Deck 4: Consolidated Financial Statements and Outside Ownership

Full screen (f)

Question

Question

Question

On January 1, Patterson Corporation acquired 80 percent of the 100,000 outstanding voting shares of Soriano, Inc., in exchange for $31.25 per share cash. The remaining 20 percent of Soriano's shares continued to trade for $30.00 both before and after Patterson's acquisition.

At January 1, Soriano's book and fair values were as follows:

In addition, Patterson assigned a $600,000 value to certain unpatented technologies recently developed by Soriano. These technologies were estimated to have a 3-year remaining life.

During the year, Soriano paid a $30,000 dividend to its shareholders. The companies reported the following revenues and expenses from their separate operations for the year ending December 31.

a. What total value should Patterson assign to its Soriano acquisition in its January 1 consolidated balance sheet

b. What valuation principle should Patterson use to report each of Soriano's identifiable assets and liabilities in its January 1 consolidated balance sheet

c. For years subsequent to acquisition, how will Soriano's identifiable assets and liabilities be valued in Patterson's consolidated reports

d. How much goodwill resulted from Patterson's acquisition of Soriano

e. What is the consolidated net income for the year and what amounts are allocated to thecontrolling and noncontrolling interests

f. What is the noncontrolling interest amount reported in the December 31 consolidated balance sheet

g. Assume instead that, based on its share prices, Soriano's January 1 total fair value was assessed at $2,250,000. How would the reported amounts for Soriano's net assets change on Patterson's acquisition-date consolidated balance sheet

At January 1, Soriano's book and fair values were as follows:

In addition, Patterson assigned a $600,000 value to certain unpatented technologies recently developed by Soriano. These technologies were estimated to have a 3-year remaining life.

During the year, Soriano paid a $30,000 dividend to its shareholders. The companies reported the following revenues and expenses from their separate operations for the year ending December 31.

a. What total value should Patterson assign to its Soriano acquisition in its January 1 consolidated balance sheet

b. What valuation principle should Patterson use to report each of Soriano's identifiable assets and liabilities in its January 1 consolidated balance sheet

c. For years subsequent to acquisition, how will Soriano's identifiable assets and liabilities be valued in Patterson's consolidated reports

d. How much goodwill resulted from Patterson's acquisition of Soriano

e. What is the consolidated net income for the year and what amounts are allocated to thecontrolling and noncontrolling interests

f. What is the noncontrolling interest amount reported in the December 31 consolidated balance sheet

g. Assume instead that, based on its share prices, Soriano's January 1 total fair value was assessed at $2,250,000. How would the reported amounts for Soriano's net assets change on Patterson's acquisition-date consolidated balance sheet

Question

On July 1, 2013, Truman Company acquired a 70 percent interest in Atlanta Company in exchange for consideration of $720,000 in cash and equity securities. The remaining 30 percent of Atlanta's shares traded closely near an average price that totaled $290,000 both before and after Truman's acquisition.

In reviewing its acquisition, Truman assigned a $100,000 fair value to a patent recently developed by Atlanta, even though it was not recorded within the financial records of the subsidiary. This patent is anticipated to have a remaining life of five years.

The following financial information is available for these two companies for 2013. In addition, the subsidiary's income was earned uniformly throughout the year. Subsidiary dividend payments were made quarterly.

Answer each of the following:

a. How did Truman allocate Atlanta's acquisition-date fair value to the various assets acquired and liabilities assumed in the combination

b. How did Truman allocate the goodwill from the acquisition across the controlling and noncontrolling interests

c. How did Truman derive the Investment in Atlanta account balance at the end of 2013

d. Prepare a worksheet to consolidate the financial statements of these two companies as of December 31, 2013.

In reviewing its acquisition, Truman assigned a $100,000 fair value to a patent recently developed by Atlanta, even though it was not recorded within the financial records of the subsidiary. This patent is anticipated to have a remaining life of five years.

The following financial information is available for these two companies for 2013. In addition, the subsidiary's income was earned uniformly throughout the year. Subsidiary dividend payments were made quarterly.

Answer each of the following:

a. How did Truman allocate Atlanta's acquisition-date fair value to the various assets acquired and liabilities assumed in the combination

b. How did Truman allocate the goodwill from the acquisition across the controlling and noncontrolling interests

c. How did Truman derive the Investment in Atlanta account balance at the end of 2013

d. Prepare a worksheet to consolidate the financial statements of these two companies as of December 31, 2013.

Question

Question

Question

On January 1, 2012, Palka, Inc., acquired 70 percent of the outstanding shares of Sellinger Company for $1,141,000 in cash. The price paid was proportionate to Sellinger's total fair value, although at the acquisition date, Sellinger had a total book value of $1,380,000. All assets acquired and liabilities assumed had fair values equal to book values except for a patent (six-year remaining life) that was undervalued on Sellinger's accounting records by $240,000.

On January 1, 2013, Palka acquired an additional 25 percent common stock equity interest in Sellinger Company for $415,000 in cash. On its internal records, Palka uses the equity method to account for its shares of Sellinger.

During the two years following the acquisition, Sellinger reported the following net income and dividends:

a. Show Palka's journal entry to record its January 1, 2013, acquisition of an additional 25 percent ownership of Sellinger Company shares.

b. Prepare a schedule showing Palka's December 31, 2013, equity method balance for its Investment in Sellinger account.

On January 1, 2013, Palka acquired an additional 25 percent common stock equity interest in Sellinger Company for $415,000 in cash. On its internal records, Palka uses the equity method to account for its shares of Sellinger.

During the two years following the acquisition, Sellinger reported the following net income and dividends:

a. Show Palka's journal entry to record its January 1, 2013, acquisition of an additional 25 percent ownership of Sellinger Company shares.

b. Prepare a schedule showing Palka's December 31, 2013, equity method balance for its Investment in Sellinger account.

Question

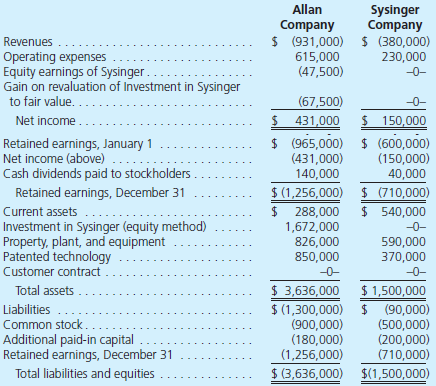

On January 1, 2012, Allan Company bought a 15 percent interest in Sysinger Company. The acquisition price of $184,500 reflected an assessment that all of Sysinger's accounts were fairly valued within the company's accounting records. During 2012, Sysinger reported net income of $100,000 and paid cash dividends of $30,000. Allan possessed the ability to influence significantly Sysinger's operations and, therefore, accounted for this investment using the equity method.

On January 1, 2013, Allan acquired an additional 80 percent interest in Sysinger and provided the following fair-value assessments of Sysinger's ownership components:

Also, as of January 1, 2013, Allan assessed a $400,000 value to an unrecorded customer contract recently negotiated by Sysinger. The customer contract is anticipated to have a remaining life of 4 years. Sysinger's other assets and liabilities were judged to have fair values equal to their book values. Allan elects to continue applying the equity method to this investment for internal reporting purposes.

At December 31, 2013, the following financial information is available for consolidation:

a. How should Allan allocate Sysinger's total acquisition-date fair value (January 1, 2013) to the assets acquired and liabilities assumed for consolidation purposes

b. Show how the following amounts on Allan's preconsolidation 2013 statements were derived:

• Equity in earnings of Sysinger.

• Gain on revaluation of Investment in Sysinger to fair value.

• Investment in Sysinger.

c. Prepare a worksheet to consolidate the financial statements of these two companies as of December 31, 2013.

On January 1, 2013, Allan acquired an additional 80 percent interest in Sysinger and provided the following fair-value assessments of Sysinger's ownership components:

Also, as of January 1, 2013, Allan assessed a $400,000 value to an unrecorded customer contract recently negotiated by Sysinger. The customer contract is anticipated to have a remaining life of 4 years. Sysinger's other assets and liabilities were judged to have fair values equal to their book values. Allan elects to continue applying the equity method to this investment for internal reporting purposes.

At December 31, 2013, the following financial information is available for consolidation:

a. How should Allan allocate Sysinger's total acquisition-date fair value (January 1, 2013) to the assets acquired and liabilities assumed for consolidation purposes

b. Show how the following amounts on Allan's preconsolidation 2013 statements were derived:

• Equity in earnings of Sysinger.

• Gain on revaluation of Investment in Sysinger to fair value.

• Investment in Sysinger.

c. Prepare a worksheet to consolidate the financial statements of these two companies as of December 31, 2013.

Question

Question

Question

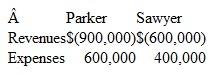

Parker, Inc.. acquires 70 percent of Sawyer Company for $420,000. The remaining.30 percent of Sawyer's outstanding shares continue to trade at a collective value of $174,000. On the acquisition date, Sawyer has the following accounts:

The buildings have a 10-year life. In addition, Sawyer holds a patent worth $140,000 that has a five-year life but is not recorded on its financial records. At the end of the year, the two companies report the following balances:

a. Assume that the acquisition took place on January 1. What figures would appear in a consolidated income statement for this year

b. Assume that the acquisition took place on April 1. Sawyer's revenues and expenses occurred uniformly throughout the year. What amounts would appear in a consolidated income statement for this year

The buildings have a 10-year life. In addition, Sawyer holds a patent worth $140,000 that has a five-year life but is not recorded on its financial records. At the end of the year, the two companies report the following balances:

a. Assume that the acquisition took place on January 1. What figures would appear in a consolidated income statement for this year

b. Assume that the acquisition took place on April 1. Sawyer's revenues and expenses occurred uniformly throughout the year. What amounts would appear in a consolidated income statement for this year

Question

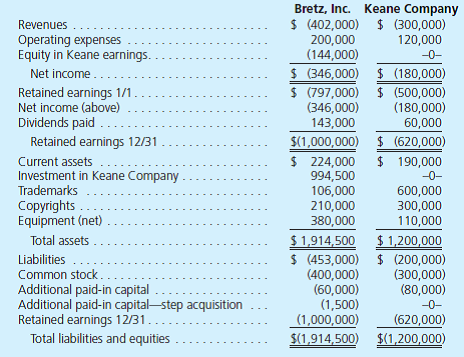

On January 1, 2012, Bretz, Inc., acquired 60 percent of the outstanding shares of Keane Company for $573,000 in cash. The price paid was proportionate to Keane's total fair value although at the date of acquisition, Keane had a total book value of $810,000. All assets acquired and liabilities assumed had fair values equal to book values except for a copyright (six-year remaining life) that was undervalued in Keane's accounting records by $120,000.

During 2012, Keane reported net income of $150,000 and paid cash dividends of $80,000. On January 1, 2013, Bretz bought an additional 30 percent interest in Keane for $300,000.

The following financial information is for these two companies for 2013. Keane issued no additional capital stock during either 2012 or 2013.

a. Show the journal entry Bretz made to record its January 1, 2013, acquisition of an additional 30 percent of Keane Company shares.

b. Prepare a schedule showing how Bretz determined the Investment in Keane Company balance as of December 31, 2013.

c. Prepare a consolidated worksheet for Bretz, Inc., and Keane Company for December 31, 2013.

During 2012, Keane reported net income of $150,000 and paid cash dividends of $80,000. On January 1, 2013, Bretz bought an additional 30 percent interest in Keane for $300,000.

The following financial information is for these two companies for 2013. Keane issued no additional capital stock during either 2012 or 2013.

a. Show the journal entry Bretz made to record its January 1, 2013, acquisition of an additional 30 percent of Keane Company shares.

b. Prepare a schedule showing how Bretz determined the Investment in Keane Company balance as of December 31, 2013.

c. Prepare a consolidated worksheet for Bretz, Inc., and Keane Company for December 31, 2013.

Question

On March 1, 2013, Nu-Auto Corporation announced its plan to acquire 90 percent of the outstanding 1,000,000 shares of Battery Tech Corporation's common stock in a business combination later in the year following regulatory approval. Nu-Auto will account for the transaction in accordance with ASC 805, Business Combinations.

On October 1, 2013, Nu-Auto acquired the 90 percent controlling interest in Battery Tech. On this date, Nu-Auto paid $60 million in cash and issued 1 million shares of Nu-Auto common stock to the selling shareholders of Battery Tech. Nu-Auto's share price was $20 on the announcement date and $27 on the acquisition date. Battery Tech's remaining 100,000 shares of common stock traded in the $108 to $112 per share range in the weeks before and after October 1, 2013.

The parties agreed that Nu-Auto would issue to the selling shareholders an additional 1 million shares contingent upon the achievement of certain performance goals during the first 18 months following the acquisition. The acquisition-date fair value of the contingent stock issue was estimated at $10 million.

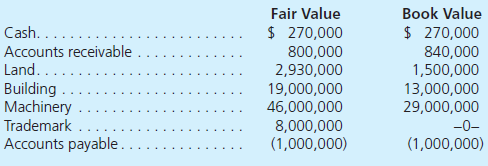

Battery Tech has a research and development (R D) project underway to develop a proprietary fast-charging battery technology. The technology has a fair value of $14 million. Nu-Auto considers this R D as in-process because it has not yet reached technological feasibility and additional R D is needed to bring the project to completion. No assets have been recorded in Battery Tech's financial records for the research and development costs related to its fast-charging battery technology.

Battery Tech's other assets and liabilities include the following:

Neither the receivables nor payables involve Nu-Auto.

Answer the following questions citing relevant support from the ASC and IFRS.

Under U.S. GAAP, what amount should Nu-Auto recognize as goodwill from the Battery Tech acquisition What alternative valuations are available for goodwill under IFRS

On October 1, 2013, Nu-Auto acquired the 90 percent controlling interest in Battery Tech. On this date, Nu-Auto paid $60 million in cash and issued 1 million shares of Nu-Auto common stock to the selling shareholders of Battery Tech. Nu-Auto's share price was $20 on the announcement date and $27 on the acquisition date. Battery Tech's remaining 100,000 shares of common stock traded in the $108 to $112 per share range in the weeks before and after October 1, 2013.

The parties agreed that Nu-Auto would issue to the selling shareholders an additional 1 million shares contingent upon the achievement of certain performance goals during the first 18 months following the acquisition. The acquisition-date fair value of the contingent stock issue was estimated at $10 million.

Battery Tech has a research and development (R D) project underway to develop a proprietary fast-charging battery technology. The technology has a fair value of $14 million. Nu-Auto considers this R D as in-process because it has not yet reached technological feasibility and additional R D is needed to bring the project to completion. No assets have been recorded in Battery Tech's financial records for the research and development costs related to its fast-charging battery technology.

Battery Tech's other assets and liabilities include the following:

Neither the receivables nor payables involve Nu-Auto.

Answer the following questions citing relevant support from the ASC and IFRS.

Under U.S. GAAP, what amount should Nu-Auto recognize as goodwill from the Battery Tech acquisition What alternative valuations are available for goodwill under IFRS

Question

Question

On January 1, Beckman, Inc., acquires 60 percent of the outstanding stock of Calvin for $36,000. Calvin (Co. has one recorded asset, a specialized production machine with a book value of $10,000 and no liabilities. The fair value of the machine is $50,000, and the remaining useful life is estimated to be 10 years. Any remaining excess fair value is attributable to an unrecorded process trade secret with an estimated future life of 4 years. Calvin's total acquisition-date fair value is $60,000.

At the end of the year, Calvin reports the following in its financial statements:

Determine the amounts that Beckman should report in its year-end consolidated financial statements for noncontrolling interest in subsidiary income, total noncontrolling interest, Calvin's machine (net of accumulated depreciation), and the process trade secret.

At the end of the year, Calvin reports the following in its financial statements:

Determine the amounts that Beckman should report in its year-end consolidated financial statements for noncontrolling interest in subsidiary income, total noncontrolling interest, Calvin's machine (net of accumulated depreciation), and the process trade secret.

Question

Question

Question

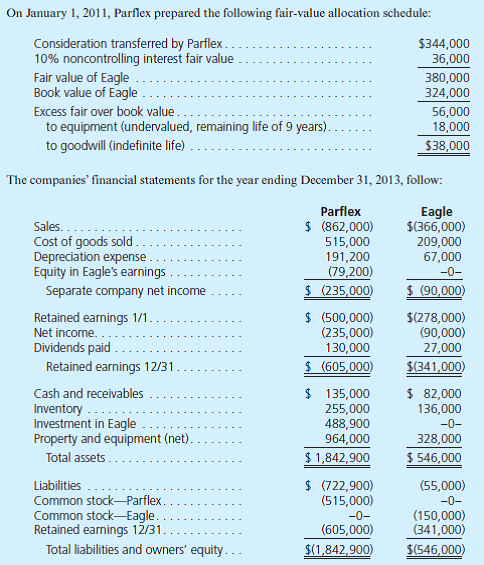

On January 1, 2011, Parflex Corporation exchanged $344,000 cash for 90% of Eagle Corporation's outstanding voting stock. Eagle's acquisition date balance sheet follows:

a. Compute the goodwill allocation to the controlling and noncontrolling interest.

b. Show how Parflex determined its "Investment in Eagle" account balance.

c. Determine the amounts that should appear on Parflex's December 31, 2013, consolidated statement of financial position and its 2013 consolidated income statement.

a. Compute the goodwill allocation to the controlling and noncontrolling interest.

b. Show how Parflex determined its "Investment in Eagle" account balance.

c. Determine the amounts that should appear on Parflex's December 31, 2013, consolidated statement of financial position and its 2013 consolidated income statement.

Question

Question

Question

On January 1, 2013, Morey, Inc., exchanged $178,000 for 25 percent of Amsterdam Corporation. Morey appropriately applied the equity method to this investment. At January 1, the book values of Amsterdam's assets and liabilities approximated their fair values.

On June 30, 2013, Morey paid $560,000 for an additional 70 percent of Amsterdam, thus increasing its overall ownership to 95 percent. The price paid for the 70 percent acquisition was proportionate to Amsterdam's total fair value. At June 30, the carrying amounts of Amsterdam's assets and liabilities approximated their fair values. Any remaining excess fair value was attributed to goodwill.

Amsterdam reports the following amounts at December 31, 2013 (credit balances shown in parentheses):

Amsterdam's revenue and expenses were distributed evenly throughout the year and no changes in Amsterdam's stock have occurred.

Using the acquisition method, compute the following:

a. The acquisition-date fair value of Amsterdam to be included in Morey's consolidated financial statements.

b. The revaluation gain (or loss) reported by Morey for its 25 percent investment in Amsterdam on June 30.

c. The amount of goodwill recognized by Morey on its December 31 balance sheet (assume no impairments have been recognized).

d. The noncontrolling interest amount reported by Morey on its

• June 30 consolidated balance sheet.

• December 31 consolidated balance sheet.

On June 30, 2013, Morey paid $560,000 for an additional 70 percent of Amsterdam, thus increasing its overall ownership to 95 percent. The price paid for the 70 percent acquisition was proportionate to Amsterdam's total fair value. At June 30, the carrying amounts of Amsterdam's assets and liabilities approximated their fair values. Any remaining excess fair value was attributed to goodwill.

Amsterdam reports the following amounts at December 31, 2013 (credit balances shown in parentheses):

Amsterdam's revenue and expenses were distributed evenly throughout the year and no changes in Amsterdam's stock have occurred.

Using the acquisition method, compute the following:

a. The acquisition-date fair value of Amsterdam to be included in Morey's consolidated financial statements.

b. The revaluation gain (or loss) reported by Morey for its 25 percent investment in Amsterdam on June 30.

c. The amount of goodwill recognized by Morey on its December 31 balance sheet (assume no impairments have been recognized).

d. The noncontrolling interest amount reported by Morey on its

• June 30 consolidated balance sheet.

• December 31 consolidated balance sheet.

Question

Question

Question

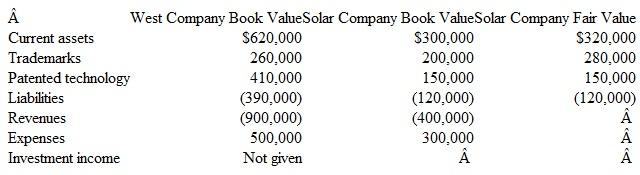

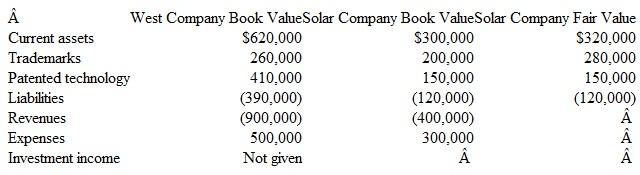

West Company acquired 60 percent of Solar Company for $300,000 when Solar's book value was $400,000. The newly comprised 40 percent noncontrolling interest had an assessed fair value of $200,000. Also at the acquisition date, Solar had a trademark (with a 10-year life) that was undervalued in the financial records by $60,000. Also, patented technology (with a 5-year life) was undervalued by $40,000. Two years later, the following figures are reported by these two companies (stockholders' equity accounts have been omitted):

What is the consolidated net income before allocation to the controlling and noncontrolling interests

A) $400,000.

B) $486,000.

C) $491,600.

D) $500,000.

What is the consolidated net income before allocation to the controlling and noncontrolling interests

A) $400,000.

B) $486,000.

C) $491,600.

D) $500,000.

Question

Question

On March 1, 2013, Nu-Auto Corporation announced its plan to acquire 90 percent of the outstanding 1,000,000 shares of Battery Tech Corporation's common stock in a business combination later in the year following regulatory approval. Nu-Auto will account for the transaction in accordance with ASC 805, Business Combinations.

On October 1, 2013, Nu-Auto acquired the 90 percent controlling interest in Battery Tech. On this date, Nu-Auto paid $60 million in cash and issued 1 million shares of Nu-Auto common stock to the selling shareholders of Battery Tech. Nu-Auto's share price was $20 on the announcement date and $27 on the acquisition date. Battery Tech's remaining 100,000 shares of common stock traded in the $108 to $112 per share range in the weeks before and after October 1, 2013.

The parties agreed that Nu-Auto would issue to the selling shareholders an additional 1 million shares contingent upon the achievement of certain performance goals during the first 18 months following the acquisition. The acquisition-date fair value of the contingent stock issue was estimated at $10 million.

Battery Tech has a research and development (R D) project underway to develop a proprietary fast-charging battery technology. The technology has a fair value of $14 million. Nu-Auto considers this R D as in-process because it has not yet reached technological feasibility and additional R D is needed to bring the project to completion. No assets have been recorded in Battery Tech's financial records for the research and development costs related to its fast-charging battery technology.

Battery Tech's other assets and liabilities include the following:

Neither the receivables nor payables involve Nu-Auto.

Answer the following questions citing relevant support from the ASC and IFRS.

What is the total consideration transferred by Nu-Auto to acquire its 90 percent controlling interest in Battery Tech

On October 1, 2013, Nu-Auto acquired the 90 percent controlling interest in Battery Tech. On this date, Nu-Auto paid $60 million in cash and issued 1 million shares of Nu-Auto common stock to the selling shareholders of Battery Tech. Nu-Auto's share price was $20 on the announcement date and $27 on the acquisition date. Battery Tech's remaining 100,000 shares of common stock traded in the $108 to $112 per share range in the weeks before and after October 1, 2013.

The parties agreed that Nu-Auto would issue to the selling shareholders an additional 1 million shares contingent upon the achievement of certain performance goals during the first 18 months following the acquisition. The acquisition-date fair value of the contingent stock issue was estimated at $10 million.

Battery Tech has a research and development (R D) project underway to develop a proprietary fast-charging battery technology. The technology has a fair value of $14 million. Nu-Auto considers this R D as in-process because it has not yet reached technological feasibility and additional R D is needed to bring the project to completion. No assets have been recorded in Battery Tech's financial records for the research and development costs related to its fast-charging battery technology.

Battery Tech's other assets and liabilities include the following:

Neither the receivables nor payables involve Nu-Auto.

Answer the following questions citing relevant support from the ASC and IFRS.

What is the total consideration transferred by Nu-Auto to acquire its 90 percent controlling interest in Battery Tech

Question

Question

Note: Problems 1 through 37 assume the use of the acquisition method. Problems 38 through 40 assume the use of the purchase method.

Use the following information for Problems 12 through 14:

West Company acquired 60 percent of Solar Company for $300,000 when Solar's book value was $400,000. The newly comprised 40 percent noncontrolling interest had an assessed fair value of $200,000. Also at the acquisition date, Solar had a trademark (with a 10-year life) that was undervalued in the financial records by $60,000. Also, patented technology (with a 5-year life) was undervalued by $40,000. Two years later, the following figures are reported by these two companies (stockholders' equity accounts have been omitted):

Assuming Solar Company has paid no dividends, what are the noncontrolling interest's share of the subsidiary's income and the ending balance of the noncontrolling interest in the subsidiary

a. $26,000 and $230,000.

b. $28,800 and $252,000.

c. $34,400 and $240,800.

d. $40,000 and $252,000.

Use the following information for Problems 12 through 14:

West Company acquired 60 percent of Solar Company for $300,000 when Solar's book value was $400,000. The newly comprised 40 percent noncontrolling interest had an assessed fair value of $200,000. Also at the acquisition date, Solar had a trademark (with a 10-year life) that was undervalued in the financial records by $60,000. Also, patented technology (with a 5-year life) was undervalued by $40,000. Two years later, the following figures are reported by these two companies (stockholders' equity accounts have been omitted):

Assuming Solar Company has paid no dividends, what are the noncontrolling interest's share of the subsidiary's income and the ending balance of the noncontrolling interest in the subsidiary

a. $26,000 and $230,000.

b. $28,800 and $252,000.

c. $34,400 and $240,800.

d. $40,000 and $252,000.

Question

On January 1, 2011, Telconnect acquires 70 percent of Bandmor for $490,000 cash. The remaining 30 percent of Bandmor's shares continued to trade at a total value of $210,000. The new subsidiary reported common stock of $300,000 on that date, with retained earnings of $180,000. A patent was undervalued in the company's financial records by $30,000. This patent had a 5-year remaining life. Goodwill of $190,000 was recognized and allocated proportionately to the controlling and noncontrolling interests. Bandmor earns income and pays cash dividends as follows:

On December 31, 2013, Telconnect owes $22,000 to Bandmor.

a. If Telconnect has applied the equity method, what consolidation entries are needed as of December 31, 2013

b. If Telconnect has applied the initial value method, what Entry *C is needed for a 2013 consolidation

c. If Telconnect has applied the partial equity method, what Entry *C is needed for a 2013 consolidation

d. What noncontrolling interest balances will appear in consolidated financial statements for 2013

On December 31, 2013, Telconnect owes $22,000 to Bandmor.

a. If Telconnect has applied the equity method, what consolidation entries are needed as of December 31, 2013

b. If Telconnect has applied the initial value method, what Entry *C is needed for a 2013 consolidation

c. If Telconnect has applied the partial equity method, what Entry *C is needed for a 2013 consolidation

d. What noncontrolling interest balances will appear in consolidated financial statements for 2013

Question

Question

Question

West Company acquired 60 percent of Solar Company for $300,000 when Solar's book value was $400,000. The newly comprised 40 percent noncontrolling interest had an assessed fair value of $200,000. Also at the acquisition date, Solar had a trademark (with a 10-year life) that was undervalued in the financial records by $60,000. Also, patented technology (with a 5-year life) was undervalued by $40,000. Two years later, the following figures are reported by these two companies (stockholders' equity accounts have been omitted):

What is the consolidated trademarks balance

A) $508,000.

B) $514,000.

C) $520,000.

D) $540,000.

What is the consolidated trademarks balance

A) $508,000.

B) $514,000.

C) $520,000.

D) $540,000.

Question

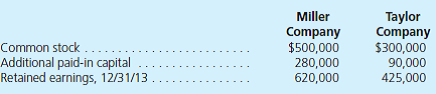

Miller Company acquired an 80 percent interest in Taylor Company on January 1, 2011. Miller paid $664,000 in cash to the owners of Taylor to acquire these shares. In addition, the remaining 20 percent of Taylor shares continued to trade at a total value of $166,000 both before and after Miller's acquisition.

On January 1, 2011, Taylor reported a book value of $600,000 (Common Stock = $300,000; Additional Paid-In Capital = $90,000; Retained Earnings = $210,000). Several of Taylor's buildings that had a remaining life of 20 years were undervalued by a total of $80,000.

During the next three years, Taylor reported the following figures:

Determine the appropriate answers for each of the following questions:

a. What amount of excess depreciation expense should be recognized in the consolidated financial statements for the initial years following this acquisition

b. If a consolidated balance sheet is prepared as of January 1, 2011, what amount of goodwill should be recognized

c. If a consolidation worksheet is prepared as of January 1, 2011, what Entry S and Entry A should be included

d. On the separate financial records of the parent company, what amount of investment income would be reported for 2011 under each of the following accounting methods

(1) The equity method.

(2) The partial equity method.

(3) The initial value method.

e. On the parent company's separate financial records, what would be the December 31, 2013, balance for the Investment in Taylor Company account under each of the following accounting methods

(1) The equity method.

(2) The partial equity method.

(3) The initial value method.

f. As of December 31, 2012, Miller's Buildings account on its separate records has a balance of $800,000 and Taylor has a similar account with a $300,000 balance. What is the consolidated balance for the Buildings account

g. What is the balance of consolidated goodwill as of December 31, 2013

h. Assume that the parent company has been applying the equity method to this investment. On December 31, 2013, the separate financial statements for the two companies present the following information:

What will be the consolidated balance of each of these accounts

On January 1, 2011, Taylor reported a book value of $600,000 (Common Stock = $300,000; Additional Paid-In Capital = $90,000; Retained Earnings = $210,000). Several of Taylor's buildings that had a remaining life of 20 years were undervalued by a total of $80,000.

During the next three years, Taylor reported the following figures:

Determine the appropriate answers for each of the following questions:

a. What amount of excess depreciation expense should be recognized in the consolidated financial statements for the initial years following this acquisition

b. If a consolidated balance sheet is prepared as of January 1, 2011, what amount of goodwill should be recognized

c. If a consolidation worksheet is prepared as of January 1, 2011, what Entry S and Entry A should be included

d. On the separate financial records of the parent company, what amount of investment income would be reported for 2011 under each of the following accounting methods

(1) The equity method.

(2) The partial equity method.

(3) The initial value method.

e. On the parent company's separate financial records, what would be the December 31, 2013, balance for the Investment in Taylor Company account under each of the following accounting methods

(1) The equity method.

(2) The partial equity method.

(3) The initial value method.

f. As of December 31, 2012, Miller's Buildings account on its separate records has a balance of $800,000 and Taylor has a similar account with a $300,000 balance. What is the consolidated balance for the Buildings account

g. What is the balance of consolidated goodwill as of December 31, 2013

h. Assume that the parent company has been applying the equity method to this investment. On December 31, 2013, the separate financial statements for the two companies present the following information:

What will be the consolidated balance of each of these accounts

Question

Question

Question

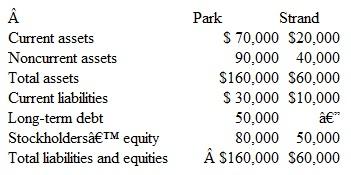

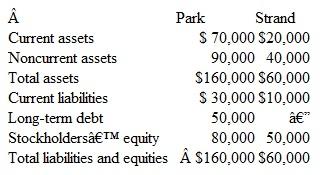

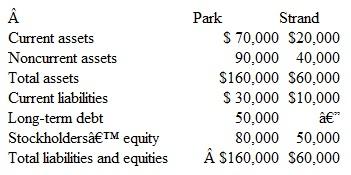

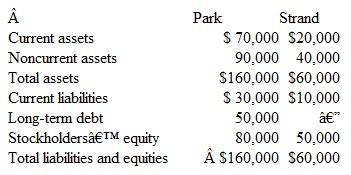

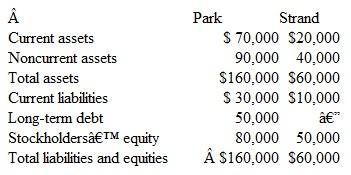

On January 1, Park Corporation and Strand Corporation had condensed balance sheets as follows:

On January 2, Park borrowed $60,000 and used the proceeds to obtain 80 percent of the outstanding common shares of Strand. The acquisition price was considered proportionate to Strand's total fair value. The $60,000 debt is payable in 10 equal annual principal payments, plus interest, beginning December 31. The excess fair value of the investment over the underlying book value of the acquired net assets is allocated to inventory (60 percent) and to goodwill (40 percent). On a consolidated balance sheet as of January 2, what should be the amount for each of the following

Current assets:

A) $105,000.

B $102,000.

C) $100,000.

D) $90,000.

On January 2, Park borrowed $60,000 and used the proceeds to obtain 80 percent of the outstanding common shares of Strand. The acquisition price was considered proportionate to Strand's total fair value. The $60,000 debt is payable in 10 equal annual principal payments, plus interest, beginning December 31. The excess fair value of the investment over the underlying book value of the acquired net assets is allocated to inventory (60 percent) and to goodwill (40 percent). On a consolidated balance sheet as of January 2, what should be the amount for each of the following

Current assets:

A) $105,000.

B $102,000.

C) $100,000.

D) $90,000.

Question

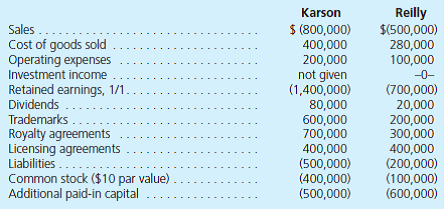

Following are several account balances taken from the records of Karson and Reilly as of December 31, 2013. A few asset accounts have been omitted here. All revenues, expenses, and dividends occurred evenly throughout the year. Annual tests have indicated no goodwill impairment.

On July 1, 2013, Karson acquired 80 percent of Reilly for $1,330,000 cash consideration. In addition, Karson agreed to pay additional cash to the former owners of Reilly if certain performance measures are achieved after three years. Karson assessed a $30,000 fair value for the contingent performance obligation as of the acquisition date and as of December 31, 2013.

On July 1, 2013, Reilly's assets and liabilities had book values equal to their fair value except for some trademarks (with 5-year remaining lives) that were undervalued by $150,000. Karson estimated Reilly's total fair value at $1,700,000 on July 1, 2013.

For a consolidation prepared at December 31, 2013, what balances would be reported for the following

On July 1, 2013, Karson acquired 80 percent of Reilly for $1,330,000 cash consideration. In addition, Karson agreed to pay additional cash to the former owners of Reilly if certain performance measures are achieved after three years. Karson assessed a $30,000 fair value for the contingent performance obligation as of the acquisition date and as of December 31, 2013.

On July 1, 2013, Reilly's assets and liabilities had book values equal to their fair value except for some trademarks (with 5-year remaining lives) that were undervalued by $150,000. Karson estimated Reilly's total fair value at $1,700,000 on July 1, 2013.

For a consolidation prepared at December 31, 2013, what balances would be reported for the following

Question

Question

Question

On January 1, Park Corporation and Strand Corporation had condensed balance sheets as follows:

On January 2, Park borrowed $60,000 and used the proceeds to obtain 80 percent of the outstanding common shares of Strand. The acquisition price was considered proportionate to Strand's total fair value. The $60,000 debt is payable in 10 equal annual principal payments, plus interest, beginning December 31. The excess fair value of the investment over the underlying book value of the acquired net assets is allocated to inventory (60 percent) and to goodwill (40 percent). On a consolidated balance sheet as of January 2, what should be the amount for each of the following

Noncurrent assets:

A) $130,000.

B) $134,000.

C) $138,000.

D) $140,000.

On January 2, Park borrowed $60,000 and used the proceeds to obtain 80 percent of the outstanding common shares of Strand. The acquisition price was considered proportionate to Strand's total fair value. The $60,000 debt is payable in 10 equal annual principal payments, plus interest, beginning December 31. The excess fair value of the investment over the underlying book value of the acquired net assets is allocated to inventory (60 percent) and to goodwill (40 percent). On a consolidated balance sheet as of January 2, what should be the amount for each of the following

Noncurrent assets:

A) $130,000.

B) $134,000.

C) $138,000.

D) $140,000.

Question

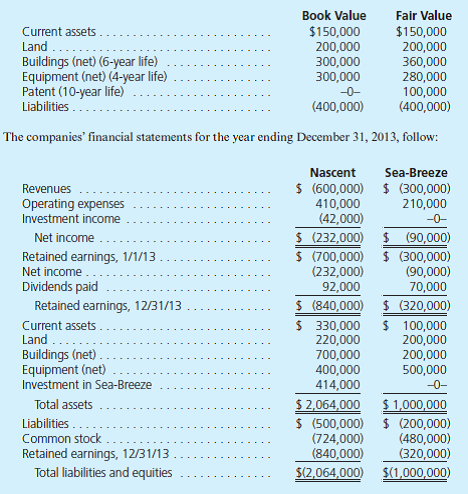

Nascent, Inc., acquires 60 percent of Sea-Breeze Corporation for $414,000 cash on January 1, 2010. The remaining 40 percent of the Sea-Breeze shares traded near a total value of $276,000 both before and after the acquisition date. On January 1, 2010, Sea-Breeze had the following assets and liabilities:

Answer the following questions:

a. How can the accountant determine that the parent has applied the initial value method

b. What is the annual excess amortization initially recognized in connection with this acquisition

c. If the parent had applied the equity method, what investment income would the parent have recorded in 2013

d. What is the parent's portion of consolidated retained earnings as of January 1, 2013

e. What is consolidated net income for 2013 and what amounts are attributable to the controlling and noncontrolling interests

f. Within consolidated statements at January 1, 2010, what balance is included for the subsidiary's Buildings account

g. What is the consolidated Buildings reported balance as of December 31, 2013

Answer the following questions:

a. How can the accountant determine that the parent has applied the initial value method

b. What is the annual excess amortization initially recognized in connection with this acquisition

c. If the parent had applied the equity method, what investment income would the parent have recorded in 2013

d. What is the parent's portion of consolidated retained earnings as of January 1, 2013

e. What is consolidated net income for 2013 and what amounts are attributable to the controlling and noncontrolling interests

f. Within consolidated statements at January 1, 2010, what balance is included for the subsidiary's Buildings account

g. What is the consolidated Buildings reported balance as of December 31, 2013

Question

On March 1, 2013, Nu-Auto Corporation announced its plan to acquire 90 percent of the outstanding 1,000,000 shares of Battery Tech Corporation's common stock in a business combination later in the year following regulatory approval. Nu-Auto will account for the transaction in accordance with ASC 805, Business Combinations.

On October 1, 2013, Nu-Auto acquired the 90 percent controlling interest in Battery Tech. On this date, Nu-Auto paid $60 million in cash and issued 1 million shares of Nu-Auto common stock to the selling shareholders of Battery Tech. Nu-Auto's share price was $20 on the announcement date and $27 on the acquisition date. Battery Tech's remaining 100,000 shares of common stock traded in the $108 to $112 per share range in the weeks before and after October 1, 2013.

The parties agreed that Nu-Auto would issue to the selling shareholders an additional 1 million shares contingent upon the achievement of certain performance goals during the first 18 months following the acquisition. The acquisition-date fair value of the contingent stock issue was estimated at $10 million.

Battery Tech has a research and development (R D) project underway to develop a proprietary fast-charging battery technology. The technology has a fair value of $14 million. Nu-Auto considers this R D as in-process because it has not yet reached technological feasibility and additional R D is needed to bring the project to completion. No assets have been recorded in Battery Tech's financial records for the research and development costs related to its fast-charging battery technology.

Battery Tech's other assets and liabilities include the following:

Neither the receivables nor payables involve Nu-Auto.

Answer the following questions citing relevant support from the ASC and IFRS.

What values should Nu-Auto assign to identifiable assets and liabilities as part of the acquisition accounting

On October 1, 2013, Nu-Auto acquired the 90 percent controlling interest in Battery Tech. On this date, Nu-Auto paid $60 million in cash and issued 1 million shares of Nu-Auto common stock to the selling shareholders of Battery Tech. Nu-Auto's share price was $20 on the announcement date and $27 on the acquisition date. Battery Tech's remaining 100,000 shares of common stock traded in the $108 to $112 per share range in the weeks before and after October 1, 2013.

The parties agreed that Nu-Auto would issue to the selling shareholders an additional 1 million shares contingent upon the achievement of certain performance goals during the first 18 months following the acquisition. The acquisition-date fair value of the contingent stock issue was estimated at $10 million.

Battery Tech has a research and development (R D) project underway to develop a proprietary fast-charging battery technology. The technology has a fair value of $14 million. Nu-Auto considers this R D as in-process because it has not yet reached technological feasibility and additional R D is needed to bring the project to completion. No assets have been recorded in Battery Tech's financial records for the research and development costs related to its fast-charging battery technology.

Battery Tech's other assets and liabilities include the following:

Neither the receivables nor payables involve Nu-Auto.

Answer the following questions citing relevant support from the ASC and IFRS.

What values should Nu-Auto assign to identifiable assets and liabilities as part of the acquisition accounting

Question

On January 1, 2011, Pride Co. purchased 90 percent of the outstanding voting shares of Star Inc. for $540,000 cash. The acquisition-date fair value of the noncontrolling interest was $60,000. At January 1, 2011, Star's net assets had a total carrying amount of $420,000. Equipment (8-year remaining life) was undervalued on Star's financial records by $80,000. Any remaining excess fair value over book value was attributed to a customer list developed by Star (4-year remaining life), but not recorded on its books. Star recorded income of $70,000 in 2011 and $80,000 in 2012. Each year since the acquisition, Star has paid a $20,000 dividend. At January 1, 2013, Pride's retained earnings show a $250,000 balance.

Selected account balances for the two companies from their separate operations were as follows:

What is consolidated net income for Pride and Star for 2013

a. $194,000.

b. $197,500.

c. $203,000.

d. $238,000.

Selected account balances for the two companies from their separate operations were as follows:

What is consolidated net income for Pride and Star for 2013

a. $194,000.

b. $197,500.

c. $203,000.

d. $238,000.

Question

On January 1, Park Corporation and Strand Corporation had condensed balance sheets as follows:

On January 2, Park borrowed $60,000 and used the proceeds to obtain 80 percent of the outstanding common shares of Strand. The acquisition price was considered proportionate to Strand's total fair value. The $60,000 debt is payable in 10 equal annual principal payments, plus interest, beginning December 31. The excess fair value of the investment over the underlying book value of the acquired net assets is allocated to inventory (60 percent) and to goodwill (40 percent). On a consolidated balance sheet as of January 2, what should be the amount for each of the following

Current liabilities:

A) $50,000.

B) $46,000.

C) $40,000.

D) $30,000.

On January 2, Park borrowed $60,000 and used the proceeds to obtain 80 percent of the outstanding common shares of Strand. The acquisition price was considered proportionate to Strand's total fair value. The $60,000 debt is payable in 10 equal annual principal payments, plus interest, beginning December 31. The excess fair value of the investment over the underlying book value of the acquired net assets is allocated to inventory (60 percent) and to goodwill (40 percent). On a consolidated balance sheet as of January 2, what should be the amount for each of the following

Current liabilities:

A) $50,000.

B) $46,000.

C) $40,000.

D) $30,000.

Question

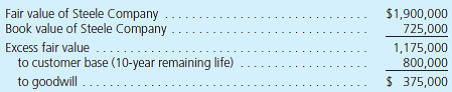

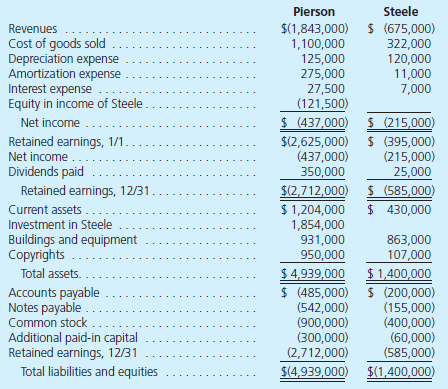

On January 1, 2012, Pierson Corporation exchanged $1,710,000 cash for 90 percent of the outstanding voting stock of Steele Company. The consideration transferred by Pierson provided a reasonable basis for assessing the total January 1, 2012, fair value of Steele Company. At the acquisition date, Steele reported the following owners' equity amounts in its balance sheet:

In determining its acquisition offer, Pierson noted that the values for Steele's recorded assets and liabilities approximated their fair values. Pierson also observed that Steele had developed internally a customer base with an assessed fair value of $800,000 that was not reflected on Steele's books. Pierson expected both cost and revenue synergies from the combination.

At the acquisition date, Pierson prepared the following fair-value allocation schedule:

At December 31, 2013, the two companies report the following balances:

a. Determine the consolidated balances for this business combination as of December 31, 2013.

b. If instead the noncontrolling interest's acquisition-date fair value is assessed at $152,500, what changes would be evident in the consolidated statements

In determining its acquisition offer, Pierson noted that the values for Steele's recorded assets and liabilities approximated their fair values. Pierson also observed that Steele had developed internally a customer base with an assessed fair value of $800,000 that was not reflected on Steele's books. Pierson expected both cost and revenue synergies from the combination.

At the acquisition date, Pierson prepared the following fair-value allocation schedule:

At December 31, 2013, the two companies report the following balances:

a. Determine the consolidated balances for this business combination as of December 31, 2013.

b. If instead the noncontrolling interest's acquisition-date fair value is assessed at $152,500, what changes would be evident in the consolidated statements

Question

Question

Question

On January 1, Park Corporation and Strand Corporation had condensed balance sheets as follows:

On January 2, Park borrowed $60,000 and used the proceeds to obtain 80 percent of the outstanding common shares of Strand. The acquisition price was considered proportionate to Strand's total fair value. The $60,000 debt is payable in 10 equal annual principal payments, plus interest, beginning December 31. The excess fair value of the investment over the underlying book value of the acquired net assets is allocated to inventory (60 percent) and to goodwill (40 percent). On a consolidated balance sheet as of January 2, what should be the amount for each of the following

Noncurrent liabilities:

a. $110,000.

b. $104,000.

c. $90,000.

d. $50,000.

On January 2, Park borrowed $60,000 and used the proceeds to obtain 80 percent of the outstanding common shares of Strand. The acquisition price was considered proportionate to Strand's total fair value. The $60,000 debt is payable in 10 equal annual principal payments, plus interest, beginning December 31. The excess fair value of the investment over the underlying book value of the acquired net assets is allocated to inventory (60 percent) and to goodwill (40 percent). On a consolidated balance sheet as of January 2, what should be the amount for each of the following

Noncurrent liabilities:

a. $110,000.

b. $104,000.

c. $90,000.

d. $50,000.

Question

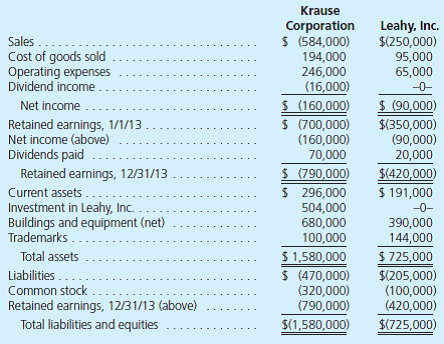

The Krause Corporation acquired 80 percent of the 100,000 outstanding voting shares of Leahy, Inc., for $6.30 per share on January 1, 2012. The remaining 20 percent of Leahy's shares also traded actively at $6.30 per share before and after Krause's acquisition. An appraisal made on that date determined that all book values appropriately reflected the fair values of Leahy's underlying accounts except that a building with a 5-year life was undervalued by $45,000 and a fully amortized trademark with an estimated 10-year remaining life had a $60,000 fair value.

At the acquisition date, Leahy reported common stock of $100,000 and a retained earnings balance of $280,000.

Following are the separate financial statements for the year ending December 31, 2013:

a. Prepare a worksheet to consolidate these two companies as of December 31, 2013.

b. Prepare a 2013 consolidated income statement for Krause and Leahy.

c. If instead the noncontrolling interest shares of Leahy had traded for $4.85 surrounding Krause's acquisition date, how would the consolidated statements change

At the acquisition date, Leahy reported common stock of $100,000 and a retained earnings balance of $280,000.

Following are the separate financial statements for the year ending December 31, 2013:

a. Prepare a worksheet to consolidate these two companies as of December 31, 2013.

b. Prepare a 2013 consolidated income statement for Krause and Leahy.

c. If instead the noncontrolling interest shares of Leahy had traded for $4.85 surrounding Krause's acquisition date, how would the consolidated statements change

Question

Question

On January 1, 2011, Pride Co. purchased 90 percent of the outstanding voting shares of Star Inc. for $540,000 cash. The acquisition-date fair value of the noncontrolling interest was $60,000. At January 1, 2011, Star's net assets had a total carrying amount of $420,000. Equipment (8-year remaining life) was undervalued on Star's financial records by $80,000. Any remaining excess fair value over book value was attributed to a customer list developed by Star (4-year remaining life), but not recorded on its books. Star recorded income of $70,000 in 2011 and $80,000 in 2012. Each year since the acquisition, Star has paid a $20,000 dividend. At January 1, 2013, Pride's retained earnings show a $250,000 balance.

Selected account balances for the two companies from their separate operations were as follows:

Assuming that Pride, in its internal records, accounts for its investment in Star using the equity method, what is Pride's share of consolidated retained earnings at January 1, 2013

A) $250,000.

B) $286,000.

C) $315,000.

D) $360,000.

Selected account balances for the two companies from their separate operations were as follows:

Assuming that Pride, in its internal records, accounts for its investment in Star using the equity method, what is Pride's share of consolidated retained earnings at January 1, 2013

A) $250,000.

B) $286,000.

C) $315,000.

D) $360,000.

Question

On January 1, Park Corporation and Strand Corporation had condensed balance sheets as follows:

On January 2, Park borrowed $60,000 and used the proceeds to obtain 80 percent of the outstanding common shares of Strand. The acquisition price was considered proportionate to Strand's total fair value. The $60,000 debt is payable in 10 equal annual principal payments, plus interest, beginning December 31. The excess fair value of the investment over the underlying book value of the acquired net assets is allocated to inventory (60 percent) and to goodwill (40 percent). On a consolidated balance sheet as of January 2, what should be the amount for each of the following

Stockholder:

A) $80,000.

B) $90,000.

C) $95,000.

D) $130,000

(AICPA adapted)

On January 2, Park borrowed $60,000 and used the proceeds to obtain 80 percent of the outstanding common shares of Strand. The acquisition price was considered proportionate to Strand's total fair value. The $60,000 debt is payable in 10 equal annual principal payments, plus interest, beginning December 31. The excess fair value of the investment over the underlying book value of the acquired net assets is allocated to inventory (60 percent) and to goodwill (40 percent). On a consolidated balance sheet as of January 2, what should be the amount for each of the following

Stockholder:

A) $80,000.

B) $90,000.

C) $95,000.

D) $130,000

(AICPA adapted)

Question

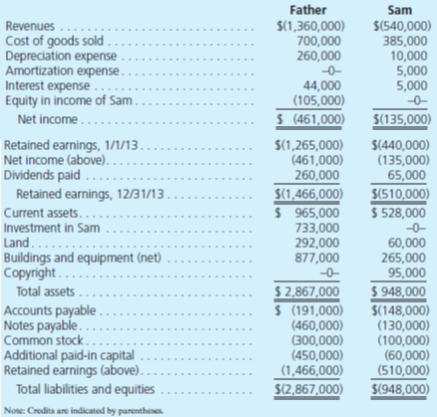

Father, Inc., buys 80 percent of the outstanding common stock of Sam Corporation on January 1, 2013, for $680,000 cash. At the acquisition date, Sam's total fair value, including the noncontrolling interest, was assessed at $850,000 although Sam's book value was only $600,000. Also, several individual items on Sam's financial records had fair values that differed from their book values as follows:

For internal reporting purposes, Father, Inc., employs the equity method to account for this investment.

The following account balances are for the year ending December 31, 2013, for both companies.

Using the acquisition method, determine consolidated balances for this business combination (through either individual computations or the use of a worksheet).

For internal reporting purposes, Father, Inc., employs the equity method to account for this investment.

The following account balances are for the year ending December 31, 2013, for both companies.

Using the acquisition method, determine consolidated balances for this business combination (through either individual computations or the use of a worksheet).

Question

Question

Question

Question

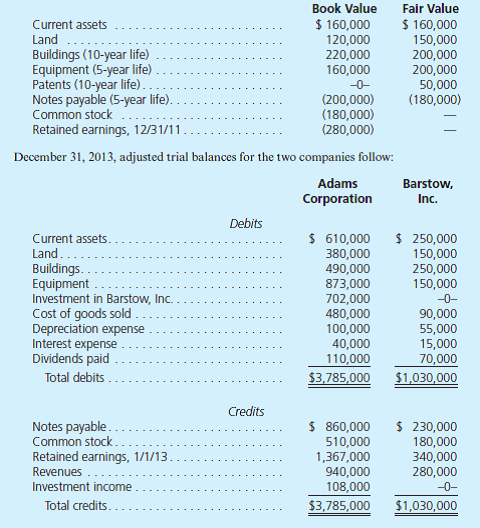

Adams Corporation acquired 90 percent of the outstanding voting shares of Barstow, Inc., on December 31, 2011. Adams paid a total of $603,000 in cash for these shares. The 10 percent noncontrolling interest shares traded on a daily basis at fair value of $67,000 both before and after Adams's acquisition. On December 31, 2011, Barstow had the following account balances:

a. Prepare schedules for acquisition-date fair-value allocations and amortizations for Adams's investment in Barstow.

b. Determine Adams's method of accounting for its investment in Barstow. Support your answer with a numerical explanation.

c. Without using a worksheet or consolidation entries, determine the balances to be reported as of December 31, 2013, for this business combination.

d. To verify the figures determined in requirement ( c ) , prepare a consolidation worksheet for Adams Corporation and Barstow, Inc., as of December 31, 2013.

a. Prepare schedules for acquisition-date fair-value allocations and amortizations for Adams's investment in Barstow.

b. Determine Adams's method of accounting for its investment in Barstow. Support your answer with a numerical explanation.

c. Without using a worksheet or consolidation entries, determine the balances to be reported as of December 31, 2013, for this business combination.

d. To verify the figures determined in requirement ( c ) , prepare a consolidation worksheet for Adams Corporation and Barstow, Inc., as of December 31, 2013.

Question

On March 1, 2013, Nu-Auto Corporation announced its plan to acquire 90 percent of the outstanding 1,000,000 shares of Battery Tech Corporation's common stock in a business combination later in the year following regulatory approval. Nu-Auto will account for the transaction in accordance with ASC 805, Business Combinations.

On October 1, 2013, Nu-Auto acquired the 90 percent controlling interest in Battery Tech. On this date, Nu-Auto paid $60 million in cash and issued 1 million shares of Nu-Auto common stock to the selling shareholders of Battery Tech. Nu-Auto's share price was $20 on the announcement date and $27 on the acquisition date. Battery Tech's remaining 100,000 shares of common stock traded in the $108 to $112 per share range in the weeks before and after October 1, 2013.

The parties agreed that Nu-Auto would issue to the selling shareholders an additional 1 million shares contingent upon the achievement of certain performance goals during the first 18 months following the acquisition. The acquisition-date fair value of the contingent stock issue was estimated at $10 million.

Battery Tech has a research and development (R D) project underway to develop a proprietary fast-charging battery technology. The technology has a fair value of $14 million. Nu-Auto considers this R D as in-process because it has not yet reached technological feasibility and additional R D is needed to bring the project to completion. No assets have been recorded in Battery Tech's financial records for the research and development costs related to its fast-charging battery technology.

Battery Tech's other assets and liabilities include the following:

Neither the receivables nor payables involve Nu-Auto.

Answer the following questions citing relevant support from the ASC and IFRS.

What is the acquisition-date value assigned to the 10 percent noncontrolling interest What are the potential noncontrolling interest valuation alternatives available under IFRS

On October 1, 2013, Nu-Auto acquired the 90 percent controlling interest in Battery Tech. On this date, Nu-Auto paid $60 million in cash and issued 1 million shares of Nu-Auto common stock to the selling shareholders of Battery Tech. Nu-Auto's share price was $20 on the announcement date and $27 on the acquisition date. Battery Tech's remaining 100,000 shares of common stock traded in the $108 to $112 per share range in the weeks before and after October 1, 2013.

The parties agreed that Nu-Auto would issue to the selling shareholders an additional 1 million shares contingent upon the achievement of certain performance goals during the first 18 months following the acquisition. The acquisition-date fair value of the contingent stock issue was estimated at $10 million.

Battery Tech has a research and development (R D) project underway to develop a proprietary fast-charging battery technology. The technology has a fair value of $14 million. Nu-Auto considers this R D as in-process because it has not yet reached technological feasibility and additional R D is needed to bring the project to completion. No assets have been recorded in Battery Tech's financial records for the research and development costs related to its fast-charging battery technology.

Battery Tech's other assets and liabilities include the following:

Neither the receivables nor payables involve Nu-Auto.

Answer the following questions citing relevant support from the ASC and IFRS.

What is the acquisition-date value assigned to the 10 percent noncontrolling interest What are the potential noncontrolling interest valuation alternatives available under IFRS

Question

Question

Question

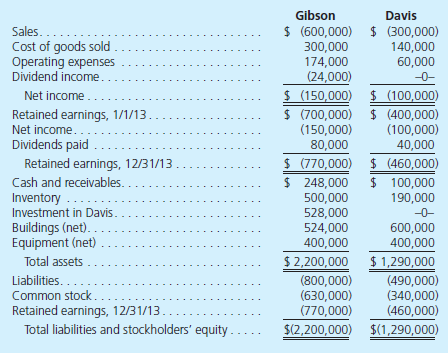

Following are the individual financial statements for Gibson and Davis for the year ending December 31, 2013:

Gibson acquired 60 percent of Davis on April 1, 2013, for $528,000. On that date, equipment owned by Davis (with a five-year remaining life) was overvalued by $30,000. Also on that date, the fair value of the 40 percent noncontrolling interest was $352,000. Davis earned income evenly during the year but paid the entire dividend on November 1, 2013.

a. Prepare a consolidated income statement for the year ending December 31, 2013.

b. Determine the consolidated balance for each of the following accounts as of December 31, 2013:

Gibson acquired 60 percent of Davis on April 1, 2013, for $528,000. On that date, equipment owned by Davis (with a five-year remaining life) was overvalued by $30,000. Also on that date, the fair value of the 40 percent noncontrolling interest was $352,000. Davis earned income evenly during the year but paid the entire dividend on November 1, 2013.

a. Prepare a consolidated income statement for the year ending December 31, 2013.

b. Determine the consolidated balance for each of the following accounts as of December 31, 2013:

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/61

Play

Full screen (f)

Deck 4: Consolidated Financial Statements and Outside Ownership

1

Jordan, Inc., holds 75 percent of the outstanding stock of Paxson Corporation. Paxson currently owes Jordan $400,000 for inventory acquired over the past few months. In preparing consolidated financial statements, what amount of this debt should be eliminated

A) -0-.

B) $100,000.

C) $300,000.

D) $400,000.

A) -0-.

B) $100,000.

C) $300,000.

D) $400,000.

The answer to this multiple choice question is "D", $400,000.

Eliminate 100% of intercompany transactions even if there is a non-controlling interest.

The journal entry to make this elimination is as follows:

Intercompany A/P $400,000

Intercompany A/R $400,000

Eliminate 100% of intercompany transactions even if there is a non-controlling interest.

The journal entry to make this elimination is as follows:

Intercompany A/P $400,000

Intercompany A/R $400,000

2

In question (8), how would the parent record the sales transaction

The sale of subsidiary shares by a parent company is accounted for differently depending on how many shares are sold. If only a small portion of shares are sold and the parent company still maintains control of the subsidiary, additional paid in capital (APIC) is credited and no gain or loss is recognized. The journal entry for this transaction is as follows:

Cash $Investment $

APIC $If a large portion of shares are sold and the parent company losses control of the subsidiary, a gain or loss is recognized. The journal entry for this transaction is as follows:Cash $

Investment $Gain on sale of shares $

Cash $Investment $

APIC $If a large portion of shares are sold and the parent company losses control of the subsidiary, a gain or loss is recognized. The journal entry for this transaction is as follows:Cash $

Investment $Gain on sale of shares $

3

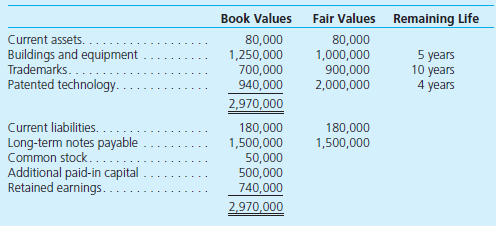

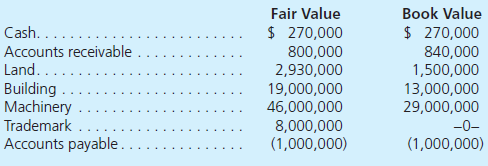

On January 1, Patterson Corporation acquired 80 percent of the 100,000 outstanding voting shares of Soriano, Inc., in exchange for $31.25 per share cash. The remaining 20 percent of Soriano's shares continued to trade for $30.00 both before and after Patterson's acquisition.

At January 1, Soriano's book and fair values were as follows:

In addition, Patterson assigned a $600,000 value to certain unpatented technologies recently developed by Soriano. These technologies were estimated to have a 3-year remaining life.

During the year, Soriano paid a $30,000 dividend to its shareholders. The companies reported the following revenues and expenses from their separate operations for the year ending December 31.

a. What total value should Patterson assign to its Soriano acquisition in its January 1 consolidated balance sheet

b. What valuation principle should Patterson use to report each of Soriano's identifiable assets and liabilities in its January 1 consolidated balance sheet

c. For years subsequent to acquisition, how will Soriano's identifiable assets and liabilities be valued in Patterson's consolidated reports

d. How much goodwill resulted from Patterson's acquisition of Soriano

e. What is the consolidated net income for the year and what amounts are allocated to thecontrolling and noncontrolling interests

f. What is the noncontrolling interest amount reported in the December 31 consolidated balance sheet

g. Assume instead that, based on its share prices, Soriano's January 1 total fair value was assessed at $2,250,000. How would the reported amounts for Soriano's net assets change on Patterson's acquisition-date consolidated balance sheet

At January 1, Soriano's book and fair values were as follows:

In addition, Patterson assigned a $600,000 value to certain unpatented technologies recently developed by Soriano. These technologies were estimated to have a 3-year remaining life.

During the year, Soriano paid a $30,000 dividend to its shareholders. The companies reported the following revenues and expenses from their separate operations for the year ending December 31.

a. What total value should Patterson assign to its Soriano acquisition in its January 1 consolidated balance sheet

b. What valuation principle should Patterson use to report each of Soriano's identifiable assets and liabilities in its January 1 consolidated balance sheet

c. For years subsequent to acquisition, how will Soriano's identifiable assets and liabilities be valued in Patterson's consolidated reports

d. How much goodwill resulted from Patterson's acquisition of Soriano

e. What is the consolidated net income for the year and what amounts are allocated to thecontrolling and noncontrolling interests

f. What is the noncontrolling interest amount reported in the December 31 consolidated balance sheet

g. Assume instead that, based on its share prices, Soriano's January 1 total fair value was assessed at $2,250,000. How would the reported amounts for Soriano's net assets change on Patterson's acquisition-date consolidated balance sheet

(a) The acquisition method denotes that Company P should assign the sum of the acquisition price and the noncontrolling interest for the acquisition. This is the amount Company P will report on the consolidated balance sheet. Both the acquisition price and noncontrolling interest need to be calculated. The acquisition price is $31.25 times 80% of 100,000 shares. Calculate the acquisition price as the amount of shares times the cost of each share:

Calculate the percentage of noncontrolling interest in the shares as 100% minus 80%:

Calculate the percentage of noncontrolling interest in the shares as 100% minus 80%:

Calculate the value of the noncontrolling interest as the amount of shares times the cost of each share:

Calculate the value of the noncontrolling interest as the amount of shares times the cost of each share:

Calculate the sum of the acquisition price and the noncontrolling interest:

Calculate the sum of the acquisition price and the noncontrolling interest:

Company P will report $3,100,000 as the value of the acquisition in Company S.

Company P will report $3,100,000 as the value of the acquisition in Company S.

(b) The acquisition method denotes that the fair value of all assets and liabilities at the time of acquisition will be reported. The fair values will be used on the consolidated financial statement.

(c) In subsequent years the parent company will continue to use the acquisition date fair value. Also any amortization and depreciation will be subtracted from the fair value.

(d) The goodwill will be calculated as the acquisition value minus the book value of the assets and the difference of fair value and book value. Calculate the book value of assets as the sum of assets minus liabilities that are not shareholder's equity:

The fair value and book value of current assets, current liabilities, and long-term notes payable are the same, so there will be no difference in value. Calculate the difference in fair value and book value for buildings and equipment, trademarks, and patented technology:

The fair value and book value of current assets, current liabilities, and long-term notes payable are the same, so there will be no difference in value. Calculate the difference in fair value and book value for buildings and equipment, trademarks, and patented technology:

Calculate the acquisition value minus the book value and the differences between fair value and book values:

Calculate the acquisition value minus the book value and the differences between fair value and book values:

The acquisition resulted in $200,000 in goodwill.

The acquisition resulted in $200,000 in goodwill.

(e) Consolidated net income will be the sum of revenues minus the sum of expenses and amortizations. The amortizations will be calculated as fair value minus book value divided by years remaining. Calculate the amortizations for buildings and equipment, trademarks, patented technology, and unpatented technology:

Calculate the sum of revenues minus the sum of expenses and amortizations:

Calculate the sum of revenues minus the sum of expenses and amortizations:

The consolidated net income for is $1,615,000 before interest allocations.

The consolidated net income for is $1,615,000 before interest allocations.

Company P's share of interest will be its own net income times its share of Company S' net income. Calculate Company P's net income as revenue minus expenses:

Calculate Company S' net income as revenue minus expenses and amortizations:

Calculate Company S' net income as revenue minus expenses and amortizations:

Calculate Company P's share of Company S' net income as the value times percent owned:

Calculate Company P's share of Company S' net income as the value times percent owned:

Calculate the sum of Company P's net income and their share of the interest in Company S:

Calculate the sum of Company P's net income and their share of the interest in Company S:

Company P's allocation of consolidated net income is $1,542,000.

Company P's allocation of consolidated net income is $1,542,000.

Calculate the noncontrolling interest's allocation of consolidated net income as the value of Company S' net income times percent owned:

The noncontrolling interest's allocation of consolidated net income is $73,000.

The noncontrolling interest's allocation of consolidated net income is $73,000.

(f) The investment balance for the noncontrolling interest at December 31 st is the initial fair value plus net income minus dividends paid. Calculate the fair value of the initial value as amount of shares times' price:

Calculate the noncontrolling interest share of dividends paid as the amount times percent owned:

Calculate the noncontrolling interest share of dividends paid as the amount times percent owned:

Calculate the sum of initial value and net income minus dividends paid:

Calculate the sum of initial value and net income minus dividends paid:

The noncontrolling investment balance in Company S is $667,000 at December 31 st on the consolidated balance sheet.

The noncontrolling investment balance in Company S is $667,000 at December 31 st on the consolidated balance sheet.

(g) The acquisition date fair value will still be given even if the fair value assessment changes. There will be no change to assets and liability values reported on the acquisition-date consolidated balance sheet.

Calculate the percentage of noncontrolling interest in the shares as 100% minus 80%: Calculate the value of the noncontrolling interest as the amount of shares times the cost of each share: Calculate the sum of the acquisition price and the noncontrolling interest: Company P will report $3,100,000 as the value of the acquisition in Company S.(b) The acquisition method denotes that the fair value of all assets and liabilities at the time of acquisition will be reported. The fair values will be used on the consolidated financial statement.

(c) In subsequent years the parent company will continue to use the acquisition date fair value. Also any amortization and depreciation will be subtracted from the fair value.

(d) The goodwill will be calculated as the acquisition value minus the book value of the assets and the difference of fair value and book value. Calculate the book value of assets as the sum of assets minus liabilities that are not shareholder's equity:

The fair value and book value of current assets, current liabilities, and long-term notes payable are the same, so there will be no difference in value. Calculate the difference in fair value and book value for buildings and equipment, trademarks, and patented technology: Calculate the acquisition value minus the book value and the differences between fair value and book values: The acquisition resulted in $200,000 in goodwill.(e) Consolidated net income will be the sum of revenues minus the sum of expenses and amortizations. The amortizations will be calculated as fair value minus book value divided by years remaining. Calculate the amortizations for buildings and equipment, trademarks, patented technology, and unpatented technology:

Calculate the sum of revenues minus the sum of expenses and amortizations: The consolidated net income for is $1,615,000 before interest allocations.Company P's share of interest will be its own net income times its share of Company S' net income. Calculate Company P's net income as revenue minus expenses:

Calculate Company S' net income as revenue minus expenses and amortizations: Calculate Company P's share of Company S' net income as the value times percent owned: Calculate the sum of Company P's net income and their share of the interest in Company S: Company P's allocation of consolidated net income is $1,542,000.Calculate the noncontrolling interest's allocation of consolidated net income as the value of Company S' net income times percent owned:

The noncontrolling interest's allocation of consolidated net income is $73,000.(f) The investment balance for the noncontrolling interest at December 31 st is the initial fair value plus net income minus dividends paid. Calculate the fair value of the initial value as amount of shares times' price:

Calculate the noncontrolling interest share of dividends paid as the amount times percent owned: Calculate the sum of initial value and net income minus dividends paid: The noncontrolling investment balance in Company S is $667,000 at December 31 st on the consolidated balance sheet.(g) The acquisition date fair value will still be given even if the fair value assessment changes. There will be no change to assets and liability values reported on the acquisition-date consolidated balance sheet.

4

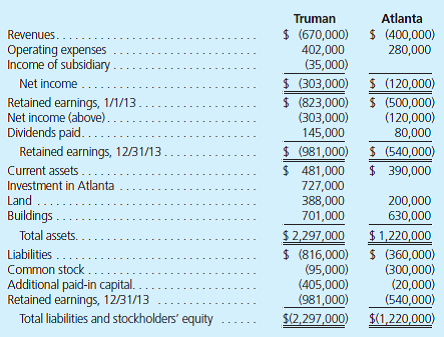

On July 1, 2013, Truman Company acquired a 70 percent interest in Atlanta Company in exchange for consideration of $720,000 in cash and equity securities. The remaining 30 percent of Atlanta's shares traded closely near an average price that totaled $290,000 both before and after Truman's acquisition.

In reviewing its acquisition, Truman assigned a $100,000 fair value to a patent recently developed by Atlanta, even though it was not recorded within the financial records of the subsidiary. This patent is anticipated to have a remaining life of five years.

The following financial information is available for these two companies for 2013. In addition, the subsidiary's income was earned uniformly throughout the year. Subsidiary dividend payments were made quarterly.

Answer each of the following:

a. How did Truman allocate Atlanta's acquisition-date fair value to the various assets acquired and liabilities assumed in the combination

b. How did Truman allocate the goodwill from the acquisition across the controlling and noncontrolling interests

c. How did Truman derive the Investment in Atlanta account balance at the end of 2013

d. Prepare a worksheet to consolidate the financial statements of these two companies as of December 31, 2013.