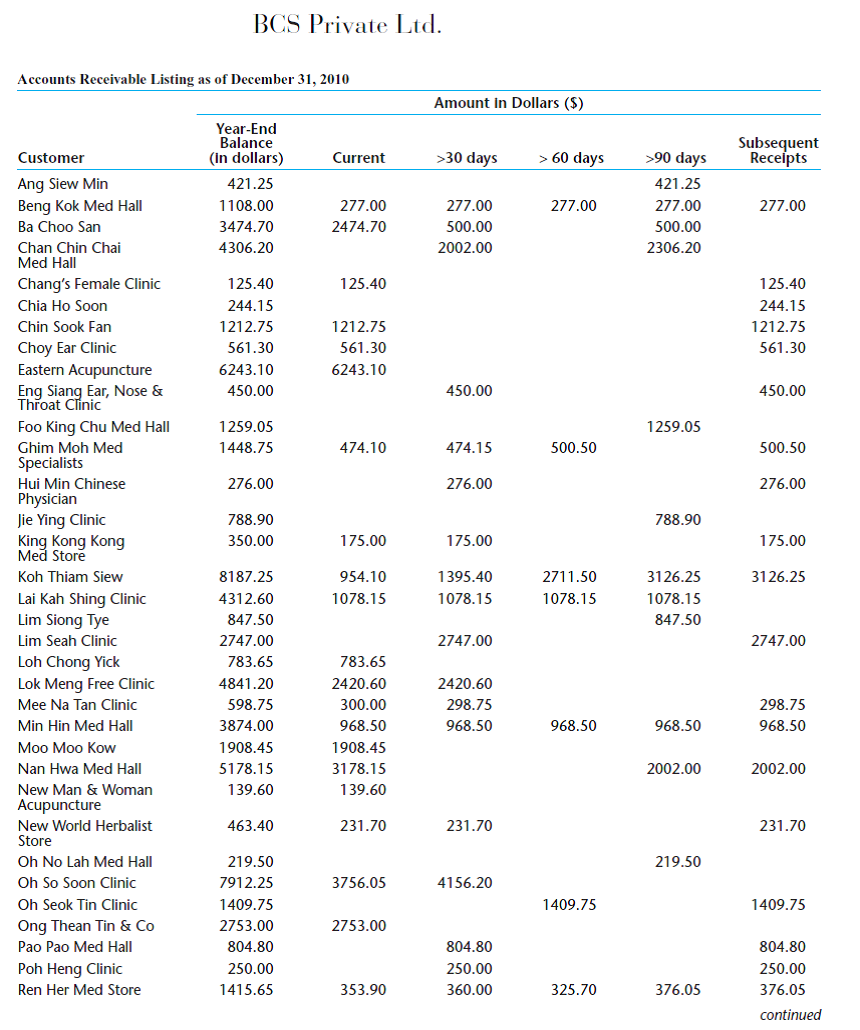

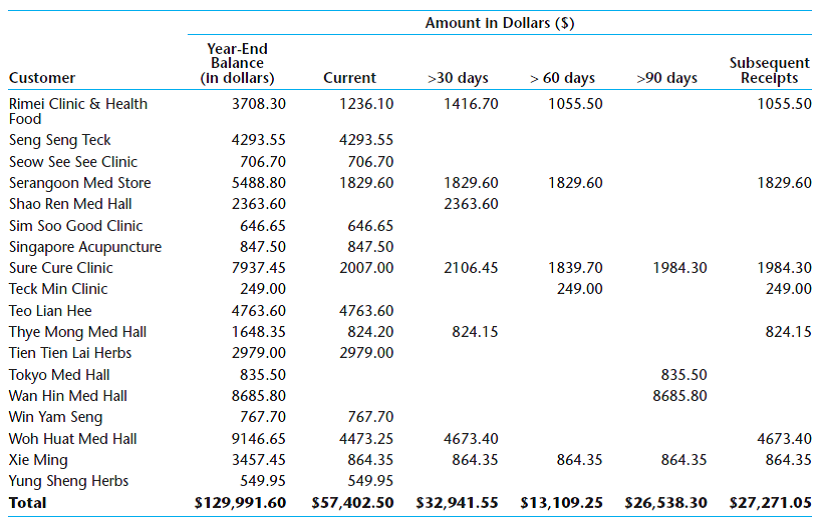

Evaluating the allowance for doubtful accounts. See Appendix B for the aged receivables trial balance for BCS. Review it and explain what the information in each column represents.

a. Use this information to calculate a bad debt provision for BCS at December 31, 2010 Last year BCS used the following percentages to calculate the bad debt provision: current accounts, .05%; 30 day accounts, 2%; 60 day accounts, 10%; 90 day accounts, 40%. First calculate the allowance using the percentages applicable in the previous year. Then, if you determine that actual write-offs last year were $20,000 more than the provision and that the economic conditions for BCS customers has worsened in the current year, explain how you could adjust the allowance.

b. Why is it necessary for BCS to estimate bad debt expense at year-end What accounting principle does BCS violate if it does not estimate bad debt

a. Use this information to calculate a bad debt provision for BCS at December 31, 2010 Last year BCS used the following percentages to calculate the bad debt provision: current accounts, .05%; 30 day accounts, 2%; 60 day accounts, 10%; 90 day accounts, 40%. First calculate the allowance using the percentages applicable in the previous year. Then, if you determine that actual write-offs last year were $20,000 more than the provision and that the economic conditions for BCS customers has worsened in the current year, explain how you could adjust the allowance.

b. Why is it necessary for BCS to estimate bad debt expense at year-end What accounting principle does BCS violate if it does not estimate bad debt

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/63

Play

Full screen (f)

Deck 4: Quality and Standards of Assurance Engagements

1

What are errors and fraud

Financial statement:

The financial statement of a company is the record of past year activities. There are many financial statements like cash flow statement, balance sheet, income statement, profit and loss account, etc.

Audit:

The audit is the process of checking the financial statements of a company `to ensure that it is 100% authentic and free from any kind of bias or fraud.

Functions of audit:

• To verify the financial statements

• To give an opinion on the financial statement after the audit

• To inform the management of the company about the fraud, if any.

Fraud:

Fraud means the willingly wrong representation of something, to hide some material facts from outsiders or mislead them about some facts.

Example: Misrepresentation of cash balance in the balance sheet, Misrepresentation of profit in the income statement to mislead the shareholders, Using wrong accounting standards, etc.

Error:

An error means mistakes. Error in auditing means that representation of wrong facts about the company by mistake. This happens when the accountant used the wrong accounting standard or assumption in the recording process of accounting transactions.

Example: Recording fixed assets on market value, recording inventory on acquiring value, etc.

The financial statement of a company is the record of past year activities. There are many financial statements like cash flow statement, balance sheet, income statement, profit and loss account, etc.

Audit:

The audit is the process of checking the financial statements of a company `to ensure that it is 100% authentic and free from any kind of bias or fraud.

Functions of audit:

• To verify the financial statements

• To give an opinion on the financial statement after the audit

• To inform the management of the company about the fraud, if any.

Fraud:

Fraud means the willingly wrong representation of something, to hide some material facts from outsiders or mislead them about some facts.

Example: Misrepresentation of cash balance in the balance sheet, Misrepresentation of profit in the income statement to mislead the shareholders, Using wrong accounting standards, etc.

Error:

An error means mistakes. Error in auditing means that representation of wrong facts about the company by mistake. This happens when the accountant used the wrong accounting standard or assumption in the recording process of accounting transactions.

Example: Recording fixed assets on market value, recording inventory on acquiring value, etc.

2

What are positive confirmations

Accounts receivable:

It is the amount due to customers on the sale of goods or services but not received yet (Credit sales).

Bad debt:

It the amount in accounts receivable that the company is not able to collect.

Allowance for doubtful debt:

It an allowance maintain by the company against the probable loss of bad debt.

Positive confirmation:

The auditor sends a confirmation letter to a sample bunch of accounts receivable of the company. The auditor sends this letter to confirm the amount it owes at the year-end.

Positive confirmation means that accounts receivable is expected to reply whether the balance is correct or incorrect. The customer needs to reply about the amount it owes.

It is the amount due to customers on the sale of goods or services but not received yet (Credit sales).

Bad debt:

It the amount in accounts receivable that the company is not able to collect.

Allowance for doubtful debt:

It an allowance maintain by the company against the probable loss of bad debt.

Positive confirmation:

The auditor sends a confirmation letter to a sample bunch of accounts receivable of the company. The auditor sends this letter to confirm the amount it owes at the year-end.

Positive confirmation means that accounts receivable is expected to reply whether the balance is correct or incorrect. The customer needs to reply about the amount it owes.

3

Analyzing the results from analytical procedures. The auditor performs preliminary analytical procedures to plan the audit. Results from the analytical procedures for the revenue process follow. In addition to the below questions, for each result, indicate how the auditor adjusts the audit program to gather evidence regarding the potential misstatements in the financial statements that could be suggested by the results from the analytical procedures.

a. The auditor compares the accounts receivable balance with the previous year's balance and finds that it has decreased. What questions should the auditor ask What misstatement could the auditor anticipate in the financial statements

b. The auditor calculates the accounts receivable turnover for the current year and the previous year and finds that it decreased for the current year. What questions should the auditor ask What misstatement could the auditor anticipate in the financial statements

c. The auditor compares the balance in the Allowance for Doubtful Accounts for the current year and the previous year and finds that it has declined in the current year. What questions should the auditor ask What misstatement could the auditor anticipate in the financial statements

d. The auditor compares the balance in the Sales Returns account for the current and previous year and finds that it has increased. What questions should the auditor ask What misstatement could the auditor anticipate in the financial statements

a. The auditor compares the accounts receivable balance with the previous year's balance and finds that it has decreased. What questions should the auditor ask What misstatement could the auditor anticipate in the financial statements

b. The auditor calculates the accounts receivable turnover for the current year and the previous year and finds that it decreased for the current year. What questions should the auditor ask What misstatement could the auditor anticipate in the financial statements

c. The auditor compares the balance in the Allowance for Doubtful Accounts for the current year and the previous year and finds that it has declined in the current year. What questions should the auditor ask What misstatement could the auditor anticipate in the financial statements

d. The auditor compares the balance in the Sales Returns account for the current and previous year and finds that it has increased. What questions should the auditor ask What misstatement could the auditor anticipate in the financial statements

Financial statement:

The financial statement of a company is the record of past year activities. There are many financial statements like cash flow statement, balance sheet, income statement, profit and loss account, etc.

Accounts receivable:

It is the amount due to customers on the sale of goods or services but not received yet (Credit sales).

Bad debt:

It the amount in accounts receivable that the company is not able to collect.

Allowance for doubtful debt:

It an allowance maintain by the company against the probable loss of bad debt.

Sales return:

It is a part of the sold goods that returned by the buyer. There are many reasons to do so. Following are some reasons for sales return:

• The quality of the received product is not the same as expected,

• There is some defect in the product,

• The buyer wants some changes in the product, like another color or size, etc.

a.

Questions the auditor will ask:

• Why the balance of account receivable decreased

• Is there is any change in the balance of bad debt expense or allowance for doubtful debt

• Is the company now conducting sales on a cash basis

Misstatement in the financial statement could be anticipated by the auditor:

• The company overstates its bad debt expenses to reduce the net profit and tax burden.

• The company overstated its account receivable last year to show high profit and to mislead the stakeholders of the company.

b.

Questions the auditor will ask:

• Why the balance decreased

• Is there is any change in bad debt expense or allowance for doubtful debt

• If the accounts receivable turnover decreased because of a decrease in the net sales then why the net sales decreased

Misstatement in the financial statement could be anticipated by the auditor:

• The company understates its net sales to reduce the net profit and tax burden.

• The company overstated its account receivable to show high profit and to mislead the stakeholders of the company.

c.

Questions the auditor will ask:

• Why the balance decreased

• Is there is any change in the balance of bad debt expenses

• Is there is any change in the company policy regarding allowance for doubtful debts

Misstatement in the financial statement could be anticipated by the auditor:

• The company understates its bad debt expenses to increase the profit this misleads the stakeholders of the company.

d.

Questions the auditor will ask:

• Why the balance increased

• Is there any change in the quality of the products

Misstatement in the financial statement could be anticipated by the auditor:

• The company overstates its sales return to reduce the net profit and tax burden.

The financial statement of a company is the record of past year activities. There are many financial statements like cash flow statement, balance sheet, income statement, profit and loss account, etc.

Accounts receivable:

It is the amount due to customers on the sale of goods or services but not received yet (Credit sales).

Bad debt:

It the amount in accounts receivable that the company is not able to collect.

Allowance for doubtful debt:

It an allowance maintain by the company against the probable loss of bad debt.

Sales return:

It is a part of the sold goods that returned by the buyer. There are many reasons to do so. Following are some reasons for sales return:

• The quality of the received product is not the same as expected,

• There is some defect in the product,

• The buyer wants some changes in the product, like another color or size, etc.

a.

Questions the auditor will ask:

• Why the balance of account receivable decreased

• Is there is any change in the balance of bad debt expense or allowance for doubtful debt

• Is the company now conducting sales on a cash basis

Misstatement in the financial statement could be anticipated by the auditor:

• The company overstates its bad debt expenses to reduce the net profit and tax burden.

• The company overstated its account receivable last year to show high profit and to mislead the stakeholders of the company.

b.

Questions the auditor will ask:

• Why the balance decreased

• Is there is any change in bad debt expense or allowance for doubtful debt

• If the accounts receivable turnover decreased because of a decrease in the net sales then why the net sales decreased

Misstatement in the financial statement could be anticipated by the auditor:

• The company understates its net sales to reduce the net profit and tax burden.

• The company overstated its account receivable to show high profit and to mislead the stakeholders of the company.

c.

Questions the auditor will ask:

• Why the balance decreased

• Is there is any change in the balance of bad debt expenses

• Is there is any change in the company policy regarding allowance for doubtful debts

Misstatement in the financial statement could be anticipated by the auditor:

• The company understates its bad debt expenses to increase the profit this misleads the stakeholders of the company.

d.

Questions the auditor will ask:

• Why the balance increased

• Is there any change in the quality of the products

Misstatement in the financial statement could be anticipated by the auditor:

• The company overstates its sales return to reduce the net profit and tax burden.

4

Bristol-Myers Squibb

Bristol-Myers produces and distributes medicines and health care products. In 2002, the company experienced one of its worst years in its 100-year history. Three of its top- selling drugs lost patent protection, and sales dramatically declined due to their generic substitutes produced by other companies. The share price of Bristol-Myers stock declined by nearly two-thirds, from about $75 in September 1999 to $25 in September 2002.

In April 2002, the company disclosed that it had used sales incentives to encourage wholesalers to buy more drugs and health care products than necessary. In July 2002, Bristol-Myers was notified that the SEC was opening a formal inquiry to determine whether the company had inflated revenue by as much as $1 billion in 2001 through the use of sales incentives. The company restated its earnings to remove the amount of excessive sales. a. Evaluate Bristol-Myers Squibb's revenue recognition policy. Why did the SEC object to it

b. If you had been Bristol-Myers Squibb's auditor, what questions would you have asked the client about the sales incentives How would you modify the audit risk model to account for them

c. Identify an internal control procedure that could have prevented the revenue misstatement that occurred.

Bristol-Myers produces and distributes medicines and health care products. In 2002, the company experienced one of its worst years in its 100-year history. Three of its top- selling drugs lost patent protection, and sales dramatically declined due to their generic substitutes produced by other companies. The share price of Bristol-Myers stock declined by nearly two-thirds, from about $75 in September 1999 to $25 in September 2002.

In April 2002, the company disclosed that it had used sales incentives to encourage wholesalers to buy more drugs and health care products than necessary. In July 2002, Bristol-Myers was notified that the SEC was opening a formal inquiry to determine whether the company had inflated revenue by as much as $1 billion in 2001 through the use of sales incentives. The company restated its earnings to remove the amount of excessive sales. a. Evaluate Bristol-Myers Squibb's revenue recognition policy. Why did the SEC object to it

b. If you had been Bristol-Myers Squibb's auditor, what questions would you have asked the client about the sales incentives How would you modify the audit risk model to account for them

c. Identify an internal control procedure that could have prevented the revenue misstatement that occurred.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

5

What do the auditing standards say about the auditor's presumption relating to the possibility of revenue fraud in the financial statements

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

6

What are negative confirmations

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

7

Performing substantive tests of transactions. The auditor performs substantive tests of transactions for sales revenue to determine that the sales revenue reported on the income statements is not materially misstated. For each procedure performed in the audit of the revenue process in the following list, indicate the management assertion that is tested during the audit procedure.

a. The auditor selects a sample of shipping documents and traces the documents to the sales invoices.

b. The auditor selects a sample of sales invoices and traces the documents to the shipping notices.

c. The auditor selects a sample of recorded sales from the sales journal and determines whether credit was approved for the sale.

d. The auditor selects a sample of recorded sales from the sales journal and vouches the prices on the sales invoices to an approved price list.

e. The auditor selects a sample of recorded sales from the sales journal and determines whether the amount billed equals the amount shipped.

a. The auditor selects a sample of shipping documents and traces the documents to the sales invoices.

b. The auditor selects a sample of sales invoices and traces the documents to the shipping notices.

c. The auditor selects a sample of recorded sales from the sales journal and determines whether credit was approved for the sale.

d. The auditor selects a sample of recorded sales from the sales journal and vouches the prices on the sales invoices to an approved price list.

e. The auditor selects a sample of recorded sales from the sales journal and determines whether the amount billed equals the amount shipped.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

8

Time Warner

In July 2002, the SEC reviewed revenue transactions by the America Online (AOL) unit of Time Warner to determine whether the company used "unconventional" ad deals to increase revenue to meet expectations of Wall Street analysts. An article appearing in The Washington Post on July 18, 2002, alleged that AOL had manipulated its ad revenue when it was waiting for approval of its merger with Time Warner, which owns CNN cable news, HBO, Warner Brothers, and Time magazine. The new company known as AOL Time Warner was created on January 11, 2001. As a result of the merger, American Online and Time Warner each became a wholly owned subsidiary of AOL Time Warner. In 2003, the name of the company was changed to Time Warner.

A Washington Post reporter reviewed a number of AOL's revenue transactions from July 2000 to March 2002. Without the unconventional deals described in the article, quarterly earnings per share would not have met analysts' forecasts for two quarters in 2000. According to the Post, during this time, "Investors punished companies whose earnings were off by even a cent." 12 AOL employees interviewed for the article said that the company was under tremendous pressure to meet its revenue targets due to the $112 billion merger pending with Time Warner. Ad revenue became very important to the Internet division as competition from other Internet service providers hurt AOL's monthly subscriber fees. Unfortunately, the contracts for the advertising services were with dot-com companies, which also were suffering from declining sales and many of which did not have the cash to pay for the ads they had agreed to buy from AOL.

The unconventional deals include a variety of methods to increase revenue. AOL's business affairs department contacted companies that were unable to pay for their long-term ad contracts and renegotiated the terms, requiring the companies to make one-time payments to renegotiate or get out of the contracts. AOL recognized all revenue for the renegotiated contracts immediately as ad revenue. Earlier, in September 2000, AOL had used another unconventional ad deal to generate revenue. It recorded ad revenue based on a lawsuit settlement. AOL purchased Movie Fone in 1999, which had won a $26.8 million settlement from Wembley PLC, a British entertainment company, but had not yet collected the claim. Instead of collecting the settlement, AOL offered Wembley the opportunity to buy $23.8 million in online ads (a good deal for Wembley because it saved $3 million). Because AOL was short of advertising revenue for the quarter ending on September 30, 2000, it had to create the Wembley ads and air them before the end of the quarter. Wembley considered the proposal for some time, but AOL could not wait for its decision because this revenue had to be booked in September 2000. Without Wembley's knowledge, AOL took artwork from Wembley's British website (24 Dogs.com, an online greyhound racing website) and created banner and button ads using the artwork and started running them on various AOL sites. Within an hour of posting the greyhound ads, the Wembley website crashed, due to the traffic generated by the AOL ads.

Despite AOL's action, Wembley reached an ad agreement with it that generated $16.4 million in ad revenue for the September 30, 2000, quarter, effectively taking a nonoperating gain on a lawsuit settlement and converting it to a more valuable operating revenue number.

a. Evaluate the revenue recognition policies used by AOL. Are the policies consistent with the applicable financial reporting framework

b. How would the auditor discover the misstatements in the financial statements

c. Describe how the audit risk model could be used in the AOL audit to consider the pending acquisition and the decline in sales revenue.

In July 2002, the SEC reviewed revenue transactions by the America Online (AOL) unit of Time Warner to determine whether the company used "unconventional" ad deals to increase revenue to meet expectations of Wall Street analysts. An article appearing in The Washington Post on July 18, 2002, alleged that AOL had manipulated its ad revenue when it was waiting for approval of its merger with Time Warner, which owns CNN cable news, HBO, Warner Brothers, and Time magazine. The new company known as AOL Time Warner was created on January 11, 2001. As a result of the merger, American Online and Time Warner each became a wholly owned subsidiary of AOL Time Warner. In 2003, the name of the company was changed to Time Warner.

A Washington Post reporter reviewed a number of AOL's revenue transactions from July 2000 to March 2002. Without the unconventional deals described in the article, quarterly earnings per share would not have met analysts' forecasts for two quarters in 2000. According to the Post, during this time, "Investors punished companies whose earnings were off by even a cent." 12 AOL employees interviewed for the article said that the company was under tremendous pressure to meet its revenue targets due to the $112 billion merger pending with Time Warner. Ad revenue became very important to the Internet division as competition from other Internet service providers hurt AOL's monthly subscriber fees. Unfortunately, the contracts for the advertising services were with dot-com companies, which also were suffering from declining sales and many of which did not have the cash to pay for the ads they had agreed to buy from AOL.

The unconventional deals include a variety of methods to increase revenue. AOL's business affairs department contacted companies that were unable to pay for their long-term ad contracts and renegotiated the terms, requiring the companies to make one-time payments to renegotiate or get out of the contracts. AOL recognized all revenue for the renegotiated contracts immediately as ad revenue. Earlier, in September 2000, AOL had used another unconventional ad deal to generate revenue. It recorded ad revenue based on a lawsuit settlement. AOL purchased Movie Fone in 1999, which had won a $26.8 million settlement from Wembley PLC, a British entertainment company, but had not yet collected the claim. Instead of collecting the settlement, AOL offered Wembley the opportunity to buy $23.8 million in online ads (a good deal for Wembley because it saved $3 million). Because AOL was short of advertising revenue for the quarter ending on September 30, 2000, it had to create the Wembley ads and air them before the end of the quarter. Wembley considered the proposal for some time, but AOL could not wait for its decision because this revenue had to be booked in September 2000. Without Wembley's knowledge, AOL took artwork from Wembley's British website (24 Dogs.com, an online greyhound racing website) and created banner and button ads using the artwork and started running them on various AOL sites. Within an hour of posting the greyhound ads, the Wembley website crashed, due to the traffic generated by the AOL ads.

Despite AOL's action, Wembley reached an ad agreement with it that generated $16.4 million in ad revenue for the September 30, 2000, quarter, effectively taking a nonoperating gain on a lawsuit settlement and converting it to a more valuable operating revenue number.

a. Evaluate the revenue recognition policies used by AOL. Are the policies consistent with the applicable financial reporting framework

b. How would the auditor discover the misstatements in the financial statements

c. Describe how the audit risk model could be used in the AOL audit to consider the pending acquisition and the decline in sales revenue.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

9

Describe two ways that a client could misstate revenue. Which of these two methods could be harder for the auditor to catch

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

10

Explain how the auditor uses accounts receivable confirmations to gather evidence regarding the account balance.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

11

Internal control procedures. The auditor has documented the following internal control procedures used by the client. For each procedure, explain the test you would perform to determine whether the control was working and the assertion that you would be testing.

a. The warehouse clerk is required to have an approved sales order before goods are released from the warehouse to be sent to the shipping department.

b. Shipping clerks compare goods received from the warehouse with approved sales orders and initial the sales order indicating their agreement.

c. The accounting department compares the sales invoice price with the master price file and initials the sales invoice indicating agreement.

d. Control amounts posted to the accounts receivable ledger are compared with control totals of invoices. A daily reconciliation report is prepared by the accounting clerk and initialed at the end of each day.

e. Sales invoices are compared with shipping documents and approved customer orders before invoices are mailed. The accounts receivable clerk initials the shipping document indicating the agreement.

f. Goods returned for credit are approved by the supervisor of the sales department. The credit memo is initialed by the supervisor indicating approval.

g. The total cash payments posted to the accounts receivable ledger from remittance advices is compared to the bank deposit slip by the treasury department. The clerk in the treasury department indicates that the two agree by initialing the reconciliation report.

a. The warehouse clerk is required to have an approved sales order before goods are released from the warehouse to be sent to the shipping department.

b. Shipping clerks compare goods received from the warehouse with approved sales orders and initial the sales order indicating their agreement.

c. The accounting department compares the sales invoice price with the master price file and initials the sales invoice indicating agreement.

d. Control amounts posted to the accounts receivable ledger are compared with control totals of invoices. A daily reconciliation report is prepared by the accounting clerk and initialed at the end of each day.

e. Sales invoices are compared with shipping documents and approved customer orders before invoices are mailed. The accounts receivable clerk initials the shipping document indicating the agreement.

f. Goods returned for credit are approved by the supervisor of the sales department. The credit memo is initialed by the supervisor indicating approval.

g. The total cash payments posted to the accounts receivable ledger from remittance advices is compared to the bank deposit slip by the treasury department. The clerk in the treasury department indicates that the two agree by initialing the reconciliation report.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

12

Xerox Corporation

Xerox Corporation, a company based in Stamford, Connecticut, is involved in the production and management of documents in the form of copy machines, fax machines, and commercial printing equipment. In the late 1990s, competition had a negative impact on Xerox sales (among others things, computer printers were replacing copiers to generate print copies). A poorly organized business restructuring also caused administrative problems and billing and sales slowdowns for Xerox. The accounting department at Xerox began being pressured to compensate for the poor sales results with accounting measures. Xerox "assigned accountants numerical goals to produce profits through accounting actions. It just became standard operating procedure that, you know, you look to the accountants to find income."

In April 2002, Xerox settled a case with the SEC, agreeing to pay a $10 million fine and restating its results back to 1997. The restatement showed that it had recorded $6.4 billion of revenue early and had overstated its pretax income by $1.41 billion over the five years, a 36% overstatement. Paul R. Berger, Associate Director of Enforcement at the SEC, described the actions of Xerox executives in the SEC enforcement notice: "Xerox's senior management orchestrated a fouryear scheme to disguise the company's true operating performance. Such conduct calls for stiff sanctions, including in this case, the imposition of the largest fine ever obtained by the SEC against a public company in a financial fraud case. The penalty also reflects, in part, a sanction for the company's lack of full cooperation in the investigation."

The SEC enforcement notice reported that the company had recorded longterm leasing agreements for copiers over shorter periods than the leases ran in order to record more revenue during the early years of the leases. The company also had made a one-time sale of accounts receivable to increase operating results but failed to disclose this fact to outsiders. Xerox established a "cookie jar" reserve account that was set up to cover merger costs but instead was used to meet analysts' quarterly earnings forecasts. From 1997 to 2000, the SEC alleged that senior managers at Xerox were paid more than $5 million on performance-based compensation and made more than $30 million from the sale of company stock.

In a related SEC inquiry, notices of possible civil action for fraud were sent to KPMG, Xerox's former auditor (that had been fired in 2001), and a number of Xerox executives (both current and former). KPMG responded that it did nothing wrong in its work for Xerox and had, in fact, been fired for forcing Xerox to conduct an independent accounting exam that resulted in an earlier Xerox restatement. The restatement in 2001 prompted the SEC investigation in 2002. Xerox executives argued that they had relied on the accounting guidance provided by KPMG.

a. Evaluate the revenue recognition policies used by Xerox. As an auditor, would you have approved them

b. Describe how the audit risk model could have been used in the Xerox audit to consider the performance-based compensation and the decline in sales revenue.

c. How would the auditor evaluate management in this company Would the auditor be aware of management's position to "look to the accountants to find income"

Xerox Corporation, a company based in Stamford, Connecticut, is involved in the production and management of documents in the form of copy machines, fax machines, and commercial printing equipment. In the late 1990s, competition had a negative impact on Xerox sales (among others things, computer printers were replacing copiers to generate print copies). A poorly organized business restructuring also caused administrative problems and billing and sales slowdowns for Xerox. The accounting department at Xerox began being pressured to compensate for the poor sales results with accounting measures. Xerox "assigned accountants numerical goals to produce profits through accounting actions. It just became standard operating procedure that, you know, you look to the accountants to find income."

In April 2002, Xerox settled a case with the SEC, agreeing to pay a $10 million fine and restating its results back to 1997. The restatement showed that it had recorded $6.4 billion of revenue early and had overstated its pretax income by $1.41 billion over the five years, a 36% overstatement. Paul R. Berger, Associate Director of Enforcement at the SEC, described the actions of Xerox executives in the SEC enforcement notice: "Xerox's senior management orchestrated a fouryear scheme to disguise the company's true operating performance. Such conduct calls for stiff sanctions, including in this case, the imposition of the largest fine ever obtained by the SEC against a public company in a financial fraud case. The penalty also reflects, in part, a sanction for the company's lack of full cooperation in the investigation."

The SEC enforcement notice reported that the company had recorded longterm leasing agreements for copiers over shorter periods than the leases ran in order to record more revenue during the early years of the leases. The company also had made a one-time sale of accounts receivable to increase operating results but failed to disclose this fact to outsiders. Xerox established a "cookie jar" reserve account that was set up to cover merger costs but instead was used to meet analysts' quarterly earnings forecasts. From 1997 to 2000, the SEC alleged that senior managers at Xerox were paid more than $5 million on performance-based compensation and made more than $30 million from the sale of company stock.

In a related SEC inquiry, notices of possible civil action for fraud were sent to KPMG, Xerox's former auditor (that had been fired in 2001), and a number of Xerox executives (both current and former). KPMG responded that it did nothing wrong in its work for Xerox and had, in fact, been fired for forcing Xerox to conduct an independent accounting exam that resulted in an earlier Xerox restatement. The restatement in 2001 prompted the SEC investigation in 2002. Xerox executives argued that they had relied on the accounting guidance provided by KPMG.

a. Evaluate the revenue recognition policies used by Xerox. As an auditor, would you have approved them

b. Describe how the audit risk model could have been used in the Xerox audit to consider the performance-based compensation and the decline in sales revenue.

c. How would the auditor evaluate management in this company Would the auditor be aware of management's position to "look to the accountants to find income"

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

13

What role does professional skepticism play in the audit of the revenue process

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

14

How does the auditor evaluate the allowance for doubtful accounts

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

15

Performing substantive tests of transactions. The following audit steps are part of the audit program for the revenue process. Indicate the assertion supported by the evidence gathered in performing each procedure.

a. Select a sample of sales invoices from the sales journal.

(1) Vouch to the supporting shipping document.

(2) Determine whether credit was approved.

(3) Vouch prices on the invoice to the approved price list.

(4) Compare the amount billed to the amount shipped.

(5) Recalculate the invoice.

(6) Compare the shipping date with the invoice date.

(7) Trace the invoice to the posting in the control account for accounts receivable and the general ledger control account.

b. Select a sample of shipping documents from the shipping department file and trace the shipments to the recorded sales invoices.

c. Scan the sales invoices and the shipping documents for missing numbers in sequence.

a. Select a sample of sales invoices from the sales journal.

(1) Vouch to the supporting shipping document.

(2) Determine whether credit was approved.

(3) Vouch prices on the invoice to the approved price list.

(4) Compare the amount billed to the amount shipped.

(5) Recalculate the invoice.

(6) Compare the shipping date with the invoice date.

(7) Trace the invoice to the posting in the control account for accounts receivable and the general ledger control account.

b. Select a sample of shipping documents from the shipping department file and trace the shipments to the recorded sales invoices.

c. Scan the sales invoices and the shipping documents for missing numbers in sequence.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

16

Gemstar-TV Guide International, Inc.

KPMG and Gemstar, publisher of TV Guide magazine, agreed to pay the SEC a $10 million fine as a penalty for overstating revenue from 1999 to 2002. The overstatements involved improperly reporting licensing and advertising revenue. The SEC said that the auditors should have known that the company improperly recognized revenue. The SEC stated that KPMG auditors substituted "management representations for competent evidence."

The revenue recognition problems were described in an accounting and auditing enforcement notice disclosing the earnings misstatement. According to the report, the revenue recognition problems were in two areas of revenue: licensing and advertising.

Licensing Revenue and Disclosure in the Footnotes

Gemstar recognized $23.5 million in licensing revenue from AOL in 2000. This revenue represented an upfront fee that should have been recognized over the eightyear time period in which the services were to be provided. Gemstar recognized $113.5 million in licensing revenue from Scientific-Atlanta for 2000-2002 and $18.1 million in licensing revenue from Time Warner Cable (TWC) for 2001-2002. According to the report, the KPMG auditors should have known that the Scientific- Atlanta and TWC revenue recognition did not conform to a financial reporting framework because the contract terms did not meet the requirements. The company did not have a contract with Scientific-Atlanta or TWC, Gemstar had not received any of the revenue, the companies disputed the revenue recognized by Gemstar, and the revenue payments were contingent on then-current contract negotiations.

According to the enforcement notice, KPMG auditors should have known that Gemstar's revenue recognition disclosure in the footnotes did not comply with disclosure requirements consistent with the financial reporting framework. Accounting Principles Board (APB) Opinion No. 22 requires disclosure of all significant accounting policies. Under generally accepted auditing procedures, auditors should read the company's annual report. The disclosure related to the AOL revenue was inadequate because the company disclosed that it recognized revenue over the life of the contract and described the AOL contract as long term but failed to recognize revenue in accordance with the disclosure (it recognized all revenue in the first year of the eight-year contract).

The disclosure for the Scientific-Atlanta and TWC revenue indicated that Gemstar had recognized revenue when it received notification that a manufacturer had shipped units using Gemstar technology. According to the SEC, the auditors should have known that Gemstar's disclosure regarding revenue recognition based on licensing revenue was inadequate to describe the actual revenue recognition for this contingent revenue.

Advertising Revenue and Disclosure in the Footnotes

Gemstar recognized $60.1 million of advertising revenue in 2001 and 2002 from Motorola, (Chicago) Tribune Company, Fantasy Sports, and various print advertisers that did not conform to the financial reporting framework. The revenue came from noncash arrangements with customers as part of various business transactions. For example, the Motorola revenue originated with an arrangement by which it paid $188 million to use Genstar's IPG technology, to settle a litigation award, and to purchase $17.5 million of prepaid advertising. The Tribune revenue originated with an arrangement between it and Gemstar in which the Tribune agreed to purchase the WGN distribution business from Gemstar in exchange for $106 million in cash and $100 million in advertising. According to the SEC, KPMG auditors should have known that the Motorola and Tribune revenue were not recognized in accordance with the financial reporting framework. According to the SEC, Gemstar could not "reliably, verifiably, and objectively" determine the fair value of the advertising portion of the arrangement because it had not sold IPG advertising that was not part of a related-party or nonmonetary transaction.

The SEC also determined that the auditors should have known that Gemstar's disclosure in its 10-K was inconsistent with the company's method of accounting for the transaction. For example, the company described its substantial growth in the Interactive Sector revenue and attributed the growth to the "successful launch of IPG advertising." However, the company did not disclose that the revenue came from the Motorola and Tribune transactions. The auditor also should have known that the company disclosed the sale of WGN but not the $100 million of advertising revenue associated with the sale.

The SEC censured KPMG, which paid a fine of $10 million to settle the charges of improper conduct. KPMG partners involved in the audit were prohibited from working for public companies for a period of one to three years. At the time, the KPMG fine was the largest ever obtained by the SEC from an accounting firm. Cash from the settlement went to the Gemstar shareholders.

a. Evaluate Gemstar's revenue recognition decisions related to the licensing and advertising revenue. Explain why the SEC disagreed with the decisions made by management.

b. Why did the SEC determine that the disclosure made by Gemstar was not consistent with the financial reporting framework Explain the proper disclosure relating to the licensing and advertising revenue.

c. What does the SEC mean that the auditors substituted "management representations for evidence" What should the auditors have done to verify the revenue

KPMG and Gemstar, publisher of TV Guide magazine, agreed to pay the SEC a $10 million fine as a penalty for overstating revenue from 1999 to 2002. The overstatements involved improperly reporting licensing and advertising revenue. The SEC said that the auditors should have known that the company improperly recognized revenue. The SEC stated that KPMG auditors substituted "management representations for competent evidence."

The revenue recognition problems were described in an accounting and auditing enforcement notice disclosing the earnings misstatement. According to the report, the revenue recognition problems were in two areas of revenue: licensing and advertising.

Licensing Revenue and Disclosure in the Footnotes

Gemstar recognized $23.5 million in licensing revenue from AOL in 2000. This revenue represented an upfront fee that should have been recognized over the eightyear time period in which the services were to be provided. Gemstar recognized $113.5 million in licensing revenue from Scientific-Atlanta for 2000-2002 and $18.1 million in licensing revenue from Time Warner Cable (TWC) for 2001-2002. According to the report, the KPMG auditors should have known that the Scientific- Atlanta and TWC revenue recognition did not conform to a financial reporting framework because the contract terms did not meet the requirements. The company did not have a contract with Scientific-Atlanta or TWC, Gemstar had not received any of the revenue, the companies disputed the revenue recognized by Gemstar, and the revenue payments were contingent on then-current contract negotiations.

According to the enforcement notice, KPMG auditors should have known that Gemstar's revenue recognition disclosure in the footnotes did not comply with disclosure requirements consistent with the financial reporting framework. Accounting Principles Board (APB) Opinion No. 22 requires disclosure of all significant accounting policies. Under generally accepted auditing procedures, auditors should read the company's annual report. The disclosure related to the AOL revenue was inadequate because the company disclosed that it recognized revenue over the life of the contract and described the AOL contract as long term but failed to recognize revenue in accordance with the disclosure (it recognized all revenue in the first year of the eight-year contract).

The disclosure for the Scientific-Atlanta and TWC revenue indicated that Gemstar had recognized revenue when it received notification that a manufacturer had shipped units using Gemstar technology. According to the SEC, the auditors should have known that Gemstar's disclosure regarding revenue recognition based on licensing revenue was inadequate to describe the actual revenue recognition for this contingent revenue.

Advertising Revenue and Disclosure in the Footnotes

Gemstar recognized $60.1 million of advertising revenue in 2001 and 2002 from Motorola, (Chicago) Tribune Company, Fantasy Sports, and various print advertisers that did not conform to the financial reporting framework. The revenue came from noncash arrangements with customers as part of various business transactions. For example, the Motorola revenue originated with an arrangement by which it paid $188 million to use Genstar's IPG technology, to settle a litigation award, and to purchase $17.5 million of prepaid advertising. The Tribune revenue originated with an arrangement between it and Gemstar in which the Tribune agreed to purchase the WGN distribution business from Gemstar in exchange for $106 million in cash and $100 million in advertising. According to the SEC, KPMG auditors should have known that the Motorola and Tribune revenue were not recognized in accordance with the financial reporting framework. According to the SEC, Gemstar could not "reliably, verifiably, and objectively" determine the fair value of the advertising portion of the arrangement because it had not sold IPG advertising that was not part of a related-party or nonmonetary transaction.

The SEC also determined that the auditors should have known that Gemstar's disclosure in its 10-K was inconsistent with the company's method of accounting for the transaction. For example, the company described its substantial growth in the Interactive Sector revenue and attributed the growth to the "successful launch of IPG advertising." However, the company did not disclose that the revenue came from the Motorola and Tribune transactions. The auditor also should have known that the company disclosed the sale of WGN but not the $100 million of advertising revenue associated with the sale.

The SEC censured KPMG, which paid a fine of $10 million to settle the charges of improper conduct. KPMG partners involved in the audit were prohibited from working for public companies for a period of one to three years. At the time, the KPMG fine was the largest ever obtained by the SEC from an accounting firm. Cash from the settlement went to the Gemstar shareholders.

a. Evaluate Gemstar's revenue recognition decisions related to the licensing and advertising revenue. Explain why the SEC disagreed with the decisions made by management.

b. Why did the SEC determine that the disclosure made by Gemstar was not consistent with the financial reporting framework Explain the proper disclosure relating to the licensing and advertising revenue.

c. What does the SEC mean that the auditors substituted "management representations for evidence" What should the auditors have done to verify the revenue

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

17

Describe the assertions made by management regarding the accounts in the revenue process.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

18

How does the auditor test the presentation and disclosure assertions for the revenue process

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

19

Performing substantive tests of balances. The following audit steps are part of the revenue process audit program. Indicate the assertion supported by the evidence gathered in performing each procedure.

a. Select a sample of customers' accounts.

(1) Vouch debits in the accounts to sales invoices.

(2) Vouch credits in the accounts to cash receipts documentation and approved credit memos.

b. Select a sample of credit memos.

(1) Review for proper approval.

(2) Trace to posting in customers' accounts.

c. Scan the accounts receivable control account for postings from sources other than the sales and cash receipts journals. Vouch a sample of such entries to supporting documents.

a. Select a sample of customers' accounts.

(1) Vouch debits in the accounts to sales invoices.

(2) Vouch credits in the accounts to cash receipts documentation and approved credit memos.

b. Select a sample of credit memos.

(1) Review for proper approval.

(2) Trace to posting in customers' accounts.

c. Scan the accounts receivable control account for postings from sources other than the sales and cash receipts journals. Vouch a sample of such entries to supporting documents.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

20

Go to the website for a company of your choice and determine how it recognizes revenue, estimates sales returns, and determines the amount of uncollectible accounts. List the revenue reported for the last two years as well as the balance in Accounts Receivable and the Allowance for Doubtful Accounts for each year. Does the change in the allowance account appear reasonable Explain your answer.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

21

What are the most important assertions for the revenue process Explain your answer.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

22

A key internal control in the revenue process is the separation of duties between cash handling and record keeping. The objective most directly associated with this control is to verify that a. Cash receipts recorded in the cash receipts journal are reasonable

B) Cash receipts are properly classified

C) Recorded cash receipts result from legitimate transactions

D) Existing cash receipts are recorded

B) Cash receipts are properly classified

C) Recorded cash receipts result from legitimate transactions

D) Existing cash receipts are recorded

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

23

Testing internal control procedures in computerized and manual accounting systems. Accounting systems typically implement controls to prevent misstatements in processing transactions. For each of the following controls described, (1) indicate the misstatement that could occur if the control is not implemented and (2) identify an audit procedure to test the control's effectiveness.

a. Sales transactions less than $25,000 are approved by the accounting system automatically (without involvement of the credit manager). Sales transactions higher than $25,000 require written approval by the credit manager.

b. All sales invoices are priced according to an authorized price list. Any exceptions to this pricing must be approved by the sales manager.

c. All shipping document are prenumbered and accounted for. Shipping document numbers are noted on all sales invoices.

d. A report of exceptions noting the failure of the invoice amount and the shipping amount to match is sent to the sales manager.

a. Sales transactions less than $25,000 are approved by the accounting system automatically (without involvement of the credit manager). Sales transactions higher than $25,000 require written approval by the credit manager.

b. All sales invoices are priced according to an authorized price list. Any exceptions to this pricing must be approved by the sales manager.

c. All shipping document are prenumbered and accounted for. Shipping document numbers are noted on all sales invoices.

d. A report of exceptions noting the failure of the invoice amount and the shipping amount to match is sent to the sales manager.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

24

Go to the SEC website ( www.sec.gov ) and identify a company that it has cited for revenue recognition problems. Describe the problem and identify the accounting principle that the company violated.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

25

What is inherent risk in the revenue process Explain when it would be high for an audit client. Explain when it could be low for an audit client.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

26

An auditor tests a company's policy of obtaining credit approval before shipping goods to customers in support of management's financial statement assertion of a. Valuation or allocation

B) Completeness

C) Existence or occurrence

D) Rights and obligations

B) Completeness

C) Existence or occurrence

D) Rights and obligations

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

27

Substantive tests of transactions. Two auditors are discussing the audit procedures for sales revenue. Stacy Mendoza believes that the best way to test sales revenue is to select a random sample of recorded sales and to trace these sales back through the system to the supporting documents, noting that all items billed were shipped and that the sales were invoiced at the correct prices. Takai Wong disagrees. He believes that it is better to gather evidence for the sales process by starting with the prenumbered shipping documents and then tracing them forward through the system to the invoice, noting the existence of control procedures and the correctness of the invoice processing.

a. If you follow Stacy's audit approach, identify the assertion supported by your evidence.

b. If you follow Takai's audit approach, identify the assertion supported by your evidence.

c. Which auditor is correct

a. If you follow Stacy's audit approach, identify the assertion supported by your evidence.

b. If you follow Takai's audit approach, identify the assertion supported by your evidence.

c. Which auditor is correct

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

28

Prepare the journal entries to record the transactions in the revenue process. Identify the balance sheet and income statements accounts included in the process.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

29

What is control risk

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

30

Which of the following internal controls would most likely reduce write-offs of uncollectible accounts receivable a. Employees responsible for authorizing sales and charge-offs of uncollectible accounts receivable are denied access to cash.

B) Shipping documents and sales invoices are matched by an employee who does not have the authority to charge off uncollectible accounts receivable.

C) Employees involved in the credit-granting function are separated from the sales function.

D) Accounts receivable master file records are reconciled to the control account by an employee who is not involved in the credit-granting function.

B) Shipping documents and sales invoices are matched by an employee who does not have the authority to charge off uncollectible accounts receivable.

C) Employees involved in the credit-granting function are separated from the sales function.

D) Accounts receivable master file records are reconciled to the control account by an employee who is not involved in the credit-granting function.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

31

Cutoff tests. While performing a sales cutoff test for your audit client, you review all shipping documents for five days before and five days after year-end. All sales are on credit and are sent FOB shipping point. Cost of goods sold is 75% of sales revenue. You are using the shipping log for the ten-day time period of the test. Test results follow.

a. Identify by shipping number the sales that the company has recorded as sales revenue at December 31, 2010.

b. Identify by shipping number the sales that should have been recorded as sales revenue at December 31, 2010.

c. Prepare the adjusting entry needed to correct the sales revenue and inventory at December 31, 2010.

d. Prepare the journal entries needed to record the sale represented by shipping document 450784, including the cash collection and the revenue recognition.

e. What accounting rule should the company use to recognize revenue

f. How is the company currently recognizing revenue

g. What questions should you ask the client to clarify the evidence you have gathered during this audit test

a. Identify by shipping number the sales that the company has recorded as sales revenue at December 31, 2010.

b. Identify by shipping number the sales that should have been recorded as sales revenue at December 31, 2010.

c. Prepare the adjusting entry needed to correct the sales revenue and inventory at December 31, 2010.

d. Prepare the journal entries needed to record the sale represented by shipping document 450784, including the cash collection and the revenue recognition.

e. What accounting rule should the company use to recognize revenue

f. How is the company currently recognizing revenue

g. What questions should you ask the client to clarify the evidence you have gathered during this audit test

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

32

Why is the revenue process important to the overall audit process

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

33

What is the auditor's responsibility for internal controls

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

34

A manufacturing company received a substantial sales return in the last month of the year, but the credit memorandum for the return was not prepared until after the auditors had completed the field work. The returned merchandise was included in the physical inventory. What control should have prevented the misstatement a. Aged trial balance of accounts receivable is prepared.

B) Credit memoranda are prenumbered and all numbers are accounted for.

C) A reconciliation of the trial balance of customer's accounts with the general ledger control is prepared periodically.

D) Receiving reports are prepared for all materials received and such reports are accounted for on a regular basis.

B) Credit memoranda are prenumbered and all numbers are accounted for.

C) A reconciliation of the trial balance of customer's accounts with the general ledger control is prepared periodically.

D) Receiving reports are prepared for all materials received and such reports are accounted for on a regular basis.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

35

Analytical procedures. You have been asked to audit the revenue from membership fees for the Orange County Master Gardeners Club. Your spouse is a member of the club.

a. What questions would you ask the club treasurer to verify the revenue

b. Let's assume that we have the following information: the club had approximately 200 members at the end of last year. Each year the club loses 15% of its members and gains 20% in new members. The dues are $50 per year, but members over 65 have a life-time membership where they do not pay dues. Approximately 20% of our membership is over 65 at any time. Describe some analytical procedures that you might use to determine that the membership revenue reported on the club's financial statements is not materially misstated.

c. Assume that membership revenue reported by the treasurer is $6,000. What would you conclude about the revenue

a. What questions would you ask the club treasurer to verify the revenue

b. Let's assume that we have the following information: the club had approximately 200 members at the end of last year. Each year the club loses 15% of its members and gains 20% in new members. The dues are $50 per year, but members over 65 have a life-time membership where they do not pay dues. Approximately 20% of our membership is over 65 at any time. Describe some analytical procedures that you might use to determine that the membership revenue reported on the club's financial statements is not materially misstated.

c. Assume that membership revenue reported by the treasurer is $6,000. What would you conclude about the revenue

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

36

Describe the business process approach to auditing. Why is it useful

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

37

When does the auditor test internal controls

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

38

The sales manager credited a salesperson, Jack Smith, with sales that were actually "house account" sales. Later Smith divided his excess sales commissions with the sales manager. What control should have prevented the misstatement a. The summary sales entries are checked periodically by persons independent of sales functions.

B) Sales orders are reviewed and approved by persons independent of the sales department.

C) The internal auditor compares the sales commission statements with the cash disbursements records.

D) Sales orders are prenumbered, and all are accounted for.

B) Sales orders are reviewed and approved by persons independent of the sales department.

C) The internal auditor compares the sales commission statements with the cash disbursements records.

D) Sales orders are prenumbered, and all are accounted for.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

39

Sales cutoff tests. Sales cutoff tests are performed to determine that sales are recorded in the correct time period according to the revenue recognition rules of the applicable financial reporting framework.

a. What is the revenue recognition rule for recording revenue when your audit client sells a product that it ships to the customer

b. What is the accounting rule for recognizing revenue when your client performs a service such as one a dentist could perform

c. How would you perform cutoff tests for a product that is shipped to the customer if your primary audit concern is gathering evidence to support the existence of the sales What conditions could be present in an audit client resulting in a risk that sales recorded at year-end do not exist

d. How would you perform cutoff tests for a service that your client performs (for example, a dentist's office) if your primary audit concern is completeness of sales

e. What conditions could be present in an audit client leading to a risk that sales recorded at year-end are incomplete

a. What is the revenue recognition rule for recording revenue when your audit client sells a product that it ships to the customer

b. What is the accounting rule for recognizing revenue when your client performs a service such as one a dentist could perform

c. How would you perform cutoff tests for a product that is shipped to the customer if your primary audit concern is gathering evidence to support the existence of the sales What conditions could be present in an audit client resulting in a risk that sales recorded at year-end do not exist

d. How would you perform cutoff tests for a service that your client performs (for example, a dentist's office) if your primary audit concern is completeness of sales

e. What conditions could be present in an audit client leading to a risk that sales recorded at year-end are incomplete

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

40

What is the auditor's responsibility in gathering evidence for the balance sheet and income statement accounts in the revenue process

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

41

How is audit testing linked to management's assertions

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

42

A sales invoice for $5,200 was computed correctly, but, by mistake, was entered as $2,500 to the sales journal and to the accounts receivable master file. The customer remitted only $2,500, the amount on his monthly statement. What control should have prevented the misstatement a. Prelisting and predetermined totals are used to control posting.

B) Sales invoice numbers, prices, discounts, extensions, and footing are independently checked.

C) The customer's monthly statements are verified and mailed by a responsible person other than the bookkeeper who prepared them.

D) Unauthorized remittance deductions made by customers or other matters in dispute are investigated promptly by a person independent of the accounts receivable function.

B) Sales invoice numbers, prices, discounts, extensions, and footing are independently checked.

C) The customer's monthly statements are verified and mailed by a responsible person other than the bookkeeper who prepared them.

D) Unauthorized remittance deductions made by customers or other matters in dispute are investigated promptly by a person independent of the accounts receivable function.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

43

Substantive test of balances. Refer to Appendix A for five replies from customers of BCS Inc. in response to the receivables confirmation conducted by Stuart Cram, the BCS auditor and a copy of two letters for which replies have not yet been received.

a. For each reply, explain what you think has happened, how you would verify your explanation, and whether the reply represents a misstatement in the BCS accounts. If so, prepare the adjusting entry.

b. For the two nonreplies, explain what other method the auditor could use to obtain some assurance on the balances involved.

a. For each reply, explain what you think has happened, how you would verify your explanation, and whether the reply represents a misstatement in the BCS accounts. If so, prepare the adjusting entry.

b. For the two nonreplies, explain what other method the auditor could use to obtain some assurance on the balances involved.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

44

How does the auditor's responsibility for gathering evidence differ between the balance sheet and income statement accounts

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

45

What are dual-purpose tests How does an auditor use them

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

46

Copies of sales invoices show different unit prices for apparently identical items. What control should have prevented the misstatement a. All sales invoices are checked as to all details after their preparation.

B) Differences reported by customers are satisfactorily investigated.

C) Statistical sales data are compiled and reconciled with recorded sales.

D) All sales invoices are compared with the customer's purchase orders.

B) Differences reported by customers are satisfactorily investigated.

C) Statistical sales data are compiled and reconciled with recorded sales.

D) All sales invoices are compared with the customer's purchase orders.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

47

Evaluating the allowance for doubtful accounts. See Appendix B for the aged receivables trial balance for BCS. Review it and explain what the information in each column represents.

a. Use this information to calculate a bad debt provision for BCS at December 31, 2010 Last year BCS used the following percentages to calculate the bad debt provision: current accounts, .05%; 30 day accounts, 2%; 60 day accounts, 10%; 90 day accounts, 40%. First calculate the allowance using the percentages applicable in the previous year. Then, if you determine that actual write-offs last year were $20,000 more than the provision and that the economic conditions for BCS customers has worsened in the current year, explain how you could adjust the allowance.

b. Why is it necessary for BCS to estimate bad debt expense at year-end What accounting principle does BCS violate if it does not estimate bad debt

a. Use this information to calculate a bad debt provision for BCS at December 31, 2010 Last year BCS used the following percentages to calculate the bad debt provision: current accounts, .05%; 30 day accounts, 2%; 60 day accounts, 10%; 90 day accounts, 40%. First calculate the allowance using the percentages applicable in the previous year. Then, if you determine that actual write-offs last year were $20,000 more than the provision and that the economic conditions for BCS customers has worsened in the current year, explain how you could adjust the allowance.

b. Why is it necessary for BCS to estimate bad debt expense at year-end What accounting principle does BCS violate if it does not estimate bad debt

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

48

Identify the most important document in the revenue process and explain why it is important.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

49

What are substantive tests of transactions

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

50

The following sales procedures were encountered during the annual audit of Marvel Wholesale Distributing Company. Use this information to answer questions 38, 39, and 40. Customer orders are received by the sales order department. A clerk computes the approximate dollar amount of the order and sends it to the credit department for approval. Credit approval is stamped on the order and sent to the accounting department. A computer is then used to generate two copies of a sales invoice. The order is filed in the customer order file.

The customer copy of the sales invoice is routed through the warehouse, and the shipping department has authority for the respective departments to release and ship the merchandise. Shipping department personnel pack the order and manually prepare a three-copy bill of lading: the original copy is mailed to the customer, the second copy is sent with shipment, and then the other is filed in sequence in the bill of lading file. The sales invoice shipping copy is sent to the accounting department with any changes resulting from lack of available merchandise.