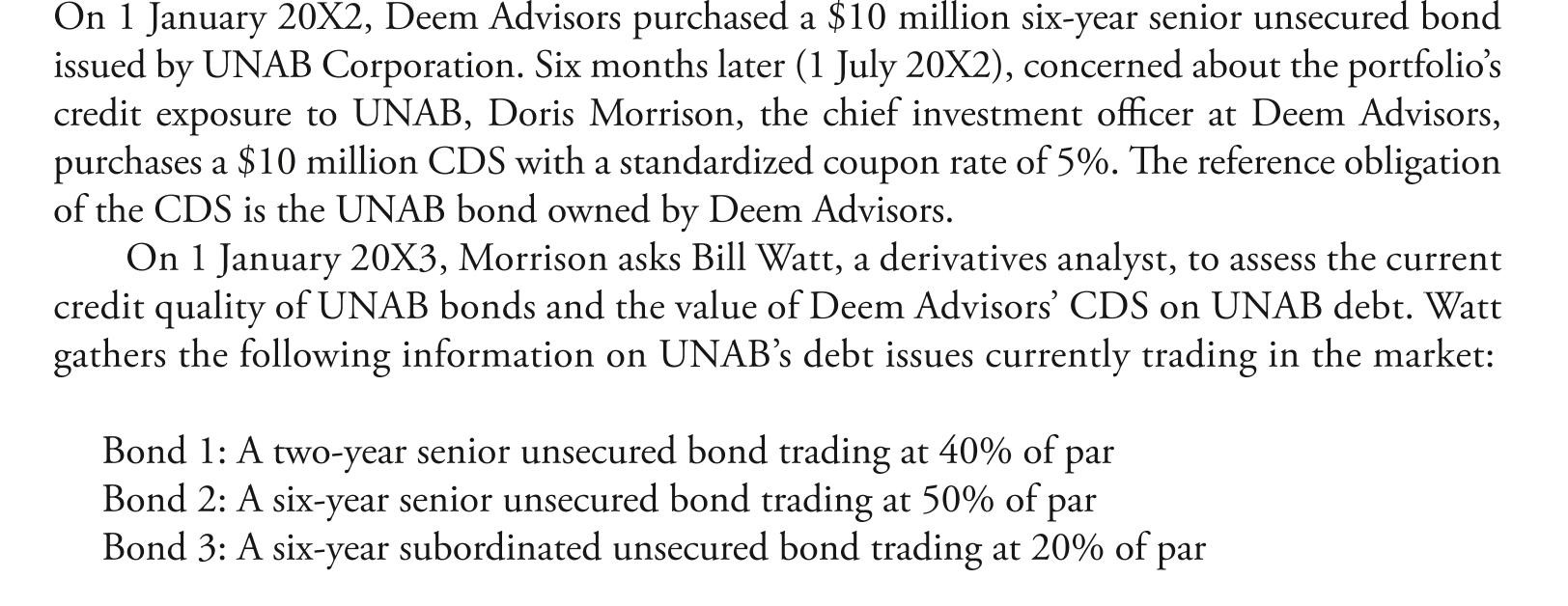

Deck 11: Credit Default Swaps

Full screen (f)

Question

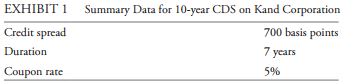

required and, if so, the amount of the premium. watt presents the information for the CdS

required and, if so, the amount of the premium. watt presents the information for the CdS in exhibit 1.

Morrison purchases the 10-year CdS on Kand Corporation debt. two months later

Morrison purchases the 10-year CdS on Kand Corporation debt. two months later the credit spread for Kand Corp. has increased by 200 basis points. Morrison asks watt

to close out the firm's CdS position on Kand Corporation by entering into new offsetting

contracts.

Tollunt Corporation

deem advisors' chief credit analyst recently reported that tollunt Corporation's five-year bond

is currently yielding 7% and a comparable CdS contract has a credit spread of 4.25%. Since

libor is 2.5%, watt has recommended executing a basis trade to take advantage of the pricing

of tollunt's bonds and CdS. The basis trade would consist of purchasing both the bond and

the CdS contract.

if deem advisors enters into a new offsetting contract two months after purchasing the CdS protection on Kand Corporation, this action will most likely result in:

A) a loss on the CdS position.

B) a gain on the CdS position.

C) neither a loss or a gain on the CdS position.

Question

The following information relates to Questions

John Smith, a fixed-income portfolio manager at a €10 billion sovereign wealth fund

(Swf), meets with Sofia Chan, a derivatives strategist with Shire Gate Securities (SGS),

to discuss investment opportunities for the fund. Chan notes that SGS adheres to iSda

(international Swaps and derivatives association) protocols for credit default swap (CdS)

transactions and that any contract must conform to iSda specifications. before the

fund can engage in trading CdS products with SGS, the fund must satisfy compliance

requirements.

Smith explains to Chan that fixed-income derivatives strategies are being contemplated

for both hedging and trading purposes. Given the size and diversified nature of the fund,

Smith asks Chan to recommend a type of CdS that would allow the Swf to simultaneously

fully hedge multiple fixed-income exposures.

Next, Smith asks Chan to assess the impact on derivative products of recent events affect-

ing Maxx Corporation, a uS company. The Swf holds an unsecured debt instrument issued

by Maxx. Chan says she is very familiar with Maxx because many of its unsecured debt obliga-

tions are commonly included in broad baskets of bonds used for

hedging purposes. SGS recently sold €400 million of protection

on the on-the-run CdX high yield (hY) index that includes a

Maxx bond; the index contains 100 entities. Chan reports that

creditors met with company executives to impose a restructuring on Maxx bonds; as a result,

all outstanding principal obligations will be reduced by 30%.

Smith and Chan discuss opportunities to add trading profits to the Swf. Smith asks Chan

to determine the probability of default associated with a five-year investment-grade bond issued

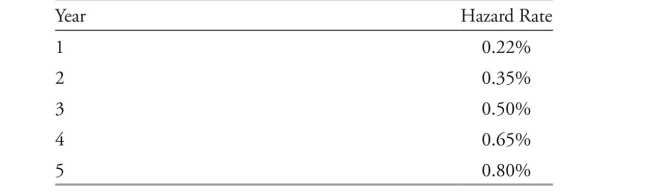

by orion industrial. Selected data on the orion industrial bond are presented in exhibit 1.

eXhibit 1 Selected data on orion industrial five-Year bond

Chan explains that a single-name CdS can also be used to add profit to the fund over

time. Chan describes a hypothetical trade in which the fund sells £6 million of five-year CdS

protection on orion, where the CdS contract has a duration of 3.9 years. Chan assumes that

the fund closes the position six months later, after orion's credit spread narrowed from 150

bps to 100 bps.

Chan discusses the mechanics of a long/short trade. in order to structure a number of

potential trades, Chan and Smith exchange their respective views on individual companies and

global economies. Chan and Smith agree on the following outlooks.

Outlook 1: italy's economy will weaken.

Outlook 2: The uS economy will strengthen relative to that of Canada.

Outlook 3: The credit quality of electric car manufacturers will improve relative to that of

traditional car manufacturers.

Chan believes uS macroeconomic data are improving and that the general economy will

strengthen in the short term. Chan suggests that a curve trade could be used by the fund to

capitalize on her short-term view of a steepening of the uS credit curve.

another short-term trading opportunity that Smith and Chan discuss involves the merger

and acquisition market. SGS believes that delta Corporation may make an unsolicited bid at

a premium to the market price for all publicly traded shares of Zega, inc. Zega's market cap-

italization and capital structure are comparable to delta's; both firms are highly levered. it is

anticipated that delta will issue new equity along with 5- and 10-year senior unsecured debt

to fund the acquisition, which will significantly increase its debt ratio.

based on exhibit 1, the probability of orion defaulting on the bond during the first three years is closest to:

A) 1.07%.

B) 2.50%.

C) 3.85%.

John Smith, a fixed-income portfolio manager at a €10 billion sovereign wealth fund

(Swf), meets with Sofia Chan, a derivatives strategist with Shire Gate Securities (SGS),

to discuss investment opportunities for the fund. Chan notes that SGS adheres to iSda

(international Swaps and derivatives association) protocols for credit default swap (CdS)

transactions and that any contract must conform to iSda specifications. before the

fund can engage in trading CdS products with SGS, the fund must satisfy compliance

requirements.

Smith explains to Chan that fixed-income derivatives strategies are being contemplated

for both hedging and trading purposes. Given the size and diversified nature of the fund,

Smith asks Chan to recommend a type of CdS that would allow the Swf to simultaneously

fully hedge multiple fixed-income exposures.

Next, Smith asks Chan to assess the impact on derivative products of recent events affect-

ing Maxx Corporation, a uS company. The Swf holds an unsecured debt instrument issued

by Maxx. Chan says she is very familiar with Maxx because many of its unsecured debt obliga-

tions are commonly included in broad baskets of bonds used for

hedging purposes. SGS recently sold €400 million of protection

on the on-the-run CdX high yield (hY) index that includes a

Maxx bond; the index contains 100 entities. Chan reports that

creditors met with company executives to impose a restructuring on Maxx bonds; as a result,

all outstanding principal obligations will be reduced by 30%.

Smith and Chan discuss opportunities to add trading profits to the Swf. Smith asks Chan

to determine the probability of default associated with a five-year investment-grade bond issued

by orion industrial. Selected data on the orion industrial bond are presented in exhibit 1.

eXhibit 1 Selected data on orion industrial five-Year bond

Chan explains that a single-name CdS can also be used to add profit to the fund over

time. Chan describes a hypothetical trade in which the fund sells £6 million of five-year CdS

protection on orion, where the CdS contract has a duration of 3.9 years. Chan assumes that

the fund closes the position six months later, after orion's credit spread narrowed from 150

bps to 100 bps.

Chan discusses the mechanics of a long/short trade. in order to structure a number of

potential trades, Chan and Smith exchange their respective views on individual companies and

global economies. Chan and Smith agree on the following outlooks.

Outlook 1: italy's economy will weaken.

Outlook 2: The uS economy will strengthen relative to that of Canada.

Outlook 3: The credit quality of electric car manufacturers will improve relative to that of

traditional car manufacturers.

Chan believes uS macroeconomic data are improving and that the general economy will

strengthen in the short term. Chan suggests that a curve trade could be used by the fund to

capitalize on her short-term view of a steepening of the uS credit curve.

another short-term trading opportunity that Smith and Chan discuss involves the merger

and acquisition market. SGS believes that delta Corporation may make an unsolicited bid at

a premium to the market price for all publicly traded shares of Zega, inc. Zega's market cap-

italization and capital structure are comparable to delta's; both firms are highly levered. it is

anticipated that delta will issue new equity along with 5- and 10-year senior unsecured debt

to fund the acquisition, which will significantly increase its debt ratio.

based on exhibit 1, the probability of orion defaulting on the bond during the first three years is closest to:

A) 1.07%.

B) 2.50%.

C) 3.85%.

Question

The following information relates to Questions

John Smith, a fixed-income portfolio manager at a €10 billion sovereign wealth fund

(Swf), meets with Sofia Chan, a derivatives strategist with Shire Gate Securities (SGS),

to discuss investment opportunities for the fund. Chan notes that SGS adheres to iSda

(international Swaps and derivatives association) protocols for credit default swap (CdS)

transactions and that any contract must conform to iSda specifications. before the

fund can engage in trading CdS products with SGS, the fund must satisfy compliance

requirements.

Smith explains to Chan that fixed-income derivatives strategies are being contemplated

for both hedging and trading purposes. Given the size and diversified nature of the fund,

Smith asks Chan to recommend a type of CdS that would allow the Swf to simultaneously

fully hedge multiple fixed-income exposures.

Next, Smith asks Chan to assess the impact on derivative products of recent events affect-

ing Maxx Corporation, a uS company. The Swf holds an unsecured debt instrument issued

by Maxx. Chan says she is very familiar with Maxx because many of its unsecured debt obliga-

tions are commonly included in broad baskets of bonds used for

hedging purposes. SGS recently sold €400 million of protection

on the on-the-run CdX high yield (hY) index that includes a

Maxx bond; the index contains 100 entities. Chan reports that

creditors met with company executives to impose a restructuring on Maxx bonds; as a result,

all outstanding principal obligations will be reduced by 30%.

Smith and Chan discuss opportunities to add trading profits to the Swf. Smith asks Chan

to determine the probability of default associated with a five-year investment-grade bond issued

by orion industrial. Selected data on the orion industrial bond are presented in exhibit 1.

eXhibit 1 Selected data on orion industrial five-Year bond

Chan explains that a single-name CdS can also be used to add profit to the fund over

time. Chan describes a hypothetical trade in which the fund sells £6 million of five-year CdS

protection on orion, where the CdS contract has a duration of 3.9 years. Chan assumes that

the fund closes the position six months later, after orion's credit spread narrowed from 150

bps to 100 bps.

Chan discusses the mechanics of a long/short trade. in order to structure a number of

potential trades, Chan and Smith exchange their respective views on individual companies and

global economies. Chan and Smith agree on the following outlooks.

Outlook 1: italy's economy will weaken.

Outlook 2: The uS economy will strengthen relative to that of Canada.

Outlook 3: The credit quality of electric car manufacturers will improve relative to that of

traditional car manufacturers.

Chan believes uS macroeconomic data are improving and that the general economy will

strengthen in the short term. Chan suggests that a curve trade could be used by the fund to

capitalize on her short-term view of a steepening of the uS credit curve.

another short-term trading opportunity that Smith and Chan discuss involves the merger

and acquisition market. SGS believes that delta Corporation may make an unsolicited bid at

a premium to the market price for all publicly traded shares of Zega, inc. Zega's market cap-

italization and capital structure are comparable to delta's; both firms are highly levered. it is

anticipated that delta will issue new equity along with 5- and 10-year senior unsecured debt

to fund the acquisition, which will significantly increase its debt ratio.

which type of CdS should Chan recommend to Smith?

A) CdS index

B) tranche CdS

C) Single-name CdS

John Smith, a fixed-income portfolio manager at a €10 billion sovereign wealth fund

(Swf), meets with Sofia Chan, a derivatives strategist with Shire Gate Securities (SGS),

to discuss investment opportunities for the fund. Chan notes that SGS adheres to iSda

(international Swaps and derivatives association) protocols for credit default swap (CdS)

transactions and that any contract must conform to iSda specifications. before the

fund can engage in trading CdS products with SGS, the fund must satisfy compliance

requirements.

Smith explains to Chan that fixed-income derivatives strategies are being contemplated

for both hedging and trading purposes. Given the size and diversified nature of the fund,

Smith asks Chan to recommend a type of CdS that would allow the Swf to simultaneously

fully hedge multiple fixed-income exposures.

Next, Smith asks Chan to assess the impact on derivative products of recent events affect-

ing Maxx Corporation, a uS company. The Swf holds an unsecured debt instrument issued

by Maxx. Chan says she is very familiar with Maxx because many of its unsecured debt obliga-

tions are commonly included in broad baskets of bonds used for

hedging purposes. SGS recently sold €400 million of protection

on the on-the-run CdX high yield (hY) index that includes a

Maxx bond; the index contains 100 entities. Chan reports that

creditors met with company executives to impose a restructuring on Maxx bonds; as a result,

all outstanding principal obligations will be reduced by 30%.

Smith and Chan discuss opportunities to add trading profits to the Swf. Smith asks Chan

to determine the probability of default associated with a five-year investment-grade bond issued

by orion industrial. Selected data on the orion industrial bond are presented in exhibit 1.

eXhibit 1 Selected data on orion industrial five-Year bond

Chan explains that a single-name CdS can also be used to add profit to the fund over

time. Chan describes a hypothetical trade in which the fund sells £6 million of five-year CdS

protection on orion, where the CdS contract has a duration of 3.9 years. Chan assumes that

the fund closes the position six months later, after orion's credit spread narrowed from 150

bps to 100 bps.

Chan discusses the mechanics of a long/short trade. in order to structure a number of

potential trades, Chan and Smith exchange their respective views on individual companies and

global economies. Chan and Smith agree on the following outlooks.

Outlook 1: italy's economy will weaken.

Outlook 2: The uS economy will strengthen relative to that of Canada.

Outlook 3: The credit quality of electric car manufacturers will improve relative to that of

traditional car manufacturers.

Chan believes uS macroeconomic data are improving and that the general economy will

strengthen in the short term. Chan suggests that a curve trade could be used by the fund to

capitalize on her short-term view of a steepening of the uS credit curve.

another short-term trading opportunity that Smith and Chan discuss involves the merger

and acquisition market. SGS believes that delta Corporation may make an unsolicited bid at

a premium to the market price for all publicly traded shares of Zega, inc. Zega's market cap-

italization and capital structure are comparable to delta's; both firms are highly levered. it is

anticipated that delta will issue new equity along with 5- and 10-year senior unsecured debt

to fund the acquisition, which will significantly increase its debt ratio.

which type of CdS should Chan recommend to Smith?

A) CdS index

B) tranche CdS

C) Single-name CdS

Question

required and, if so, the amount of the premium. watt presents the information for the CdS in exhibit 1.

Morrison purchases the 10-year CdS on Kand Corporation debt. two months later the credit spread for Kand Corp. has increased by 200 basis points. Morrison asks watt

to close out the firm's CdS position on Kand Corporation by entering into new offsetting

contracts.

Tollunt Corporation

deem advisors' chief credit analyst recently reported that tollunt Corporation's five-year bond

is currently yielding 7% and a comparable CdS contract has a credit spread of 4.25%. Since

libor is 2.5%, watt has recommended executing a basis trade to take advantage of the pricing

of tollunt's bonds and CdS. The basis trade would consist of purchasing both the bond and

the CdS contract.

based on exhibit 1, the upfront premium as a percent of the notional for the CdS protec- tion on Kand Corp. would be closest to:

A) 2.0%.

B) 9.8%.

C) 14.0%.

Question

The following information relates to Questions

John Smith, a fixed-income portfolio manager at a €10 billion sovereign wealth fund

(Swf), meets with Sofia Chan, a derivatives strategist with Shire Gate Securities (SGS),

to discuss investment opportunities for the fund. Chan notes that SGS adheres to iSda

(international Swaps and derivatives association) protocols for credit default swap (CdS)

transactions and that any contract must conform to iSda specifications. before the

fund can engage in trading CdS products with SGS, the fund must satisfy compliance

requirements.

Smith explains to Chan that fixed-income derivatives strategies are being contemplated

for both hedging and trading purposes. Given the size and diversified nature of the fund,

Smith asks Chan to recommend a type of CdS that would allow the Swf to simultaneously

fully hedge multiple fixed-income exposures.

Next, Smith asks Chan to assess the impact on derivative products of recent events affect-

ing Maxx Corporation, a uS company. The Swf holds an unsecured debt instrument issued

by Maxx. Chan says she is very familiar with Maxx because many of its unsecured debt obliga-

tions are commonly included in broad baskets of bonds used for

hedging purposes. SGS recently sold €400 million of protection

on the on-the-run CdX high yield (hY) index that includes a

Maxx bond; the index contains 100 entities. Chan reports that

creditors met with company executives to impose a restructuring on Maxx bonds; as a result,

all outstanding principal obligations will be reduced by 30%.

Smith and Chan discuss opportunities to add trading profits to the Swf. Smith asks Chan

to determine the probability of default associated with a five-year investment-grade bond issued

by orion industrial. Selected data on the orion industrial bond are presented in exhibit 1.

eXhibit 1 Selected data on orion industrial five-Year bond

Chan explains that a single-name CdS can also be used to add profit to the fund over

time. Chan describes a hypothetical trade in which the fund sells £6 million of five-year CdS

protection on orion, where the CdS contract has a duration of 3.9 years. Chan assumes that

the fund closes the position six months later, after orion's credit spread narrowed from 150

bps to 100 bps.

Chan discusses the mechanics of a long/short trade. in order to structure a number of

potential trades, Chan and Smith exchange their respective views on individual companies and

global economies. Chan and Smith agree on the following outlooks.

Outlook 1: italy's economy will weaken.

Outlook 2: The uS economy will strengthen relative to that of Canada.

Outlook 3: The credit quality of electric car manufacturers will improve relative to that of

traditional car manufacturers.

Chan believes uS macroeconomic data are improving and that the general economy will

strengthen in the short term. Chan suggests that a curve trade could be used by the fund to

capitalize on her short-term view of a steepening of the uS credit curve.

another short-term trading opportunity that Smith and Chan discuss involves the merger

and acquisition market. SGS believes that delta Corporation may make an unsolicited bid at

a premium to the market price for all publicly traded shares of Zega, inc. Zega's market cap-

italization and capital structure are comparable to delta's; both firms are highly levered. it is

anticipated that delta will issue new equity along with 5- and 10-year senior unsecured debt

to fund the acquisition, which will significantly increase its debt ratio.

a profitable equity-versus-credit trade involving delta and Zega is to:

A) short Zega shares and short delta 10-year CdS.

B) go long Zega shares and short delta 5-year CdS.

C) go long delta shares and go long delta 5-year CdS.

John Smith, a fixed-income portfolio manager at a €10 billion sovereign wealth fund

(Swf), meets with Sofia Chan, a derivatives strategist with Shire Gate Securities (SGS),

to discuss investment opportunities for the fund. Chan notes that SGS adheres to iSda

(international Swaps and derivatives association) protocols for credit default swap (CdS)

transactions and that any contract must conform to iSda specifications. before the

fund can engage in trading CdS products with SGS, the fund must satisfy compliance

requirements.

Smith explains to Chan that fixed-income derivatives strategies are being contemplated

for both hedging and trading purposes. Given the size and diversified nature of the fund,

Smith asks Chan to recommend a type of CdS that would allow the Swf to simultaneously

fully hedge multiple fixed-income exposures.

Next, Smith asks Chan to assess the impact on derivative products of recent events affect-

ing Maxx Corporation, a uS company. The Swf holds an unsecured debt instrument issued

by Maxx. Chan says she is very familiar with Maxx because many of its unsecured debt obliga-

tions are commonly included in broad baskets of bonds used for

hedging purposes. SGS recently sold €400 million of protection

on the on-the-run CdX high yield (hY) index that includes a

Maxx bond; the index contains 100 entities. Chan reports that

creditors met with company executives to impose a restructuring on Maxx bonds; as a result,

all outstanding principal obligations will be reduced by 30%.

Smith and Chan discuss opportunities to add trading profits to the Swf. Smith asks Chan

to determine the probability of default associated with a five-year investment-grade bond issued

by orion industrial. Selected data on the orion industrial bond are presented in exhibit 1.

eXhibit 1 Selected data on orion industrial five-Year bond

Chan explains that a single-name CdS can also be used to add profit to the fund over

time. Chan describes a hypothetical trade in which the fund sells £6 million of five-year CdS

protection on orion, where the CdS contract has a duration of 3.9 years. Chan assumes that

the fund closes the position six months later, after orion's credit spread narrowed from 150

bps to 100 bps.

Chan discusses the mechanics of a long/short trade. in order to structure a number of

potential trades, Chan and Smith exchange their respective views on individual companies and

global economies. Chan and Smith agree on the following outlooks.

Outlook 1: italy's economy will weaken.

Outlook 2: The uS economy will strengthen relative to that of Canada.

Outlook 3: The credit quality of electric car manufacturers will improve relative to that of

traditional car manufacturers.

Chan believes uS macroeconomic data are improving and that the general economy will

strengthen in the short term. Chan suggests that a curve trade could be used by the fund to

capitalize on her short-term view of a steepening of the uS credit curve.

another short-term trading opportunity that Smith and Chan discuss involves the merger

and acquisition market. SGS believes that delta Corporation may make an unsolicited bid at

a premium to the market price for all publicly traded shares of Zega, inc. Zega's market cap-

italization and capital structure are comparable to delta's; both firms are highly levered. it is

anticipated that delta will issue new equity along with 5- and 10-year senior unsecured debt

to fund the acquisition, which will significantly increase its debt ratio.

a profitable equity-versus-credit trade involving delta and Zega is to:

A) short Zega shares and short delta 10-year CdS.

B) go long Zega shares and short delta 5-year CdS.

C) go long delta shares and go long delta 5-year CdS.

Question

required and, if so, the amount of the premium. watt presents the information for the CdS in exhibit 1.

Morrison purchases the 10-year CdS on Kand Corporation debt. two months later the credit spread for Kand Corp. has increased by 200 basis points. Morrison asks watt

to close out the firm's CdS position on Kand Corporation by entering into new offsetting

contracts.

Tollunt Corporation

deem advisors' chief credit analyst recently reported that tollunt Corporation's five-year bond

is currently yielding 7% and a comparable CdS contract has a credit spread of 4.25%. Since

libor is 2.5%, watt has recommended executing a basis trade to take advantage of the pricing

of tollunt's bonds and CdS. The basis trade would consist of purchasing both the bond and

the CdS contract.

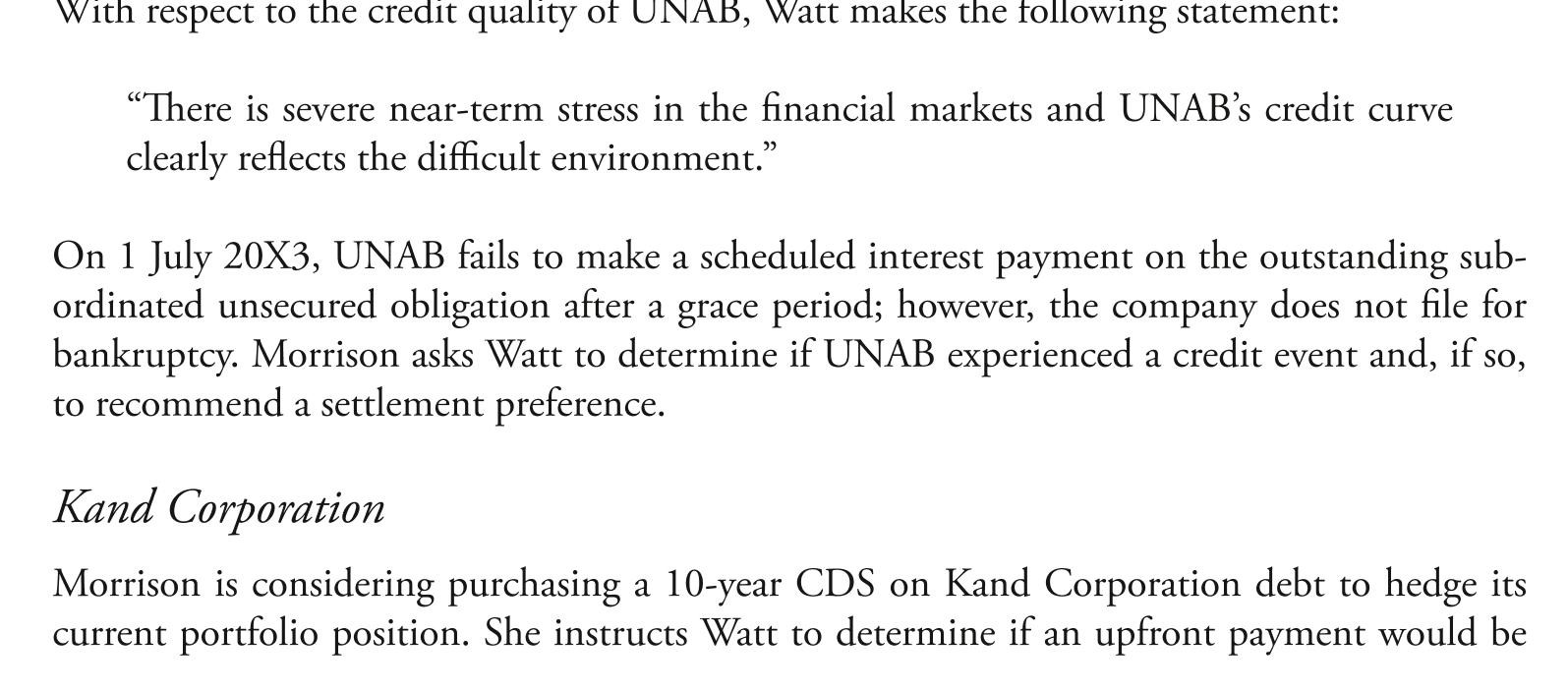

Should watt conclude that uNab experienced a credit event?

A) Yes.

B) No, because uNab did not file for bankruptcy.

C) No, because the failure to pay occurred on a subordinated unsecured bond.

Question

The following information relates to Questions

John Smith, a fixed-income portfolio manager at a €10 billion sovereign wealth fund

(Swf), meets with Sofia Chan, a derivatives strategist with Shire Gate Securities (SGS),

to discuss investment opportunities for the fund. Chan notes that SGS adheres to iSda

(international Swaps and derivatives association) protocols for credit default swap (CdS)

transactions and that any contract must conform to iSda specifications. before the

fund can engage in trading CdS products with SGS, the fund must satisfy compliance

requirements.

Smith explains to Chan that fixed-income derivatives strategies are being contemplated

for both hedging and trading purposes. Given the size and diversified nature of the fund,

Smith asks Chan to recommend a type of CdS that would allow the Swf to simultaneously

fully hedge multiple fixed-income exposures.

Next, Smith asks Chan to assess the impact on derivative products of recent events affect-

ing Maxx Corporation, a uS company. The Swf holds an unsecured debt instrument issued

by Maxx. Chan says she is very familiar with Maxx because many of its unsecured debt obliga-

tions are commonly included in broad baskets of bonds used for

hedging purposes. SGS recently sold €400 million of protection

on the on-the-run CdX high yield (hY) index that includes a

Maxx bond; the index contains 100 entities. Chan reports that

creditors met with company executives to impose a restructuring on Maxx bonds; as a result,

all outstanding principal obligations will be reduced by 30%.

Smith and Chan discuss opportunities to add trading profits to the Swf. Smith asks Chan

to determine the probability of default associated with a five-year investment-grade bond issued

by orion industrial. Selected data on the orion industrial bond are presented in exhibit 1.

eXhibit 1 Selected data on orion industrial five-Year bond

Chan explains that a single-name CdS can also be used to add profit to the fund over

time. Chan describes a hypothetical trade in which the fund sells £6 million of five-year CdS

protection on orion, where the CdS contract has a duration of 3.9 years. Chan assumes that

the fund closes the position six months later, after orion's credit spread narrowed from 150

bps to 100 bps.

Chan discusses the mechanics of a long/short trade. in order to structure a number of

potential trades, Chan and Smith exchange their respective views on individual companies and

global economies. Chan and Smith agree on the following outlooks.

Outlook 1: italy's economy will weaken.

Outlook 2: The uS economy will strengthen relative to that of Canada.

Outlook 3: The credit quality of electric car manufacturers will improve relative to that of

traditional car manufacturers.

Chan believes uS macroeconomic data are improving and that the general economy will

strengthen in the short term. Chan suggests that a curve trade could be used by the fund to

capitalize on her short-term view of a steepening of the uS credit curve.

another short-term trading opportunity that Smith and Chan discuss involves the merger

and acquisition market. SGS believes that delta Corporation may make an unsolicited bid at

a premium to the market price for all publicly traded shares of Zega, inc. Zega's market cap-

italization and capital structure are comparable to delta's; both firms are highly levered. it is

anticipated that delta will issue new equity along with 5- and 10-year senior unsecured debt

to fund the acquisition, which will significantly increase its debt ratio.

The hypothetical orion trade generated an approximate:

A) loss of £117,000.

B) gain of £117,000.

C) gain of £234,000.

John Smith, a fixed-income portfolio manager at a €10 billion sovereign wealth fund

(Swf), meets with Sofia Chan, a derivatives strategist with Shire Gate Securities (SGS),

to discuss investment opportunities for the fund. Chan notes that SGS adheres to iSda

(international Swaps and derivatives association) protocols for credit default swap (CdS)

transactions and that any contract must conform to iSda specifications. before the

fund can engage in trading CdS products with SGS, the fund must satisfy compliance

requirements.

Smith explains to Chan that fixed-income derivatives strategies are being contemplated

for both hedging and trading purposes. Given the size and diversified nature of the fund,

Smith asks Chan to recommend a type of CdS that would allow the Swf to simultaneously

fully hedge multiple fixed-income exposures.

Next, Smith asks Chan to assess the impact on derivative products of recent events affect-

ing Maxx Corporation, a uS company. The Swf holds an unsecured debt instrument issued

by Maxx. Chan says she is very familiar with Maxx because many of its unsecured debt obliga-

tions are commonly included in broad baskets of bonds used for

hedging purposes. SGS recently sold €400 million of protection

on the on-the-run CdX high yield (hY) index that includes a

Maxx bond; the index contains 100 entities. Chan reports that

creditors met with company executives to impose a restructuring on Maxx bonds; as a result,

all outstanding principal obligations will be reduced by 30%.

Smith and Chan discuss opportunities to add trading profits to the Swf. Smith asks Chan

to determine the probability of default associated with a five-year investment-grade bond issued

by orion industrial. Selected data on the orion industrial bond are presented in exhibit 1.

eXhibit 1 Selected data on orion industrial five-Year bond

Chan explains that a single-name CdS can also be used to add profit to the fund over

time. Chan describes a hypothetical trade in which the fund sells £6 million of five-year CdS

protection on orion, where the CdS contract has a duration of 3.9 years. Chan assumes that

the fund closes the position six months later, after orion's credit spread narrowed from 150

bps to 100 bps.

Chan discusses the mechanics of a long/short trade. in order to structure a number of

potential trades, Chan and Smith exchange their respective views on individual companies and

global economies. Chan and Smith agree on the following outlooks.

Outlook 1: italy's economy will weaken.

Outlook 2: The uS economy will strengthen relative to that of Canada.

Outlook 3: The credit quality of electric car manufacturers will improve relative to that of

traditional car manufacturers.

Chan believes uS macroeconomic data are improving and that the general economy will

strengthen in the short term. Chan suggests that a curve trade could be used by the fund to

capitalize on her short-term view of a steepening of the uS credit curve.

another short-term trading opportunity that Smith and Chan discuss involves the merger

and acquisition market. SGS believes that delta Corporation may make an unsolicited bid at

a premium to the market price for all publicly traded shares of Zega, inc. Zega's market cap-

italization and capital structure are comparable to delta's; both firms are highly levered. it is

anticipated that delta will issue new equity along with 5- and 10-year senior unsecured debt

to fund the acquisition, which will significantly increase its debt ratio.

The hypothetical orion trade generated an approximate:

A) loss of £117,000.

B) gain of £117,000.

C) gain of £234,000.

Question

The following information relates to Questions

John Smith, a fixed-income portfolio manager at a €10 billion sovereign wealth fund

(Swf), meets with Sofia Chan, a derivatives strategist with Shire Gate Securities (SGS),

to discuss investment opportunities for the fund. Chan notes that SGS adheres to iSda

(international Swaps and derivatives association) protocols for credit default swap (CdS)

transactions and that any contract must conform to iSda specifications. before the

fund can engage in trading CdS products with SGS, the fund must satisfy compliance

requirements.

Smith explains to Chan that fixed-income derivatives strategies are being contemplated

for both hedging and trading purposes. Given the size and diversified nature of the fund,

Smith asks Chan to recommend a type of CdS that would allow the Swf to simultaneously

fully hedge multiple fixed-income exposures.

Next, Smith asks Chan to assess the impact on derivative products of recent events affect-

ing Maxx Corporation, a uS company. The Swf holds an unsecured debt instrument issued

by Maxx. Chan says she is very familiar with Maxx because many of its unsecured debt obliga-

tions are commonly included in broad baskets of bonds used for

hedging purposes. SGS recently sold €400 million of protection

on the on-the-run CdX high yield (hY) index that includes a

Maxx bond; the index contains 100 entities. Chan reports that

creditors met with company executives to impose a restructuring on Maxx bonds; as a result,

all outstanding principal obligations will be reduced by 30%.

Smith and Chan discuss opportunities to add trading profits to the Swf. Smith asks Chan

to determine the probability of default associated with a five-year investment-grade bond issued

by orion industrial. Selected data on the orion industrial bond are presented in exhibit 1.

eXhibit 1 Selected data on orion industrial five-Year bond

Chan explains that a single-name CdS can also be used to add profit to the fund over

time. Chan describes a hypothetical trade in which the fund sells £6 million of five-year CdS

protection on orion, where the CdS contract has a duration of 3.9 years. Chan assumes that

the fund closes the position six months later, after orion's credit spread narrowed from 150

bps to 100 bps.

Chan discusses the mechanics of a long/short trade. in order to structure a number of

potential trades, Chan and Smith exchange their respective views on individual companies and

global economies. Chan and Smith agree on the following outlooks.

Outlook 1: italy's economy will weaken.

Outlook 2: The uS economy will strengthen relative to that of Canada.

Outlook 3: The credit quality of electric car manufacturers will improve relative to that of

traditional car manufacturers.

Chan believes uS macroeconomic data are improving and that the general economy will

strengthen in the short term. Chan suggests that a curve trade could be used by the fund to

capitalize on her short-term view of a steepening of the uS credit curve.

another short-term trading opportunity that Smith and Chan discuss involves the merger

and acquisition market. SGS believes that delta Corporation may make an unsolicited bid at

a premium to the market price for all publicly traded shares of Zega, inc. Zega's market cap-

italization and capital structure are comparable to delta's; both firms are highly levered. it is

anticipated that delta will issue new equity along with 5- and 10-year senior unsecured debt

to fund the acquisition, which will significantly increase its debt ratio.

to close the position on the hypothetical orion trade, the fund:

A) sells protection at a higher premium than it paid at the start of the trade.

B) buys protection at a lower premium than it received at the start of the trade.

C) buys protection at a higher premium than it received at the start of the trade.

John Smith, a fixed-income portfolio manager at a €10 billion sovereign wealth fund

(Swf), meets with Sofia Chan, a derivatives strategist with Shire Gate Securities (SGS),

to discuss investment opportunities for the fund. Chan notes that SGS adheres to iSda

(international Swaps and derivatives association) protocols for credit default swap (CdS)

transactions and that any contract must conform to iSda specifications. before the

fund can engage in trading CdS products with SGS, the fund must satisfy compliance

requirements.

Smith explains to Chan that fixed-income derivatives strategies are being contemplated

for both hedging and trading purposes. Given the size and diversified nature of the fund,

Smith asks Chan to recommend a type of CdS that would allow the Swf to simultaneously

fully hedge multiple fixed-income exposures.

Next, Smith asks Chan to assess the impact on derivative products of recent events affect-

ing Maxx Corporation, a uS company. The Swf holds an unsecured debt instrument issued

by Maxx. Chan says she is very familiar with Maxx because many of its unsecured debt obliga-

tions are commonly included in broad baskets of bonds used for

hedging purposes. SGS recently sold €400 million of protection

on the on-the-run CdX high yield (hY) index that includes a

Maxx bond; the index contains 100 entities. Chan reports that

creditors met with company executives to impose a restructuring on Maxx bonds; as a result,

all outstanding principal obligations will be reduced by 30%.

Smith and Chan discuss opportunities to add trading profits to the Swf. Smith asks Chan

to determine the probability of default associated with a five-year investment-grade bond issued

by orion industrial. Selected data on the orion industrial bond are presented in exhibit 1.

eXhibit 1 Selected data on orion industrial five-Year bond

Chan explains that a single-name CdS can also be used to add profit to the fund over

time. Chan describes a hypothetical trade in which the fund sells £6 million of five-year CdS

protection on orion, where the CdS contract has a duration of 3.9 years. Chan assumes that

the fund closes the position six months later, after orion's credit spread narrowed from 150

bps to 100 bps.

Chan discusses the mechanics of a long/short trade. in order to structure a number of

potential trades, Chan and Smith exchange their respective views on individual companies and

global economies. Chan and Smith agree on the following outlooks.

Outlook 1: italy's economy will weaken.

Outlook 2: The uS economy will strengthen relative to that of Canada.

Outlook 3: The credit quality of electric car manufacturers will improve relative to that of

traditional car manufacturers.

Chan believes uS macroeconomic data are improving and that the general economy will

strengthen in the short term. Chan suggests that a curve trade could be used by the fund to

capitalize on her short-term view of a steepening of the uS credit curve.

another short-term trading opportunity that Smith and Chan discuss involves the merger

and acquisition market. SGS believes that delta Corporation may make an unsolicited bid at

a premium to the market price for all publicly traded shares of Zega, inc. Zega's market cap-

italization and capital structure are comparable to delta's; both firms are highly levered. it is

anticipated that delta will issue new equity along with 5- and 10-year senior unsecured debt

to fund the acquisition, which will significantly increase its debt ratio.

to close the position on the hypothetical orion trade, the fund:

A) sells protection at a higher premium than it paid at the start of the trade.

B) buys protection at a lower premium than it received at the start of the trade.

C) buys protection at a higher premium than it received at the start of the trade.

Question

The following information relates to Questions

John Smith, a fixed-income portfolio manager at a €10 billion sovereign wealth fund

(Swf), meets with Sofia Chan, a derivatives strategist with Shire Gate Securities (SGS),

to discuss investment opportunities for the fund. Chan notes that SGS adheres to iSda

(international Swaps and derivatives association) protocols for credit default swap (CdS)

transactions and that any contract must conform to iSda specifications. before the

fund can engage in trading CdS products with SGS, the fund must satisfy compliance

requirements.

Smith explains to Chan that fixed-income derivatives strategies are being contemplated

for both hedging and trading purposes. Given the size and diversified nature of the fund,

Smith asks Chan to recommend a type of CdS that would allow the Swf to simultaneously

fully hedge multiple fixed-income exposures.

Next, Smith asks Chan to assess the impact on derivative products of recent events affect-

ing Maxx Corporation, a uS company. The Swf holds an unsecured debt instrument issued

by Maxx. Chan says she is very familiar with Maxx because many of its unsecured debt obliga-

tions are commonly included in broad baskets of bonds used for

hedging purposes. SGS recently sold €400 million of protection

on the on-the-run CdX high yield (hY) index that includes a

Maxx bond; the index contains 100 entities. Chan reports that

creditors met with company executives to impose a restructuring on Maxx bonds; as a result,

all outstanding principal obligations will be reduced by 30%.

Smith and Chan discuss opportunities to add trading profits to the Swf. Smith asks Chan

to determine the probability of default associated with a five-year investment-grade bond issued

by orion industrial. Selected data on the orion industrial bond are presented in exhibit 1.

eXhibit 1 Selected data on orion industrial five-Year bond

Chan explains that a single-name CdS can also be used to add profit to the fund over

time. Chan describes a hypothetical trade in which the fund sells £6 million of five-year CdS

protection on orion, where the CdS contract has a duration of 3.9 years. Chan assumes that

the fund closes the position six months later, after orion's credit spread narrowed from 150

bps to 100 bps.

Chan discusses the mechanics of a long/short trade. in order to structure a number of

potential trades, Chan and Smith exchange their respective views on individual companies and

global economies. Chan and Smith agree on the following outlooks.

Outlook 1: italy's economy will weaken.

Outlook 2: The uS economy will strengthen relative to that of Canada.

Outlook 3: The credit quality of electric car manufacturers will improve relative to that of

traditional car manufacturers.

Chan believes uS macroeconomic data are improving and that the general economy will

strengthen in the short term. Chan suggests that a curve trade could be used by the fund to

capitalize on her short-term view of a steepening of the uS credit curve.

another short-term trading opportunity that Smith and Chan discuss involves the merger

and acquisition market. SGS believes that delta Corporation may make an unsolicited bid at

a premium to the market price for all publicly traded shares of Zega, inc. Zega's market cap-

italization and capital structure are comparable to delta's; both firms are highly levered. it is

anticipated that delta will issue new equity along with 5- and 10-year senior unsecured debt

to fund the acquisition, which will significantly increase its debt ratio.

based on the three economic outlook statements, a profitable long/short trade would be to:

A) go long a Canadian CdX iG and short a uS CdX iG.

B) short an itraxx Crossover and go long an itraxx Main.

C) short electric car CdS and go long traditional car CdS.

John Smith, a fixed-income portfolio manager at a €10 billion sovereign wealth fund

(Swf), meets with Sofia Chan, a derivatives strategist with Shire Gate Securities (SGS),

to discuss investment opportunities for the fund. Chan notes that SGS adheres to iSda

(international Swaps and derivatives association) protocols for credit default swap (CdS)

transactions and that any contract must conform to iSda specifications. before the

fund can engage in trading CdS products with SGS, the fund must satisfy compliance

requirements.

Smith explains to Chan that fixed-income derivatives strategies are being contemplated

for both hedging and trading purposes. Given the size and diversified nature of the fund,

Smith asks Chan to recommend a type of CdS that would allow the Swf to simultaneously

fully hedge multiple fixed-income exposures.

Next, Smith asks Chan to assess the impact on derivative products of recent events affect-

ing Maxx Corporation, a uS company. The Swf holds an unsecured debt instrument issued

by Maxx. Chan says she is very familiar with Maxx because many of its unsecured debt obliga-

tions are commonly included in broad baskets of bonds used for

hedging purposes. SGS recently sold €400 million of protection

on the on-the-run CdX high yield (hY) index that includes a

Maxx bond; the index contains 100 entities. Chan reports that

creditors met with company executives to impose a restructuring on Maxx bonds; as a result,

all outstanding principal obligations will be reduced by 30%.

Smith and Chan discuss opportunities to add trading profits to the Swf. Smith asks Chan

to determine the probability of default associated with a five-year investment-grade bond issued

by orion industrial. Selected data on the orion industrial bond are presented in exhibit 1.

eXhibit 1 Selected data on orion industrial five-Year bond

Chan explains that a single-name CdS can also be used to add profit to the fund over

time. Chan describes a hypothetical trade in which the fund sells £6 million of five-year CdS

protection on orion, where the CdS contract has a duration of 3.9 years. Chan assumes that

the fund closes the position six months later, after orion's credit spread narrowed from 150

bps to 100 bps.

Chan discusses the mechanics of a long/short trade. in order to structure a number of

potential trades, Chan and Smith exchange their respective views on individual companies and

global economies. Chan and Smith agree on the following outlooks.

Outlook 1: italy's economy will weaken.

Outlook 2: The uS economy will strengthen relative to that of Canada.

Outlook 3: The credit quality of electric car manufacturers will improve relative to that of

traditional car manufacturers.

Chan believes uS macroeconomic data are improving and that the general economy will

strengthen in the short term. Chan suggests that a curve trade could be used by the fund to

capitalize on her short-term view of a steepening of the uS credit curve.

another short-term trading opportunity that Smith and Chan discuss involves the merger

and acquisition market. SGS believes that delta Corporation may make an unsolicited bid at

a premium to the market price for all publicly traded shares of Zega, inc. Zega's market cap-

italization and capital structure are comparable to delta's; both firms are highly levered. it is

anticipated that delta will issue new equity along with 5- and 10-year senior unsecured debt

to fund the acquisition, which will significantly increase its debt ratio.

based on the three economic outlook statements, a profitable long/short trade would be to:

A) go long a Canadian CdX iG and short a uS CdX iG.

B) short an itraxx Crossover and go long an itraxx Main.

C) short electric car CdS and go long traditional car CdS.

Question

required and, if so, the amount of the premium. watt presents the information for the CdS in exhibit 1.

Morrison purchases the 10-year CdS on Kand Corporation debt. two months later the credit spread for Kand Corp. has increased by 200 basis points. Morrison asks watt

to close out the firm's CdS position on Kand Corporation by entering into new offsetting

contracts.

Tollunt Corporation

deem advisors' chief credit analyst recently reported that tollunt Corporation's five-year bond

is currently yielding 7% and a comparable CdS contract has a credit spread of 4.25%. Since

libor is 2.5%, watt has recommended executing a basis trade to take advantage of the pricing

of tollunt's bonds and CdS. The basis trade would consist of purchasing both the bond and

the CdS contract.

based on basis trade for tollunt Corporation, if convergence occurs in the bond and CdS markets, the trade will capture a profit closest to:

A) 0.25%.

B) 1.75%.

C) 2.75%.

Question

The following information relates to Questions

John Smith, a fixed-income portfolio manager at a €10 billion sovereign wealth fund

(Swf), meets with Sofia Chan, a derivatives strategist with Shire Gate Securities (SGS),

to discuss investment opportunities for the fund. Chan notes that SGS adheres to iSda

(international Swaps and derivatives association) protocols for credit default swap (CdS)

transactions and that any contract must conform to iSda specifications. before the

fund can engage in trading CdS products with SGS, the fund must satisfy compliance

requirements.

Smith explains to Chan that fixed-income derivatives strategies are being contemplated

for both hedging and trading purposes. Given the size and diversified nature of the fund,

Smith asks Chan to recommend a type of CdS that would allow the Swf to simultaneously

fully hedge multiple fixed-income exposures.

Next, Smith asks Chan to assess the impact on derivative products of recent events affect-

ing Maxx Corporation, a uS company. The Swf holds an unsecured debt instrument issued

by Maxx. Chan says she is very familiar with Maxx because many of its unsecured debt obliga-

tions are commonly included in broad baskets of bonds used for

hedging purposes. SGS recently sold €400 million of protection

on the on-the-run CdX high yield (hY) index that includes a

Maxx bond; the index contains 100 entities. Chan reports that

creditors met with company executives to impose a restructuring on Maxx bonds; as a result,

all outstanding principal obligations will be reduced by 30%.

Smith and Chan discuss opportunities to add trading profits to the Swf. Smith asks Chan

to determine the probability of default associated with a five-year investment-grade bond issued

by orion industrial. Selected data on the orion industrial bond are presented in exhibit 1.

eXhibit 1 Selected data on orion industrial five-Year bond

Chan explains that a single-name CdS can also be used to add profit to the fund over

time. Chan describes a hypothetical trade in which the fund sells £6 million of five-year CdS

protection on orion, where the CdS contract has a duration of 3.9 years. Chan assumes that

the fund closes the position six months later, after orion's credit spread narrowed from 150

bps to 100 bps.

Chan discusses the mechanics of a long/short trade. in order to structure a number of

potential trades, Chan and Smith exchange their respective views on individual companies and

global economies. Chan and Smith agree on the following outlooks.

Outlook 1: italy's economy will weaken.

Outlook 2: The uS economy will strengthen relative to that of Canada.

Outlook 3: The credit quality of electric car manufacturers will improve relative to that of

traditional car manufacturers.

Chan believes uS macroeconomic data are improving and that the general economy will

strengthen in the short term. Chan suggests that a curve trade could be used by the fund to

capitalize on her short-term view of a steepening of the uS credit curve.

another short-term trading opportunity that Smith and Chan discuss involves the merger

and acquisition market. SGS believes that delta Corporation may make an unsolicited bid at

a premium to the market price for all publicly traded shares of Zega, inc. Zega's market cap-

italization and capital structure are comparable to delta's; both firms are highly levered. it is

anticipated that delta will issue new equity along with 5- and 10-year senior unsecured debt

to fund the acquisition, which will significantly increase its debt ratio.

The curve trade that would best capitalize on Chan's view of the uS credit curve is to:

A) short a 20-year CdX and short a 2-year CdX.

B) short a 20-year CdX and go long a 2-year CdX.

C) go long a 20-year CdX and short a 2-year CdX.

John Smith, a fixed-income portfolio manager at a €10 billion sovereign wealth fund

(Swf), meets with Sofia Chan, a derivatives strategist with Shire Gate Securities (SGS),

to discuss investment opportunities for the fund. Chan notes that SGS adheres to iSda

(international Swaps and derivatives association) protocols for credit default swap (CdS)

transactions and that any contract must conform to iSda specifications. before the

fund can engage in trading CdS products with SGS, the fund must satisfy compliance

requirements.

Smith explains to Chan that fixed-income derivatives strategies are being contemplated

for both hedging and trading purposes. Given the size and diversified nature of the fund,

Smith asks Chan to recommend a type of CdS that would allow the Swf to simultaneously

fully hedge multiple fixed-income exposures.

Next, Smith asks Chan to assess the impact on derivative products of recent events affect-

ing Maxx Corporation, a uS company. The Swf holds an unsecured debt instrument issued

by Maxx. Chan says she is very familiar with Maxx because many of its unsecured debt obliga-

tions are commonly included in broad baskets of bonds used for

hedging purposes. SGS recently sold €400 million of protection

on the on-the-run CdX high yield (hY) index that includes a

Maxx bond; the index contains 100 entities. Chan reports that

creditors met with company executives to impose a restructuring on Maxx bonds; as a result,

all outstanding principal obligations will be reduced by 30%.

Smith and Chan discuss opportunities to add trading profits to the Swf. Smith asks Chan

to determine the probability of default associated with a five-year investment-grade bond issued

by orion industrial. Selected data on the orion industrial bond are presented in exhibit 1.

eXhibit 1 Selected data on orion industrial five-Year bond

Chan explains that a single-name CdS can also be used to add profit to the fund over

time. Chan describes a hypothetical trade in which the fund sells £6 million of five-year CdS

protection on orion, where the CdS contract has a duration of 3.9 years. Chan assumes that

the fund closes the position six months later, after orion's credit spread narrowed from 150

bps to 100 bps.

Chan discusses the mechanics of a long/short trade. in order to structure a number of

potential trades, Chan and Smith exchange their respective views on individual companies and

global economies. Chan and Smith agree on the following outlooks.

Outlook 1: italy's economy will weaken.

Outlook 2: The uS economy will strengthen relative to that of Canada.

Outlook 3: The credit quality of electric car manufacturers will improve relative to that of

traditional car manufacturers.

Chan believes uS macroeconomic data are improving and that the general economy will

strengthen in the short term. Chan suggests that a curve trade could be used by the fund to

capitalize on her short-term view of a steepening of the uS credit curve.

another short-term trading opportunity that Smith and Chan discuss involves the merger

and acquisition market. SGS believes that delta Corporation may make an unsolicited bid at

a premium to the market price for all publicly traded shares of Zega, inc. Zega's market cap-

italization and capital structure are comparable to delta's; both firms are highly levered. it is

anticipated that delta will issue new equity along with 5- and 10-year senior unsecured debt

to fund the acquisition, which will significantly increase its debt ratio.

The curve trade that would best capitalize on Chan's view of the uS credit curve is to:

A) short a 20-year CdX and short a 2-year CdX.

B) short a 20-year CdX and go long a 2-year CdX.

C) go long a 20-year CdX and short a 2-year CdX.

Question

required and, if so, the amount of the premium. watt presents the information for the CdS in exhibit 1.

Morrison purchases the 10-year CdS on Kand Corporation debt. two months later the credit spread for Kand Corp. has increased by 200 basis points. Morrison asks watt

to close out the firm's CdS position on Kand Corporation by entering into new offsetting

contracts.

Tollunt Corporation

deem advisors' chief credit analyst recently reported that tollunt Corporation's five-year bond

is currently yielding 7% and a comparable CdS contract has a credit spread of 4.25%. Since

libor is 2.5%, watt has recommended executing a basis trade to take advantage of the pricing

of tollunt's bonds and CdS. The basis trade would consist of purchasing both the bond and

the CdS contract.

according to watt's statement, the shape of uNab's credit curve is most likely:

A) flat.

B) upward-sloping.

C) downward-sloping.

Question

The following information relates to Questions

John Smith, a fixed-income portfolio manager at a €10 billion sovereign wealth fund

(Swf), meets with Sofia Chan, a derivatives strategist with Shire Gate Securities (SGS),

to discuss investment opportunities for the fund. Chan notes that SGS adheres to iSda

(international Swaps and derivatives association) protocols for credit default swap (CdS)

transactions and that any contract must conform to iSda specifications. before the

fund can engage in trading CdS products with SGS, the fund must satisfy compliance

requirements.

Smith explains to Chan that fixed-income derivatives strategies are being contemplated

for both hedging and trading purposes. Given the size and diversified nature of the fund,

Smith asks Chan to recommend a type of CdS that would allow the Swf to simultaneously

fully hedge multiple fixed-income exposures.

Next, Smith asks Chan to assess the impact on derivative products of recent events affect-

ing Maxx Corporation, a uS company. The Swf holds an unsecured debt instrument issued

by Maxx. Chan says she is very familiar with Maxx because many of its unsecured debt obliga-

tions are commonly included in broad baskets of bonds used for

hedging purposes. SGS recently sold €400 million of protection

on the on-the-run CdX high yield (hY) index that includes a

Maxx bond; the index contains 100 entities. Chan reports that

creditors met with company executives to impose a restructuring on Maxx bonds; as a result,

all outstanding principal obligations will be reduced by 30%.

Smith and Chan discuss opportunities to add trading profits to the Swf. Smith asks Chan

to determine the probability of default associated with a five-year investment-grade bond issued

by orion industrial. Selected data on the orion industrial bond are presented in exhibit 1.

eXhibit 1 Selected data on orion industrial five-Year bond

Chan explains that a single-name CdS can also be used to add profit to the fund over

time. Chan describes a hypothetical trade in which the fund sells £6 million of five-year CdS

protection on orion, where the CdS contract has a duration of 3.9 years. Chan assumes that

the fund closes the position six months later, after orion's credit spread narrowed from 150

bps to 100 bps.

Chan discusses the mechanics of a long/short trade. in order to structure a number of

potential trades, Chan and Smith exchange their respective views on individual companies and

global economies. Chan and Smith agree on the following outlooks.

Outlook 1: italy's economy will weaken.

Outlook 2: The uS economy will strengthen relative to that of Canada.

Outlook 3: The credit quality of electric car manufacturers will improve relative to that of

traditional car manufacturers.

Chan believes uS macroeconomic data are improving and that the general economy will

strengthen in the short term. Chan suggests that a curve trade could be used by the fund to

capitalize on her short-term view of a steepening of the uS credit curve.

another short-term trading opportunity that Smith and Chan discuss involves the merger

and acquisition market. SGS believes that delta Corporation may make an unsolicited bid at

a premium to the market price for all publicly traded shares of Zega, inc. Zega's market cap-

italization and capital structure are comparable to delta's; both firms are highly levered. it is

anticipated that delta will issue new equity along with 5- and 10-year senior unsecured debt

to fund the acquisition, which will significantly increase its debt ratio.

following the Maxx restructuring, the CdX hY notional will be closest to:

A) €396.0 million.

B) €398.8 million.

C) $400.0 million.

John Smith, a fixed-income portfolio manager at a €10 billion sovereign wealth fund

(Swf), meets with Sofia Chan, a derivatives strategist with Shire Gate Securities (SGS),

to discuss investment opportunities for the fund. Chan notes that SGS adheres to iSda

(international Swaps and derivatives association) protocols for credit default swap (CdS)

transactions and that any contract must conform to iSda specifications. before the

fund can engage in trading CdS products with SGS, the fund must satisfy compliance

requirements.

Smith explains to Chan that fixed-income derivatives strategies are being contemplated

for both hedging and trading purposes. Given the size and diversified nature of the fund,

Smith asks Chan to recommend a type of CdS that would allow the Swf to simultaneously

fully hedge multiple fixed-income exposures.

Next, Smith asks Chan to assess the impact on derivative products of recent events affect-

ing Maxx Corporation, a uS company. The Swf holds an unsecured debt instrument issued

by Maxx. Chan says she is very familiar with Maxx because many of its unsecured debt obliga-

tions are commonly included in broad baskets of bonds used for

hedging purposes. SGS recently sold €400 million of protection

on the on-the-run CdX high yield (hY) index that includes a

Maxx bond; the index contains 100 entities. Chan reports that

creditors met with company executives to impose a restructuring on Maxx bonds; as a result,

all outstanding principal obligations will be reduced by 30%.

Smith and Chan discuss opportunities to add trading profits to the Swf. Smith asks Chan

to determine the probability of default associated with a five-year investment-grade bond issued

by orion industrial. Selected data on the orion industrial bond are presented in exhibit 1.

eXhibit 1 Selected data on orion industrial five-Year bond

Chan explains that a single-name CdS can also be used to add profit to the fund over

time. Chan describes a hypothetical trade in which the fund sells £6 million of five-year CdS

protection on orion, where the CdS contract has a duration of 3.9 years. Chan assumes that

the fund closes the position six months later, after orion's credit spread narrowed from 150

bps to 100 bps.

Chan discusses the mechanics of a long/short trade. in order to structure a number of

potential trades, Chan and Smith exchange their respective views on individual companies and

global economies. Chan and Smith agree on the following outlooks.

Outlook 1: italy's economy will weaken.

Outlook 2: The uS economy will strengthen relative to that of Canada.

Outlook 3: The credit quality of electric car manufacturers will improve relative to that of

traditional car manufacturers.

Chan believes uS macroeconomic data are improving and that the general economy will

strengthen in the short term. Chan suggests that a curve trade could be used by the fund to

capitalize on her short-term view of a steepening of the uS credit curve.

another short-term trading opportunity that Smith and Chan discuss involves the merger

and acquisition market. SGS believes that delta Corporation may make an unsolicited bid at

a premium to the market price for all publicly traded shares of Zega, inc. Zega's market cap-

italization and capital structure are comparable to delta's; both firms are highly levered. it is

anticipated that delta will issue new equity along with 5- and 10-year senior unsecured debt

to fund the acquisition, which will significantly increase its debt ratio.

following the Maxx restructuring, the CdX hY notional will be closest to:

A) €396.0 million.

B) €398.8 million.

C) $400.0 million.

Question

The following information relates to Questions

John Smith, a fixed-income portfolio manager at a €10 billion sovereign wealth fund

(Swf), meets with Sofia Chan, a derivatives strategist with Shire Gate Securities (SGS),

to discuss investment opportunities for the fund. Chan notes that SGS adheres to iSda

(international Swaps and derivatives association) protocols for credit default swap (CdS)

transactions and that any contract must conform to iSda specifications. before the

fund can engage in trading CdS products with SGS, the fund must satisfy compliance

requirements.

Smith explains to Chan that fixed-income derivatives strategies are being contemplated

for both hedging and trading purposes. Given the size and diversified nature of the fund,

Smith asks Chan to recommend a type of CdS that would allow the Swf to simultaneously

fully hedge multiple fixed-income exposures.

Next, Smith asks Chan to assess the impact on derivative products of recent events affect-

ing Maxx Corporation, a uS company. The Swf holds an unsecured debt instrument issued

by Maxx. Chan says she is very familiar with Maxx because many of its unsecured debt obliga-

tions are commonly included in broad baskets of bonds used for

hedging purposes. SGS recently sold €400 million of protection

on the on-the-run CdX high yield (hY) index that includes a

Maxx bond; the index contains 100 entities. Chan reports that

creditors met with company executives to impose a restructuring on Maxx bonds; as a result,

all outstanding principal obligations will be reduced by 30%.

Smith and Chan discuss opportunities to add trading profits to the Swf. Smith asks Chan

to determine the probability of default associated with a five-year investment-grade bond issued

by orion industrial. Selected data on the orion industrial bond are presented in exhibit 1.

eXhibit 1 Selected data on orion industrial five-Year bond

Chan explains that a single-name CdS can also be used to add profit to the fund over

time. Chan describes a hypothetical trade in which the fund sells £6 million of five-year CdS

protection on orion, where the CdS contract has a duration of 3.9 years. Chan assumes that

the fund closes the position six months later, after orion's credit spread narrowed from 150

bps to 100 bps.

Chan discusses the mechanics of a long/short trade. in order to structure a number of

potential trades, Chan and Smith exchange their respective views on individual companies and

global economies. Chan and Smith agree on the following outlooks.

Outlook 1: italy's economy will weaken.

Outlook 2: The uS economy will strengthen relative to that of Canada.

Outlook 3: The credit quality of electric car manufacturers will improve relative to that of

traditional car manufacturers.

Chan believes uS macroeconomic data are improving and that the general economy will

strengthen in the short term. Chan suggests that a curve trade could be used by the fund to

capitalize on her short-term view of a steepening of the uS credit curve.

another short-term trading opportunity that Smith and Chan discuss involves the merger

and acquisition market. SGS believes that delta Corporation may make an unsolicited bid at

a premium to the market price for all publicly traded shares of Zega, inc. Zega's market cap-

italization and capital structure are comparable to delta's; both firms are highly levered. it is

anticipated that delta will issue new equity along with 5- and 10-year senior unsecured debt

to fund the acquisition, which will significantly increase its debt ratio.

to satisfy the compliance requirements referenced by Chan, the fund is most likely required to:

A) set a notional amount.

B) post an upfront payment.

C) sign an iSda master agreement.

John Smith, a fixed-income portfolio manager at a €10 billion sovereign wealth fund

(Swf), meets with Sofia Chan, a derivatives strategist with Shire Gate Securities (SGS),

to discuss investment opportunities for the fund. Chan notes that SGS adheres to iSda

(international Swaps and derivatives association) protocols for credit default swap (CdS)

transactions and that any contract must conform to iSda specifications. before the

fund can engage in trading CdS products with SGS, the fund must satisfy compliance

requirements.

Smith explains to Chan that fixed-income derivatives strategies are being contemplated

for both hedging and trading purposes. Given the size and diversified nature of the fund,

Smith asks Chan to recommend a type of CdS that would allow the Swf to simultaneously

fully hedge multiple fixed-income exposures.

Next, Smith asks Chan to assess the impact on derivative products of recent events affect-

ing Maxx Corporation, a uS company. The Swf holds an unsecured debt instrument issued

by Maxx. Chan says she is very familiar with Maxx because many of its unsecured debt obliga-

tions are commonly included in broad baskets of bonds used for

hedging purposes. SGS recently sold €400 million of protection

on the on-the-run CdX high yield (hY) index that includes a

Maxx bond; the index contains 100 entities. Chan reports that

creditors met with company executives to impose a restructuring on Maxx bonds; as a result,

all outstanding principal obligations will be reduced by 30%.

Smith and Chan discuss opportunities to add trading profits to the Swf. Smith asks Chan

to determine the probability of default associated with a five-year investment-grade bond issued

by orion industrial. Selected data on the orion industrial bond are presented in exhibit 1.

eXhibit 1 Selected data on orion industrial five-Year bond

Chan explains that a single-name CdS can also be used to add profit to the fund over

time. Chan describes a hypothetical trade in which the fund sells £6 million of five-year CdS

protection on orion, where the CdS contract has a duration of 3.9 years. Chan assumes that

the fund closes the position six months later, after orion's credit spread narrowed from 150

bps to 100 bps.

Chan discusses the mechanics of a long/short trade. in order to structure a number of

potential trades, Chan and Smith exchange their respective views on individual companies and

global economies. Chan and Smith agree on the following outlooks.

Outlook 1: italy's economy will weaken.

Outlook 2: The uS economy will strengthen relative to that of Canada.

Outlook 3: The credit quality of electric car manufacturers will improve relative to that of

traditional car manufacturers.

Chan believes uS macroeconomic data are improving and that the general economy will

strengthen in the short term. Chan suggests that a curve trade could be used by the fund to

capitalize on her short-term view of a steepening of the uS credit curve.

another short-term trading opportunity that Smith and Chan discuss involves the merger

and acquisition market. SGS believes that delta Corporation may make an unsolicited bid at

a premium to the market price for all publicly traded shares of Zega, inc. Zega's market cap-

italization and capital structure are comparable to delta's; both firms are highly levered. it is

anticipated that delta will issue new equity along with 5- and 10-year senior unsecured debt

to fund the acquisition, which will significantly increase its debt ratio.

to satisfy the compliance requirements referenced by Chan, the fund is most likely required to:

A) set a notional amount.

B) post an upfront payment.

C) sign an iSda master agreement.

Question

required and, if so, the amount of the premium. watt presents the information for the CdS in exhibit 1.

Morrison purchases the 10-year CdS on Kand Corporation debt. two months later the credit spread for Kand Corp. has increased by 200 basis points. Morrison asks watt

to close out the firm's CdS position on Kand Corporation by entering into new offsetting

contracts.

Tollunt Corporation

deem advisors' chief credit analyst recently reported that tollunt Corporation's five-year bond

is currently yielding 7% and a comparable CdS contract has a credit spread of 4.25%. Since

libor is 2.5%, watt has recommended executing a basis trade to take advantage of the pricing

of tollunt's bonds and CdS. The basis trade would consist of purchasing both the bond and

the CdS contract.

if uNab experienced a credit event on 1 July, watt should recommend that deem advisors:

A) prefer a cash settlement.

B) prefer a physical settlement.

C) be indifferent between a cash or a physical settlement.

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/15

Play

Full screen (f)

Deck 11: Credit Default Swaps

1

required and, if so, the amount of the premium. watt presents the information for the CdS in exhibit 1.

Morrison purchases the 10-year CdS on Kand Corporation debt. two months later the credit spread for Kand Corp. has increased by 200 basis points. Morrison asks watt

to close out the firm's CdS position on Kand Corporation by entering into new offsetting

contracts.

Tollunt Corporation

deem advisors' chief credit analyst recently reported that tollunt Corporation's five-year bond

is currently yielding 7% and a comparable CdS contract has a credit spread of 4.25%. Since

libor is 2.5%, watt has recommended executing a basis trade to take advantage of the pricing

of tollunt's bonds and CdS. The basis trade would consist of purchasing both the bond and

the CdS contract.

if deem advisors enters into a new offsetting contract two months after purchasing the CdS protection on Kand Corporation, this action will most likely result in:

A) a loss on the CdS position.

B) a gain on the CdS position.