Deck 6: Process Costing

Full screen (f)

Question

Question

Question

Nonuniform Inputs, Weighted Average

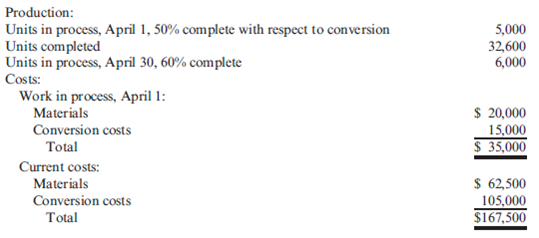

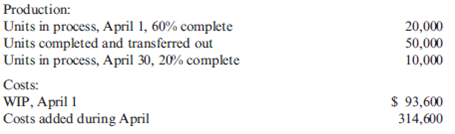

Integer Inc. had the following production and cost information for its fabrication department during April (materials are added at the beginning of the fabrication process):

Integer uses the weighted average method.

Required:

1. Prepare an equivalent units schedule.

2. Calculate the unit cost. (Note: Round answers to two decimal places).

3. Calculate the cost of units transferred out and the cost of EWIP.

Integer Inc. had the following production and cost information for its fabrication department during April (materials are added at the beginning of the fabrication process):

Integer uses the weighted average method.

Required:

1. Prepare an equivalent units schedule.

2. Calculate the unit cost. (Note: Round answers to two decimal places).

3. Calculate the cost of units transferred out and the cost of EWIP.

Question

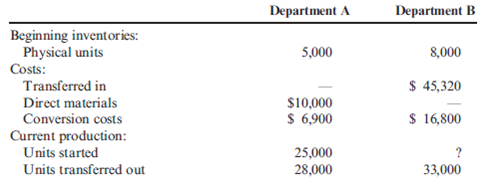

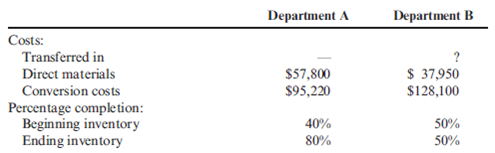

Transferred-In Cost

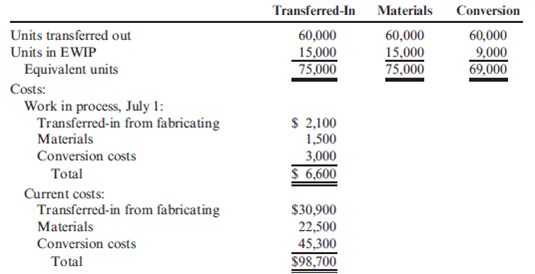

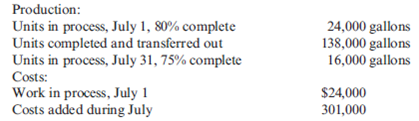

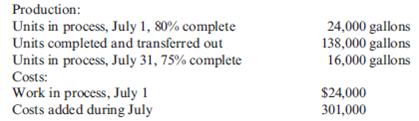

Golding's finishing department had the following data for July:

Required:

1. Calculate unit costs for the following categories: transferred-in, materials, and conversion.

2. Calculate total unit cost.

Golding's finishing department had the following data for July:

Required:

1. Calculate unit costs for the following categories: transferred-in, materials, and conversion.

2. Calculate total unit cost.

Question

Process Costing versus Alternative Costing Methods, Impact on Resource Allocation Decision

Golding Manufacturing, a division of Farnsworth Sporting Inc., produces two different models of bows and eight models of knives. The bow-manufacturing process involves the production of two major subassemblies: the limbs and the handles. The limbs pass through four sequential processes before reaching final assembly: layup, molding, fabricating, and finishing. In the layup department, limbs are created by laminating layers of wood. In the molding department, the limbs are heat-treated, under pressure, to form strong resilient limbs. In the fabricating department, any protruding glue or other processing residue is removed. Finally, in the finishing department, the limbs are cleaned with acetone, dried, and sprayed with the final finishes.

The handles pass through two processes before reaching final assembly: pattern and finishing. In the pattern department, blocks of wood are fed into a machine that is set to shape the handles. Different patterns are possible, depending on the machine's setting. After coming out of the machine, the handles are cleaned and smoothed. They then pass to the finishing department, where they are sprayed with the final finishes. In final assembly, the limbs and handles are assembled into different models using purchased parts such as pulley assemblies, weight-adjustment bolts, side plates, and string.

Golding, since its inception, has been using process costing to assign product costs. A predetermined overhead rate is used based on direct labor dollars (80% of direct labor dollars). Recently, Golding has hired a new controller, Karen Jenkins. After reviewing the product-costing procedures, Karen requested a meeting with the divisional manager, Aaron Suhr. The following is a transcript of their conversation:

Karen : Aaron, I have some concerns about our cost accounting system. We make two different models of bows and are treating them as if they were the same product. Now I know that the only real difference between the models is the handle. The processing of the handles is the same, but the handles differ significantly in the amount and quality of wood used. Our current costing does not reflect this difference in material input.

Aaron : Your predecessor is responsible. He believed that tracking the difference in material cost wasn't worth the effort. He simply didn't believe that it would make much difference in the unit cost of either model.

Karen : Well, he may have been right, but I have my doubts. If there is a significant difference, it could affect our views of which model is more important to the company. The additional bookkeeping isn't very stringent. All we have to worry about is the pattern department. The other departments fit what I view as a process-costing pattern.

Aaron : Why don't you look into it? If there is a significant difference, go ahead and adjust the costing system.

After the meeting, Karen decided to collect cost data on the two models: the Deluxe model and the Econo model. She decided to track the costs for one week. At the end of the week, she had collected the following data from the pattern department:

a. There were a total of 2,500 bows completed: 1,000 Deluxe models and 1,500 Econo models.

b. There was no BWIP; however, there were 300 units in EWIP: 200 Deluxe and 100 Econo models. Both models were 80% complete with respect to conversion costs and 100% complete with respect to materials.

c. The pattern department experienced the following costs:

d. On an experimental basis, the requisition forms for materials were modified to identify the dollar value of the materials used by the Econo and Deluxe models:

Required:

1. Compute the unit cost for the handles produced by the pattern department assuming that process costing is totally appropriate. Round unit cost to two decimal places.

2. Compute the unit cost of each handle using the separate cost information provided on materials. Round unit cost to two decimal places.

3. Compare the unit costs computed in Requirements 1 and 2. Is Karen justified in her belief that a pure process-costing relationship is not appropriate? Describe the costing system that you would recommend.

4. In the past, the marketing manager has requested more money for advertising the Econo line. Aaron has repeatedly refused to grant any increase in this product's advertising budget because its per-unit profit (selling price minus manufacturing cost) is so low. Given the results in Requirements 1 through 3, was Aaron justified in his position?

Golding Manufacturing, a division of Farnsworth Sporting Inc., produces two different models of bows and eight models of knives. The bow-manufacturing process involves the production of two major subassemblies: the limbs and the handles. The limbs pass through four sequential processes before reaching final assembly: layup, molding, fabricating, and finishing. In the layup department, limbs are created by laminating layers of wood. In the molding department, the limbs are heat-treated, under pressure, to form strong resilient limbs. In the fabricating department, any protruding glue or other processing residue is removed. Finally, in the finishing department, the limbs are cleaned with acetone, dried, and sprayed with the final finishes.

The handles pass through two processes before reaching final assembly: pattern and finishing. In the pattern department, blocks of wood are fed into a machine that is set to shape the handles. Different patterns are possible, depending on the machine's setting. After coming out of the machine, the handles are cleaned and smoothed. They then pass to the finishing department, where they are sprayed with the final finishes. In final assembly, the limbs and handles are assembled into different models using purchased parts such as pulley assemblies, weight-adjustment bolts, side plates, and string.

Golding, since its inception, has been using process costing to assign product costs. A predetermined overhead rate is used based on direct labor dollars (80% of direct labor dollars). Recently, Golding has hired a new controller, Karen Jenkins. After reviewing the product-costing procedures, Karen requested a meeting with the divisional manager, Aaron Suhr. The following is a transcript of their conversation:

Karen : Aaron, I have some concerns about our cost accounting system. We make two different models of bows and are treating them as if they were the same product. Now I know that the only real difference between the models is the handle. The processing of the handles is the same, but the handles differ significantly in the amount and quality of wood used. Our current costing does not reflect this difference in material input.

Aaron : Your predecessor is responsible. He believed that tracking the difference in material cost wasn't worth the effort. He simply didn't believe that it would make much difference in the unit cost of either model.

Karen : Well, he may have been right, but I have my doubts. If there is a significant difference, it could affect our views of which model is more important to the company. The additional bookkeeping isn't very stringent. All we have to worry about is the pattern department. The other departments fit what I view as a process-costing pattern.

Aaron : Why don't you look into it? If there is a significant difference, go ahead and adjust the costing system.

After the meeting, Karen decided to collect cost data on the two models: the Deluxe model and the Econo model. She decided to track the costs for one week. At the end of the week, she had collected the following data from the pattern department:

a. There were a total of 2,500 bows completed: 1,000 Deluxe models and 1,500 Econo models.

b. There was no BWIP; however, there were 300 units in EWIP: 200 Deluxe and 100 Econo models. Both models were 80% complete with respect to conversion costs and 100% complete with respect to materials.

c. The pattern department experienced the following costs:

d. On an experimental basis, the requisition forms for materials were modified to identify the dollar value of the materials used by the Econo and Deluxe models:

Required:

1. Compute the unit cost for the handles produced by the pattern department assuming that process costing is totally appropriate. Round unit cost to two decimal places.

2. Compute the unit cost of each handle using the separate cost information provided on materials. Round unit cost to two decimal places.

3. Compare the unit costs computed in Requirements 1 and 2. Is Karen justified in her belief that a pure process-costing relationship is not appropriate? Describe the costing system that you would recommend.

4. In the past, the marketing manager has requested more money for advertising the Econo line. Aaron has repeatedly refused to grant any increase in this product's advertising budget because its per-unit profit (selling price minus manufacturing cost) is so low. Given the results in Requirements 1 through 3, was Aaron justified in his position?

Question

Question

Question

Question

( Appendix 6A ) First-In, First-Out Method; Equivalent Units

Lawson Company produces a product where all manufacturing inputs are applied uniformly. Lawson produced the following physical flow schedule for March:

Required:

Prepare a schedule of equivalent units using the FIFO method.

Lawson Company produces a product where all manufacturing inputs are applied uniformly. Lawson produced the following physical flow schedule for March:

Required:

Prepare a schedule of equivalent units using the FIFO method.

Question

Equivalent Units; Valuation of Work-in-Process Inventories; First-In, First-Out versus Weighted Average

AKL Foundry manufactures metal components for different kinds of equipment used by the aerospace, commercial aircraft, medical equipment, and electronic industries. The company uses investment casting to produce the required components. Investment casting consists of creating, in wax, a replica of the final product and pouring a hard shell around it. After removing the wax, molten metal is poured into the resulting cavity. What remains after the shell is broken is the desired metal object ready to be put to its designated use.

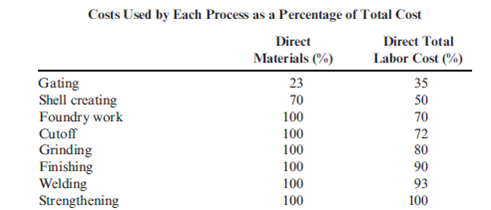

Metal components pass through eight processes: gating, shell creating, foundry work, cutoff, grinding, finishing, welding, and strengthening. Gating creates the wax mold and clusters the wax pattern around a sprue (a hole through which the molten metal will be poured through the gates into the mold in the foundry process), which is joined and supported by gates (flow channels) to form a tree of patterns. In the shell-creating process, the wax molds are alternately dipped in a ceramic slurry and a fluidized bed of progressively coarser refractory grain until a sufficiently thick shell (or mold) completely encases the wax pattern. After drying, the mold is sent to the foundry process. Here, the wax is melted out of the mold, and the shell is fired, strengthened, and brought to the proper temperature. Molten metal is then poured into the dewaxed shell. Finally, the ceramic shell is removed, and the finished product is sent to the cutoff process, where the parts are separated from the tree by the use of a band saw. The parts are then sent to the grinding process, where the gates that allowed the molten metal to flow into the ceramic cavities are ground off using large abrasive grinders. In the finishing process, rough edges caused by the grinders are removed by small handheld pneumatic tools. Parts that are flawed at this point are sent to welding for corrective treatment. The last process uses heat to treat the parts to bring them to the desired strength.

In 2015, the two partners who owned AKL Foundry decided to split up and divide the business. In dissolving their business relationship, they were faced with the problem of dividing the business assets equitably. Since the company had two plants-one in Arizona and one in New Mexico-a suggestion was made to split the business on the basis of geographic location. One partner would assume ownership of the plant in New Mexico, and the other would assume ownership of the plant in Arizona. However, this arrangement had one major complication: the amount of WIP inventory located in the Arizona plant.

The Arizona facilities had been in operation for more than a decade and were full of WIP. The New Mexico facility had been operational for only 2 years and had much smaller WIP inventories. The partner located in New Mexico argued that to disregard the unequal value of the WIP inventories would be grossly unfair.

Unfortunately, during the entire business history of AKL Foundry, WIP inventories had never been assigned any value. In computing the cost of goods sold each year, the company had followed the policy of adding depreciation to the out-of-pocket costs of direct labor, direct materials, and overhead. Accruals for the company are nearly nonexistent, and there are hardly ever any ending inventories of materials.

During 2015, the Arizona plant had sales of $2,028,670. The cost of goods sold is itemized as follows:

Upon request, the owners of AKL provided the following supplementary information (percentages are cumulative):

Gating had 10,000 units in BWIP, 60% complete. Assume that all materials are added at the beginning of each process. During the year, 50,000 units were completed and transferred out. The ending inventory had 11,000 unfinished units, 60% complete.

Required:

1. The partners of AKL want a reasonable estimate of the cost of WIP inventories. Using the gating department's inventory as an example, prepare an estimate of the cost of the EWIP. What assumptions did you make? Did you use the FIFO or weighted average method? Why? ( Note : Round unit cost to two decimal places.)

2. Assume that the shell-creating process has 8,000 units in BWIP, 20% complete. During the year, 50,000 units were completed and transferred out. ( Note : All 50,000 units were sold; no other units were sold.) The EWIP inventory had 8,000 units, 30% complete. Compute the value of the shell-creating department's EWIP. What additional assumptions had to be made?

AKL Foundry manufactures metal components for different kinds of equipment used by the aerospace, commercial aircraft, medical equipment, and electronic industries. The company uses investment casting to produce the required components. Investment casting consists of creating, in wax, a replica of the final product and pouring a hard shell around it. After removing the wax, molten metal is poured into the resulting cavity. What remains after the shell is broken is the desired metal object ready to be put to its designated use.

Metal components pass through eight processes: gating, shell creating, foundry work, cutoff, grinding, finishing, welding, and strengthening. Gating creates the wax mold and clusters the wax pattern around a sprue (a hole through which the molten metal will be poured through the gates into the mold in the foundry process), which is joined and supported by gates (flow channels) to form a tree of patterns. In the shell-creating process, the wax molds are alternately dipped in a ceramic slurry and a fluidized bed of progressively coarser refractory grain until a sufficiently thick shell (or mold) completely encases the wax pattern. After drying, the mold is sent to the foundry process. Here, the wax is melted out of the mold, and the shell is fired, strengthened, and brought to the proper temperature. Molten metal is then poured into the dewaxed shell. Finally, the ceramic shell is removed, and the finished product is sent to the cutoff process, where the parts are separated from the tree by the use of a band saw. The parts are then sent to the grinding process, where the gates that allowed the molten metal to flow into the ceramic cavities are ground off using large abrasive grinders. In the finishing process, rough edges caused by the grinders are removed by small handheld pneumatic tools. Parts that are flawed at this point are sent to welding for corrective treatment. The last process uses heat to treat the parts to bring them to the desired strength.

In 2015, the two partners who owned AKL Foundry decided to split up and divide the business. In dissolving their business relationship, they were faced with the problem of dividing the business assets equitably. Since the company had two plants-one in Arizona and one in New Mexico-a suggestion was made to split the business on the basis of geographic location. One partner would assume ownership of the plant in New Mexico, and the other would assume ownership of the plant in Arizona. However, this arrangement had one major complication: the amount of WIP inventory located in the Arizona plant.

The Arizona facilities had been in operation for more than a decade and were full of WIP. The New Mexico facility had been operational for only 2 years and had much smaller WIP inventories. The partner located in New Mexico argued that to disregard the unequal value of the WIP inventories would be grossly unfair.

Unfortunately, during the entire business history of AKL Foundry, WIP inventories had never been assigned any value. In computing the cost of goods sold each year, the company had followed the policy of adding depreciation to the out-of-pocket costs of direct labor, direct materials, and overhead. Accruals for the company are nearly nonexistent, and there are hardly ever any ending inventories of materials.

During 2015, the Arizona plant had sales of $2,028,670. The cost of goods sold is itemized as follows:

Upon request, the owners of AKL provided the following supplementary information (percentages are cumulative):

Gating had 10,000 units in BWIP, 60% complete. Assume that all materials are added at the beginning of each process. During the year, 50,000 units were completed and transferred out. The ending inventory had 11,000 unfinished units, 60% complete.

Required:

1. The partners of AKL want a reasonable estimate of the cost of WIP inventories. Using the gating department's inventory as an example, prepare an estimate of the cost of the EWIP. What assumptions did you make? Did you use the FIFO or weighted average method? Why? ( Note : Round unit cost to two decimal places.)

2. Assume that the shell-creating process has 8,000 units in BWIP, 20% complete. During the year, 50,000 units were completed and transferred out. ( Note : All 50,000 units were sold; no other units were sold.) The EWIP inventory had 8,000 units, 30% complete. Compute the value of the shell-creating department's EWIP. What additional assumptions had to be made?

Question

Question

Question

( Appendix 6A ) First-In, First-Out Method; Equivalent Units

Inca Inc. produces soft drinks. Mixing is the first department and its output is measured in gallons. Inca uses the FIFO method. All manufacturing costs are added uniformly. For July, the mixing department provided the following information:

Refer to the information for Inca Inc. on the previous page.

Required:

1. Calculate the equivalent units for August.

2. Calculate the unit cost. (Note: Round to two decimal places).

3. Assign costs to units transferred out and EWIP using the FIFO method.

Inca Inc. produces soft drinks. Mixing is the first department and its output is measured in gallons. Inca uses the FIFO method. All manufacturing costs are added uniformly. For July, the mixing department provided the following information:

Refer to the information for Inca Inc. on the previous page.

Required:

1. Calculate the equivalent units for August.

2. Calculate the unit cost. (Note: Round to two decimal places).

3. Assign costs to units transferred out and EWIP using the FIFO method.

Question

( Appendix 6A ) First-In, First-Out Method; Unit Cost; Valuing Inventories

Loren Inc. manufactures products that pass through two or more processes. During April, equivalent units were computed using the FIFO method:

Required:

1. Calculate the unit cost for April using the FIFO method. (Note: Round to two decimal places.)

2. Using the FIFO method, determine the cost of EWIP and the cost of the goods transferred out.

Loren Inc. manufactures products that pass through two or more processes. During April, equivalent units were computed using the FIFO method:

Required:

1. Calculate the unit cost for April using the FIFO method. (Note: Round to two decimal places.)

2. Using the FIFO method, determine the cost of EWIP and the cost of the goods transferred out.

Question

Question

Question

Question

( Appendix 6A ) FIFO; Production Report

Inca Inc. produces soft drinks. Mixing is the first department and its output is measured in gallons. Inca uses the FIFO method. All manufacturing costs are added uniformly. For July, the mixing department provided the following information:

Refer to the information for Inca Inc. on the previous page.

Required:

Prepare a production report.

Inca Inc. produces soft drinks. Mixing is the first department and its output is measured in gallons. Inca uses the FIFO method. All manufacturing costs are added uniformly. For July, the mixing department provided the following information:

Refer to the information for Inca Inc. on the previous page.

Required:

Prepare a production report.

Question

Question

Question

Question

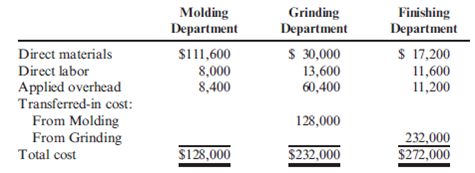

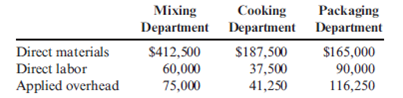

Basic Cost Flows

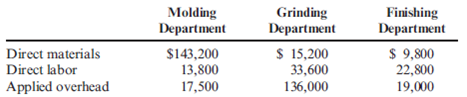

Davis Company produces a common machine component for industrial equipment in three departments: molding, grinding, and finishing. The following data are available for November:

During November, 9,000 components were completed. There is no beginning or ending WIP in any department.

Required:

1. Prepare a schedule showing, for each department, the cost of direct materials, direct labor, applied overhead, product transferred in from a prior department, and total manufacturing cost.

2. Calculate the unit cost. ( Note : Round the unit cost to two decimal places.)

Davis Company produces a common machine component for industrial equipment in three departments: molding, grinding, and finishing. The following data are available for November:

During November, 9,000 components were completed. There is no beginning or ending WIP in any department.

Required:

1. Prepare a schedule showing, for each department, the cost of direct materials, direct labor, applied overhead, product transferred in from a prior department, and total manufacturing cost.

2. Calculate the unit cost. ( Note : Round the unit cost to two decimal places.)

Question

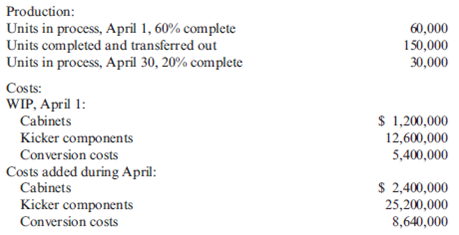

Steps in Preparing a Production Report

Recently, Stillwater Designs expanded its market by becoming an original equipment supplier to Jeep Wrangler. Stillwater Designs produces factory upgraded speakers specifically for Jeep Wrangler. The Kicker components and speaker cabinets are outsourced with assembly remaining in-house. Stillwater Designs assemble the product by placing the speakers and other components in cabinets that define an audio package upgrade and that can be placed into the Jeep Wrangler, producing the desired factory-installed appearance. Speaker cabinets and associated Kicker components are added at the beginning of the assembly process.

Assume that Stillwater Designs uses the weighted average method to cost out the audio package. The following are cost and production data for the assembly process for April:

Required:

1. Prepare a physical flow analysis for the assembly department for the month of April.

2. Calculate equivalent units of production for the assembly department for the month of April.

3. Calculate unit cost for the assembly department for the month of April.

4. Calculate the cost of units transferred out and the cost of EWIP inventory.

5. Prepare a cost reconciliation for the assembly department for the month of April.

Recently, Stillwater Designs expanded its market by becoming an original equipment supplier to Jeep Wrangler. Stillwater Designs produces factory upgraded speakers specifically for Jeep Wrangler. The Kicker components and speaker cabinets are outsourced with assembly remaining in-house. Stillwater Designs assemble the product by placing the speakers and other components in cabinets that define an audio package upgrade and that can be placed into the Jeep Wrangler, producing the desired factory-installed appearance. Speaker cabinets and associated Kicker components are added at the beginning of the assembly process.

Assume that Stillwater Designs uses the weighted average method to cost out the audio package. The following are cost and production data for the assembly process for April:

Required:

1. Prepare a physical flow analysis for the assembly department for the month of April.

2. Calculate equivalent units of production for the assembly department for the month of April.

3. Calculate unit cost for the assembly department for the month of April.

4. Calculate the cost of units transferred out and the cost of EWIP inventory.

5. Prepare a cost reconciliation for the assembly department for the month of April.

Question

Question

Question

Journal Entries, Basic Cost Flows

In December, Davis Company had the following cost flows:

Required:

1. Prepare the journal entries to transfer costs from (a) Molding to Grinding, (b) Grinding to Finishing, and (c) Finishing to Finished Goods.

2. CONCEPTUAL CONNECTION Explain how the journal entries differ from a job-order cost system.

In December, Davis Company had the following cost flows:

Required:

1. Prepare the journal entries to transfer costs from (a) Molding to Grinding, (b) Grinding to Finishing, and (c) Finishing to Finished Goods.

2. CONCEPTUAL CONNECTION Explain how the journal entries differ from a job-order cost system.

Question

Question

Question

Question

Equivalent Units, Unit Cost, Valuation of Goods Transferred Out and Ending Work in Process

The blending department had the following data for the month of March:

Required:

1. What is the output in equivalent units for March?

2. What is the unit manufacturing cost for March?

3. Compute the cost of goods transferred out for March.

4. Calculate the value of March's EWIP.

The blending department had the following data for the month of March:

Required:

1. What is the output in equivalent units for March?

2. What is the unit manufacturing cost for March?

3. Compute the cost of goods transferred out for March.

4. Calculate the value of March's EWIP.

Question

Equivalent Units, Unit Cost, Weighted Average

Alfombra Inc. manufactures throw rugs. The throw-rug department weaves cloth and yarn into throw rugs of various sizes. Alfombra uses the weighted average method. Materials are added uniformly throughout the weaving process. In August, Alfombra switched from FIFO to the weighted average method. The following data are for the throw-rug department for August:

Refer to the information for Alfombra Inc. above.

Required:

1. Prepare a physical flow analysis for the throw-rug department for August.

2. Calculate equivalent units of production for the throw-rug department for August.

3. Calculate the unit cost for the throw-rug department for August.

4. Show that the cost per unit calculated in Requirement 3 is a weighted average of the FIFO cost per equivalent unit in BWIP and the FIFO cost per equivalent unit for August. ( Hint : The weights are in proportion to the number of units from each source.)

Alfombra Inc. manufactures throw rugs. The throw-rug department weaves cloth and yarn into throw rugs of various sizes. Alfombra uses the weighted average method. Materials are added uniformly throughout the weaving process. In August, Alfombra switched from FIFO to the weighted average method. The following data are for the throw-rug department for August:

Refer to the information for Alfombra Inc. above.

Required:

1. Prepare a physical flow analysis for the throw-rug department for August.

2. Calculate equivalent units of production for the throw-rug department for August.

3. Calculate the unit cost for the throw-rug department for August.

4. Show that the cost per unit calculated in Requirement 3 is a weighted average of the FIFO cost per equivalent unit in BWIP and the FIFO cost per equivalent unit for August. ( Hint : The weights are in proportion to the number of units from each source.)

Question

Question

Question

Weighted Average Method, Equivalent Units

Goforth Company produces a product where all manufacturing inputs are applied uniformly. Goforth produced the following physical flow schedule for April:

Required:

Prepare a schedule of equivalent units using the weighted average method.

Goforth Company produces a product where all manufacturing inputs are applied uniformly. Goforth produced the following physical flow schedule for April:

Required:

Prepare a schedule of equivalent units using the weighted average method.

Question

Production Report

Alfombra Inc. manufactures throw rugs. The throw-rug department weaves cloth and yarn into throw rugs of various sizes. Alfombra uses the weighted average method. Materials are added uniformly throughout the weaving process. In August, Alfombra switched from FIFO to the weighted average method. The following data are for the throw-rug department for August:

Refer to the information for Alfombra Inc. above. The owner of Alfombra insisted on a formal report that provided all the details of the weighted average method. In the manufacturing process, all materials are added uniformly throughout the process.

Required:

Prepare a production report for the throw-rug department for August using the weighted average method.

Alfombra Inc. manufactures throw rugs. The throw-rug department weaves cloth and yarn into throw rugs of various sizes. Alfombra uses the weighted average method. Materials are added uniformly throughout the weaving process. In August, Alfombra switched from FIFO to the weighted average method. The following data are for the throw-rug department for August:

Refer to the information for Alfombra Inc. above. The owner of Alfombra insisted on a formal report that provided all the details of the weighted average method. In the manufacturing process, all materials are added uniformly throughout the process.

Required:

Prepare a production report for the throw-rug department for August using the weighted average method.

Question

Question

Question

Question

Weighted Average Method, Unit Cost, Valuing Inventories

Cassien Inc. manufactures products that pass through two or more processes. During June, equivalent units were computed using the weighted average method:

Required:

1. Calculate the unit cost for June using the weighted average method.

2. Using the weighted average method, determine the cost of EWIP and the cost of the goods transferred out.

3. CONCEPTUAL CONNECTION Cassien had just finished implementing a series of measures designed to reduce the unit cost to $2.00 and was assured that this had been achieved and should be realized for June's production; yet upon seeing the unit cost for June, the president of the company was disappointed. Can you explain why the full effect of the cost reductions may not show up in June? What can you suggest to overcome this problem?

Cassien Inc. manufactures products that pass through two or more processes. During June, equivalent units were computed using the weighted average method:

Required:

1. Calculate the unit cost for June using the weighted average method.

2. Using the weighted average method, determine the cost of EWIP and the cost of the goods transferred out.

3. CONCEPTUAL CONNECTION Cassien had just finished implementing a series of measures designed to reduce the unit cost to $2.00 and was assured that this had been achieved and should be realized for June's production; yet upon seeing the unit cost for June, the president of the company was disappointed. Can you explain why the full effect of the cost reductions may not show up in June? What can you suggest to overcome this problem?

Question

Question

Question

Question

Question

Weighted Average Method, Unit Costs, Valuing Inventories

Byford Inc. produces a product that passes through two processes. During November, equivalent units were calculated using the weighted average method:

The costs that Byford had to account for during the month of November were as follows:

Required:

1. Using the weighted average method, determine unit cost.

2. Under the weighted average method, what is the total cost of units transferred out? What is the cost assigned to units in ending inventory?

3. CONCEPTUAL CONNECTION Bill Johnson, the manager of Byford, is considering switching from weighted average to FIFO. Explain the key differences between the two approaches and make a recommendation to Bill about which method should be used.

Byford Inc. produces a product that passes through two processes. During November, equivalent units were calculated using the weighted average method:

The costs that Byford had to account for during the month of November were as follows:

Required:

1. Using the weighted average method, determine unit cost.

2. Under the weighted average method, what is the total cost of units transferred out? What is the cost assigned to units in ending inventory?

3. CONCEPTUAL CONNECTION Bill Johnson, the manager of Byford, is considering switching from weighted average to FIFO. Explain the key differences between the two approaches and make a recommendation to Bill about which method should be used.

Question

Weighted Average Method, Single-Department Analysis

Millie Company produces a product that passes through an assembly process and a finishing process. All manufacturing costs are added uniformly for both processes. The following information was obtained for the assembly department for June:

a. WIP, June 1, had 24,000 units (60% completed) and the following costs:

b. During June, 70,000 units were completed and transferred to the finishing department, and the following costs were added to production:

c. On June 30, there were 10,000 partially completed units in process. These units were 70% complete.

Refer to the information for Millie Company above.

Required:

Prepare a production report for the assembly department for June using the weighted average method of costing. The report should disclose the physical flow of units, equivalent units, and unit costs and should track the disposition of manufacturing costs.

Millie Company produces a product that passes through an assembly process and a finishing process. All manufacturing costs are added uniformly for both processes. The following information was obtained for the assembly department for June:

a. WIP, June 1, had 24,000 units (60% completed) and the following costs:

b. During June, 70,000 units were completed and transferred to the finishing department, and the following costs were added to production:

c. On June 30, there were 10,000 partially completed units in process. These units were 70% complete.

Refer to the information for Millie Company above.

Required:

Prepare a production report for the assembly department for June using the weighted average method of costing. The report should disclose the physical flow of units, equivalent units, and unit costs and should track the disposition of manufacturing costs.

Question

Question

Question

Basic Cost Flows

Pleni Company produces 18-ounce boxes of a wheat cereal in three departments: Mixing, Cooking, and Packaging. During August, Pleni produced 125,000 boxes with the following costs:

Required:

1. Calculate the costs transferred out of each department.

2. Prepare journal entries that reflect these cost transfers.

Pleni Company produces 18-ounce boxes of a wheat cereal in three departments: Mixing, Cooking, and Packaging. During August, Pleni produced 125,000 boxes with the following costs:

Required:

1. Calculate the costs transferred out of each department.

2. Prepare journal entries that reflect these cost transfers.

Question

Question

First-In, First-Out Method; Single-Department Analysis; One Cost Category

Millie Company produces a product that passes through an assembly process and a finishing process. All manufacturing costs are added uniformly for both processes. The following information was obtained for the assembly department for June:

a. WIP, June 1, had 24,000 units (60% completed) and the following costs:

b. During June, 70,000 units were completed and transferred to the finishing department, and the following costs were added to production:

c. On June 30, there were 10,000 partially completed units in process. These units were 70% complete.

Refer to the information for Millie Company above.

Required:

Prepare a production report for the assembly department for June using the FIFO method of costing. The report should disclose the physical flow of units, equivalent units, and unit costs and should track the disposition of manufacturing costs. (Note: Carry the unit cost computation to four decimal places.)

Millie Company produces a product that passes through an assembly process and a finishing process. All manufacturing costs are added uniformly for both processes. The following information was obtained for the assembly department for June:

a. WIP, June 1, had 24,000 units (60% completed) and the following costs:

b. During June, 70,000 units were completed and transferred to the finishing department, and the following costs were added to production:

c. On June 30, there were 10,000 partially completed units in process. These units were 70% complete.

Refer to the information for Millie Company above.

Required:

Prepare a production report for the assembly department for June using the FIFO method of costing. The report should disclose the physical flow of units, equivalent units, and unit costs and should track the disposition of manufacturing costs. (Note: Carry the unit cost computation to four decimal places.)

Question

Question

Question

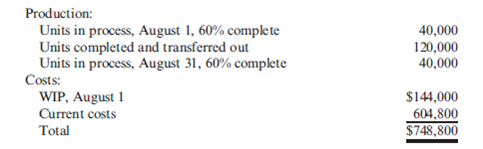

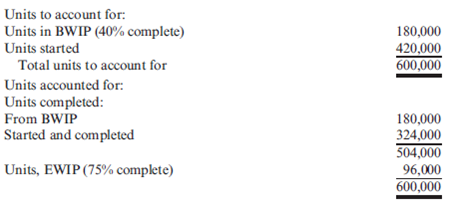

Equivalent Units, No Beginning Work in Process

Fried Manufacturing produces cylinders used in internal combustion engines. During June, Fried's welding department had the following data:

Required:

Calculate June's output for the welding department in equivalent units of production.

Fried Manufacturing produces cylinders used in internal combustion engines. During June, Fried's welding department had the following data:

Required:

Calculate June's output for the welding department in equivalent units of production.

Question

Physical Flow Schedule

Nelrok Company manufactures fertilizer. Department 1 mixes the chemicals required for the fertilizer. The following data are for the year:

Required:

Prepare a physical flow schedule.

Nelrok Company manufactures fertilizer. Department 1 mixes the chemicals required for the fertilizer. The following data are for the year:

Required:

Prepare a physical flow schedule.

Question

Weighted Average Method, Separate Materials Cost

Janbo Company produces a variety of stationery products. One product, sealing wax sticks, passes through two processes: blending and molding. The weighted average method is used to account for the costs of production. After blending, the resulting product is sent to the molding department, where it is poured into molds and cooled. The following information relates to the blending process for August:

a. WIP, August 1, had 30,000 pounds, 20% complete. Costs associated with partially completed units were:

b. WIP, August 31, had 50,000 pounds, 40% complete.

c. Units completed and transferred out totaled 480,000 pounds. Costs added during the month were (all inputs are added uniformly):

Required:

1. Prepare (a) a physical flow schedule and (b) an equivalent unit schedule.

2. Calculate the unit cost. (Note: Round to three decimal places.)

3. Compute the cost of EWIP and the cost of goods transferred out.

4. Prepare a cost reconciliation.

5. Suppose that the materials added uniformly in blending are paraffin and pigment and that the manager of the company wants to know how much each of these materials costs per equivalent unit produced. The costs of the materials in BWIP are as follows:

The costs of the materials added during the month are also given:

Prepare an equivalent unit schedule with cost categories for each material. Calculate the cost per unit for each type of material.

Janbo Company produces a variety of stationery products. One product, sealing wax sticks, passes through two processes: blending and molding. The weighted average method is used to account for the costs of production. After blending, the resulting product is sent to the molding department, where it is poured into molds and cooled. The following information relates to the blending process for August:

a. WIP, August 1, had 30,000 pounds, 20% complete. Costs associated with partially completed units were:

b. WIP, August 31, had 50,000 pounds, 40% complete.

c. Units completed and transferred out totaled 480,000 pounds. Costs added during the month were (all inputs are added uniformly):

Required:

1. Prepare (a) a physical flow schedule and (b) an equivalent unit schedule.

2. Calculate the unit cost. (Note: Round to three decimal places.)

3. Compute the cost of EWIP and the cost of goods transferred out.

4. Prepare a cost reconciliation.

5. Suppose that the materials added uniformly in blending are paraffin and pigment and that the manager of the company wants to know how much each of these materials costs per equivalent unit produced. The costs of the materials in BWIP are as follows:

The costs of the materials added during the month are also given:

Prepare an equivalent unit schedule with cost categories for each material. Calculate the cost per unit for each type of material.

Question

Question

Question

Question

Production Report, Weighted Average

Mino Inc. manufactures chocolate syrup in three departments: Cooking, Mixing, and Bottling. Mino uses the weighted average method. The following are cost and production data for the cooking department for April ( Note : Assume that units are measured in gallons):

Required:

Prepare a production report for the cooking department.

Mino Inc. manufactures chocolate syrup in three departments: Cooking, Mixing, and Bottling. Mino uses the weighted average method. The following are cost and production data for the cooking department for April ( Note : Assume that units are measured in gallons):

Required:

Prepare a production report for the cooking department.

Question

Weighted Average Method, Journal Entries

Seacrest Company uses a process costing system. The company manufactures a product that is processed in two departments: A and B. As work is completed, it is transferred out. All inputs are added uniformly in Department A. The following summarizes the production activity and costs for November:

Required:

1. Using the weighted average method, prepare the following for Department A: (a) a physical flow schedule, (b) an equivalent unit calculation, (c) calculation of unit costs (Note:Round to two decimal places), (d) cost of EWIP and cost of goods transferred out, and (e) a cost reconciliation.

2. CONCEPTUAL CONNECTION Prepare journal entries that show the flow of manufacturing costs for Department A. Use a conversion cost control account for conversion costs. Many firms are now combining direct labor and overhead costs into one category. They are not tracking direct labor separately. Offer some reasons for this practice.

Seacrest Company uses a process costing system. The company manufactures a product that is processed in two departments: A and B. As work is completed, it is transferred out. All inputs are added uniformly in Department A. The following summarizes the production activity and costs for November:

Required:

1. Using the weighted average method, prepare the following for Department A: (a) a physical flow schedule, (b) an equivalent unit calculation, (c) calculation of unit costs (Note:Round to two decimal places), (d) cost of EWIP and cost of goods transferred out, and (e) a cost reconciliation.

2. CONCEPTUAL CONNECTION Prepare journal entries that show the flow of manufacturing costs for Department A. Use a conversion cost control account for conversion costs. Many firms are now combining direct labor and overhead costs into one category. They are not tracking direct labor separately. Offer some reasons for this practice.

Question

Question

Question

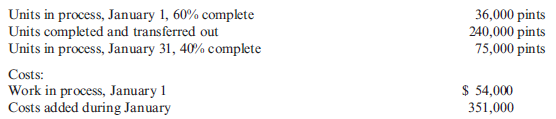

Weighted Average Method, Unit Cost, Valuing Inventories

Manzer Enterprises produces premier raspberry jam. Output is measured in pints. Manzer uses the weighted average method. During January, Manzer had the following production data:

Required:

1. Using the weighted average method, calculate the equivalent units for January.

2. Calculate the unit cost for January.

3. Assign costs to units transferred out and EWIP.

Manzer Enterprises produces premier raspberry jam. Output is measured in pints. Manzer uses the weighted average method. During January, Manzer had the following production data:

Required:

1. Using the weighted average method, calculate the equivalent units for January.

2. Calculate the unit cost for January.

3. Assign costs to units transferred out and EWIP.

Question

Nonuniform Inputs, Equivalent Units

Terry Linens Inc. manufactures bed and bath linens. The bath linens department sews terry cloth into towels of various sizes. Terry uses the weighted average method. All materials are added at the beginning of the process. The following data are for the bath linens department for August:

Required:

Calculate equivalent units of production for the bath linens department for August.

Terry Linens Inc. manufactures bed and bath linens. The bath linens department sews terry cloth into towels of various sizes. Terry uses the weighted average method. All materials are added at the beginning of the process. The following data are for the bath linens department for August:

Required:

Calculate equivalent units of production for the bath linens department for August.

Question

Question

Question

Question

Physical Flow Schedule

Buckner Inc. just finished its second month of operations. Buckner mass produces integrated circuits. The following production information is provided for December:

Required:

Prepare a physical flow schedule.

Buckner Inc. just finished its second month of operations. Buckner mass produces integrated circuits. The following production information is provided for December:

Required:

Prepare a physical flow schedule.

Question

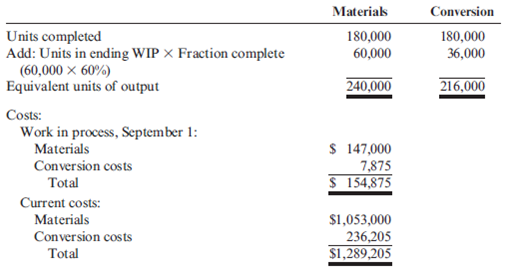

Unit Cost and Cost Assignment, Nonuniform Inputs

Loran Inc. had the following equivalent units schedule and cost for its fabrication department during September:

Required:

1. Calculate the unit cost for materials, for conversion, and in total for the fabrication department for September.

2. Calculate the cost of units transferred out and the cost of EWIP.

Loran Inc. had the following equivalent units schedule and cost for its fabrication department during September:

Required:

1. Calculate the unit cost for materials, for conversion, and in total for the fabrication department for September.

2. Calculate the cost of units transferred out and the cost of EWIP.

Question

Weighted Average Method, Nonuniform Inputs, Multiple Departments

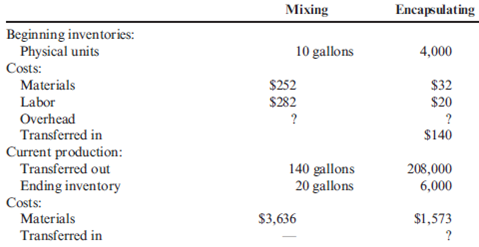

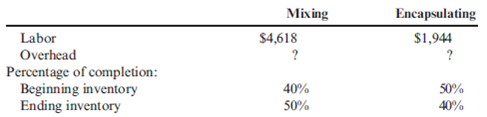

Benson Pharmaceuticals uses a process-costing system to compute the unit costs of the over-thecounter cold remedies that it produces. It has three departments: Mixing, Encapsulating, and Bottling. In Mixing, the ingredients for the cold capsules are measured, sifted, and blended (materials are thus assumed to be uniformly added throughout the process). The mix is transferred out in gallon containers. The encapsulating department takes the powdered mix and places it in capsules (capsules are necessarily added at the beginning of the process). One gallon of powdered mix converts into 1,500 capsules. After the capsules are filled and polished, they are transferred to Bottling, where they are placed in bottles that are then affixed with a safety seal, lid, and label. Each bottle receives 50 capsules.

During March, the following results are available for the first two departments:

Overhead in both departments is applied as a percentage of direct labor costs. In the mixing department, overhead is 200% of direct labor. In the encapsulating department, the overhead rate is 150% of direct labor.

Required:

1. Prepare a production report for the mixing department using the weighted average method.

Follow the five steps outlined in the chapter. (Note: Round to two decimal places for the unit cost.)

2. Prepare a production report for the encapsulating department using the weighted average method. Follow the five steps outlined in the chapter. (Note: Round to four decimal places for the unit cost.)

3. CONCEPTUAL CONNECTION Explain why the weighted average method is easier to use than FIFO. Explain when weighted average will give about the same results as FIFO.

Benson Pharmaceuticals uses a process-costing system to compute the unit costs of the over-thecounter cold remedies that it produces. It has three departments: Mixing, Encapsulating, and Bottling. In Mixing, the ingredients for the cold capsules are measured, sifted, and blended (materials are thus assumed to be uniformly added throughout the process). The mix is transferred out in gallon containers. The encapsulating department takes the powdered mix and places it in capsules (capsules are necessarily added at the beginning of the process). One gallon of powdered mix converts into 1,500 capsules. After the capsules are filled and polished, they are transferred to Bottling, where they are placed in bottles that are then affixed with a safety seal, lid, and label. Each bottle receives 50 capsules.

During March, the following results are available for the first two departments:

Overhead in both departments is applied as a percentage of direct labor costs. In the mixing department, overhead is 200% of direct labor. In the encapsulating department, the overhead rate is 150% of direct labor.

Required:

1. Prepare a production report for the mixing department using the weighted average method.

Follow the five steps outlined in the chapter. (Note: Round to two decimal places for the unit cost.)

2. Prepare a production report for the encapsulating department using the weighted average method. Follow the five steps outlined in the chapter. (Note: Round to four decimal places for the unit cost.)

3. CONCEPTUAL CONNECTION Explain why the weighted average method is easier to use than FIFO. Explain when weighted average will give about the same results as FIFO.

Question

Question

Question

Production Report, Weighted Average

Murray Inc. manufactures bicycle frames in two departments: Cutting and Welding. Murray uses the weighted average method. Manufacturing costs are added uniformly throughout the process. The following are cost and production data for the cutting department for October:

Required:

Prepare a production report for the cutting department.

Murray Inc. manufactures bicycle frames in two departments: Cutting and Welding. Murray uses the weighted average method. Manufacturing costs are added uniformly throughout the process. The following are cost and production data for the cutting department for October:

Required:

Prepare a production report for the cutting department.

Question

Nonuniform Inputs, Transferred-In Cost

Drysdale Dairy produces a variety of dairy products. In Department 12, cream (transferred in from Department 6) and other materials (sugar and flavorings) are mixed at the beginning of the process and churned to make ice cream. The following data are for Department 12 for August:

Required:

1. Prepare a physical flow schedule for the month.

2. Using the weighted average method, calculate equivalent units for the following categories: transferred-in, materials, and conversion.

Drysdale Dairy produces a variety of dairy products. In Department 12, cream (transferred in from Department 6) and other materials (sugar and flavorings) are mixed at the beginning of the process and churned to make ice cream. The following data are for Department 12 for August:

Required:

1. Prepare a physical flow schedule for the month.

2. Using the weighted average method, calculate equivalent units for the following categories: transferred-in, materials, and conversion.

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/75

Play

Full screen (f)

Deck 6: Process Costing

1

How would process costing for services differ from process costing for manufactured goods?

Identify the differences between process costing for manufacturing and service firms:

Service firms:

Service firm may or may not have WIP inventories. For example a batch of tax return can be partially completed at the end of a period. However, many services are provided so quickly that there are not WIP inventories Therefore, process costing is relatively simple.

Manufacturing firms may have significant beginning and ending WIP inventories. These cause complications in process costing due to several factors such as the presence of beginning and ending WIP inventories and different approached to the treatment of beginning inventory cost like FIFO, Weighted Average etc.

Manufacturing firms may have significant beginning and ending WIP inventories. These cause complications in process costing due to several factors such as the presence of beginning and ending WIP inventories and different approached to the treatment of beginning inventory cost like FIFO, Weighted Average etc.

Therefore, process costing is relatively complicated. The total cost for particular process is divided by the normal output of that process to compute unit cost: of that process:

Service firms:

Service firm may or may not have WIP inventories. For example a batch of tax return can be partially completed at the end of a period. However, many services are provided so quickly that there are not WIP inventories Therefore, process costing is relatively simple.

Manufacturing firms may have significant beginning and ending WIP inventories. These cause complications in process costing due to several factors such as the presence of beginning and ending WIP inventories and different approached to the treatment of beginning inventory cost like FIFO, Weighted Average etc. Therefore, process costing is relatively complicated. The total cost for particular process is divided by the normal output of that process to compute unit cost: of that process:

2

Explain why transferred-in costs are a special type of raw material for the receiving department.

In process manufacturing, some departments receive partially completed goods from prior department. The usual approach is to treat transferred in goods as a separate material category when calculating equivalent units.

Thus, the department receiving transferred in goods would have three input categories.

• One for the transferred in material

• One for material added

• One for conversion cost

In dealing in transferred in goods, two important points should be remembered.

1) The cost of this material is the goods transferred out as computed in the prior department.

2) The units started in the subsequent department correspond to the units transferred out from the prior department

Transferred in goods are viewed as materials added at the beginning of the process. They are treated as a separated input category, and equivalent units and a until costs are calculated for transferred in material.

The only additional complication introduced in the analysis for a subsequent department is the presence of the transferred in category. As shown, dealing with this category is similar to handing any other category. However, it must be remembered that the current cost of this special type of raw material is the cost of the units transferred in from the prior process and that the units transferred in are the units started.

Thus, the department receiving transferred in goods would have three input categories.

• One for the transferred in material

• One for material added

• One for conversion cost

In dealing in transferred in goods, two important points should be remembered.

1) The cost of this material is the goods transferred out as computed in the prior department.

2) The units started in the subsequent department correspond to the units transferred out from the prior department

Transferred in goods are viewed as materials added at the beginning of the process. They are treated as a separated input category, and equivalent units and a until costs are calculated for transferred in material.

The only additional complication introduced in the analysis for a subsequent department is the presence of the transferred in category. As shown, dealing with this category is similar to handing any other category. However, it must be remembered that the current cost of this special type of raw material is the cost of the units transferred in from the prior process and that the units transferred in are the units started.

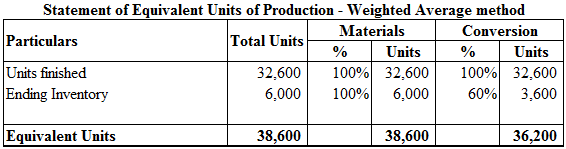

3

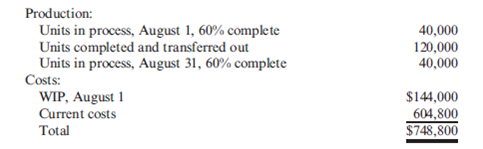

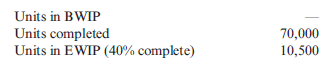

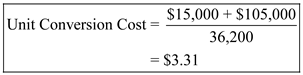

Nonuniform Inputs, Weighted Average

Integer Inc. had the following production and cost information for its fabrication department during April (materials are added at the beginning of the fabrication process):

Integer uses the weighted average method.

Required:

1. Prepare an equivalent units schedule.

2. Calculate the unit cost. (Note: Round answers to two decimal places).

3. Calculate the cost of units transferred out and the cost of EWIP.

Integer Inc. had the following production and cost information for its fabrication department during April (materials are added at the beginning of the fabrication process):

Integer uses the weighted average method.

Required:

1. Prepare an equivalent units schedule.

2. Calculate the unit cost. (Note: Round answers to two decimal places).

3. Calculate the cost of units transferred out and the cost of EWIP.

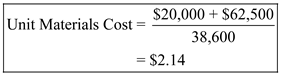

Weighted average method of equivalent units:

The cost of beginning work in process is treated as the process introduced and completed during the current period.

1.

Prepare the equivalent unit schedule as shown below:

The equivalent units of production for materials are 38,600 units and for conversion it is 36,200 units.

The equivalent units of production for materials are 38,600 units and for conversion it is 36,200 units.

2.

Calculate the unit costs.

Therefore, the cost per unit is $5.45.

Therefore, the cost per unit is $5.45.

3.

Calculate the cost of goods transferred out.

Therefore, the cost of goods transferred out is

Therefore, the cost of goods transferred out is

.

.

Calculate the cost of ending work in process (EWIP).

Therefore, the cost of ending work in process is

Therefore, the cost of ending work in process is

.

.

The cost of beginning work in process is treated as the process introduced and completed during the current period.

1.

Prepare the equivalent unit schedule as shown below:

The equivalent units of production for materials are 38,600 units and for conversion it is 36,200 units.2.

Calculate the unit costs.

Therefore, the cost per unit is $5.45.3.

Calculate the cost of goods transferred out.

Therefore, the cost of goods transferred out is .Calculate the cost of ending work in process (EWIP).

Therefore, the cost of ending work in process is . 4

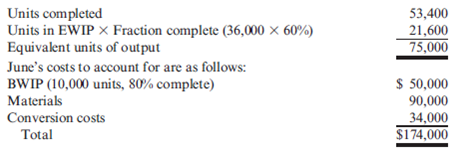

Transferred-In Cost

Golding's finishing department had the following data for July:

Required:

1. Calculate unit costs for the following categories: transferred-in, materials, and conversion.

2. Calculate total unit cost.

Golding's finishing department had the following data for July:

Required:

1. Calculate unit costs for the following categories: transferred-in, materials, and conversion.

2. Calculate total unit cost.

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

5

Process Costing versus Alternative Costing Methods, Impact on Resource Allocation Decision

Golding Manufacturing, a division of Farnsworth Sporting Inc., produces two different models of bows and eight models of knives. The bow-manufacturing process involves the production of two major subassemblies: the limbs and the handles. The limbs pass through four sequential processes before reaching final assembly: layup, molding, fabricating, and finishing. In the layup department, limbs are created by laminating layers of wood. In the molding department, the limbs are heat-treated, under pressure, to form strong resilient limbs. In the fabricating department, any protruding glue or other processing residue is removed. Finally, in the finishing department, the limbs are cleaned with acetone, dried, and sprayed with the final finishes.

The handles pass through two processes before reaching final assembly: pattern and finishing. In the pattern department, blocks of wood are fed into a machine that is set to shape the handles. Different patterns are possible, depending on the machine's setting. After coming out of the machine, the handles are cleaned and smoothed. They then pass to the finishing department, where they are sprayed with the final finishes. In final assembly, the limbs and handles are assembled into different models using purchased parts such as pulley assemblies, weight-adjustment bolts, side plates, and string.

Golding, since its inception, has been using process costing to assign product costs. A predetermined overhead rate is used based on direct labor dollars (80% of direct labor dollars). Recently, Golding has hired a new controller, Karen Jenkins. After reviewing the product-costing procedures, Karen requested a meeting with the divisional manager, Aaron Suhr. The following is a transcript of their conversation:

Karen : Aaron, I have some concerns about our cost accounting system. We make two different models of bows and are treating them as if they were the same product. Now I know that the only real difference between the models is the handle. The processing of the handles is the same, but the handles differ significantly in the amount and quality of wood used. Our current costing does not reflect this difference in material input.

Aaron : Your predecessor is responsible. He believed that tracking the difference in material cost wasn't worth the effort. He simply didn't believe that it would make much difference in the unit cost of either model.

Karen : Well, he may have been right, but I have my doubts. If there is a significant difference, it could affect our views of which model is more important to the company. The additional bookkeeping isn't very stringent. All we have to worry about is the pattern department. The other departments fit what I view as a process-costing pattern.

Aaron : Why don't you look into it? If there is a significant difference, go ahead and adjust the costing system.

After the meeting, Karen decided to collect cost data on the two models: the Deluxe model and the Econo model. She decided to track the costs for one week. At the end of the week, she had collected the following data from the pattern department:

a. There were a total of 2,500 bows completed: 1,000 Deluxe models and 1,500 Econo models.

b. There was no BWIP; however, there were 300 units in EWIP: 200 Deluxe and 100 Econo models. Both models were 80% complete with respect to conversion costs and 100% complete with respect to materials.

c. The pattern department experienced the following costs:

d. On an experimental basis, the requisition forms for materials were modified to identify the dollar value of the materials used by the Econo and Deluxe models:

Required:

1. Compute the unit cost for the handles produced by the pattern department assuming that process costing is totally appropriate. Round unit cost to two decimal places.

2. Compute the unit cost of each handle using the separate cost information provided on materials. Round unit cost to two decimal places.

3. Compare the unit costs computed in Requirements 1 and 2. Is Karen justified in her belief that a pure process-costing relationship is not appropriate? Describe the costing system that you would recommend.

4. In the past, the marketing manager has requested more money for advertising the Econo line. Aaron has repeatedly refused to grant any increase in this product's advertising budget because its per-unit profit (selling price minus manufacturing cost) is so low. Given the results in Requirements 1 through 3, was Aaron justified in his position?

Golding Manufacturing, a division of Farnsworth Sporting Inc., produces two different models of bows and eight models of knives. The bow-manufacturing process involves the production of two major subassemblies: the limbs and the handles. The limbs pass through four sequential processes before reaching final assembly: layup, molding, fabricating, and finishing. In the layup department, limbs are created by laminating layers of wood. In the molding department, the limbs are heat-treated, under pressure, to form strong resilient limbs. In the fabricating department, any protruding glue or other processing residue is removed. Finally, in the finishing department, the limbs are cleaned with acetone, dried, and sprayed with the final finishes.

The handles pass through two processes before reaching final assembly: pattern and finishing. In the pattern department, blocks of wood are fed into a machine that is set to shape the handles. Different patterns are possible, depending on the machine's setting. After coming out of the machine, the handles are cleaned and smoothed. They then pass to the finishing department, where they are sprayed with the final finishes. In final assembly, the limbs and handles are assembled into different models using purchased parts such as pulley assemblies, weight-adjustment bolts, side plates, and string.

Golding, since its inception, has been using process costing to assign product costs. A predetermined overhead rate is used based on direct labor dollars (80% of direct labor dollars). Recently, Golding has hired a new controller, Karen Jenkins. After reviewing the product-costing procedures, Karen requested a meeting with the divisional manager, Aaron Suhr. The following is a transcript of their conversation:

Karen : Aaron, I have some concerns about our cost accounting system. We make two different models of bows and are treating them as if they were the same product. Now I know that the only real difference between the models is the handle. The processing of the handles is the same, but the handles differ significantly in the amount and quality of wood used. Our current costing does not reflect this difference in material input.

Aaron : Your predecessor is responsible. He believed that tracking the difference in material cost wasn't worth the effort. He simply didn't believe that it would make much difference in the unit cost of either model.

Karen : Well, he may have been right, but I have my doubts. If there is a significant difference, it could affect our views of which model is more important to the company. The additional bookkeeping isn't very stringent. All we have to worry about is the pattern department. The other departments fit what I view as a process-costing pattern.

Aaron : Why don't you look into it? If there is a significant difference, go ahead and adjust the costing system.

After the meeting, Karen decided to collect cost data on the two models: the Deluxe model and the Econo model. She decided to track the costs for one week. At the end of the week, she had collected the following data from the pattern department:

a. There were a total of 2,500 bows completed: 1,000 Deluxe models and 1,500 Econo models.

b. There was no BWIP; however, there were 300 units in EWIP: 200 Deluxe and 100 Econo models. Both models were 80% complete with respect to conversion costs and 100% complete with respect to materials.

c. The pattern department experienced the following costs:

d. On an experimental basis, the requisition forms for materials were modified to identify the dollar value of the materials used by the Econo and Deluxe models:

Required:

1. Compute the unit cost for the handles produced by the pattern department assuming that process costing is totally appropriate. Round unit cost to two decimal places.

2. Compute the unit cost of each handle using the separate cost information provided on materials. Round unit cost to two decimal places.

3. Compare the unit costs computed in Requirements 1 and 2. Is Karen justified in her belief that a pure process-costing relationship is not appropriate? Describe the costing system that you would recommend.

4. In the past, the marketing manager has requested more money for advertising the Econo line. Aaron has repeatedly refused to grant any increase in this product's advertising budget because its per-unit profit (selling price minus manufacturing cost) is so low. Given the results in Requirements 1 through 3, was Aaron justified in his position?

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

6

The costs transferred from a prior process to a subsequent process are

A) treated as another type of materials cost for the receiving department.

B) referred to as transferred-in costs (for the receiving department).

C) referred to as the cost of goods transferred out (for the transferring department).

D) all of the above.

E) none of the above.

A) treated as another type of materials cost for the receiving department.

B) referred to as transferred-in costs (for the receiving department).

C) referred to as the cost of goods transferred out (for the transferring department).

D) all of the above.

E) none of the above.

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

7

For September, Murphy Company has manufacturing costs in BWIP equal to $100,000. During September, the manufacturing costs incurred were $550,000. Using the weighted average method, Murphy had 100,000 equivalent units for September. The equivalent unit cost for September is

A) $1.00.

B) $7.50.

C) $6.50.

D) $6.00.

E) $6.62.

A) $1.00.

B) $7.50.

C) $6.50.

D) $6.00.

E) $6.62.

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

8

Transferred-In Cost

Fuerza Inc. produces a protein drink. The product is sold by the gallon. The company has two departments: Mixing and Bottling. For August, the bottling department had 60,000 gallons in beginning inventory (with transferred-in costs of $213,000) and completed 262,500 gallons during the month. Further, the mixing department completed and transferred out 240,000 gallons at a cost of $687,000 in August.

Required:

1. Prepare a physical flow schedule for the bottling department.

2. Calculate equivalent units for the transferred-in category.

3. Calculate the unit cost for the transferred-in category.

Fuerza Inc. produces a protein drink. The product is sold by the gallon. The company has two departments: Mixing and Bottling. For August, the bottling department had 60,000 gallons in beginning inventory (with transferred-in costs of $213,000) and completed 262,500 gallons during the month. Further, the mixing department completed and transferred out 240,000 gallons at a cost of $687,000 in August.

Required:

1. Prepare a physical flow schedule for the bottling department.

2. Calculate equivalent units for the transferred-in category.

3. Calculate the unit cost for the transferred-in category.

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

9

( Appendix 6A ) First-In, First-Out Method; Equivalent Units

Lawson Company produces a product where all manufacturing inputs are applied uniformly. Lawson produced the following physical flow schedule for March:

Required:

Prepare a schedule of equivalent units using the FIFO method.

Lawson Company produces a product where all manufacturing inputs are applied uniformly. Lawson produced the following physical flow schedule for March:

Required:

Prepare a schedule of equivalent units using the FIFO method.

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

10

Equivalent Units; Valuation of Work-in-Process Inventories; First-In, First-Out versus Weighted Average

AKL Foundry manufactures metal components for different kinds of equipment used by the aerospace, commercial aircraft, medical equipment, and electronic industries. The company uses investment casting to produce the required components. Investment casting consists of creating, in wax, a replica of the final product and pouring a hard shell around it. After removing the wax, molten metal is poured into the resulting cavity. What remains after the shell is broken is the desired metal object ready to be put to its designated use.

Metal components pass through eight processes: gating, shell creating, foundry work, cutoff, grinding, finishing, welding, and strengthening. Gating creates the wax mold and clusters the wax pattern around a sprue (a hole through which the molten metal will be poured through the gates into the mold in the foundry process), which is joined and supported by gates (flow channels) to form a tree of patterns. In the shell-creating process, the wax molds are alternately dipped in a ceramic slurry and a fluidized bed of progressively coarser refractory grain until a sufficiently thick shell (or mold) completely encases the wax pattern. After drying, the mold is sent to the foundry process. Here, the wax is melted out of the mold, and the shell is fired, strengthened, and brought to the proper temperature. Molten metal is then poured into the dewaxed shell. Finally, the ceramic shell is removed, and the finished product is sent to the cutoff process, where the parts are separated from the tree by the use of a band saw. The parts are then sent to the grinding process, where the gates that allowed the molten metal to flow into the ceramic cavities are ground off using large abrasive grinders. In the finishing process, rough edges caused by the grinders are removed by small handheld pneumatic tools. Parts that are flawed at this point are sent to welding for corrective treatment. The last process uses heat to treat the parts to bring them to the desired strength.

In 2015, the two partners who owned AKL Foundry decided to split up and divide the business. In dissolving their business relationship, they were faced with the problem of dividing the business assets equitably. Since the company had two plants-one in Arizona and one in New Mexico-a suggestion was made to split the business on the basis of geographic location. One partner would assume ownership of the plant in New Mexico, and the other would assume ownership of the plant in Arizona. However, this arrangement had one major complication: the amount of WIP inventory located in the Arizona plant.