Deck 5: Responsibility Accounting and Transfer Pricing

Full screen (f)

Question

Question

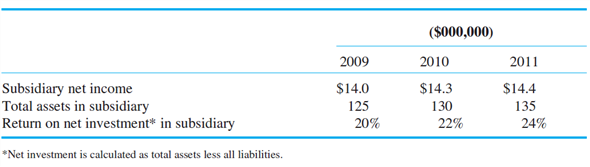

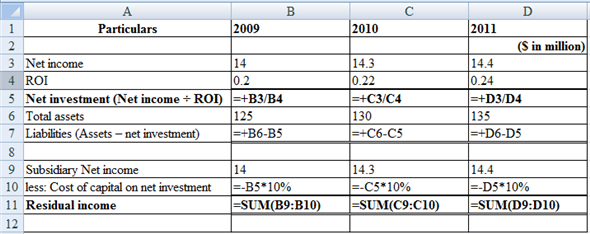

Canadian Subsidiary

The following data summarize the operating performance of your company's wholly owned Canadian subsidiary for 2009 to 2011. The cost of capital for this subsidiary is 10 percent.

Required:

Critically evaluate the performance of this subsidiary.

The following data summarize the operating performance of your company's wholly owned Canadian subsidiary for 2009 to 2011. The cost of capital for this subsidiary is 10 percent.

Required:

Critically evaluate the performance of this subsidiary.

Question

Executive Inn

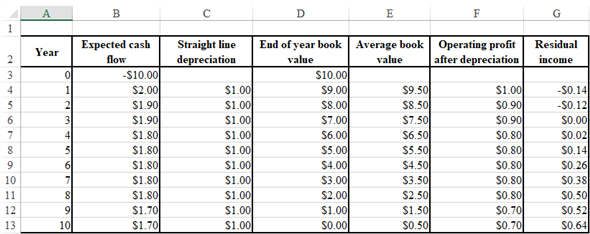

Sarah Adams manages Executive Inn of Toronto, a 200-room facility that rents furnished suites to executives by the month. The market is for people relocating to Toronto and waiting for permanent housing. Adams's compensation contains a fixed component and a bonus based on the net cash flows from operations. She seeks to maximize her compensation. Adams likes her job and has learned a lot, but she expects to be working for a financial institution within five years. Adams's occupancy rate is running at 98 percent, and she is considering a $10 million expansion of the present building to add more rental units. She has very good private knowledge of the future cash flows. In year 1, they will be $2 million and will decline $100,000 a year. The following table summarizes the expansion's cash flows:

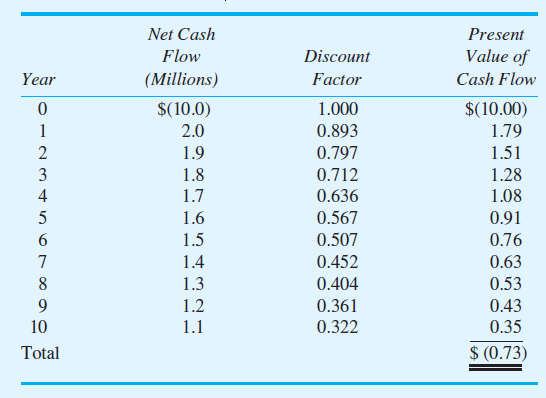

Based on the preceding data, Adams prepares a discounted cash flow analysis of the addition, which is contained in the following report:

The discount factors are based on a weighted-average cost of capital of 12 percent, which accurately reflects the inn's nondiversifiable risk.

Adams's boss, Kathy Judson, manages the Inn Division of Comfort Inc., which has 15 properties

located around North America, including Executive Inn of Toronto. Judson does not have the detailed knowledge of the Toronto hotel/rental market as Adams does. Her general knowledge is not as detailed or as accurate as Adams's. (For the following questions, ignore taxes.)

Required:

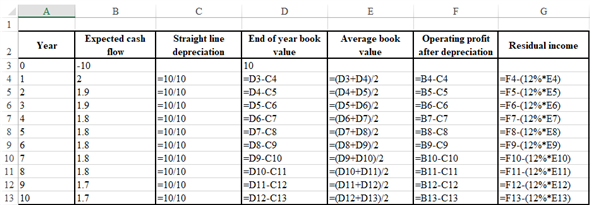

a. The Inn Division of Comfort Inc. has a very crude accounting system that does not assign the depreciation of particular inns to individual managers. As a result, Adams's annual net cash flow statement is based on the operating revenues less operating expenses. Neither the cost of expansion nor depreciation on expanding her inn is charged to her operating statement. Given the facts provided so far, what decision do you expect her to make regarding building the $10 million addition? Explain why.

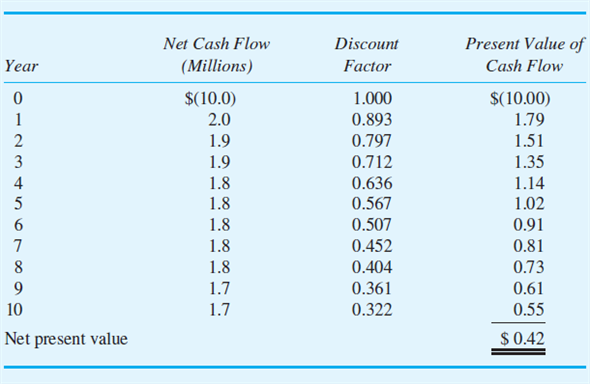

b. Adams prepares the following report for Judson to justify the expansion project:

Judson realizes that Adams's projected cash flows are most likely optimistic, but she does not know how optimistic or even whether or not the project is a positive net present value project. She decides to change Adams's performance measure used in computing her bonus. Adams's compensation will be based on residual income (EVA). Judson also changes the accounting system to track asset expansion and depreciation on the expansion. Adams's profits from operations will now be charged for straight-line depreciation of the expansion using a 10-year life (assume a zero salvage value). Calculate Adams's expected

residual income from the expansion for each of the next 10 years.

c. Based on your calculations in part ( b ), will Adams propose the expansion project? Explain why.

d. Instead of using residual income as Adams's performance measure in part ( b ), Judson uses net cash flows from operations less straight-line depreciation. Will Adams seek to undertake the expansion? Explain why.

e. Reconcile any differences in your answers for parts ( c ) and ( d ).

Sarah Adams manages Executive Inn of Toronto, a 200-room facility that rents furnished suites to executives by the month. The market is for people relocating to Toronto and waiting for permanent housing. Adams's compensation contains a fixed component and a bonus based on the net cash flows from operations. She seeks to maximize her compensation. Adams likes her job and has learned a lot, but she expects to be working for a financial institution within five years. Adams's occupancy rate is running at 98 percent, and she is considering a $10 million expansion of the present building to add more rental units. She has very good private knowledge of the future cash flows. In year 1, they will be $2 million and will decline $100,000 a year. The following table summarizes the expansion's cash flows:

Based on the preceding data, Adams prepares a discounted cash flow analysis of the addition, which is contained in the following report:

The discount factors are based on a weighted-average cost of capital of 12 percent, which accurately reflects the inn's nondiversifiable risk.

Adams's boss, Kathy Judson, manages the Inn Division of Comfort Inc., which has 15 properties

located around North America, including Executive Inn of Toronto. Judson does not have the detailed knowledge of the Toronto hotel/rental market as Adams does. Her general knowledge is not as detailed or as accurate as Adams's. (For the following questions, ignore taxes.)

Required:

a. The Inn Division of Comfort Inc. has a very crude accounting system that does not assign the depreciation of particular inns to individual managers. As a result, Adams's annual net cash flow statement is based on the operating revenues less operating expenses. Neither the cost of expansion nor depreciation on expanding her inn is charged to her operating statement. Given the facts provided so far, what decision do you expect her to make regarding building the $10 million addition? Explain why.

b. Adams prepares the following report for Judson to justify the expansion project:

Judson realizes that Adams's projected cash flows are most likely optimistic, but she does not know how optimistic or even whether or not the project is a positive net present value project. She decides to change Adams's performance measure used in computing her bonus. Adams's compensation will be based on residual income (EVA). Judson also changes the accounting system to track asset expansion and depreciation on the expansion. Adams's profits from operations will now be charged for straight-line depreciation of the expansion using a 10-year life (assume a zero salvage value). Calculate Adams's expected

residual income from the expansion for each of the next 10 years.

c. Based on your calculations in part ( b ), will Adams propose the expansion project? Explain why.

d. Instead of using residual income as Adams's performance measure in part ( b ), Judson uses net cash flows from operations less straight-line depreciation. Will Adams seek to undertake the expansion? Explain why.

e. Reconcile any differences in your answers for parts ( c ) and ( d ).

Question

Question

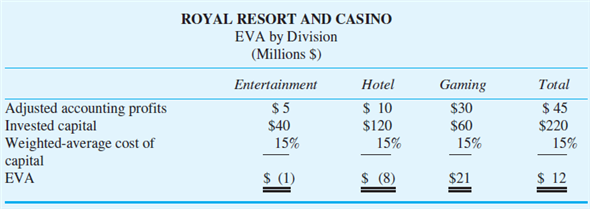

Royal Resort and Casino

Royal Resort and Casino (RRC), a publicly traded company, caters to affluent customers seeking plush surroundings, high-quality food and entertainment, and all the "glitz" associated with the best resorts and casinos. RRC consists of three divisions: hotel, gaming, and entertainment. The hotel division manages the reservation system and lodging operations. Gaming consists of operations, security, and junkets. Junkets offers complimentary air fare and lodging and entertainment at RRC for customers known to wager large sums. The entertainment division consists of restaurants, lounges, catering, and shows. It books lounge shows and top-name entertainment in the theater. Although many of those people attending the shows and eating in the restaurants stay at RRC, customers staying at other hotels and casinos in the area also frequent RRC's shows, restaurants, and gaming operations. The following table disaggregates RRC's total EVA of $12 million into an EVA for each division:

Based on an analysis of similar companies, it is determined that each division has the same weighted-average cost of capital of 15 percent. Across town from RRC is a city block with three separate businesses: Big Horseshoe Slots Casino, Nell's Lounge and Grill, and Sunnyside Motel. These businesses serve a less affluent clientele.

Required:

a. Why does RRC operate as a single firm, whereas Big Horseshoe Slots, Nell's Lounge and Grill, and Sunnyside Motel operate as three separate firms?

b. Describe some of the interdependencies that are likely to exist across RRC's three divisions.

c. Describe some of the internal administrative devices, accounting-based measures, and/or organizational structures that senior managers at RRC can use to control the interdependencies that you described in part (b).

d. Critically evaluate each of the "solutions" you proposed in part (c).

Royal Resort and Casino (RRC), a publicly traded company, caters to affluent customers seeking plush surroundings, high-quality food and entertainment, and all the "glitz" associated with the best resorts and casinos. RRC consists of three divisions: hotel, gaming, and entertainment. The hotel division manages the reservation system and lodging operations. Gaming consists of operations, security, and junkets. Junkets offers complimentary air fare and lodging and entertainment at RRC for customers known to wager large sums. The entertainment division consists of restaurants, lounges, catering, and shows. It books lounge shows and top-name entertainment in the theater. Although many of those people attending the shows and eating in the restaurants stay at RRC, customers staying at other hotels and casinos in the area also frequent RRC's shows, restaurants, and gaming operations. The following table disaggregates RRC's total EVA of $12 million into an EVA for each division:

Based on an analysis of similar companies, it is determined that each division has the same weighted-average cost of capital of 15 percent. Across town from RRC is a city block with three separate businesses: Big Horseshoe Slots Casino, Nell's Lounge and Grill, and Sunnyside Motel. These businesses serve a less affluent clientele.

Required:

a. Why does RRC operate as a single firm, whereas Big Horseshoe Slots, Nell's Lounge and Grill, and Sunnyside Motel operate as three separate firms?

b. Describe some of the interdependencies that are likely to exist across RRC's three divisions.

c. Describe some of the internal administrative devices, accounting-based measures, and/or organizational structures that senior managers at RRC can use to control the interdependencies that you described in part (b).

d. Critically evaluate each of the "solutions" you proposed in part (c).

Question

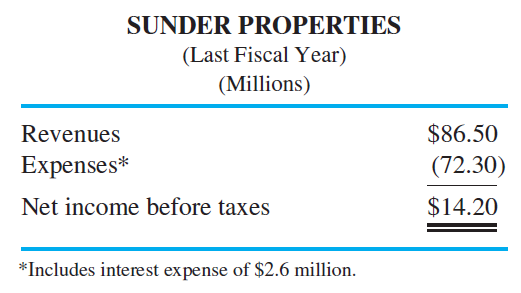

Sunder Properties

Brighton Holdings owns private companies and hires professional managers to run its companies. One company in Brighton Holdings' portfolio is Sunder Properties. Sunder owns and operates apartment complexes, and has the following operating statement.

Brighton Holdings estimates Sunder Properties' before-tax weighted average cost of capital to be 15 percent. Brighton Holdings rewards managers of their operating companies based on the operating company's before-tax return on assets. (The higher the operating company's before-tax ROA, the more Sunder managers are paid.) Sunder Properties' total assets at the end of the last fiscal year are $64 million.

Required:

a. Calculate Sunder's ROA last year.

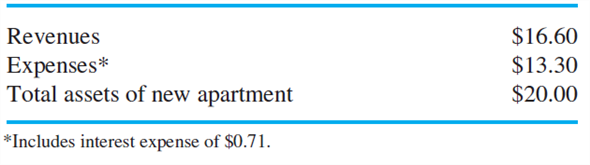

b. Sunder management is considering purchasing a new apartment complex called Valley View that has the following operating characteristics (millions $):

Will the managers of Sunder Properties purchase Valley View?

c. If they had the same information about Valley View as Sunder's management, would the shareholders of Brighton Holdings accept or reject the acquisition of Valley View in part (b)?

d. What advice would you offer the management team of Brighton Holdings?

Brighton Holdings owns private companies and hires professional managers to run its companies. One company in Brighton Holdings' portfolio is Sunder Properties. Sunder owns and operates apartment complexes, and has the following operating statement.

Brighton Holdings estimates Sunder Properties' before-tax weighted average cost of capital to be 15 percent. Brighton Holdings rewards managers of their operating companies based on the operating company's before-tax return on assets. (The higher the operating company's before-tax ROA, the more Sunder managers are paid.) Sunder Properties' total assets at the end of the last fiscal year are $64 million.

Required:

a. Calculate Sunder's ROA last year.

b. Sunder management is considering purchasing a new apartment complex called Valley View that has the following operating characteristics (millions $):

Will the managers of Sunder Properties purchase Valley View?

c. If they had the same information about Valley View as Sunder's management, would the shareholders of Brighton Holdings accept or reject the acquisition of Valley View in part (b)?

d. What advice would you offer the management team of Brighton Holdings?

Question

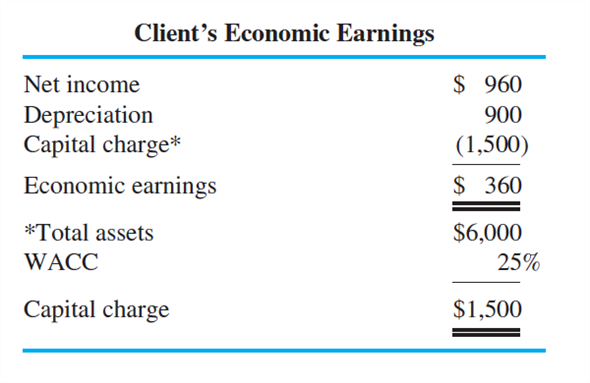

Economic Earnings

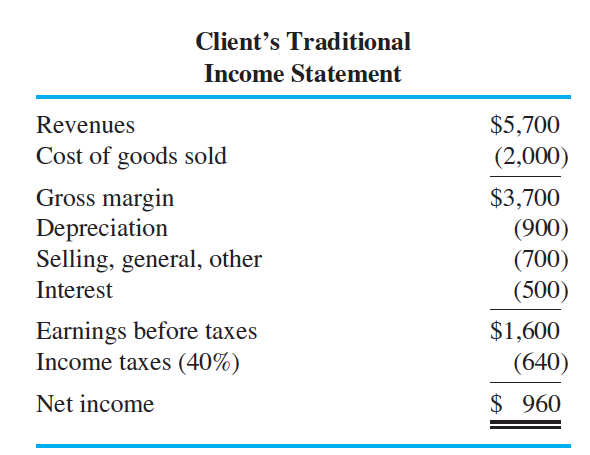

A large consulting firm is looking to expand the services currently offered its clients. The firm has developed a new performance metric called "Economic Earnings," or EE for short. The performance metric is argued to be a better measure of both divisional performance and firmwide performance, and hence "a more rational platform for compensating employees and managers." The consulting firm is seeking to convince clients they should replace their current metrics, such as accounting net income, ROA, EVA, and so forth, with EE.

EE starts with traditional accounting net income but then makes a series of adjustments. The primary adjustment is to add back depreciation and then subtract a required return on invested capital. The consultants argue for adding accounting depreciation back because it is a sunk cost. It does not represent a current cash flow. For example, suppose a client has accounting net income calculated as:

Suppose the client has total assets of $6,000 and a risk-adjusted weighted-average cost of capital (WACC) of 25 percent. Then this client's EE is calculated as follows:

Required:

Critically evaluate EE as a performance measure. What are its strengths and weaknesses?

A large consulting firm is looking to expand the services currently offered its clients. The firm has developed a new performance metric called "Economic Earnings," or EE for short. The performance metric is argued to be a better measure of both divisional performance and firmwide performance, and hence "a more rational platform for compensating employees and managers." The consulting firm is seeking to convince clients they should replace their current metrics, such as accounting net income, ROA, EVA, and so forth, with EE.

EE starts with traditional accounting net income but then makes a series of adjustments. The primary adjustment is to add back depreciation and then subtract a required return on invested capital. The consultants argue for adding accounting depreciation back because it is a sunk cost. It does not represent a current cash flow. For example, suppose a client has accounting net income calculated as:

Suppose the client has total assets of $6,000 and a risk-adjusted weighted-average cost of capital (WACC) of 25 percent. Then this client's EE is calculated as follows:

Required:

Critically evaluate EE as a performance measure. What are its strengths and weaknesses?

Question

Question

Question

Question

Question

Question

Question

Cogen

Cogen Cogen's Turbine Division manufactures gas-powered turbines for generating electric power and hot water for heating systems. Turbine's variable cost per unit is $150,000 and its fixed cost is $1.8 million per month. It has excess capacity. Cogen's Generator Division buys gas turbines from Cogen's Turbine Division and incorporates them into electric steam-generating units. Both divisional managers are evaluated and rewarded as profit centers.

The Generator Division has variable cost of $200,000 per completed unit, excluding the cost of the turbine, and fixed cost of $1.4 million per month. The Generator Division faces the following monthly demand schedule for its complete generating unit (turbine and generator):

Required:

a. If the transfer price of turbines is set at Turbine's variable cost ($150,000), how many turbines will the Generator Division purchase to maximize its profits?

b. The Turbine Division expects to sell a total of 20 turbines a month, which includes both external and

c. If the transfer price of turbines is set at Turbine's (average) full cost calculated in part (b), how many turbines will the Generator Division purchase?

d. Should Cogen use a variable-cost transfer price or a full-cost transfer price to transfer turbines between the Turbine and Generator divisions? Why?

Cogen Cogen's Turbine Division manufactures gas-powered turbines for generating electric power and hot water for heating systems. Turbine's variable cost per unit is $150,000 and its fixed cost is $1.8 million per month. It has excess capacity. Cogen's Generator Division buys gas turbines from Cogen's Turbine Division and incorporates them into electric steam-generating units. Both divisional managers are evaluated and rewarded as profit centers.

The Generator Division has variable cost of $200,000 per completed unit, excluding the cost of the turbine, and fixed cost of $1.4 million per month. The Generator Division faces the following monthly demand schedule for its complete generating unit (turbine and generator):

Required:

a. If the transfer price of turbines is set at Turbine's variable cost ($150,000), how many turbines will the Generator Division purchase to maximize its profits?

b. The Turbine Division expects to sell a total of 20 turbines a month, which includes both external and

c. If the transfer price of turbines is set at Turbine's (average) full cost calculated in part (b), how many turbines will the Generator Division purchase?

d. Should Cogen use a variable-cost transfer price or a full-cost transfer price to transfer turbines between the Turbine and Generator divisions? Why?

Question

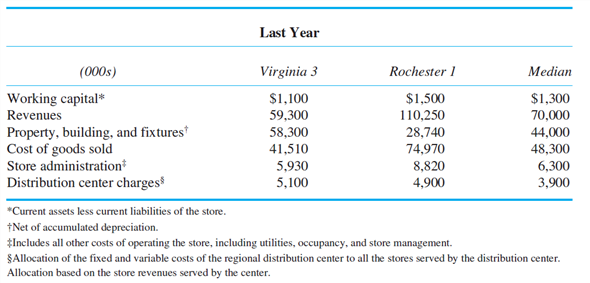

Wegmans

Wegmans, a privately owned regional supermarket chain founded in Rochester, New York, in 1916, focuses on the more affluent market by providing a unique shopping experience and value. Wegmans' much larger stores stock roughly twice as many items as other supermarkets and offer more displays of fresh produce, artisan breads, fresh seafood, and take-out or in-store dining of restaurant-quality entrees. The company currently operates more than 80 stores and 10 regional distribution centers in five states stretching from New York to Virginia. Their most recent expansion is into Virginia with three new stores and a new Wegmans Virginia distribution center serving the three new stores, but with capacity to serve more Virginia stores as they are opened.

As Wegmans expands geographically, it must open regional distribution centers that are responsible for accurate and on-time selection, inventorying, and delivery of the thousands of products (fresh produce, meats, seafood, frozen goods, etc.) sold in the stores in that distribution center's region. Each store in the region is allocated a share of the costs of its distribution center based on total store revenues served by the distribution center.

Senior management uses residual income to evaluate the performance of each store (and reward store management). All Wegmans stores face the same weighted-average cost of capital (13 percent) applied to direct investment in each store (working capital and property, building, and fixtures). The following table summarizes last year's operations of the newest Virginia store (Virginia 3), Wegmans flagship store (Rochester 1), and the Wegmans store with median revenues across the entire 80-store chain (Median). Virginia 3's results in the table represent the first complete year of operations since opening the store. "Rochester 1" is Wegmans' first megastore, rebuilt and expanded in 1990, with a very large and loyal customer base. All figures are in thousands of dollars.

Required:

a. Compute the residual incomes for the Virginia 3, Rochester 1, and the Median stores.

b. Write a memo to senior Wegmans management evaluating the performance of Virginia 3 relative to Rochester 1 and to the Median store. Be sure to provide credible explanations for all material differences in performance between Virginia 3 and the other two Wegmans stores.

Wegmans, a privately owned regional supermarket chain founded in Rochester, New York, in 1916, focuses on the more affluent market by providing a unique shopping experience and value. Wegmans' much larger stores stock roughly twice as many items as other supermarkets and offer more displays of fresh produce, artisan breads, fresh seafood, and take-out or in-store dining of restaurant-quality entrees. The company currently operates more than 80 stores and 10 regional distribution centers in five states stretching from New York to Virginia. Their most recent expansion is into Virginia with three new stores and a new Wegmans Virginia distribution center serving the three new stores, but with capacity to serve more Virginia stores as they are opened.

As Wegmans expands geographically, it must open regional distribution centers that are responsible for accurate and on-time selection, inventorying, and delivery of the thousands of products (fresh produce, meats, seafood, frozen goods, etc.) sold in the stores in that distribution center's region. Each store in the region is allocated a share of the costs of its distribution center based on total store revenues served by the distribution center.

Senior management uses residual income to evaluate the performance of each store (and reward store management). All Wegmans stores face the same weighted-average cost of capital (13 percent) applied to direct investment in each store (working capital and property, building, and fixtures). The following table summarizes last year's operations of the newest Virginia store (Virginia 3), Wegmans flagship store (Rochester 1), and the Wegmans store with median revenues across the entire 80-store chain (Median). Virginia 3's results in the table represent the first complete year of operations since opening the store. "Rochester 1" is Wegmans' first megastore, rebuilt and expanded in 1990, with a very large and loyal customer base. All figures are in thousands of dollars.

Required:

a. Compute the residual incomes for the Virginia 3, Rochester 1, and the Median stores.

b. Write a memo to senior Wegmans management evaluating the performance of Virginia 3 relative to Rochester 1 and to the Median store. Be sure to provide credible explanations for all material differences in performance between Virginia 3 and the other two Wegmans stores.

Question

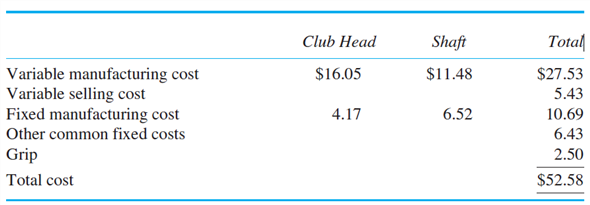

Zee Spin Wedges

Zee Spin manufactures a line of golf club wedges (sand wedge, pitching wedge, lob wedge, and attack wedge) that vary with loft and club head sole design. The wedges have become very popular among professional and serious golfers because of their unique club head design and shafts. All Zee Spin wedges consist of three parts: club head, shaft, and grip. Zee Spin manufactures the club heads and shafts and purchases the grips. The three components are assembled to produce a wedge that is sold to distributors, who then sell them to golf pro shops and websites. The shafts are specially designed to match the playing characteristics of the Zee Spin wedge club head.

The following table summarizes the total costs of producing a complete Zee Spin wedge. All the various models of Zee Spin wedges (sand wedge, pitching wedge, lob wedge, and attack wedge) have the same cost structure.

Zee Spin traditionally only sold complete wedges (club head, shaft, and grip), and the company Was treated as a single profit center. But with the success of the Zee Spin brand and recent inquiries from other club makers about purchasing just Zee Spin shafts, which are unique in the industry, Zee Spin is going to sell both complete wedges (as they do now) and individual shafts. To implement this strategy, Zee Spin will create two profit centers: Wedges and Shafts. The Shaft profit center will produce shafts for external customers, as well as for the Zee Spin Wedge profit center. There will be two profit center managers in Zee Spin that will be rewarded based on the profits of their respective profit centers. The Zee Spin wedges will continue to be sold for $75 per complete wedge, while the shafts will be sold for $23 per shaft.

Shafts that are sold externally will incur variable selling costs of $2.43 (primarily sales commission and shipping). These costs are not incurred for shafts sold internally to the Wedge profit center.

Required:

a. The owners of Zee Spin want to maximize profits and realize that, to properly motivate the managers of the Wedges and Shafts profit centers, they need to set the proper transfer price for the shafts produced by the Shafts profit center and sold to the Wedges profit center. Using the actual data provided in the problem, what transfer price should be used for the shafts produced by the Shafts profit center and sold to the Wedges profit center? (Your answer should be a specific number, such as $18.00.)

b. After implementing the transfer price policy you described in part (a), what problems should the owners of Zee Spin anticipate? Stated differently, what non-firm-value maximizing behaviors by the two profit center managers should the owners of Zee Spin expect to occur?

Zee Spin manufactures a line of golf club wedges (sand wedge, pitching wedge, lob wedge, and attack wedge) that vary with loft and club head sole design. The wedges have become very popular among professional and serious golfers because of their unique club head design and shafts. All Zee Spin wedges consist of three parts: club head, shaft, and grip. Zee Spin manufactures the club heads and shafts and purchases the grips. The three components are assembled to produce a wedge that is sold to distributors, who then sell them to golf pro shops and websites. The shafts are specially designed to match the playing characteristics of the Zee Spin wedge club head.

The following table summarizes the total costs of producing a complete Zee Spin wedge. All the various models of Zee Spin wedges (sand wedge, pitching wedge, lob wedge, and attack wedge) have the same cost structure.

Zee Spin traditionally only sold complete wedges (club head, shaft, and grip), and the company Was treated as a single profit center. But with the success of the Zee Spin brand and recent inquiries from other club makers about purchasing just Zee Spin shafts, which are unique in the industry, Zee Spin is going to sell both complete wedges (as they do now) and individual shafts. To implement this strategy, Zee Spin will create two profit centers: Wedges and Shafts. The Shaft profit center will produce shafts for external customers, as well as for the Zee Spin Wedge profit center. There will be two profit center managers in Zee Spin that will be rewarded based on the profits of their respective profit centers. The Zee Spin wedges will continue to be sold for $75 per complete wedge, while the shafts will be sold for $23 per shaft.

Shafts that are sold externally will incur variable selling costs of $2.43 (primarily sales commission and shipping). These costs are not incurred for shafts sold internally to the Wedge profit center.

Required:

a. The owners of Zee Spin want to maximize profits and realize that, to properly motivate the managers of the Wedges and Shafts profit centers, they need to set the proper transfer price for the shafts produced by the Shafts profit center and sold to the Wedges profit center. Using the actual data provided in the problem, what transfer price should be used for the shafts produced by the Shafts profit center and sold to the Wedges profit center? (Your answer should be a specific number, such as $18.00.)

b. After implementing the transfer price policy you described in part (a), what problems should the owners of Zee Spin anticipate? Stated differently, what non-firm-value maximizing behaviors by the two profit center managers should the owners of Zee Spin expect to occur?

Question

Creative Learning Centers

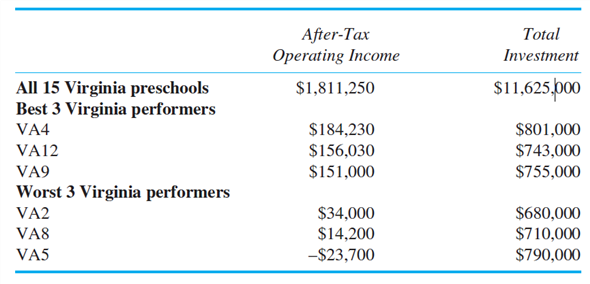

Creative Learning Centers (CLC), a for-profit firm, operates over 100 preschools primarily located in the northeast for children ages 4-6. CLC's innovative curriculum utilizes the latest technology and offers young minds creative expression, language and social skills, physical movement, music, and number skills-all provided by professional trained teachers. CLC leases buildings for their schools and invests substantial resources in leasehold improvements for classrooms, technology, and playground equipment. CLC's cost of capital is 12 percent. Typical tuition is about $6,300 per year for a five-day-a-week, four-hour-per-day program. Maria Schnelling manages 15 CLC schools in the state of Virginia. She has decision-making responsibility for staffing and operating her schools, as well as the responsibility for recommending adding new schools and closing existing schools. The following table provides current operating data on all of her 15 preschools, and breaks out her top- and bottom-performing schools:

"After-tax operating income" represents all revenues less all expenses (including depreciation and taxes but excluding any interest on debt to finance the investment) of running a school for the last 12 months.

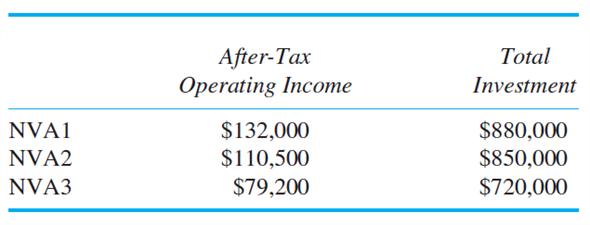

Ms. Schnelling has identified three possible locations for new CLC preschools in Virginia (denoted as NVA1, NVA2, and NVA3).The following table provides current projected data on the three new preschools:

Required:

a. If Maria Schnelling is evaluated and rewarded based on after-tax operating income, which of her 15 existing schools will she recommend closing, and which of her three new schools will she recommend opening? (Justify your answers.)

b. If Maria Schnelling is evaluated and rewarded based on return on investment, which of her existing 15 schools will she recommend closing, and which of her three new schools will she recommend opening? (Show computations.)

c. You have been hired as a consultant to the board of directors to advise the board as to how CLC should measure and reward the performance of CLC managers, such as Ms. Schnelling in Virginia. How should CLC measure and reward its state managers? Provide a compelling rationale to support your recommendation. (Support your recommendation with relevant computations.)

Creative Learning Centers (CLC), a for-profit firm, operates over 100 preschools primarily located in the northeast for children ages 4-6. CLC's innovative curriculum utilizes the latest technology and offers young minds creative expression, language and social skills, physical movement, music, and number skills-all provided by professional trained teachers. CLC leases buildings for their schools and invests substantial resources in leasehold improvements for classrooms, technology, and playground equipment. CLC's cost of capital is 12 percent. Typical tuition is about $6,300 per year for a five-day-a-week, four-hour-per-day program. Maria Schnelling manages 15 CLC schools in the state of Virginia. She has decision-making responsibility for staffing and operating her schools, as well as the responsibility for recommending adding new schools and closing existing schools. The following table provides current operating data on all of her 15 preschools, and breaks out her top- and bottom-performing schools:

"After-tax operating income" represents all revenues less all expenses (including depreciation and taxes but excluding any interest on debt to finance the investment) of running a school for the last 12 months.

Ms. Schnelling has identified three possible locations for new CLC preschools in Virginia (denoted as NVA1, NVA2, and NVA3).The following table provides current projected data on the three new preschools:

Required:

a. If Maria Schnelling is evaluated and rewarded based on after-tax operating income, which of her 15 existing schools will she recommend closing, and which of her three new schools will she recommend opening? (Justify your answers.)

b. If Maria Schnelling is evaluated and rewarded based on return on investment, which of her existing 15 schools will she recommend closing, and which of her three new schools will she recommend opening? (Show computations.)

c. You have been hired as a consultant to the board of directors to advise the board as to how CLC should measure and reward the performance of CLC managers, such as Ms. Schnelling in Virginia. How should CLC measure and reward its state managers? Provide a compelling rationale to support your recommendation. (Support your recommendation with relevant computations.)

Question

Warm Boots

Warm Boots manufactures and sells a patented ski boot with 9-volt batteries designed to keep a skier's feet warm even when the outside temperature reaches -10 °Celsius. Warm Boots is organized into three divisions: Administration (accounting, finance, human resources, CEO, and CFO), Manufacturing, and Marketing and Sales. To promote cost efficiency, Manufacturing is treated as a cost center, where its managweek times the actual average cost of manufacturing the boots in that week. The manager of M S has the discretion to set the price per pair of boots and is paid a bonus based on M S reported profits. The following table summarizes how price and total cost varies with the number of boots produced and sold PER WEEK. "Total Cost" includes both fixed and variable cost where the fixed cost is the annual fixed cost divided by 52 (the number of weeks in the year).

Required:

a. As the head of Manufacturing, how many boots will you manufacture if given the discretion to set production levels? Show calculations to support your answer.

b. If you managed the M S Division of Warm Boots, and given the production level (and its resulting average cost) chosen by the Manufacturing manager in part a, what price (and quantity level) would you choose for a pair of boots that maximizes your bonus? Show calculations to support your answer.

c. Given the decisions of the Manufacturing and M S managers in parts (a) and (b), is the firm maximizing profits? Explain why profits are or are not being maximized.

Warm Boots manufactures and sells a patented ski boot with 9-volt batteries designed to keep a skier's feet warm even when the outside temperature reaches -10 °Celsius. Warm Boots is organized into three divisions: Administration (accounting, finance, human resources, CEO, and CFO), Manufacturing, and Marketing and Sales. To promote cost efficiency, Manufacturing is treated as a cost center, where its managweek times the actual average cost of manufacturing the boots in that week. The manager of M S has the discretion to set the price per pair of boots and is paid a bonus based on M S reported profits. The following table summarizes how price and total cost varies with the number of boots produced and sold PER WEEK. "Total Cost" includes both fixed and variable cost where the fixed cost is the annual fixed cost divided by 52 (the number of weeks in the year).

Required:

a. As the head of Manufacturing, how many boots will you manufacture if given the discretion to set production levels? Show calculations to support your answer.

b. If you managed the M S Division of Warm Boots, and given the production level (and its resulting average cost) chosen by the Manufacturing manager in part a, what price (and quantity level) would you choose for a pair of boots that maximizes your bonus? Show calculations to support your answer.

c. Given the decisions of the Manufacturing and M S managers in parts (a) and (b), is the firm maximizing profits? Explain why profits are or are not being maximized.

Question

University Lab Testing

Joanna Wu manages the University Lab Testing department within the University Hospital. Lab Testing, a profit center, performs most of the standard medical tests (such as blood tests) for other university clinical care units as well as for outside health care providers (independent hospitals, clinics, and physician groups). These outside health care providers are charged a price for each lab test using a predetermined rate schedule. University Hospital health care providers reimburse University Lab Testing using a transfer price formula. Roughly 70 percent of all Lab Testing procedures are performed for University Hospital units and the remainder for outside health care providers. Other lab testing firms in the community perform many of the same tests as Lab Testing. Lab Testing operates at about 85 percent capacity, on average. But when Lab Testing is operating at 100 percent of capacity, it must refuse outside work and even sends some inside- (University Hospital-) generated specimens to other community testing labs.

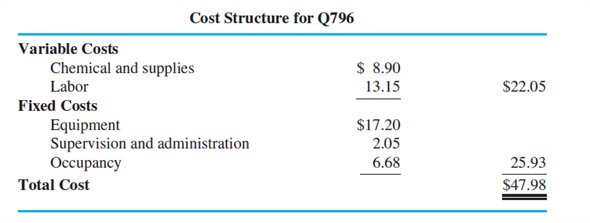

A standard blood test (code Q796) performed by Lab Testing has the following cost structure:

The predetermined rate paid by the outsiders (non-University Hospital health care providers) for this test (Q796) is $68.90.

Required:

a. Suppose Lab Testing has excess capacity. What transfer price maximizes University Hospital's profits?

b. Using the transfer price you chose in part (a), how much profit does Joanna Wu generate for her department if she performs one more Q796 test for an internal University Hospital user?

c. Suppose Lab Testing has no excess capacity. What transfer price maximizes University Hospital's profits?

d. Using the transfer price you chose in part (c), how much profit does Joanna Wu generate for her department if she performs one more Q796 test for an internal University Hospital user?

e. What transfer pricing policy should University Hospital implement regarding other University Hospital clinical care units reimbursing Lab Testing for Q796 blood tests? Be sure to describe the logic (and any administrative problems that you considered) underlying your proposed transfer pricing policy for Q796.

Joanna Wu manages the University Lab Testing department within the University Hospital. Lab Testing, a profit center, performs most of the standard medical tests (such as blood tests) for other university clinical care units as well as for outside health care providers (independent hospitals, clinics, and physician groups). These outside health care providers are charged a price for each lab test using a predetermined rate schedule. University Hospital health care providers reimburse University Lab Testing using a transfer price formula. Roughly 70 percent of all Lab Testing procedures are performed for University Hospital units and the remainder for outside health care providers. Other lab testing firms in the community perform many of the same tests as Lab Testing. Lab Testing operates at about 85 percent capacity, on average. But when Lab Testing is operating at 100 percent of capacity, it must refuse outside work and even sends some inside- (University Hospital-) generated specimens to other community testing labs.

A standard blood test (code Q796) performed by Lab Testing has the following cost structure:

The predetermined rate paid by the outsiders (non-University Hospital health care providers) for this test (Q796) is $68.90.

Required:

a. Suppose Lab Testing has excess capacity. What transfer price maximizes University Hospital's profits?

b. Using the transfer price you chose in part (a), how much profit does Joanna Wu generate for her department if she performs one more Q796 test for an internal University Hospital user?

c. Suppose Lab Testing has no excess capacity. What transfer price maximizes University Hospital's profits?

d. Using the transfer price you chose in part (c), how much profit does Joanna Wu generate for her department if she performs one more Q796 test for an internal University Hospital user?

e. What transfer pricing policy should University Hospital implement regarding other University Hospital clinical care units reimbursing Lab Testing for Q796 blood tests? Be sure to describe the logic (and any administrative problems that you considered) underlying your proposed transfer pricing policy for Q796.

Question

Question

Question

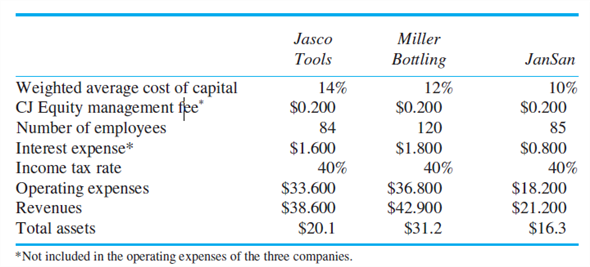

CJ Equity Partners

CJ Equity Partners is a privately held firm that buys small family-owned firms, installs professional managers to run the firms, and then sells them three to five years later, often for a substantial profit. CJ Equity is owned by four partners who raise capital from wealthy investors and invest this money in unrelated firms. Their aim is to provide a 15 percent rate of return on their investors' capital after paying the partners of CJ Equity a management fee. CJ Equity currently owns three operating companies: a tool and die company (Jasco Tools), a chemical bottling company (Miller Bottling), and a janitorial supply company (JanSan). The professional managers running these three companies are paid a fixed salary and bonus based on the performance of their company. Currently, CJ Equity is measuring and rewarding its three professional managers based on the net income after taxes of their individual companies. The following table summarizes the current year's operations of each of the three companies (all dollar amounts in millions):

CJ Equity charges each of the three operating companies an annual management fee of $200,000 for managing the companies, including filing the various tax returns. The weighted average cost of capital represents CJ Equity's estimate of the risk-adjusted, after-tax rate of return of similar companies in each operating company's industry.

You have been hired by CJ Equity as a consultant to recommend whether CJ Equity should change the way it measures the performance of the three companies (net income after taxes), which is then used to compute the professional managers' bonuses.

Required:

a. Design and prepare a performance report for the three operating companies that you believe best measures each operating company's performance and which will be used in computing the three professional managers' bonuses. In other words, using your performance measure, compute the performance of each of the three operating companies.

b. Write a short memo explaining why you believe the performance measure you chose in part (a) best measures the performance of the three professional managers.

CJ Equity Partners is a privately held firm that buys small family-owned firms, installs professional managers to run the firms, and then sells them three to five years later, often for a substantial profit. CJ Equity is owned by four partners who raise capital from wealthy investors and invest this money in unrelated firms. Their aim is to provide a 15 percent rate of return on their investors' capital after paying the partners of CJ Equity a management fee. CJ Equity currently owns three operating companies: a tool and die company (Jasco Tools), a chemical bottling company (Miller Bottling), and a janitorial supply company (JanSan). The professional managers running these three companies are paid a fixed salary and bonus based on the performance of their company. Currently, CJ Equity is measuring and rewarding its three professional managers based on the net income after taxes of their individual companies. The following table summarizes the current year's operations of each of the three companies (all dollar amounts in millions):

CJ Equity charges each of the three operating companies an annual management fee of $200,000 for managing the companies, including filing the various tax returns. The weighted average cost of capital represents CJ Equity's estimate of the risk-adjusted, after-tax rate of return of similar companies in each operating company's industry.

You have been hired by CJ Equity as a consultant to recommend whether CJ Equity should change the way it measures the performance of the three companies (net income after taxes), which is then used to compute the professional managers' bonuses.

Required:

a. Design and prepare a performance report for the three operating companies that you believe best measures each operating company's performance and which will be used in computing the three professional managers' bonuses. In other words, using your performance measure, compute the performance of each of the three operating companies.

b. Write a short memo explaining why you believe the performance measure you chose in part (a) best measures the performance of the three professional managers.

Question

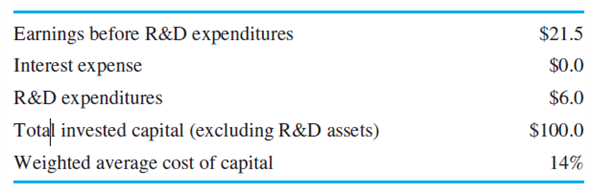

R D Inc.

R D Inc. has the following financial data for the current year (millions):

Assume the tax rate is zero.

Required:

a. R D Inc. writes off R D expenditures as an operating expense. Calculate R D Inc.'s EVA for the current year.

b. R D Inc. decides to capitalize R D and amortize it over three years. R D expenditures for the last three years have been $6.0 million per year. Calculate R D Inc.'s EVA for the current year after capitalizing the current year and previous years' R D and amortizing the capitalized R D balance.

c. In the specific case of R D Inc., how does capitalizing and amortizing R D expenditures instead of expensing R D affect the incentive for managers approaching retirement to underspend on R D at R D Inc.

R D Inc. has the following financial data for the current year (millions):

Assume the tax rate is zero.

Required:

a. R D Inc. writes off R D expenditures as an operating expense. Calculate R D Inc.'s EVA for the current year.

b. R D Inc. decides to capitalize R D and amortize it over three years. R D expenditures for the last three years have been $6.0 million per year. Calculate R D Inc.'s EVA for the current year after capitalizing the current year and previous years' R D and amortizing the capitalized R D balance.

c. In the specific case of R D Inc., how does capitalizing and amortizing R D expenditures instead of expensing R D affect the incentive for managers approaching retirement to underspend on R D at R D Inc.

Question

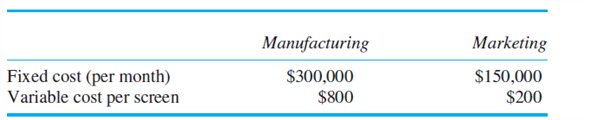

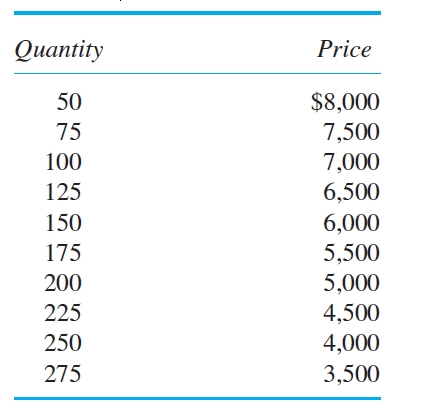

Flat Images

Flat Images develops and manufactures large, state-of-the-art flat-panel television screens that consumer electronic companies purchase and incorporate into a complete TV unit by adding the case, mounting brackets, tuner, amplifier, other electronics, and speakers. Flat Images has just introduced a new high-resolution, high-definition 60-inch screen. Flat Images is composed of two profit centers: Manufacturing and Marketing. Manufacturing produces sets that are sold internally to Marketing. Each profit center has the following cost structure:

Note that Marketing's fixed cost of $150,000 and variable cost of $200 per screen do not contain any transfer price from Manufacturing. The numbers in the preceding table consist only of their own costs, not any costs transferred from the other department. The selling price that Marketing receives for each 60-inch screen depends on the number of screens sold that month, according to the following table: 12

Required:

a. Suppose that Manufacturing sets a transfer price for each screen at $4,800. How many screens will Marketing purchase to maximize Marketing's profits (after Marketing pays Manufacturing $4,800 per screen) and how much profit will Marketing make?

b. At a transfer price of $4,800 per screen, and assuming Marketing buys the number of screens you calculated in part ( a ), how much profit is Manufacturing reporting?

c. At an internal transfer price of $4,800, and assuming Marketing purchases the number of screens you calculate in part ( a ), what is Flat Images' profit?

d. Given the cost structures of Manufacturing and Marketing, and the price-quantity relation given in the problem, how many 60-inch screens should Flat Image manufacture and sell to maximize firmwide profits?

e. If parts ( c ) and ( d ) are the same, explain why they are the same. If they are different, explain why they are different.

f. What transfer price should Flat Images set to maximize firmwide profits? (Give a quantitative number.)

12 An equivalent way to express the price-quantity relation in the table is P = $9,000 - 20 Q, where P = price and Q = quantity.

Flat Images develops and manufactures large, state-of-the-art flat-panel television screens that consumer electronic companies purchase and incorporate into a complete TV unit by adding the case, mounting brackets, tuner, amplifier, other electronics, and speakers. Flat Images has just introduced a new high-resolution, high-definition 60-inch screen. Flat Images is composed of two profit centers: Manufacturing and Marketing. Manufacturing produces sets that are sold internally to Marketing. Each profit center has the following cost structure:

Note that Marketing's fixed cost of $150,000 and variable cost of $200 per screen do not contain any transfer price from Manufacturing. The numbers in the preceding table consist only of their own costs, not any costs transferred from the other department. The selling price that Marketing receives for each 60-inch screen depends on the number of screens sold that month, according to the following table: 12

Required:

a. Suppose that Manufacturing sets a transfer price for each screen at $4,800. How many screens will Marketing purchase to maximize Marketing's profits (after Marketing pays Manufacturing $4,800 per screen) and how much profit will Marketing make?

b. At a transfer price of $4,800 per screen, and assuming Marketing buys the number of screens you calculated in part ( a ), how much profit is Manufacturing reporting?

c. At an internal transfer price of $4,800, and assuming Marketing purchases the number of screens you calculate in part ( a ), what is Flat Images' profit?

d. Given the cost structures of Manufacturing and Marketing, and the price-quantity relation given in the problem, how many 60-inch screens should Flat Image manufacture and sell to maximize firmwide profits?

e. If parts ( c ) and ( d ) are the same, explain why they are the same. If they are different, explain why they are different.

f. What transfer price should Flat Images set to maximize firmwide profits? (Give a quantitative number.)

12 An equivalent way to express the price-quantity relation in the table is P = $9,000 - 20 Q, where P = price and Q = quantity.

Question

Premier Brands

Premier Brands buys and manages consumer personal products brands such as cosmetics, hair care, and personal hygiene. Premier management purchases underperforming brands and redesigns to the mega-retail chains (Walmart and Kmart). Each product line manager is evaluated and rewarded based on return on net assets (RONA). RONA is calculated as net income divided by net assets where net assets is total assets invested in the product line less current liabilities in the product line [RONA = Net income/(Total assets - Current liabilities)]. For every 1 percent of RONA (or fraction thereof) in excess of 12 percent of the product line returns, the product line manager receives a bonus of $250,000. So, if a manager's RONA is 13.68 percent, his or her bonus is $420,000 [(13.68% - 12.00%) × 100 × $250,000]. Premier's weighted average cost of capital (WACC) is 12.43 percent.

Amy Guttman, one of Premier's three product line managers, manages a portfolio of four brands in the hair care business. These four brands currently generate a net income of $708,000, requiring $6.5 million of total assets and $1.3 million of current liabilities. Guttman is evaluating two possible brand acquisitions: Brand 1 and Brand 2. The following table summarizes the salient information about each brand (thousands).

![Premier Brands Premier Brands buys and manages consumer personal products brands such as cosmetics, hair care, and personal hygiene. Premier management purchases underperforming brands and redesigns to the mega-retail chains (Walmart and Kmart). Each product line manager is evaluated and rewarded based on return on net assets (RONA). RONA is calculated as net income divided by net assets where net assets is total assets invested in the product line less current liabilities in the product line [RONA = Net income/(Total assets - Current liabilities)]. For every 1 percent of RONA (or fraction thereof) in excess of 12 percent of the product line returns, the product line manager receives a bonus of $250,000. So, if a manager's RONA is 13.68 percent, his or her bonus is $420,000 [(13.68% - 12.00%) × 100 × $250,000]. Premier's weighted average cost of capital (WACC) is 12.43 percent. Amy Guttman, one of Premier's three product line managers, manages a portfolio of four brands in the hair care business. These four brands currently generate a net income of $708,000, requiring $6.5 million of total assets and $1.3 million of current liabilities. Guttman is evaluating two possible brand acquisitions: Brand 1 and Brand 2. The following table summarizes the salient information about each brand (thousands). Required: a. Given Premier's incentive plan, will Amy Guttman acquire Brand 1 and/or Brand 2, or neither? Justify your answer with supporting calculations. b. Suppose that Premier's WACC is 15.22 percent instead of 12.43 percent, and the bonus system remains as described in the problem. How do Amy's decisions in part ( a ) change? Explain your answer. c. Given the facts as stated in the problem, if you were the sole owner of Premier Products, would you acquire Brand 1 and/or Brand 2, or neither? Justify your answer with supporting calculations. d. Given the facts as stated in the problem, except that Premier's WACC is 15.22 percent instead of 12.43 percent, if you were the sole owner of Premier Products, would you acquire Brand 1 and/or Brand 2, or neither? Justify your answer with supporting calculations. e. Why do some companies use RONA instead of ROA (net income/total assets)? In other words, describe how the incentives generated by using RONA differ from the incentives from using ROA.<div style=padding-top: 35px>](https://storage.examlex.com/SM1501/11eb743f_dd0f_970d_93a8_ddf4b7274641_SM1501_00.jpg)

Required:

a. Given Premier's incentive plan, will Amy Guttman acquire Brand 1 and/or Brand 2, or neither? Justify your answer with supporting calculations.

b. Suppose that Premier's WACC is 15.22 percent instead of 12.43 percent, and the bonus system remains as described in the problem. How do Amy's decisions in part ( a ) change? Explain your answer.

c. Given the facts as stated in the problem, if you were the sole owner of Premier Products, would you acquire Brand 1 and/or Brand 2, or neither? Justify your answer with supporting calculations.

d. Given the facts as stated in the problem, except that Premier's WACC is 15.22 percent instead of 12.43 percent, if you were the sole owner of Premier Products, would you acquire Brand 1 and/or Brand 2, or neither? Justify your answer with supporting calculations.

e. Why do some companies use RONA instead of ROA (net income/total assets)? In other words, describe how the incentives generated by using RONA differ from the incentives from using ROA.

Premier Brands buys and manages consumer personal products brands such as cosmetics, hair care, and personal hygiene. Premier management purchases underperforming brands and redesigns to the mega-retail chains (Walmart and Kmart). Each product line manager is evaluated and rewarded based on return on net assets (RONA). RONA is calculated as net income divided by net assets where net assets is total assets invested in the product line less current liabilities in the product line [RONA = Net income/(Total assets - Current liabilities)]. For every 1 percent of RONA (or fraction thereof) in excess of 12 percent of the product line returns, the product line manager receives a bonus of $250,000. So, if a manager's RONA is 13.68 percent, his or her bonus is $420,000 [(13.68% - 12.00%) × 100 × $250,000]. Premier's weighted average cost of capital (WACC) is 12.43 percent.

Amy Guttman, one of Premier's three product line managers, manages a portfolio of four brands in the hair care business. These four brands currently generate a net income of $708,000, requiring $6.5 million of total assets and $1.3 million of current liabilities. Guttman is evaluating two possible brand acquisitions: Brand 1 and Brand 2. The following table summarizes the salient information about each brand (thousands).

Required:

a. Given Premier's incentive plan, will Amy Guttman acquire Brand 1 and/or Brand 2, or neither? Justify your answer with supporting calculations.

b. Suppose that Premier's WACC is 15.22 percent instead of 12.43 percent, and the bonus system remains as described in the problem. How do Amy's decisions in part ( a ) change? Explain your answer.

c. Given the facts as stated in the problem, if you were the sole owner of Premier Products, would you acquire Brand 1 and/or Brand 2, or neither? Justify your answer with supporting calculations.

d. Given the facts as stated in the problem, except that Premier's WACC is 15.22 percent instead of 12.43 percent, if you were the sole owner of Premier Products, would you acquire Brand 1 and/or Brand 2, or neither? Justify your answer with supporting calculations.

e. Why do some companies use RONA instead of ROA (net income/total assets)? In other words, describe how the incentives generated by using RONA differ from the incentives from using ROA.

Question

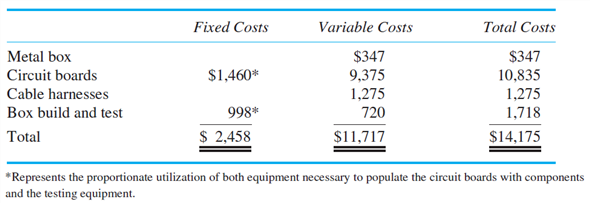

Easton Electronics

Easton Electronics in Irvine, California, is a contract manufacturer that assembles complex solidstate circuit boards for advanced technology companies in the aerospace and health sciences industries. The contract manufacturing industry is very competitive in terms of pricing and performance (quality and on-time delivery). Outsourcing clients specialize in the design of sophisticated electronics products and then rely on their contract manufacturing partners (like Easton) to produce their designs. Once a new product is designed, the advanced technology firm solicits firm, fixed-price bids for the electronic components.

A completed electronic component consists of several assembled circuit boards, a box containing the boards, cables connecting the boards inside the box, cables connecting the box to other components, and exhaustive testing of the complete box build. The technology firm either solicits bids for each separate component (box, boards, and cables) or selects an integrated supplier that can deliver a completely assembled box that has been tested. After receiving the initial bids but prior to selecting the winning bidder, the technology firm selects two or three finalists and then spends considerable resources to qualify new suppliers by sending teams of engineers and purchasing specialists to inspect the bidders' manufacturing facility, procurement process, and quality programs.

Once a contract manufacturer is chosen, most clients are reluctant to switch to new suppliers because of the high search and startup costs of moving to a new supplier. Although some Easton customers source their metal boxes, boards, and cables from different contractors and then assemble the final electronic components into a complete unit that they test, most of Easton clients rely on Easton to provide a complete unit (box, circuit boards, connecting cabling, and final testing).

Easton has recently acquired a wholly owned cable company (TT Cabling). With the acquisition, Easton has two profit centers: Irvine (which manufactures the boards, builds the complete box, and assembles and tests it) and TT Cabling (which only makes and tests the cables). Currently, TT sells most of its cables to a different set of customers than those who have their boards built by Easton.

After the acquisition, Easton has a single sales force that sells board assembly, box build, and cables.

Easton assembles the electronic controller for a particular health imaging system for Scopics Imaging (SI). Easton manufactures the circuit boards, buys a sheet metal box designed specifically to house the boards, buys the cables to connect the boards within the box and other cables to connect the box to other components, tests the box, and delivers the completed unit to SI to plug the box intoits imaging system.

Irvine currently purchases four cables for the SI program. The following table summarizes Irvine's cost for ONE complete SI box:

Although Irvine purchases the cables for the SI program from an outside cable company, Easton senior managers are analyzing whether to have TT Cabling supply these cables. The managers of TT Cabling have submitted a bid to Irvine of $1,700 for the four cables in the SI assembly. The Irvine managers oppose buying the cables from TT because the TT bid of $1,700 is significantly higher than the outside cable supplier ($1,275). The bid of $1,700 submitted by TT for the four SI cables consists of variable costs of $1,000, fixed manufacturing costs of $300, and profits of $400.

The quality of the TT cables (including reliability of delivery schedule) is the same for both the TT cables and the outside supplier of cables.

When bidding on new proposals that involve complete box builds, Easton management wonders

whether they should continue to solicit price quotes from outside cable suppliers only, solicit bids from both outside cable suppliers and TT, or only get price quotes from TT Cabling.

Required:

Write a memo to the senior managers of Easton electronics proposing a policy that describes how Easton should decide whether to purchase cables externally or internally (through TT). The memo should describe the decision-making process, the relevant considerations, and the underlying objectives of such a policy. Use the SI cables as an example of how your Easton cable sourcing policy should be applied.

Easton Electronics in Irvine, California, is a contract manufacturer that assembles complex solidstate circuit boards for advanced technology companies in the aerospace and health sciences industries. The contract manufacturing industry is very competitive in terms of pricing and performance (quality and on-time delivery). Outsourcing clients specialize in the design of sophisticated electronics products and then rely on their contract manufacturing partners (like Easton) to produce their designs. Once a new product is designed, the advanced technology firm solicits firm, fixed-price bids for the electronic components.

A completed electronic component consists of several assembled circuit boards, a box containing the boards, cables connecting the boards inside the box, cables connecting the box to other components, and exhaustive testing of the complete box build. The technology firm either solicits bids for each separate component (box, boards, and cables) or selects an integrated supplier that can deliver a completely assembled box that has been tested. After receiving the initial bids but prior to selecting the winning bidder, the technology firm selects two or three finalists and then spends considerable resources to qualify new suppliers by sending teams of engineers and purchasing specialists to inspect the bidders' manufacturing facility, procurement process, and quality programs.

Once a contract manufacturer is chosen, most clients are reluctant to switch to new suppliers because of the high search and startup costs of moving to a new supplier. Although some Easton customers source their metal boxes, boards, and cables from different contractors and then assemble the final electronic components into a complete unit that they test, most of Easton clients rely on Easton to provide a complete unit (box, circuit boards, connecting cabling, and final testing).

Easton has recently acquired a wholly owned cable company (TT Cabling). With the acquisition, Easton has two profit centers: Irvine (which manufactures the boards, builds the complete box, and assembles and tests it) and TT Cabling (which only makes and tests the cables). Currently, TT sells most of its cables to a different set of customers than those who have their boards built by Easton.

After the acquisition, Easton has a single sales force that sells board assembly, box build, and cables.

Easton assembles the electronic controller for a particular health imaging system for Scopics Imaging (SI). Easton manufactures the circuit boards, buys a sheet metal box designed specifically to house the boards, buys the cables to connect the boards within the box and other cables to connect the box to other components, tests the box, and delivers the completed unit to SI to plug the box intoits imaging system.

Irvine currently purchases four cables for the SI program. The following table summarizes Irvine's cost for ONE complete SI box:

Although Irvine purchases the cables for the SI program from an outside cable company, Easton senior managers are analyzing whether to have TT Cabling supply these cables. The managers of TT Cabling have submitted a bid to Irvine of $1,700 for the four cables in the SI assembly. The Irvine managers oppose buying the cables from TT because the TT bid of $1,700 is significantly higher than the outside cable supplier ($1,275). The bid of $1,700 submitted by TT for the four SI cables consists of variable costs of $1,000, fixed manufacturing costs of $300, and profits of $400.

The quality of the TT cables (including reliability of delivery schedule) is the same for both the TT cables and the outside supplier of cables.

When bidding on new proposals that involve complete box builds, Easton management wonders

whether they should continue to solicit price quotes from outside cable suppliers only, solicit bids from both outside cable suppliers and TT, or only get price quotes from TT Cabling.

Required:

Write a memo to the senior managers of Easton electronics proposing a policy that describes how Easton should decide whether to purchase cables externally or internally (through TT). The memo should describe the decision-making process, the relevant considerations, and the underlying objectives of such a policy. Use the SI cables as an example of how your Easton cable sourcing policy should be applied.

Question

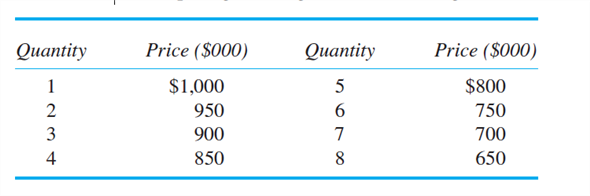

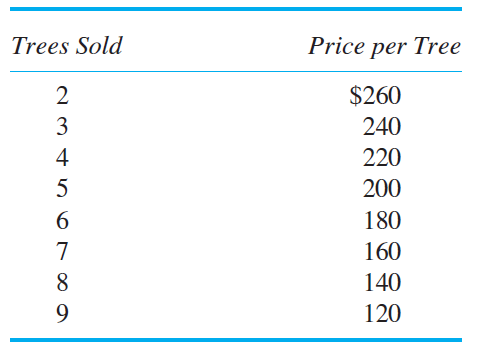

Evergreen Nursery and Landscape

Evergreen Nursery and Landscape has two profit centers: Nursery and Landscape. Nursery buys young evergreen trees, grows them for a year, and then sells them to Landscape. Landscape then sells and plants them for residential customers. Nursery only sells its trees to Landscape, and Landscape only buys trees from Nursery. Landscape faces the following demand curve per month for planted trees by residential customers:

( Note: The demand curve in the table can be represented as P = 300 - 20 Q. )

Nursery has variable costs of $10 per tree and fixed costs of $210 per month. Landscape has variable costs of $50 per tree (before paying Nursery a transfer price for the tree) and fixed costs of $290 per month.

Required:

a. Assume the owner of Evergreen Nursery and Landscape knows all the costs of both divisions and the demand curve. If the owner sets the price for trees planted by Landscape, what final price for a planted tree would the owner set to maximize her profits and how many trees per month get planted?

b. Suppose the owner does not know the demand curve faced by Landscape, but she does know each division's fixed and variable costs. What transfer price would the owner set to maximize her profits?

c. Suppose that Nursery sets the transfer price at $75 per tree. How many trees will Landscape purchase from Nursery and plant per month in order to maximize Landscape's profits (including the transfer price of $75 per tree)?

d. What is Nursery's profit from setting a transfer price of $75, assuming Landscape maximizes its profits as in part ( c )?

e. Compare the firmwide profits that result from the transfer price chosen in part ( b ) and the firmwide profits that result from a $75 transfer price chosen in part ( c ), and explain why they are either the same or different.

Evergreen Nursery and Landscape has two profit centers: Nursery and Landscape. Nursery buys young evergreen trees, grows them for a year, and then sells them to Landscape. Landscape then sells and plants them for residential customers. Nursery only sells its trees to Landscape, and Landscape only buys trees from Nursery. Landscape faces the following demand curve per month for planted trees by residential customers:

( Note: The demand curve in the table can be represented as P = 300 - 20 Q. )

Nursery has variable costs of $10 per tree and fixed costs of $210 per month. Landscape has variable costs of $50 per tree (before paying Nursery a transfer price for the tree) and fixed costs of $290 per month.

Required:

a. Assume the owner of Evergreen Nursery and Landscape knows all the costs of both divisions and the demand curve. If the owner sets the price for trees planted by Landscape, what final price for a planted tree would the owner set to maximize her profits and how many trees per month get planted?

b. Suppose the owner does not know the demand curve faced by Landscape, but she does know each division's fixed and variable costs. What transfer price would the owner set to maximize her profits?

c. Suppose that Nursery sets the transfer price at $75 per tree. How many trees will Landscape purchase from Nursery and plant per month in order to maximize Landscape's profits (including the transfer price of $75 per tree)?

d. What is Nursery's profit from setting a transfer price of $75, assuming Landscape maximizes its profits as in part ( c )?

e. Compare the firmwide profits that result from the transfer price chosen in part ( b ) and the firmwide profits that result from a $75 transfer price chosen in part ( c ), and explain why they are either the same or different.

Question

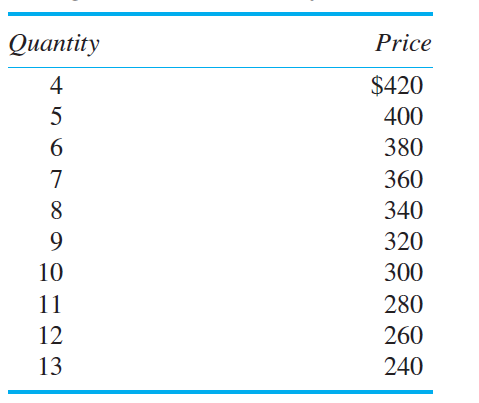

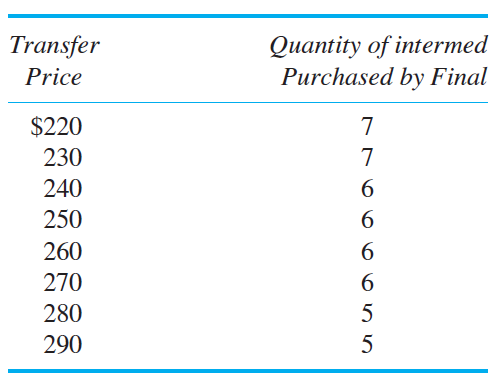

Transfer Price Company

The Transfer Price Company has two divisions (Intermediate and Final) that report to the corporate office (Corporate). The two divisions are profit centers. Intermediate produces a proprietary product (called " intermed ") that it sells both inside the firm to Final and outside the firm. Final can only purchase intermed from Intermediate because Intermediate holds the patent to manufacture intermed. Intermed's variable cost is $15 per unit, and Intermediate has excess capacity in the sense that it can

satisfy demand from both its outside customers and Final. Final buys one intermed from Intermediate, incurs an additional variable cost of $5 per unit, and sells the product (called " final ") to external consumers. Final faces the following demand schedule for final.

(The preceding demand schedule can be represented algebraically as: P = $500 - 20 Q.)

Required:

a. Calculate the quantity-price combination of final that maximizes firm value. In other words, if Corporate knew the variable costs of the two divisions, for what price would they sell final, and how many units of intermed would Corporate tell Intermediate to produce and transfer to Final?

b. Assume that the managers in Corporate do not know the variable costs in the two divisions. Intermediate has the decision rights to set the transfer price of intermed to Final. Intermediate knows Final's variable cost of $5 and the demand schedule Final faces for selling final to its customers. Intermediate, therefore, knows that the following schedule explains how many units of intermed Final will purchase given the transfer price Intermediate sets:

In other words, if Intermediate sets a transfer price of $260, Final will purchase six units of intermed and produce 6 units of final. Given the above schedule of possible transfer prices that Intermediate can choose, what transfer price will Intermediate set to maximize its profits?

c. While Corporate does not know intermed's variable cost, it does know that the total cost of intermed is $48 per unit. This $48 per unit cost consists of both the variable costs to manufacture intermed plus the allocated fixed manufacturing costs. Intermediate allocates all its fixed costs over all the products it produces, including intermed. If Corporate sets the transfer price of intermed at $48, how many units of intermed will Final purchase?

d. What is the dollar impact on Intermediate's profits if Final purchases the number of intermeds calculated in part ( c )?

e. Should Corporate allow Intermediate to set the transfer price for intermed that you calculated in part ( b ), or should Corporate set the transfer price at $48 as in part ( c )? Support your recommendation with a quantitative analysis.

The Transfer Price Company has two divisions (Intermediate and Final) that report to the corporate office (Corporate). The two divisions are profit centers. Intermediate produces a proprietary product (called " intermed ") that it sells both inside the firm to Final and outside the firm. Final can only purchase intermed from Intermediate because Intermediate holds the patent to manufacture intermed. Intermed's variable cost is $15 per unit, and Intermediate has excess capacity in the sense that it can

satisfy demand from both its outside customers and Final. Final buys one intermed from Intermediate, incurs an additional variable cost of $5 per unit, and sells the product (called " final ") to external consumers. Final faces the following demand schedule for final.

(The preceding demand schedule can be represented algebraically as: P = $500 - 20 Q.)

Required:

a. Calculate the quantity-price combination of final that maximizes firm value. In other words, if Corporate knew the variable costs of the two divisions, for what price would they sell final, and how many units of intermed would Corporate tell Intermediate to produce and transfer to Final?

b. Assume that the managers in Corporate do not know the variable costs in the two divisions. Intermediate has the decision rights to set the transfer price of intermed to Final. Intermediate knows Final's variable cost of $5 and the demand schedule Final faces for selling final to its customers. Intermediate, therefore, knows that the following schedule explains how many units of intermed Final will purchase given the transfer price Intermediate sets:

In other words, if Intermediate sets a transfer price of $260, Final will purchase six units of intermed and produce 6 units of final. Given the above schedule of possible transfer prices that Intermediate can choose, what transfer price will Intermediate set to maximize its profits?

c. While Corporate does not know intermed's variable cost, it does know that the total cost of intermed is $48 per unit. This $48 per unit cost consists of both the variable costs to manufacture intermed plus the allocated fixed manufacturing costs. Intermediate allocates all its fixed costs over all the products it produces, including intermed. If Corporate sets the transfer price of intermed at $48, how many units of intermed will Final purchase?

d. What is the dollar impact on Intermediate's profits if Final purchases the number of intermeds calculated in part ( c )?

e. Should Corporate allow Intermediate to set the transfer price for intermed that you calculated in part ( b ), or should Corporate set the transfer price at $48 as in part ( c )? Support your recommendation with a quantitative analysis.

Question

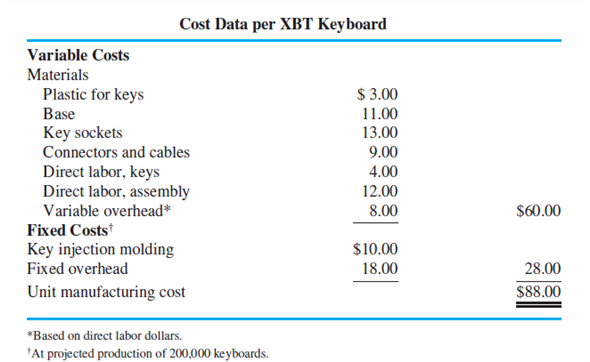

XBT Keyboards The keyboard division of XBT, a personal computer manufacturing firm, fabricates 50-key keyboards for both XBT and non-XBT computers. Keyboards for XBT machines are included as part of the XBT personal computer and are also sold separately. The keyboard division is a profit center. Keyboards included as part of the XBT PCs are transferred to the PC division at variable cost ($60) plus a 20 percent markup. The same keyboard, when sold separately (as a replacement part) or sold for non-XBT machines, is priced at $100. Projected sales are 50,000 keyboards transferred to the PC division (included as part of the XBT PC) and 150,000 keyboards sold externally. The keys for the keyboard are fabricated by XBT on leased plastic injection-molding machines and then placed in purchased key sockets. These keys and sockets are assembled into a base, and connectors and cables are attached. Ten million keys are molded each year on four machines to meet the projected demand of 200,000 keyboards. Molding machines are leased for $500,000 per year per machine; maximum practical capacity is 2.5 million keys per machine per year. The variable overhead account includes all of the variable factory overhead costs for both key manufacturing and assembly. Studies have shown that variable overhead is more highly correlated with direct labor dollars than any other volume measure.

Sara Litle, manager of the keyboard division, is considering a proposal to buy some keys from an outside vendor instead of fabricating them inside XBT. These keys (which do not include the sockets) will be used in the keyboards included with XBT PCs but not in keyboards sold separately or sold to non-XBT computer manufacturers. The lease on one of XBT's key injection-molding machines is about to expire and the capacity it provides can be easily shifted to the outside vendor.

The outside vendor will produce keys for $0.39 per key and will guarantee capacity of at least 2.5 million keys per year. Litle is compensated based on the profits of the keyboard division. She is considering returning one of the injection-molding machines when its lease expires and purchasing keys from the outside vendor.

Required:

a. How much will XBT save per key if it outsources the 2.5 million keys rather than producing them internally?

b. What decision do you expect Sara Litle to make? Explain why.

c. If you were a large shareholder of XBT and knew all the facts, would you make the same decision as Litle? Explain.

d. What changes in XBT's accounting system and/or organizational structure would you suggest, given the facts of the case? Explain why.