Deck 7: Cost-Volume-Profit Analysis

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

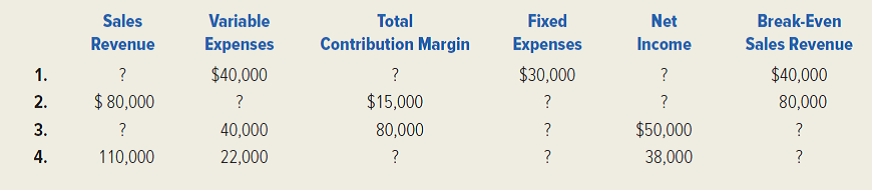

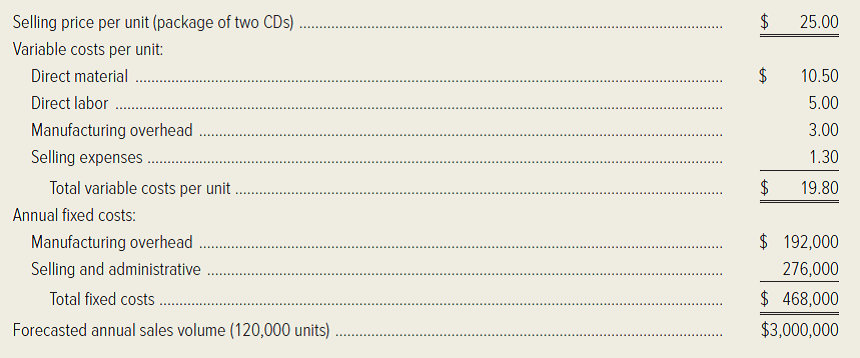

Fill in the missing data for each of the following independent cases. (Ignore income taxes.)

Question

Question

Question

Question

Refer to the data given in the preceding exercise. (Ignore income taxes.)

Required:

1. Prepare a fully labeled profit-volume graph for the Houston Armadillos.

2. What is the safety margin for the baseball franchise if the team plays a 12-game season and the team owner expects the stadium to be 30 percent full for each game?

3. If the stadium is half full for each game, what ticket price would the team have to charge in order to break even?

Required:

1. Prepare a fully labeled profit-volume graph for the Houston Armadillos.

2. What is the safety margin for the baseball franchise if the team plays a 12-game season and the team owner expects the stadium to be 30 percent full for each game?

3. If the stadium is half full for each game, what ticket price would the team have to charge in order to break even?

Question

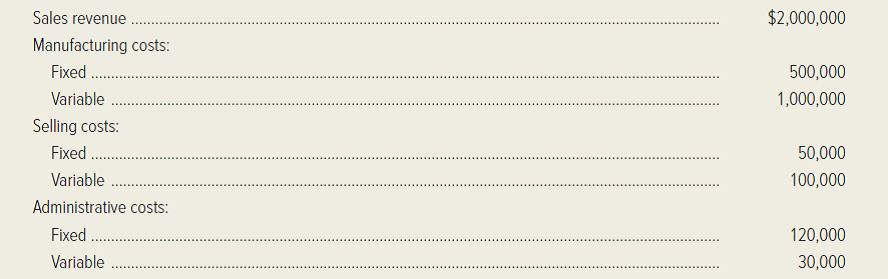

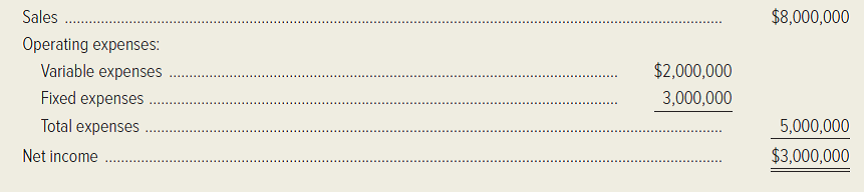

Europa Publications, Inc. specializes in reference books that keep abreast of the rapidly changing political and economic issues in Europe. The results of the company's operations during the prior year are given in the following table. All units produced during the year were sold. (Ignore income taxes.)

Required:

1. Prepare a traditional income statement and a contribution income statement for the company.

2. What is the firm's operating leverage for the sales volume generated during the prior year?

3. Suppose sales revenue increases by 10 percent. What will be the percentage increase in net income?

4. Which income statement would an operating manager use to answer requirement (3)? Why?

Required:

1. Prepare a traditional income statement and a contribution income statement for the company.

2. What is the firm's operating leverage for the sales volume generated during the prior year?

3. Suppose sales revenue increases by 10 percent. What will be the percentage increase in net income?

4. Which income statement would an operating manager use to answer requirement (3)? Why?

Question

Tim's Bicycle Shop sells 21-speed bicycles. For purposes of a cost-volume-profit analysis, the shop owner has divided sales into two categories, as follows:

Three-quarters of the shop's sales are medium-quality bikes. The shop's annual fixed expenses are $65,000. (In the following requirements, ignore income taxes.)

Required:

1. Compute the unit contribution margin for each product type.

2. What is the shop's sales mix?

3. Compute the weighted-average unit contribution margin, assuming a constant sales mix.

4. What is the shop's break-even sales volume in dollars? Assume a constant sales mix.

5. How many bicycles of each type must be sold to earn a target net income of $48,750? Assume a constant sales mix.

Three-quarters of the shop's sales are medium-quality bikes. The shop's annual fixed expenses are $65,000. (In the following requirements, ignore income taxes.)

Required:

1. Compute the unit contribution margin for each product type.

2. What is the shop's sales mix?

3. Compute the weighted-average unit contribution margin, assuming a constant sales mix.

4. What is the shop's break-even sales volume in dollars? Assume a constant sales mix.

5. How many bicycles of each type must be sold to earn a target net income of $48,750? Assume a constant sales mix.

Question

Use the Internet to access the website of one of these airlines, or a different airline of your choosing.

Required: Find the company's most recent annual report. Does the management discussion in the report disclose the airline's break-even load factor? If so, what is it for the most recent year reported?

Required: Find the company's most recent annual report. Does the management discussion in the report disclose the airline's break-even load factor? If so, what is it for the most recent year reported?

Question

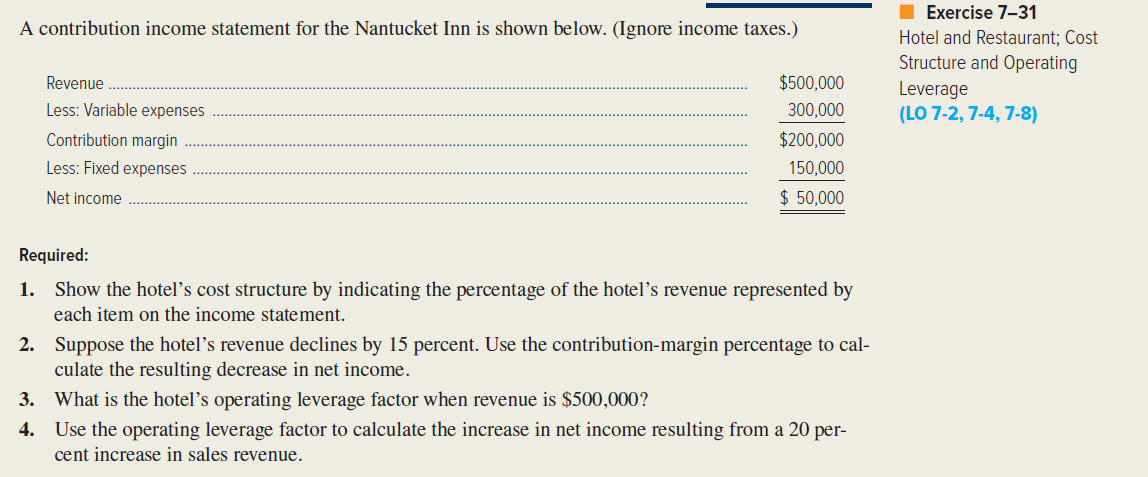

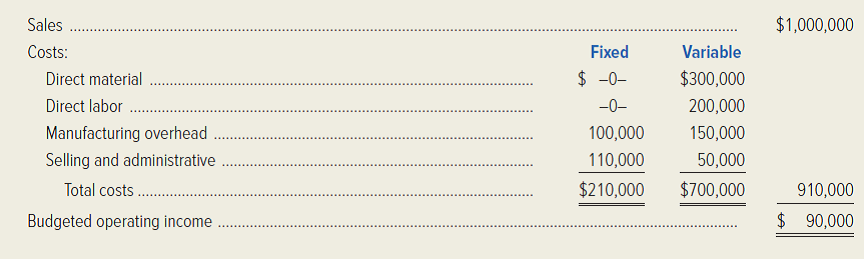

A contribution income statement for the Nantucket Inn is shown below. (Ignore income taxes.)

Required:

1. Show the hotel's cost structure by indicating the percentage of the hotel's revenue represented by each item on the income statement.

2. Suppose the hotel's revenue declines by 15 percent. Use the contribution-margin percentage to calculate the resulting decrease in net income.

3. What is the hotel's operating leverage factor when revenue is $500,000?

4. Use the operating leverage factor to calculate the increase in net income resulting from a 20 percent increase in sales revenue.

Required:

1. Show the hotel's cost structure by indicating the percentage of the hotel's revenue represented by each item on the income statement.

2. Suppose the hotel's revenue declines by 15 percent. Use the contribution-margin percentage to calculate the resulting decrease in net income.

3. What is the hotel's operating leverage factor when revenue is $500,000?

4. Use the operating leverage factor to calculate the increase in net income resulting from a 20 percent increase in sales revenue.

Question

Refer to the income statement given in the preceding exercise. Prepare a new contribution income statement for the Nantucket Inn in each of the following independent situations. (Ignore income taxes.)

1. The hotel's volume of activity increases by 20 percent, and fixed expenses increase by 40 percent.

2. The ratio of variable expenses to revenue doubles. There is no change in the hotel's volume of activity. Fixed expenses decline by $25,000.

1. The hotel's volume of activity increases by 20 percent, and fixed expenses increase by 40 percent.

2. The ratio of variable expenses to revenue doubles. There is no change in the hotel's volume of activity. Fixed expenses decline by $25,000.

Question

Question

Question

Question

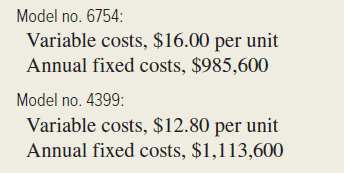

Corrigan Enterprises is studying the acquisition of two electrical component insertion systems for producing its sole product, the universal gismo. Data relevant to the systems follow.

Corrigan's selling price is $64 per unit for the universal gismo, which is subject to a 5 percent sales commission. (In the following requirements, ignore income taxes.)

Required:

1. How many units must the company sell to break even if Model 6754 is selected?

2. Which of the two systems would be more profitable if sales and production are expected to average 46,000 units per year?

3. Assume Model 4399 requires the purchase of additional equipment that is not reflected in the preceding figures. The equipment will cost $450,000 and will be depreciated over a five-year life by the straight-line method. How many units must Corrigan sell to earn $956,400 of income if Model 4399 is selected? As in requirement (2), sales and production are expected to average 46,000 units per year.

4. Ignoring the information presented in requirement (3), at what volume level will management be indifferent between the acquisition of Model 6754 and Model 4399? In other words, at what volume level will the annual total cost of each system be equal? ( Hint: At any given sales volume, sales commissions will be the same amount regardless of which model is selected.)

Corrigan's selling price is $64 per unit for the universal gismo, which is subject to a 5 percent sales commission. (In the following requirements, ignore income taxes.)

Required:

1. How many units must the company sell to break even if Model 6754 is selected?

2. Which of the two systems would be more profitable if sales and production are expected to average 46,000 units per year?

3. Assume Model 4399 requires the purchase of additional equipment that is not reflected in the preceding figures. The equipment will cost $450,000 and will be depreciated over a five-year life by the straight-line method. How many units must Corrigan sell to earn $956,400 of income if Model 4399 is selected? As in requirement (2), sales and production are expected to average 46,000 units per year.

4. Ignoring the information presented in requirement (3), at what volume level will management be indifferent between the acquisition of Model 6754 and Model 4399? In other words, at what volume level will the annual total cost of each system be equal? ( Hint: At any given sales volume, sales commissions will be the same amount regardless of which model is selected.)

Question

Houston-based Advanced Electronics manufactures audio speakers for desktop computers. The following data relate to the period just ended when the company produced and sold 42,000 speaker sets:

Management is considering relocating its manufacturing facilities to northern Mexico to reduce costs. Variable costs are expected to average $18 per set; annual fixed costs are anticipated to be $1,984,000. (In the following requirements, ignore income taxes.)

Required:

1. Calculate the company's current income and determine the level of dollar sales needed to double that figure, assuming that manufacturing operations remain in the United States.

2. Determine the break-even point in speaker sets if operations are shifted to Mexico.

3. Assume that management desires to achieve the Mexican break-even point; however, operations will remain in the United States.

a. If variable costs remain constant, what must management do to fixed costs? By how much must fixed costs change?

b. If fixed costs remain constant, what must management do to the variable cost per unit? By how much must unit variable cost change?

4. Determine the impact (increase, decrease, or no effect) of the following operating changes.

a. Effect of an increase in direct material costs on the break-even point.

b. Effect of an increase in fixed administrative costs on the unit contribution margin.

c. Effect of an increase in the unit contribution margin on net income.

d. Effect of a decrease in the number of units sold on the break-even point.

Management is considering relocating its manufacturing facilities to northern Mexico to reduce costs. Variable costs are expected to average $18 per set; annual fixed costs are anticipated to be $1,984,000. (In the following requirements, ignore income taxes.)

Required:

1. Calculate the company's current income and determine the level of dollar sales needed to double that figure, assuming that manufacturing operations remain in the United States.

2. Determine the break-even point in speaker sets if operations are shifted to Mexico.

3. Assume that management desires to achieve the Mexican break-even point; however, operations will remain in the United States.

a. If variable costs remain constant, what must management do to fixed costs? By how much must fixed costs change?

b. If fixed costs remain constant, what must management do to the variable cost per unit? By how much must unit variable cost change?

4. Determine the impact (increase, decrease, or no effect) of the following operating changes.

a. Effect of an increase in direct material costs on the break-even point.

b. Effect of an increase in fixed administrative costs on the unit contribution margin.

c. Effect of an increase in the unit contribution margin on net income.

d. Effect of a decrease in the number of units sold on the break-even point.

Question

Lawrence Corporation sells two ceiling fans, Deluxe and Basic. Current sales total 60,000 units, consisting of 39,000 Deluxe units and 21,000 Basic units. Selling price and variable cost information follow.

Salespeople currently receive flat salaries that total $400,000. Management is contemplating a change to a compensation plan that is based on commissions in an effort to boost the company's presence in the marketplace. Two plans are under consideration:

Required:

1. Define the term sales mix.

2. Comparing Plan A to the current compensation arrangement:

a. Will Plan A achieve management's objective of an increased presence in the marketplace? Briefly explain.

b. From a sales-mix perspective, will the salespeople be promoting the product that one would logically expect? Briefly discuss.

c. Will the sales force likely be satisfied with the results of Plan A? Why?

d. Will Lawrence likely be satisfied with the resulting impact of Plan A on company profitability? Why?

3. Assume that Plan B is under consideration.

a. Compare Plan A and Plan B with respect to total units sold and the sales mix. Comment on the results.

b. In comparison with flat salaries, is Plan B more attractive to the sales force? To the company? Show calculations to support your answers.

Salespeople currently receive flat salaries that total $400,000. Management is contemplating a change to a compensation plan that is based on commissions in an effort to boost the company's presence in the marketplace. Two plans are under consideration:

Required:

1. Define the term sales mix.

2. Comparing Plan A to the current compensation arrangement:

a. Will Plan A achieve management's objective of an increased presence in the marketplace? Briefly explain.

b. From a sales-mix perspective, will the salespeople be promoting the product that one would logically expect? Briefly discuss.

c. Will the sales force likely be satisfied with the results of Plan A? Why?

d. Will Lawrence likely be satisfied with the resulting impact of Plan A on company profitability? Why?

3. Assume that Plan B is under consideration.

a. Compare Plan A and Plan B with respect to total units sold and the sales mix. Comment on the results.

b. In comparison with flat salaries, is Plan B more attractive to the sales force? To the company? Show calculations to support your answers.

Question

Consolidated Industries is studying the addition of a new valve to its product line. The valve would be used by manufacturers of irrigation equipment. The company anticipates starting with a relatively low sales volume and then boosting demand over the next several years. A new salesperson must be hired because Consolidated's current sales force is working at capacity. Two compensation plans are under consideration:

Consolidated Industries will purchase the valve for $50 and sell it for $80. Anticipated demand during the first year is 6,000 units. (In the following requirements, ignore income taxes.)

Required:

1. Compute the break-even point in units for Plan A and Plan B.

2. What is meant by the term operating leverage ?

3. Analyze the cost structures of both plans at the anticipated demand of 6,000 units. Which of the two plans has a higher operating leverage factor?

4. Assume that a general economic downturn occurred during year 2, with product demand falling from 6,000 to 5,000 units. Determine the percentage decrease in company net income if Consolidated had adopted Plan A.

5. Repeat requirement (4) for Plan B. Compare Plan A and Plan B, and explain a major factor that underlies any resulting differences.

6. Briefly discuss the likely profitability impact of an economic recession for highly automated manufacturers. What can you say about the risk associated with these firms?

Consolidated Industries will purchase the valve for $50 and sell it for $80. Anticipated demand during the first year is 6,000 units. (In the following requirements, ignore income taxes.)

Required:

1. Compute the break-even point in units for Plan A and Plan B.

2. What is meant by the term operating leverage ?

3. Analyze the cost structures of both plans at the anticipated demand of 6,000 units. Which of the two plans has a higher operating leverage factor?

4. Assume that a general economic downturn occurred during year 2, with product demand falling from 6,000 to 5,000 units. Determine the percentage decrease in company net income if Consolidated had adopted Plan A.

5. Repeat requirement (4) for Plan B. Compare Plan A and Plan B, and explain a major factor that underlies any resulting differences.

6. Briefly discuss the likely profitability impact of an economic recession for highly automated manufacturers. What can you say about the risk associated with these firms?

Question

Serendipity Sound, Inc. manufactures and sells compact discs. Price and cost data are as follows:

In the following requirements, ignore income taxes.

Required:

1. What is Serendipity Sound's break-even point in units?

2. What is the company's break-even point in sales dollars?

3. How many units would Serendipity Sound have to sell in order to earn $260,000?

4. What is the firm's margin of safety?

5. Management estimates that direct-labor costs will increase by 8 percent next year. How many units will the company have to sell next year to reach its break-even point?

6. If the company's direct-labor costs do increase by 8 percent, what selling price per unit of product must it charge to maintain the same contribution-margin ratio?

(CMA, adapted)

In the following requirements, ignore income taxes.

Required:

1. What is Serendipity Sound's break-even point in units?

2. What is the company's break-even point in sales dollars?

3. How many units would Serendipity Sound have to sell in order to earn $260,000?

4. What is the firm's margin of safety?

5. Management estimates that direct-labor costs will increase by 8 percent next year. How many units will the company have to sell next year to reach its break-even point?

6. If the company's direct-labor costs do increase by 8 percent, what selling price per unit of product must it charge to maintain the same contribution-margin ratio?

(CMA, adapted)

Question

Athletico, Inc. manufactures warm-up suits. The company's projected income for the coming year, based on sales of 160,000 units, is as follows:

Required: In completing the following requirements, ignore income taxes.

1. Prepare a CVP graph for Athletico, Inc. for the coming year.

2. Calculate the firm's break-even point for the year in sales dollars.

3. What is the company's margin of safety for the year?

4. Compute Athletico's operating leverage factor, based on the budgeted sales volume for the year.

5. Compute Athletico's required sales in dollars in order to earn income of $4,500,000 in the coming year.

6. Describe the firm's cost structure. Calculate the percentage relationships between variable and fixed expenses and sales revenue.

(CMA, adapted)

Required: In completing the following requirements, ignore income taxes.

1. Prepare a CVP graph for Athletico, Inc. for the coming year.

2. Calculate the firm's break-even point for the year in sales dollars.

3. What is the company's margin of safety for the year?

4. Compute Athletico's operating leverage factor, based on the budgeted sales volume for the year.

5. Compute Athletico's required sales in dollars in order to earn income of $4,500,000 in the coming year.

6. Describe the firm's cost structure. Calculate the percentage relationships between variable and fixed expenses and sales revenue.

(CMA, adapted)

Question

The European Division of Worldwide Reference Corporation produces a pocket dictionary containing popular phrases in six European languages. Annual budget data for the coming year follow. Projected sales are 100,000 books.

Required:

1. Calculate the break-even point in units and in sales dollars.

2. If the European Division is subject to an income-tax rate of 40 percent, compute the number of units the company would have to sell to earn an after-tax profit of $90,000.

3. If fixed costs increased $31,500 with no other cost or revenue factor changing, compute the firm's break-even sales in units.

4. Prepare a profit-volume graph for the European Division.

5. Due to an unstable political situation in the country in which the European Division is located, management believes the country may split into two independent nations. If this happens, the tax rate could rise to 50 percent. Assuming all other data as in the original problem, how many pocket dictionaries must be sold to earn $90,000 after taxes?

6. Build a spreadsheet: Construct an Excel spreadsheet to solve requirements (1), (2), (3), and (5) above. Show how the solution will change if the following information changes: sales amounted to $1,100,000 and fixed manufacturing overhead was $110,000.

(CMA, adapted)

Required:

1. Calculate the break-even point in units and in sales dollars.

2. If the European Division is subject to an income-tax rate of 40 percent, compute the number of units the company would have to sell to earn an after-tax profit of $90,000.

3. If fixed costs increased $31,500 with no other cost or revenue factor changing, compute the firm's break-even sales in units.

4. Prepare a profit-volume graph for the European Division.

5. Due to an unstable political situation in the country in which the European Division is located, management believes the country may split into two independent nations. If this happens, the tax rate could rise to 50 percent. Assuming all other data as in the original problem, how many pocket dictionaries must be sold to earn $90,000 after taxes?

6. Build a spreadsheet: Construct an Excel spreadsheet to solve requirements (1), (2), (3), and (5) above. Show how the solution will change if the following information changes: sales amounted to $1,100,000 and fixed manufacturing overhead was $110,000.

(CMA, adapted)

Question

Question

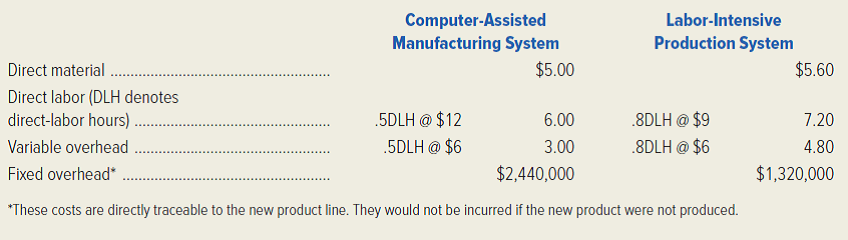

Celestial Products, Inc. has decided to introduce a new product, which can be manufactured by either a computer-assisted manufacturing system or a labor-intensive production system. The manufacturing method will not affect the quality of the product. The estimated manufacturing costs by the two methods are as follows:

The company's marketing research department has recommended an introductory unit sales price of $30. Selling expenses are estimated to be $500,000 annually plus $2 for each unit sold. (Ignore income taxes.)

Required:

1. Calculate the estimated break-even point in annual unit sales of the new product if the company uses the ( a ) computer-assisted manufacturing system; ( b ) labor-intensive production system.

2. Determine the annual unit sales volume at which the firm would be indifferent between the two manufacturing methods.

3. Management must decide which manufacturing method to employ. One factor it should consider is operating leverage. Explain the concept of operating leverage. How is this concept related to Celestial Products' decision?

4. Describe the circumstances under which the firm should employ each of the two manufacturing methods.

5. Identify some business factors other than operating leverage that management should consider before selecting the manufacturing method.

(CMA, adapted)

The company's marketing research department has recommended an introductory unit sales price of $30. Selling expenses are estimated to be $500,000 annually plus $2 for each unit sold. (Ignore income taxes.)

Required:

1. Calculate the estimated break-even point in annual unit sales of the new product if the company uses the ( a ) computer-assisted manufacturing system; ( b ) labor-intensive production system.

2. Determine the annual unit sales volume at which the firm would be indifferent between the two manufacturing methods.

3. Management must decide which manufacturing method to employ. One factor it should consider is operating leverage. Explain the concept of operating leverage. How is this concept related to Celestial Products' decision?

4. Describe the circumstances under which the firm should employ each of the two manufacturing methods.

5. Identify some business factors other than operating leverage that management should consider before selecting the manufacturing method.

(CMA, adapted)

Question

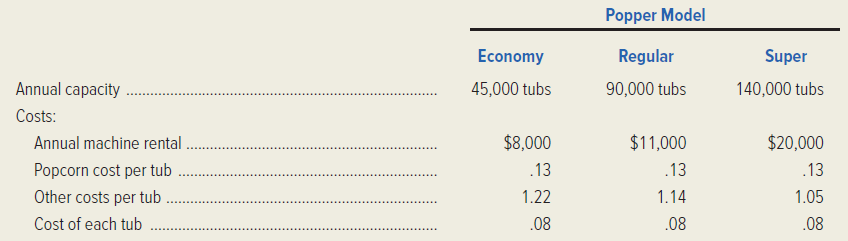

Silver Screen, Inc. owns and operates a nationwide chain of movie theaters. The 500 properties in the Silver Screen chain vary from low-volume, small-town, single-screen theaters to high-volume, urban, multiscreen theaters. The firm's management is considering installing popcorn machines, which would allow the theaters to sell freshly popped corn rather than prepopped corn. This new feature would be advertised to increase patronage at the company's theaters. The fresh popcorn will be sold for $1.75 per tub. The annual rental costs and the operating costs vary with the size of the popcorn machines. The machine capacities and costs are shown below. (Ignore income taxes.)

Required:

1. Calculate each theater's break-even sales volume (measured in tubs of popcorn) for each model of popcorn popper.

2. Prepare a profit-volume graph for one theater, assuming that the Super Popper is purchased.

3. Calculate the volume (in tubs) at which the Economy Popper and the Regular Popper earn the same profit or loss in each movie theater.

(CMA, adapted)

Required:

1. Calculate each theater's break-even sales volume (measured in tubs of popcorn) for each model of popcorn popper.

2. Prepare a profit-volume graph for one theater, assuming that the Super Popper is purchased.

3. Calculate the volume (in tubs) at which the Economy Popper and the Regular Popper earn the same profit or loss in each movie theater.

(CMA, adapted)

Question

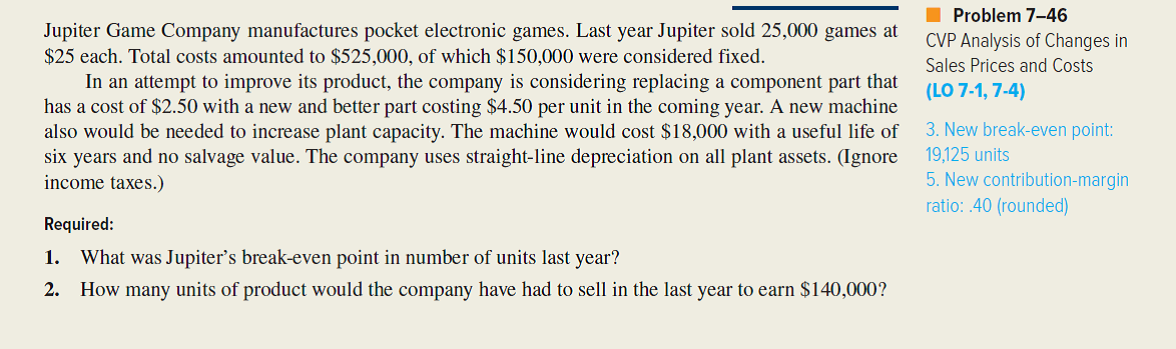

Question

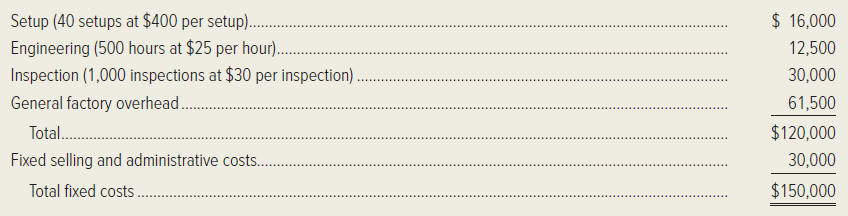

Refer to the original data given for Jupiter Game Company in the preceding problem. An activity-based costing study has revealed that Jupiter's $150,000 of fixed costs include the following components:

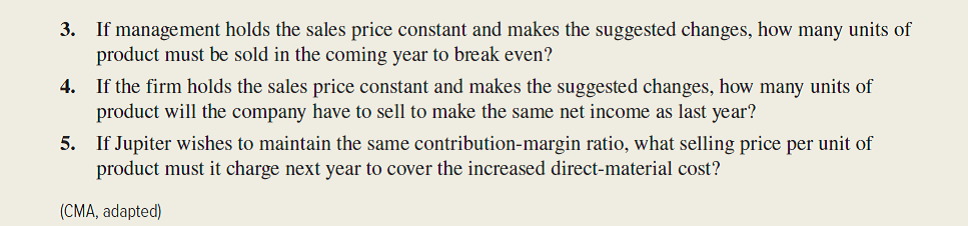

Management is considering the installation of new, highly automated manufacturing equipment that would significantly alter the production process. In addition, management plans a move toward just-in-time inventory and production management. If the new equipment is installed, setups will be quicker and less expensive. Under the proposed JIT approach, there would be 300 setups per year at $50 per setup. Since a total quality control program would accompany the move toward JIT, only 100 inspections would be anticipated annually, at a cost of $45 each. After the installation of the new production system, 800 hours of engineering would be required at a cost of $28 per hour. General factory overhead would increase to $166,100. However, the automated equipment would allow Jupiter to cut its unit variable cost by 20 percent. Moreover, the more consistent product quality anticipated would allow management to raise the price of electronic games to $26 per unit. (Ignore income taxes.)

Required:

1. Upon seeing the ABC analysis given in the problem, Jupiter's vice president for manufacturing exclaimed to the controller, "I thought you told me this $150,000 cost was fixed. These don't look like fixed costs at all. What you're telling me now is that setup costs us $400 every time we set up a production run. What gives?" As Jupiter's controller, write a short memo explaining to the vice president what is going on.

2. Compute Jupiter's new break-even point if the proposed automated equipment is installed.

3. Determine how many units Jupiter will have to sell to show a profit of $140,000, assuming the new technology is adopted.

4. If Jupiter adopts the new manufacturing technology, will its break-even point be higher or lower? Will the number of sales units required to earn a profit of $140,000 be higher or lower? (Refer to your answers for the first two requirements of the preceding problem.) Are the results in this case consistent with what you would typically expect to find? Explain.

5. The decision as to whether to purchase the automated manufacturing equipment will be made by Jupiter's board of directors. In order to support the proposed acquisition, the vice president for manufacturing asked the controller to prepare a report on the financial implications of the decision. As part of the report, the vice president asked the controller to compute the new break-even point, assuming the installation of the equipment. The controller complied, as in requirement (2) of this problem.

When the vice president for manufacturing saw that the break-even point would increase, he asked the controller to delete the break-even analysis from the report. What should the controller do? Which ethical standards for managerial accountants are involved here?

Management is considering the installation of new, highly automated manufacturing equipment that would significantly alter the production process. In addition, management plans a move toward just-in-time inventory and production management. If the new equipment is installed, setups will be quicker and less expensive. Under the proposed JIT approach, there would be 300 setups per year at $50 per setup. Since a total quality control program would accompany the move toward JIT, only 100 inspections would be anticipated annually, at a cost of $45 each. After the installation of the new production system, 800 hours of engineering would be required at a cost of $28 per hour. General factory overhead would increase to $166,100. However, the automated equipment would allow Jupiter to cut its unit variable cost by 20 percent. Moreover, the more consistent product quality anticipated would allow management to raise the price of electronic games to $26 per unit. (Ignore income taxes.)

Required:

1. Upon seeing the ABC analysis given in the problem, Jupiter's vice president for manufacturing exclaimed to the controller, "I thought you told me this $150,000 cost was fixed. These don't look like fixed costs at all. What you're telling me now is that setup costs us $400 every time we set up a production run. What gives?" As Jupiter's controller, write a short memo explaining to the vice president what is going on.

2. Compute Jupiter's new break-even point if the proposed automated equipment is installed.

3. Determine how many units Jupiter will have to sell to show a profit of $140,000, assuming the new technology is adopted.

4. If Jupiter adopts the new manufacturing technology, will its break-even point be higher or lower? Will the number of sales units required to earn a profit of $140,000 be higher or lower? (Refer to your answers for the first two requirements of the preceding problem.) Are the results in this case consistent with what you would typically expect to find? Explain.

5. The decision as to whether to purchase the automated manufacturing equipment will be made by Jupiter's board of directors. In order to support the proposed acquisition, the vice president for manufacturing asked the controller to prepare a report on the financial implications of the decision. As part of the report, the vice president asked the controller to compute the new break-even point, assuming the installation of the equipment. The controller complied, as in requirement (2) of this problem.

When the vice president for manufacturing saw that the break-even point would increase, he asked the controller to delete the break-even analysis from the report. What should the controller do? Which ethical standards for managerial accountants are involved here?

Question

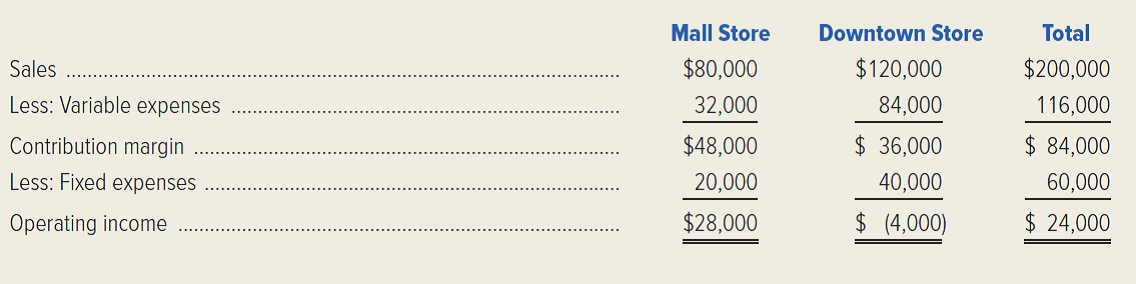

Condensed monthly income data for Thurber Book Stores are presented in the following table for November 20x1. (Ignore income taxes.)

Additional Information:

• Management estimates that closing the downtown store would result in a 10 percent decrease in mall store sales, while closing the mall store would not affect downtown store sales.

• One-fourth of each store's fixed expenses would continue through December 31, 20x2, if either store were closed.

• The operating results for November 20x1 are representative of all months.

Required:

1. Calculate the increase or decrease in Thurber's monthly operating income during 20x2 if the downtown store is closed.

2. The management of Thurber Book Stores is considering a promotional campaign at the downtown store that would not affect the mall store. Annual promotional expenses at the downtown store would be increased by $60,000 in order to increase downtown store sales by 10 percent. What would be the effect of this promotional campaign on the company's monthly operating income during 20x2?

3. One-half of the downtown store's dollar sales are from items sold at their variable cost to attract customers to the store. Thurber's management is considering the deletion of these items, a move that would reduce the downtown store's direct fixed expenses by 15 percent and result in the loss of 20 percent of the remaining downtown store's sales volume. This change would not affect the mall store. What would be the effect on Thurber's monthly operating income if the items sold at their variable cost are eliminated?

4. Build a spreadsheet: Construct an Excel spreadsheet to solve all of the preceding requirements. Show how the solution will change if the following information changes: the downtown store's sales amounted to $126,000 and its variable expenses were $86,000.

(CMA, adapted)

Additional Information:

• Management estimates that closing the downtown store would result in a 10 percent decrease in mall store sales, while closing the mall store would not affect downtown store sales.

• One-fourth of each store's fixed expenses would continue through December 31, 20x2, if either store were closed.

• The operating results for November 20x1 are representative of all months.

Required:

1. Calculate the increase or decrease in Thurber's monthly operating income during 20x2 if the downtown store is closed.

2. The management of Thurber Book Stores is considering a promotional campaign at the downtown store that would not affect the mall store. Annual promotional expenses at the downtown store would be increased by $60,000 in order to increase downtown store sales by 10 percent. What would be the effect of this promotional campaign on the company's monthly operating income during 20x2?

3. One-half of the downtown store's dollar sales are from items sold at their variable cost to attract customers to the store. Thurber's management is considering the deletion of these items, a move that would reduce the downtown store's direct fixed expenses by 15 percent and result in the loss of 20 percent of the remaining downtown store's sales volume. This change would not affect the mall store. What would be the effect on Thurber's monthly operating income if the items sold at their variable cost are eliminated?

4. Build a spreadsheet: Construct an Excel spreadsheet to solve all of the preceding requirements. Show how the solution will change if the following information changes: the downtown store's sales amounted to $126,000 and its variable expenses were $86,000.

(CMA, adapted)

Question

Cincinnati Tool Company (CTC) manufactures a line of electric garden tools that are sold in general hardware stores. The company's controller, Will Fulton, has just received the sales forecast for the coming year for CTC's three products: hedge clippers, weeders, and leaf blowers. CTC has experienced considerable variations in sales volumes and variable costs over the past two years, and Fulton believes the forecast should be carefully evaluated from a cost-volume-profit viewpoint. The preliminary budget information for 20x2 follows:

For 20x2, CTC's fixed manufacturing overhead is budgeted at $2,000,000, and the company's fixed selling and administrative expenses are forecasted to be $600,000. CTC has a tax rate of 40 percent.

Required:

1. Determine CTC's budgeted net income for 20x2.

2. Assuming the sales mix remains as budgeted, determine how many units of each product CTC must sell in order to break even in 20x2.

3. After preparing the original estimates, management determined that its variable manufacturing cost of leaf blowers would increase by 20 percent, and the variable selling cost of hedge clippers could be expected to increase by $1.00 per unit. However, management has decided not to change the selling price of either product. In addition, management has learned that its leaf blower has been perceived as the best value on the market, and it can expect to sell three times as many leaf blowers as each of its other products. Under these circumstances, determine how many units of each product CTC would have to sell in order to break even in 20x2.

(CMA, adapted)

For 20x2, CTC's fixed manufacturing overhead is budgeted at $2,000,000, and the company's fixed selling and administrative expenses are forecasted to be $600,000. CTC has a tax rate of 40 percent.

Required:

1. Determine CTC's budgeted net income for 20x2.

2. Assuming the sales mix remains as budgeted, determine how many units of each product CTC must sell in order to break even in 20x2.

3. After preparing the original estimates, management determined that its variable manufacturing cost of leaf blowers would increase by 20 percent, and the variable selling cost of hedge clippers could be expected to increase by $1.00 per unit. However, management has decided not to change the selling price of either product. In addition, management has learned that its leaf blower has been perceived as the best value on the market, and it can expect to sell three times as many leaf blowers as each of its other products. Under these circumstances, determine how many units of each product CTC would have to sell in order to break even in 20x2.

(CMA, adapted)

Question

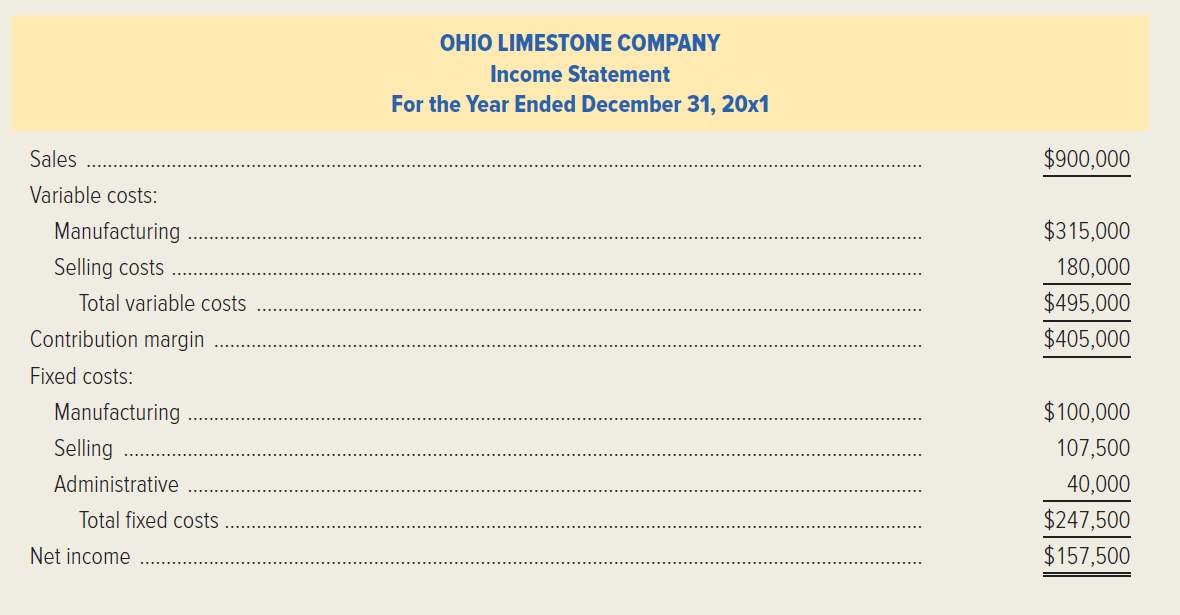

Ohio Limestone Company produces thin limestone sheets used for cosmetic facing on buildings. The following income statement represents the operating results for the year just ended. The company had sales of 1,800 tons during the year. The manufacturing capacity of the firm's facilities is 3,000 tons per year. (Ignore income taxes.)

Required:

1. Calculate the company's break-even volume in tons for 20x1.

2. If the sales volume is estimated to be 2,100 tons in the next year, and if the prices and costs stay at the same levels and amounts, what is the net income that management can expect for 20x2?

3. Ohio Limestone has been trying for years to get a foothold in the European market. The company has a potential German customer that has offered to buy 1,500 tons at $450 per ton. Assume that all of the firm's costs would be at the same levels and rates as in 20x1. What net income would the firm earn if it took this order and rejected some business from regular customers so as not to exceed capacity?

4. Ohio Limestone plans to market its product in a new territory. Management estimates that an advertising and promotion program costing $61,500 annually would be needed for the next two or three years. In addition, a $25 per ton sales commission to the sales force in the new territory, over and above the current commission, would be required. How many tons would have to be sold in the new territory to maintain the firm's current net income? Assume that sales and costs will continue as in 20x1 in the firm's established territories.

5. Management is considering replacing its labor-intensive process with an automated production system. This would result in an increase of $58,500 annually in fixed manufacturing costs. The variable manufacturing costs would decrease by $25 per ton. Compute the new break-even volume in tons and in sales dollars.

6. Ignore the facts presented in requirement (5). Assume that management estimates that the selling price per ton would decline by 10 percent next year. Variable costs would increase by $40 per ton, and fixed costs would not change. What sales volume in dollars would be required to earn a net income of $94,500 next year?

(CMA, adapted)

Required:

1. Calculate the company's break-even volume in tons for 20x1.

2. If the sales volume is estimated to be 2,100 tons in the next year, and if the prices and costs stay at the same levels and amounts, what is the net income that management can expect for 20x2?

3. Ohio Limestone has been trying for years to get a foothold in the European market. The company has a potential German customer that has offered to buy 1,500 tons at $450 per ton. Assume that all of the firm's costs would be at the same levels and rates as in 20x1. What net income would the firm earn if it took this order and rejected some business from regular customers so as not to exceed capacity?

4. Ohio Limestone plans to market its product in a new territory. Management estimates that an advertising and promotion program costing $61,500 annually would be needed for the next two or three years. In addition, a $25 per ton sales commission to the sales force in the new territory, over and above the current commission, would be required. How many tons would have to be sold in the new territory to maintain the firm's current net income? Assume that sales and costs will continue as in 20x1 in the firm's established territories.

5. Management is considering replacing its labor-intensive process with an automated production system. This would result in an increase of $58,500 annually in fixed manufacturing costs. The variable manufacturing costs would decrease by $25 per ton. Compute the new break-even volume in tons and in sales dollars.

6. Ignore the facts presented in requirement (5). Assume that management estimates that the selling price per ton would decline by 10 percent next year. Variable costs would increase by $40 per ton, and fixed costs would not change. What sales volume in dollars would be required to earn a net income of $94,500 next year?

(CMA, adapted)

Question

Alpine Thrills Ski Company recently expanded its manufacturing capacity. The firm will now be able to produce up to 15,000 pairs of cross-country skis of either the mountaineering model or the touring model. The sales department assures management that it can sell between 9,000 and 13,000 units of either product this year. Because the models are very similar, the company will produce only one of the two models.

The following information was compiled by the accounting department.

Fixed costs will total $369,600 if the mountaineering model is produced but will be only $316,800 if the touring model is produced. Alpine Thrills Ski Company is subject to a 40 percent income tax rate. (Round each answer to the nearest whole number.)

Required:

1. Compute the contribution-margin ratio for the touring model.

2. If Alpine Thrills Ski Company desires an after-tax net income of $22,080, how many pairs of touring skis will the company have to sell?

3. How much would the variable cost per unit of the touring model have to change before it had the same break-even point in units as the mountaineering model?

4. Suppose the variable cost per unit of touring skis decreases by 10 percent, and the total fixed cost of touring skis increases by 10 percent. Compute the new break-even point.

5. Suppose management decided to produce both products. If the two models are sold in equal proportions, and total fixed costs amount to $343,200, what is the firm's break-even point in units?

(CMA, adapted)

The following information was compiled by the accounting department.

Fixed costs will total $369,600 if the mountaineering model is produced but will be only $316,800 if the touring model is produced. Alpine Thrills Ski Company is subject to a 40 percent income tax rate. (Round each answer to the nearest whole number.)

Required:

1. Compute the contribution-margin ratio for the touring model.

2. If Alpine Thrills Ski Company desires an after-tax net income of $22,080, how many pairs of touring skis will the company have to sell?

3. How much would the variable cost per unit of the touring model have to change before it had the same break-even point in units as the mountaineering model?

4. Suppose the variable cost per unit of touring skis decreases by 10 percent, and the total fixed cost of touring skis increases by 10 percent. Compute the new break-even point.

5. Suppose management decided to produce both products. If the two models are sold in equal proportions, and total fixed costs amount to $343,200, what is the firm's break-even point in units?

(CMA, adapted)

Question

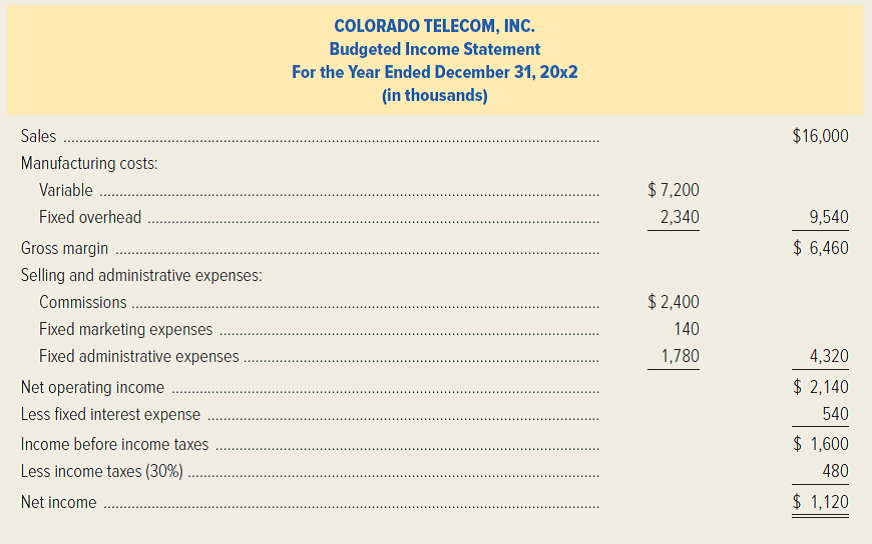

Colorado Telecom, Inc. manufactures telecommunications equipment. The company has always been production oriented and sells its products through agents. Agents are paid a commission of 15 percent of the selling price. Colorado Telecom's budgeted income statement for 20x2 follows:

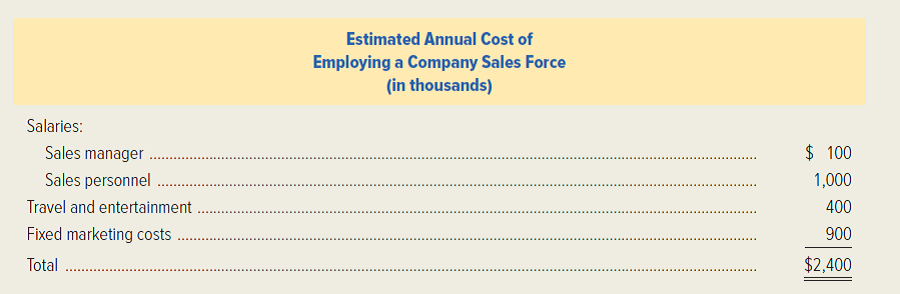

After the profit plan was completed for the coming year, Colorado Telecom's sales agents demanded that the commissions be increased to 22½ percent of the selling price. This demand was the latest in a series of actions that Liliana Richmond, the company's president, believed had gone too far. She asked Molly Rosewood, the most sales-oriented officer in her production-oriented company, to estimate the cost to the company of employing its own sales force. Rosewood's estimate of the additional annual cost of employing its own sales force, exclusive of commissions, follows. Sales personnel would receive a commission of 10 percent of the selling price in addition to their salary.

Required:

1. Calculate Colorado Telecom's estimated break-even point in sales dollars for 20x2.

a. If the events that are represented in the budgeted income statement take place.

b. If the company employs its own sales force.

2. If Colorado Telecom continues to sell through agents and pays the increased commission of 22½ percent of the selling price, determine the estimated volume in sales dollars for 20x2 that would be required to generate the same net income as projected in the budgeted income statement.

3. Determine the estimated volume in sales dollars that would result in equal net income for 20x2 regardless of whether the company continues to sell through agents and pays a commission of 22½ percent of the selling price or employs its own sales force.

(CMA, adapted)

After the profit plan was completed for the coming year, Colorado Telecom's sales agents demanded that the commissions be increased to 22½ percent of the selling price. This demand was the latest in a series of actions that Liliana Richmond, the company's president, believed had gone too far. She asked Molly Rosewood, the most sales-oriented officer in her production-oriented company, to estimate the cost to the company of employing its own sales force. Rosewood's estimate of the additional annual cost of employing its own sales force, exclusive of commissions, follows. Sales personnel would receive a commission of 10 percent of the selling price in addition to their salary.

Required:

1. Calculate Colorado Telecom's estimated break-even point in sales dollars for 20x2.

a. If the events that are represented in the budgeted income statement take place.

b. If the company employs its own sales force.

2. If Colorado Telecom continues to sell through agents and pays the increased commission of 22½ percent of the selling price, determine the estimated volume in sales dollars for 20x2 that would be required to generate the same net income as projected in the budgeted income statement.

3. Determine the estimated volume in sales dollars that would result in equal net income for 20x2 regardless of whether the company continues to sell through agents and pays a commission of 22½ percent of the selling price or employs its own sales force.

(CMA, adapted)

Question

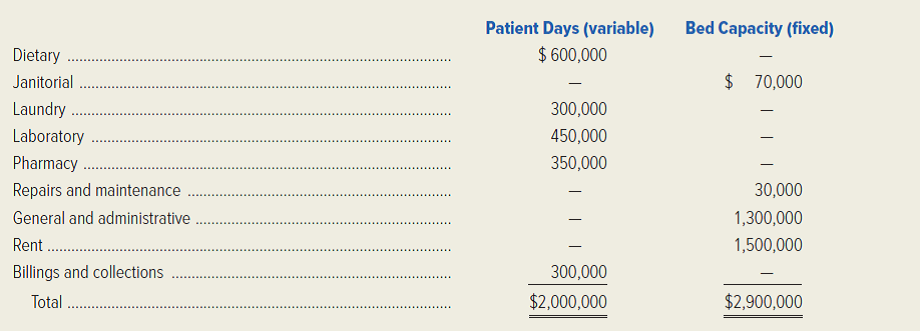

Delaware Medical Center operates a general hospital. The medical center also rents space and beds to separately owned entities rendering specialized services, such as Pediatrics and Psychiatric Care. Delaware charges each separate entity for common services, such as patients' meals and laundry, and for administrative services, such as billings and collections. Space and bed rentals are fixed charges for the year, based on bed capacity rented to each entity. Delaware Medical Center charged the following costs to Pediatrics for the year ended June 30, 20x1:

During the year ended June 30, 20x1, Pediatrics charged each patient an average of $300 per day, had a capacity of 60 beds, and had revenue of $6 million for 365 days. In addition, Pediatrics directly employed personnel with the following annual salary costs per employee: supervising nurses, $25,000; nurses, $20,000; and aides, $9,000.

Delaware Medical Center has the following minimum departmental personnel requirements, based on total annual patient days:

Pediatrics always employs only the minimum number of required personnel. Salaries of supervising nurses, nurses, and aides are therefore fixed within ranges of annual patient days.

Pediatrics operated at 100 percent capacity on 90 days during the year ended June 30, 20x1. Administrators estimate that on these 90 days, Pediatrics could have filled another 20 beds above capacity. Delaware Medical Center has an additional 20 beds available for rent for the year ending June 30, 20x2. Such additional rental would increase Pediatrics' fixed charges based on bed capacity. (In the following requirements, ignore income taxes.)

Required:

1. Calculate the minimum number of patient days required for Pediatrics to break even for the year ending June 30, 20x2, if the additional 20 beds are not rented. Patient demand is unknown, but assume that revenue per patient day, cost per patient day, cost per bed, and salary rates will remain the same as for the year ended June 30, 20x1.

2. Assume that patient demand, revenue per patient day, cost per patient day, cost per bed, and salary rates for the year ending June 30, 20x2, remain the same as for the year ended June 30, 20x1. Prepare a schedule of Pediatrics' increase in revenue and increase in costs for the year ending June 30, 20x2. Determine the net increase or decrease in Pediatrics' earnings from the additional 20 beds if Pediatrics rents this extra capacity from Delaware Medical Center.

(CPA, adapted)

During the year ended June 30, 20x1, Pediatrics charged each patient an average of $300 per day, had a capacity of 60 beds, and had revenue of $6 million for 365 days. In addition, Pediatrics directly employed personnel with the following annual salary costs per employee: supervising nurses, $25,000; nurses, $20,000; and aides, $9,000.

Delaware Medical Center has the following minimum departmental personnel requirements, based on total annual patient days:

Pediatrics always employs only the minimum number of required personnel. Salaries of supervising nurses, nurses, and aides are therefore fixed within ranges of annual patient days.

Pediatrics operated at 100 percent capacity on 90 days during the year ended June 30, 20x1. Administrators estimate that on these 90 days, Pediatrics could have filled another 20 beds above capacity. Delaware Medical Center has an additional 20 beds available for rent for the year ending June 30, 20x2. Such additional rental would increase Pediatrics' fixed charges based on bed capacity. (In the following requirements, ignore income taxes.)

Required:

1. Calculate the minimum number of patient days required for Pediatrics to break even for the year ending June 30, 20x2, if the additional 20 beds are not rented. Patient demand is unknown, but assume that revenue per patient day, cost per patient day, cost per bed, and salary rates will remain the same as for the year ended June 30, 20x1.

2. Assume that patient demand, revenue per patient day, cost per patient day, cost per bed, and salary rates for the year ending June 30, 20x2, remain the same as for the year ended June 30, 20x1. Prepare a schedule of Pediatrics' increase in revenue and increase in costs for the year ending June 30, 20x2. Determine the net increase or decrease in Pediatrics' earnings from the additional 20 beds if Pediatrics rents this extra capacity from Delaware Medical Center.

(CPA, adapted)

Question

Question

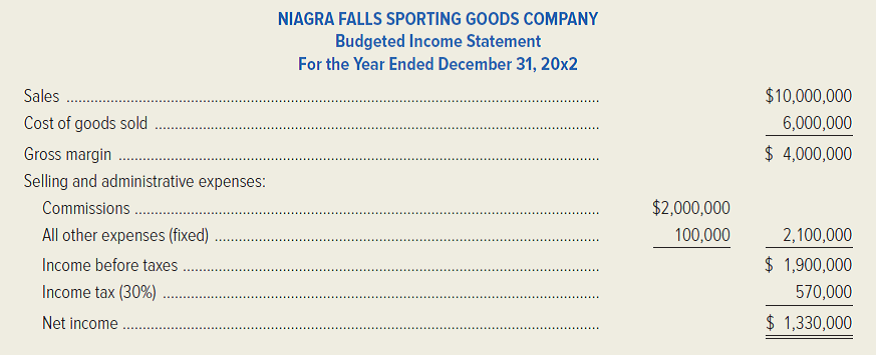

Niagra Falls Sporting Goods Company, a wholesale supply company, engages independent sales agents to market the company's products throughout New York and Ontario. These agents currently receive a commission of 20 percent of sales, but they are demanding an increase to 25 percent of sales made during the year ending December 31, 20x2. The controller already prepared the 20x2 budget before learning of the agents' demand for an increase in commissions. The budgeted 20x2 income statement is shown below. Assume that cost of goods sold is 100 percent variable cost.

The company's sales manager, Joey Dulwich, is considering the possibility of employing full-time sales personnel. Three individuals would be required, at an estimated annual salary of $30,000 each, plus commissions of 5 percent of sales. In addition, a sales manager would be employed at a fixed annual salary of $160,000. All other fixed costs, as well as the variable cost percentages, would remain the same as the estimates in the 20x2 budgeted income statement.

Required:

1. Compute Niagra Falls Sporting Goods' estimated break-even point in sales dollars for the year ending December 31, 20x2, based on the budgeted income statement prepared by the controller.

2. Compute the estimated break-even point in sales dollars for the year ending December 31, 20x2, if the company employs its own sales personnel.

3. Compute the estimated volume in sales dollars that would be required for the year ending December 31, 20x2, to yield the same net income as projected in the budgeted income statement, if management continues to use the independent sales agents and agrees to their demand for a 25 percent sales commission.

4. Compute the estimated volume in sales dollars that would generate an identical net income for the year ending December 31, 20x2, regardless of whether Niagra Falls Sporting Goods Company employs its own sales personnel or continues to use the independent sales agents and pays them a 25 percent commission.

(CPA, adapted)

The company's sales manager, Joey Dulwich, is considering the possibility of employing full-time sales personnel. Three individuals would be required, at an estimated annual salary of $30,000 each, plus commissions of 5 percent of sales. In addition, a sales manager would be employed at a fixed annual salary of $160,000. All other fixed costs, as well as the variable cost percentages, would remain the same as the estimates in the 20x2 budgeted income statement.

Required:

1. Compute Niagra Falls Sporting Goods' estimated break-even point in sales dollars for the year ending December 31, 20x2, based on the budgeted income statement prepared by the controller.

2. Compute the estimated break-even point in sales dollars for the year ending December 31, 20x2, if the company employs its own sales personnel.

3. Compute the estimated volume in sales dollars that would be required for the year ending December 31, 20x2, to yield the same net income as projected in the budgeted income statement, if management continues to use the independent sales agents and agrees to their demand for a 25 percent sales commission.

4. Compute the estimated volume in sales dollars that would generate an identical net income for the year ending December 31, 20x2, regardless of whether Niagra Falls Sporting Goods Company employs its own sales personnel or continues to use the independent sales agents and pays them a 25 percent commission.

(CPA, adapted)

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/55

Play

Full screen (f)

Deck 7: Cost-Volume-Profit Analysis

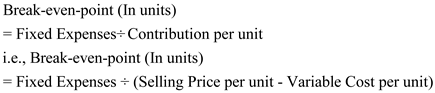

1

Briefly explain each of the following methods of computing a break-even point in units: ( a ) contribution-margin approach, ( b ) equation approach, and ( c ) graphical approach.

Break-even point :

'Break-even point' is the level of production activity where there is neither profit nor loss for the organization. It is the point at which where the revenues of the organization are equal to its expenses.

In other words, it is the point of activity at which the organization 'breaks-even'.

It must be noted that for identifying the 'breakeven point', importance is given to the behavior of the costs in terms of fixed and variable costs.

There are three different approaches to calculate the break-even point. They are :

a. Contribution - Margin approach

b. Equation Approach

c. Graphical Approach

a. Contribution - Margin Approach :

Contribution - Margin refers to the difference between the sales revenue and the variable costs i.e.,

In this context it must be remembered that the contribution is towards the recovery of the fixed expenses and focus is on 'contribution per unit'.

In this context it must be remembered that the contribution is towards the recovery of the fixed expenses and focus is on 'contribution per unit'.

Therefore

b. Equation Approach:

b. Equation Approach:

The equation approach is used along with the Contribution Margin Approach, i.e., the variables used are similar to those in Contribution-Margin Approach, which are now presented in an Equation form.

The equation is

Where sales = Sales Volume × Selling Price in Units per Unit

Where sales = Sales Volume × Selling Price in Units per Unit

Variable Expenses = Sales Volume × Variable Expenses in Units per Unit

Fixed = Fixed (as given)

Therefore,

Sales Selling price Sales Variable Fixed volume in × per (-) Volume in × Expense (-) Expenses = Profit units unit units per unit

Contribution margin approach and the Equation Approach are two alternative and equivalent approaches to find out the break-even point.

* Given the sales price per unit, variable expense per unit the fixed expenses and the profit being zero at Break-even-point.

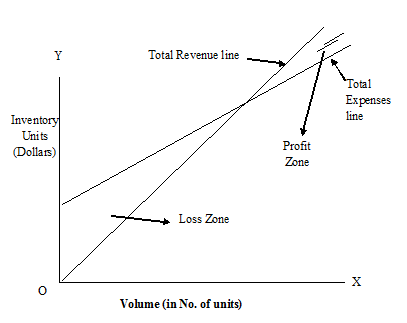

c. Graphical Approach :

This is an extension to the contribution-margin Approach and Equation Approach.

In both these approaches we can find out the break-even point, which provides important information as a basis for managerial decision - making just as a starting point.

Identifying the break-even-point is not an end in itself. Through it is an 'important starting point, it does not reflect the changed in the profit in accordance with the changes in activity or output.

It is in order to establish a relationship between the profit and the volume of activity the 'Graphical Approach' is adopted.

The graph developed under this approach is commonly known as 'Cost-Volume-Profit' (CVP) graph.

Steps to develop the CVP graph:

Step 1: Draw two axes of the graph from the origin (o), i.e., one horizontal axis (0-x) and the other vertical axis (0-y).

Step 2: Label the horizontal axis (0-x) in 'number of units of output' and the vertical axis (0-y) in monetary terms i.e., dollars.

Step 3: Draw the 'fixed expenses' line. Fixed expenses do not change with activity or number of units. The total fixed expenses are constant for all levels of output unless there is a permanent shift in the production capacity. Therefore the 'fixed expenses line' will be 'parallel' to the horizontal axis.

Step 4: calculate the 'total expenses' (fixed expenses + Variable expenses) at any given volume. Plot the same on the graph.

Step 5: Draw the 'total expenses line'. Observe that this line passes through the point plotted in step 4 and intercepts the fixed-expenses line.

Step 6: Complete the sale revenue at any given volume and plot this point on the graph.

Step 7: Draw the 'total revenue line' which passes through the point in step 6.

Step 8: The point at which the 'total revenue line' intercepts the 'total expenses line' is the break-even point. Any activity or output above this point will fetch profits and any below this point will result in losses.

The same is presented in the following graph.

'Break-even point' is the level of production activity where there is neither profit nor loss for the organization. It is the point at which where the revenues of the organization are equal to its expenses.

In other words, it is the point of activity at which the organization 'breaks-even'.

It must be noted that for identifying the 'breakeven point', importance is given to the behavior of the costs in terms of fixed and variable costs.

There are three different approaches to calculate the break-even point. They are :

a. Contribution - Margin approach

b. Equation Approach

c. Graphical Approach

a. Contribution - Margin Approach :

Contribution - Margin refers to the difference between the sales revenue and the variable costs i.e.,

In this context it must be remembered that the contribution is towards the recovery of the fixed expenses and focus is on 'contribution per unit'.Therefore

b. Equation Approach: The equation approach is used along with the Contribution Margin Approach, i.e., the variables used are similar to those in Contribution-Margin Approach, which are now presented in an Equation form.

The equation is

Where sales = Sales Volume × Selling Price in Units per Unit Variable Expenses = Sales Volume × Variable Expenses in Units per Unit

Fixed = Fixed (as given)

Therefore,

Sales Selling price Sales Variable Fixed volume in × per (-) Volume in × Expense (-) Expenses = Profit units unit units per unit

Contribution margin approach and the Equation Approach are two alternative and equivalent approaches to find out the break-even point.

* Given the sales price per unit, variable expense per unit the fixed expenses and the profit being zero at Break-even-point.

c. Graphical Approach :

This is an extension to the contribution-margin Approach and Equation Approach.

In both these approaches we can find out the break-even point, which provides important information as a basis for managerial decision - making just as a starting point.

Identifying the break-even-point is not an end in itself. Through it is an 'important starting point, it does not reflect the changed in the profit in accordance with the changes in activity or output.

It is in order to establish a relationship between the profit and the volume of activity the 'Graphical Approach' is adopted.

The graph developed under this approach is commonly known as 'Cost-Volume-Profit' (CVP) graph.

Steps to develop the CVP graph:

Step 1: Draw two axes of the graph from the origin (o), i.e., one horizontal axis (0-x) and the other vertical axis (0-y).

Step 2: Label the horizontal axis (0-x) in 'number of units of output' and the vertical axis (0-y) in monetary terms i.e., dollars.

Step 3: Draw the 'fixed expenses' line. Fixed expenses do not change with activity or number of units. The total fixed expenses are constant for all levels of output unless there is a permanent shift in the production capacity. Therefore the 'fixed expenses line' will be 'parallel' to the horizontal axis.

Step 4: calculate the 'total expenses' (fixed expenses + Variable expenses) at any given volume. Plot the same on the graph.

Step 5: Draw the 'total expenses line'. Observe that this line passes through the point plotted in step 4 and intercepts the fixed-expenses line.

Step 6: Complete the sale revenue at any given volume and plot this point on the graph.

Step 7: Draw the 'total revenue line' which passes through the point in step 6.

Step 8: The point at which the 'total revenue line' intercepts the 'total expenses line' is the break-even point. Any activity or output above this point will fetch profits and any below this point will result in losses.

The same is presented in the following graph.

2

What is the meaning of the term unit contribution margin? Contribution to what?

This term is used in ' break-even analysis' where the total expenses are divided into two categories based on their behavior viz., fixed expenses and variable expenses.

Unit contribution margin refers to the difference between selling price per unit and the variable expenses per unit.

It is observed that whatever is the amount that is available from the sales revenue after recovering the variable expenses, which will contribute towards the recovery of fixed expenses.

In other words, excess of sales revenue over the total variable expenses is the contribution towards the recovery of the fixed expenses , and the unit contribution margin is nothing but the per unit excess or margin of sales revenue over per unit variable expense which will contribute towards the recovery of fixed expenses.

The Unit Contribution Margin is the crucial variable which helps in determining the break-even-point. i.e., since at break-even point there is no profit or loss, the revenue must be equal to the fixed expenses.

The 'Unit Contribution Margin' helps in determining these number of units (break-even units) the revenue on which will be just equal to the fixed expenses.

The formula for break-even point on the basis of

Units Contribution Margin = Fixed Expenses

Unit contribution margin refers to the difference between selling price per unit and the variable expenses per unit.

It is observed that whatever is the amount that is available from the sales revenue after recovering the variable expenses, which will contribute towards the recovery of fixed expenses.

In other words, excess of sales revenue over the total variable expenses is the contribution towards the recovery of the fixed expenses , and the unit contribution margin is nothing but the per unit excess or margin of sales revenue over per unit variable expense which will contribute towards the recovery of fixed expenses.

The Unit Contribution Margin is the crucial variable which helps in determining the break-even-point. i.e., since at break-even point there is no profit or loss, the revenue must be equal to the fixed expenses.

The 'Unit Contribution Margin' helps in determining these number of units (break-even units) the revenue on which will be just equal to the fixed expenses.

The formula for break-even point on the basis of

Units Contribution Margin = Fixed Expenses

3

What information is conveyed by a cost-volume-profit graph in addition to a company's break-even point?

Information Conveyed by a Cost-Volume-Profit chart:

Profitability:

Information regarding change in the profit due to change in the volume, profit, and loss area can be obtained.

Angle of Incidence:

Angle of incidence is the angle where total sales line cuts the total cost line. It is break-even point for the company. If the angle at this point, if large, then company is said to make profits at higher rate and vice versa.

Relationship between variable cost, fixed costs, and contribution from the sale revenue can be obtained.

Margin of Safety:

The sales revenue over and above the break-even point is termed as margin of safety.

Profitability:

Information regarding change in the profit due to change in the volume, profit, and loss area can be obtained.

Angle of Incidence:

Angle of incidence is the angle where total sales line cuts the total cost line. It is break-even point for the company. If the angle at this point, if large, then company is said to make profits at higher rate and vice versa.

Relationship between variable cost, fixed costs, and contribution from the sale revenue can be obtained.

Margin of Safety:

The sales revenue over and above the break-even point is termed as margin of safety.

4

What does the term safety margin mean?

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

5

Suppose the fixed expenses of a travel agency increase. What will happen to its break-even point, measured in number of clients served? Why?

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

6

Delmarva Oyster Company has been able to decrease its variable expenses per pound of oysters harvested. How will this affect the firm's break-even sales volume?

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

7

In a strategy meeting, a manufacturing company's president said, "If we raise the price of our product, the company's break-even point will be lower." The financial vice president responded by saying, "Then we should raise our price. The company will be less likely to incur a loss." Do you agree with the president? Why? Do you agree with the financial vice president? Why?

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

8

What will happen to a company's break-even point if the sales price and unit variable cost of its only product increase by the same dollar amount?

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

9

An art museum covers its operating expenses by charging a small admission fee. The objective of the nonprofit organization is to break even. A local arts enthusiast has just pledged an annual donation of $10,000 to the museum. How will the donation affect the museum's break-even attendance level?

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

10

How can a profit-volume graph be used to predict a company's profit for a particular sales volume?

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

11

List the most important assumptions of cost-volume-profit analysis.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

12

Why do many operating managers prefer a contribution income statement instead of a traditional income statement?

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

13

What is the difference between a manufacturing company's gross margin and its total contribution margin?

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

14

East Company manufactures VCRs using a completely automated production process. West Company also manufactures VCRs, but its products are assembled manually. How will these two firms' cost structures differ? Which company will have a higher operating leverage factor?

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

15

When sales volume increases, which company will experience a larger percentage increase in profit: company X, which has mostly fixed expenses, or company Y, which has mostly variable expenses?

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

16

What does the term sales mix mean? How is a weighted-average unit contribution margin computed?

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

17

A car rental agency rents subcompact, compact, and full-size automobiles. What assumptions would be made about the agency's sales mix for the purpose of a cost-volume-profit analysis?

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

18

How can a hotel's management use cost-volume-profit analysis to help in deciding on room rates?

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

19

How could cost-volume-profit analysis be used in budgeting? In making a decision about advertising?

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

20

Two companies have identical fixed expenses, unit variable expenses, and profits. Yet one company has set a much lower price for its product. Explain how this can happen.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

21

A company with an advanced manufacturing environment typically will have a higher break-even point, greater operating leverage, and larger safety margin than a labor-intensive firm. True or false? Explain.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

22

Explain briefly how activity-based costing (ABC) affects cost-volume-profit analysis.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

23

Fill in the missing data for each of the following independent cases. (Ignore income taxes.)

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

24

College Pizza delivers pizzas to the dormitories and apartments near a major state university. The company's annual fixed expenses are $40,000. The sales price of a pizza is $10, and it costs the company $5 to make and deliver each pizza. (In the following requirements, ignore income taxes.)

Required:

1. Using the contribution-margin approach, compute the company's break-even point in units (pizzas).

2. What is the contribution-margin ratio?

3. Compute the break-even sales revenue. Use the contribution-margin ratio in your calculation.

4. How many pizzas must the company sell to earn a target profit of $65,000? Use the equation method.

Required:

1. Using the contribution-margin approach, compute the company's break-even point in units (pizzas).

2. What is the contribution-margin ratio?

3. Compute the break-even sales revenue. Use the contribution-margin ratio in your calculation.

4. How many pizzas must the company sell to earn a target profit of $65,000? Use the equation method.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

25

Rosario Company, which is located in Buenos Aires, Argentina, manufactures a component used in farm machinery. The firm's fixed costs are 4,000,000 p per year. The variable cost of each component is 2,000 p, and the components are sold for 3,000 p each. The company sold 5,000 components during the prior year. ( p denotes the peso, Argentina's national currency. Several countries use the peso as their monetary unit. On the day this exercise was written, Argentina's peso was worth.104 U.S. dollar. In the following requirements, ignore income taxes.)

Required: Answer requirements (1) through (4) independently.

1. Compute the break-even point in units.

2. What will the new break-even point be if fixed costs increase by 10 percent?

3. What was the company's net income for the prior year?

4. The sales manager believes that a reduction in the sales price to 2,500 p will result in orders for 1,200 more components each year. What will the break-even point be if the price is changed?

5. Should the price change discussed in requirement (4) be made?

Required: Answer requirements (1) through (4) independently.

1. Compute the break-even point in units.

2. What will the new break-even point be if fixed costs increase by 10 percent?

3. What was the company's net income for the prior year?

4. The sales manager believes that a reduction in the sales price to 2,500 p will result in orders for 1,200 more components each year. What will the break-even point be if the price is changed?

5. Should the price change discussed in requirement (4) be made?

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

26

The Houston Armadillos, a minor-league baseball team, play their weekly games in a small stadium just outside Houston. The stadium holds 10,000 people and tickets sell for $10 each. The franchise owner estimates that the team's annual fixed expenses are $180,000, and the variable expense per ticket sold is $1. (In the following requirements, ignore income taxes.)

Required:

1. Draw a cost-volume-profit graph for the sports franchise. Label the axes, break-even point, profit and loss areas, fixed expenses, variable expenses, total-expense line, and total-revenue line.

2. If the stadium is half full for each game, how many games must the team play to break even?

Required:

1. Draw a cost-volume-profit graph for the sports franchise. Label the axes, break-even point, profit and loss areas, fixed expenses, variable expenses, total-expense line, and total-revenue line.

2. If the stadium is half full for each game, how many games must the team play to break even?

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

27

Refer to the data given in the preceding exercise. (Ignore income taxes.)

Required:

1. Prepare a fully labeled profit-volume graph for the Houston Armadillos.

2. What is the safety margin for the baseball franchise if the team plays a 12-game season and the team owner expects the stadium to be 30 percent full for each game?

3. If the stadium is half full for each game, what ticket price would the team have to charge in order to break even?

Required:

1. Prepare a fully labeled profit-volume graph for the Houston Armadillos.

2. What is the safety margin for the baseball franchise if the team plays a 12-game season and the team owner expects the stadium to be 30 percent full for each game?