Deck 3: Unit 21-32

Full screen (f)

Question

Question

Question

Bludger Ltd's auditors were appointed after the end of the financial year and discovered that the company had also changed banks shortly after the year end. The directors refused permission for the auditors to contact the previous bankers for confirmation of the year end bank balance without giving any good reason. The total of net current assets was £1.2m of which the bank balance amounted to £123,000 overdrawn.

Which of the following options should the auditors take when considering their audit report?

Which of the following options should the auditors take when considering their audit report?

Question

Question

Question

Question

Question

Question

Bludger Ltd's auditors were appointed after the end of the financial year and discovered that the company had also changed banks shortly after the year end. The directors refused permission for the auditors to contact the previous bankers for confirmation of the year end bank balance without giving any good reason. The total of net current assets was £1.2m of which the bank balance amounted to £123,000 overdrawn.

Which of the following options should the auditors take when considering their audit report?

Which of the following options should the auditors take when considering their audit report?

Question

Question

Question

Question

Question

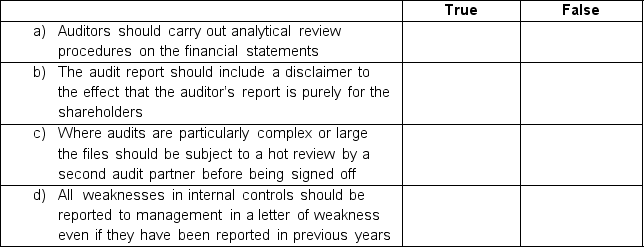

An external auditor is required to carry out a final review to ensure their conclusions are supported by sufficient reliable evidence

Select whether each of the statements below is true or false in connection with the final audit review

a) Auditors should carry out analytical review procedures on the financial statements

b) The audit report should include a disclaimer to the effect that the auditor's report is purely for the shareholders

c) Where audits are particularly complex or large the files should be subject to a hot review by a second audit partner before being signed off

d) All weaknesses in internal controls should be reported to management in a letter of weakness even if they have been reported in previous years

Select whether each of the statements below is true or false in connection with the final audit review

a) Auditors should carry out analytical review procedures on the financial statements

b) The audit report should include a disclaimer to the effect that the auditor's report is purely for the shareholders

c) Where audits are particularly complex or large the files should be subject to a hot review by a second audit partner before being signed off

d) All weaknesses in internal controls should be reported to management in a letter of weakness even if they have been reported in previous years

Question

Question

Question

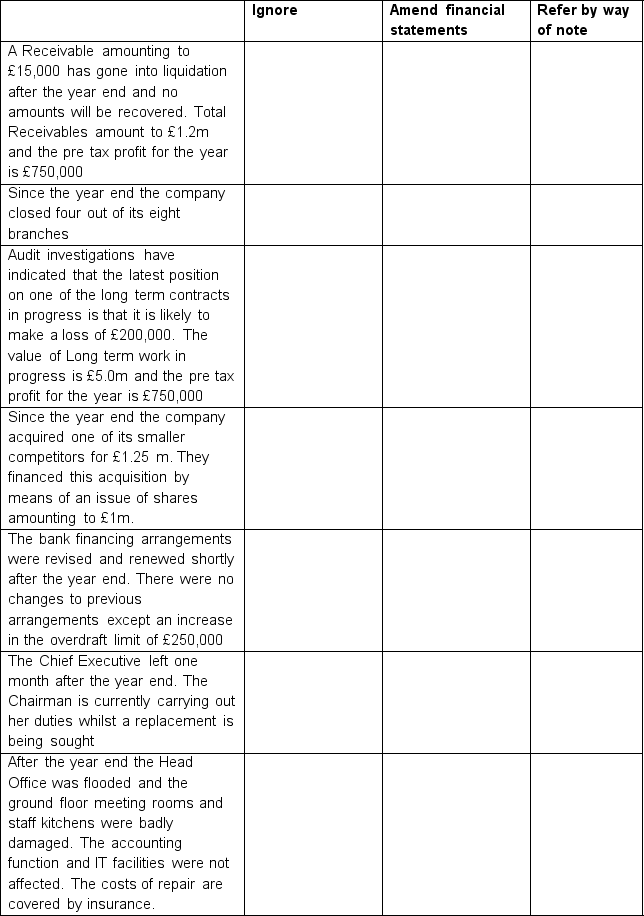

You are reviewing the audit files of Monty Ltd with a view to finalising the audit. From your review of the files you identify the following factors. Identify whether or not they can be

a) Ignored

b) Whether the financial statements might have to be amended

c) Whether or not the financial statements should include a reference by way of a note without any adjustment to the figures

In the table below tick the response you feel is the most appropriate

a) Ignored

b) Whether the financial statements might have to be amended

c) Whether or not the financial statements should include a reference by way of a note without any adjustment to the figures

In the table below tick the response you feel is the most appropriate

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/30

Play

Full screen (f)

Deck 3: Unit 21-32

1

To which of the following stakeholders do the auditors of Tesco plc have a legal as opposed to a moral responsibility

A) The bank

B) The employees

C) HM Revenue and Customs

D) People intending to buy shares in the company

E) A supplier of goods to Tesco plc

F) The shareholders

G) The government of the United Kingdom

H) The council of the Stock Exchange

A) The bank

B) The employees

C) HM Revenue and Customs

D) People intending to buy shares in the company

E) A supplier of goods to Tesco plc

F) The shareholders

G) The government of the United Kingdom

H) The council of the Stock Exchange

F

2

Give three examples of where auditors' routine audit procedures involve periods after the year end date, excluding consideration of post balance sheet events.

-reviewing payments of receivables balances after the year end.

-tracing uncleared cheques and uncredited lodgements from the bank reconciliation.

-carrying out audit work on the client's cut-off procedures.

-tracing uncleared cheques and uncredited lodgements from the bank reconciliation.

-carrying out audit work on the client's cut-off procedures.

3

Bludger Ltd's auditors were appointed after the end of the financial year and discovered that the company had also changed banks shortly after the year end. The directors refused permission for the auditors to contact the previous bankers for confirmation of the year end bank balance without giving any good reason. The total of net current assets was £1.2m of which the bank balance amounted to £123,000 overdrawn.

Which of the following options should the auditors take when considering their audit report?

Which of the following options should the auditors take when considering their audit report?

The report should be as clear and informative as possible to assist the shareholders in understanding the reasons for the qualification and its effects.

Wherever possible it should quantify the effect of the matter being qualified upon the financial statements.

Matters of significance which have arisen during the audit can be referred to in the 'Key Audit Matters section of the audit report. However in this case the refusal of the directors to allow the auditors to contact the bank is far too significant to be ignored or simply mentioned in passing so will result in a modified audit report.

In this case, assuming this is the only issue, there is no disagreement so the 'Except for' material disagreement and the Adverse opinion options aren't available to the auditor. Consequently this is a limitation of scope qualification.

The bank letter is used for more than simply verifying the bank balance - it is also used to request additional information from the bank regarding such matters as security for borrowings, overdraft limits, other bank accounts etc.

The auditors should be able to satisfy themselves as to the bank balance from other sources - principally a bank statement - so validating the Statement of Financial Position isn't a huge problem -even if the bank balance is material at 10% of net current assets - the problem for the auditors is what is not disclosed.

Accordingly the audit report will have to be modified for an 'except for' limitation of scope with a full explanation of the effect of the modification on the financial statements and the reasons for modifying the report.

Wherever possible it should quantify the effect of the matter being qualified upon the financial statements.

Matters of significance which have arisen during the audit can be referred to in the 'Key Audit Matters section of the audit report. However in this case the refusal of the directors to allow the auditors to contact the bank is far too significant to be ignored or simply mentioned in passing so will result in a modified audit report.

In this case, assuming this is the only issue, there is no disagreement so the 'Except for' material disagreement and the Adverse opinion options aren't available to the auditor. Consequently this is a limitation of scope qualification.

The bank letter is used for more than simply verifying the bank balance - it is also used to request additional information from the bank regarding such matters as security for borrowings, overdraft limits, other bank accounts etc.

The auditors should be able to satisfy themselves as to the bank balance from other sources - principally a bank statement - so validating the Statement of Financial Position isn't a huge problem -even if the bank balance is material at 10% of net current assets - the problem for the auditors is what is not disclosed.

Accordingly the audit report will have to be modified for an 'except for' limitation of scope with a full explanation of the effect of the modification on the financial statements and the reasons for modifying the report.

4

Use the information in the following paragraphs to answer questions three and four

You are the auditor of Whizzipop plc a manufacturer of soft drinks. The draft consolidated

financial statements for the year ended 30 September 2X18 show revenue of $125 million (2X17 - $114 million), profit before taxation of $12.4 million (2X17 - $10.9 million) and total assets of $110 million (2X17 - $93 million).

It has several subsidiaries, some of which are audited by firms other than yours. The financial statements of one such subsidiary company, Twizzle, for the year ended 30 September 2X18, are audited by another firm. Profit before taxation of $0.4 million and total assets of $34.1 million have been included in the draft consolidated financial statements of Whizzipop. The notes to Twizzle's financial statements as at 30 September 2X18 disclose a contingent liability for a pending legal matter estimated at $0.2 million. In November 2X18, the courts found Twizzle to be liable for costs and damages amounting to $1.1 million. However, Twizzle's directors have refused to make a provision, for any amount, as they have lodged an appeal against the judgement.

What evidence would you expect to see in respect of this liability?

You are the auditor of Whizzipop plc a manufacturer of soft drinks. The draft consolidated

financial statements for the year ended 30 September 2X18 show revenue of $125 million (2X17 - $114 million), profit before taxation of $12.4 million (2X17 - $10.9 million) and total assets of $110 million (2X17 - $93 million).

It has several subsidiaries, some of which are audited by firms other than yours. The financial statements of one such subsidiary company, Twizzle, for the year ended 30 September 2X18, are audited by another firm. Profit before taxation of $0.4 million and total assets of $34.1 million have been included in the draft consolidated financial statements of Whizzipop. The notes to Twizzle's financial statements as at 30 September 2X18 disclose a contingent liability for a pending legal matter estimated at $0.2 million. In November 2X18, the courts found Twizzle to be liable for costs and damages amounting to $1.1 million. However, Twizzle's directors have refused to make a provision, for any amount, as they have lodged an appeal against the judgement.

What evidence would you expect to see in respect of this liability?

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

5

Management representations are a source of audit evidence. These representations may be oral or written, and may be obtained either on an informal or formal basis. The auditors will include information obtained in this manner in their audit working papers where it forms part of the total audit evidence.

Discuss the implications for the auditor of a small company, if the directors refuse to sign the

Letter of Representation.

Discuss the implications for the auditor of a small company, if the directors refuse to sign the

Letter of Representation.

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

6

Explain in not more than 500 words why the auditors would not consider a hurricane landing on the main office building and totally destroying it after the year end to be a non adjusting event?

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

7

Chugalug Ltd has three subsidiary companies and is engaged in a joint venture with an Italian company called Intervole. It has an agreement with one of its major suppliers whereby they share information so they can arrange for materials deliveries on a 'just-in-time' basis.

The wife of the managing director , who runs her own furnishings business, won a tender to supply and fit tables and chairs to the conference area in the head office. Chugalug is also part of a business consortium which shares good practice and lobbies the local Member of Parliament to make representations to the government on their behalf. This is operated through the local Chamber of Commerce. Chugalug owns shares in a rival company, Gluggit plc which it shows as an investment in its Statement of Financial position.

a) What is meant by a 'related party'

b) Which of the involvements of Chugalug shown above a not involvements with related party

The wife of the managing director , who runs her own furnishings business, won a tender to supply and fit tables and chairs to the conference area in the head office. Chugalug is also part of a business consortium which shares good practice and lobbies the local Member of Parliament to make representations to the government on their behalf. This is operated through the local Chamber of Commerce. Chugalug owns shares in a rival company, Gluggit plc which it shows as an investment in its Statement of Financial position.

a) What is meant by a 'related party'

b) Which of the involvements of Chugalug shown above a not involvements with related party

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

8

List the basic assumptions under which an entity would be considered to be a going concern

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

9

Bludger Ltd's auditors were appointed after the end of the financial year and discovered that the company had also changed banks shortly after the year end. The directors refused permission for the auditors to contact the previous bankers for confirmation of the year end bank balance without giving any good reason. The total of net current assets was £1.2m of which the bank balance amounted to £123,000 overdrawn.

Which of the following options should the auditors take when considering their audit report?

Which of the following options should the auditors take when considering their audit report?

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

10

At the completion stage of an audit there are a number of final review procedures which must be carried out prior to signing the audit report. In not more than 500 words explain these procedures and the reasons for them.

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

11

Use the information in the following paragraphs to answer questions three and four

You are the auditor of Whizzipop plc a manufacturer of soft drinks. The draft consolidated

financial statements for the year ended 30 September 2X18 show revenue of $125 million (2X17 - $114 million), profit before taxation of $12.4 million (2X17 - $10.9 million) and total assets of $110 million (2X17 - $93 million).

It has several subsidiaries, some of which are audited by firms other than yours. The financial statements of one such subsidiary company, Twizzle, for the year ended 30 September 2X18, are audited by another firm. Profit before taxation of $0.4 million and total assets of $34.1 million have been included in the draft consolidated financial statements of Whizzipop. The notes to Twizzle's financial statements as at 30 September 2X18 disclose a contingent liability for a pending legal matter estimated at $0.2 million. In November 2X18, the courts found Twizzle to be liable for costs and damages amounting to $1.1 million. However, Twizzle's directors have refused to make a provision, for any amount, as they have lodged an appeal against the judgement.

What action would you, as group auditor, take in respect of this liability?

You are the auditor of Whizzipop plc a manufacturer of soft drinks. The draft consolidated

financial statements for the year ended 30 September 2X18 show revenue of $125 million (2X17 - $114 million), profit before taxation of $12.4 million (2X17 - $10.9 million) and total assets of $110 million (2X17 - $93 million).

It has several subsidiaries, some of which are audited by firms other than yours. The financial statements of one such subsidiary company, Twizzle, for the year ended 30 September 2X18, are audited by another firm. Profit before taxation of $0.4 million and total assets of $34.1 million have been included in the draft consolidated financial statements of Whizzipop. The notes to Twizzle's financial statements as at 30 September 2X18 disclose a contingent liability for a pending legal matter estimated at $0.2 million. In November 2X18, the courts found Twizzle to be liable for costs and damages amounting to $1.1 million. However, Twizzle's directors have refused to make a provision, for any amount, as they have lodged an appeal against the judgement.

What action would you, as group auditor, take in respect of this liability?

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

12

List three advantages and three disadvantages to firms' outsourcing

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

13

Decide whether or not these statements are true or false

a. Auditors owe a duty of care to potential investors in their client

b. Auditors may reduce the consequences of a negligence claim against them by operating as a limited liability partnership

c. In order to prove a successful claim for negligence the client only has to suffer a loss which is the fault of the auditors

a. Auditors owe a duty of care to potential investors in their client

b. Auditors may reduce the consequences of a negligence claim against them by operating as a limited liability partnership

c. In order to prove a successful claim for negligence the client only has to suffer a loss which is the fault of the auditors

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

14

An external auditor is required to carry out a final review to ensure their conclusions are supported by sufficient reliable evidence

Select whether each of the statements below is true or false in connection with the final audit review

a) Auditors should carry out analytical review procedures on the financial statements

b) The audit report should include a disclaimer to the effect that the auditor's report is purely for the shareholders

c) Where audits are particularly complex or large the files should be subject to a hot review by a second audit partner before being signed off

d) All weaknesses in internal controls should be reported to management in a letter of weakness even if they have been reported in previous years

Select whether each of the statements below is true or false in connection with the final audit review

a) Auditors should carry out analytical review procedures on the financial statements

b) The audit report should include a disclaimer to the effect that the auditor's report is purely for the shareholders

c) Where audits are particularly complex or large the files should be subject to a hot review by a second audit partner before being signed off

d) All weaknesses in internal controls should be reported to management in a letter of weakness even if they have been reported in previous years

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

15

Discuss the difference between a review engagement and a statutory year-end audit.

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

16

The audit of your client Sprightly plc revealed a major control weakness in the management of investments. The company recently recruited a financial analyst, as an employee, to manage the investment of surplus funds. Company policy is to invest in the shares of large quoted companies. The audit discovered a number of situations where the financial analyst had made substantial profits for the company by speculating in risky investments such as derivatives. Such investments could result in massive losses. The matter was reported in writing to the chief financial officer four months ago but no action has yet been taken.

What action should the auditors take in respect of this discovery?

What action should the auditors take in respect of this discovery?

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

17

You are reviewing the audit files of Monty Ltd with a view to finalising the audit. From your review of the files you identify the following factors. Identify whether or not they can be

a) Ignored

b) Whether the financial statements might have to be amended

c) Whether or not the financial statements should include a reference by way of a note without any adjustment to the figures

In the table below tick the response you feel is the most appropriate

a) Ignored

b) Whether the financial statements might have to be amended

c) Whether or not the financial statements should include a reference by way of a note without any adjustment to the figures

In the table below tick the response you feel is the most appropriate

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

18

In order to prove a successful claim for negligence against an audit firm there has to be a duty of care which was breached by the audit firm with the result that a loss was incurred. Auditors Woody & Co were amazed to receive a negligence claim from one of their client's bankers Gurney plc who had lent money to their client, Megabuild, after the year end and subsequently lost their money when a construction project Megabuild had been involved in went badly wrong and bankrupted them. The claim said that the auditors had significantly failed to estimate the losses on the project with the result that the bank, had they known the true position, would not have lent money to Megabuild.

Gurney plc is claiming its losses from Woody & Co. What advice would you give to Woody & Co in this situation?

Gurney plc is claiming its losses from Woody & Co. What advice would you give to Woody & Co in this situation?

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

19

State whether each of these statements are true or false

a. Auditors have no responsibility for validating comparative figures providing the audit report for the previous financial period has not been modified

b. Auditors must check that the opening balances have been brought forward correctly into the new accounting period

c. Where the financial statements for the previous accounting period were audited by another firm the incoming auditors must get confirmation from the outgoing auditors that their auditor's report is unchanged

a. Auditors have no responsibility for validating comparative figures providing the audit report for the previous financial period has not been modified

b. Auditors must check that the opening balances have been brought forward correctly into the new accounting period

c. Where the financial statements for the previous accounting period were audited by another firm the incoming auditors must get confirmation from the outgoing auditors that their auditor's report is unchanged

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

20

You are an audit manager with Spottit & Hope. One of your clients, Bolington Limited, has recently asked your firm to perform a limited review of the financial statements.

During your review, you discovered a cash payment of $50,000. You have asked the company for details of this payment, and the directors have told you that it was an agency

fee, and they cannot tell you any more details as the company would lose its competitive

advantage. Profit before tax is $2m.

Your audit supervisor is happy with this explanation, and has proposed a draft review

report with the following opinion paragraph:

'Based on our review nothing has come to our attention which indicates that the financial

statements do not give a true and fair view'.

Discuss the validity or otherwise of the suggested opinion, and discuss the appropriateness of alternative opinions and suggest suitable wording for the opinion you consider to be most appropriate.

During your review, you discovered a cash payment of $50,000. You have asked the company for details of this payment, and the directors have told you that it was an agency

fee, and they cannot tell you any more details as the company would lose its competitive

advantage. Profit before tax is $2m.

Your audit supervisor is happy with this explanation, and has proposed a draft review

report with the following opinion paragraph:

'Based on our review nothing has come to our attention which indicates that the financial

statements do not give a true and fair view'.

Discuss the validity or otherwise of the suggested opinion, and discuss the appropriateness of alternative opinions and suggest suitable wording for the opinion you consider to be most appropriate.

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

21

The Chairman's Report of Pudding plc states that investment property rental forms a major part of revenue. However, a note to the financial statements shows that property rental represents only 1·6% of total revenue for the year. The audit senior is satisfied that the revenue figures are correct. The audit senior has noted that an unmodified audit report should be given as the audit opinion does not extend to the other reports.

Is the audit senior correct?

Is the audit senior correct?

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

22

Use the information in the following paragraph to answer questions 22 and 23

You are a member of the audit team for the audit of Learnersinnit plc, a private provider of high quality educational services. The team have just completed the interim audit for the current year. You performed the work on the salaries system where you have noted the following issues:

The company currently has over three hundred teaching and office staff, organised into several different departments. The staff are paid on a fixed scale with annual increments agreed by the board. The Salaries Department prepares one month's payroll from the names on the previous payroll, adding or deleting names as instructed by the personnel department. Details of increased pay rates resulting from promotion are also supplied by the Personnel Department. Sometimes, however, the Personnel Department is so busy that they forget to telephone the Salaries Department with details of staff changes or promotions. To correct these oversights, there is sometimes an extra payroll run to prepare additional payments where necessary.

The payroll is prepared by either of the two Salaries Department staff, depending on whoever is available. The payroll calculations are usually checked for accuracy by the other employee in the department, unless one of them is absent through illness or is on holiday.

The Personnel Department manager corrects any payroll errors identified on her own computer, which is part of the same computer network, and then signs the payroll electronically to indicate overall approval. She does not have time to authorise any additional runs which are necessary, however, as these are usually required urgently.

Payments are made to staff by credit transfer directly to their bank accounts. Payments to statutory authorities, pension funds etc of the amounts deducted from employees plus the employers contributions are also paid by credit transfer within the required timescales.

Draft a formal Management Letter (or Letter of Weaknesses) in respect of the internal control systems of Learnersinnit plc, as outlined above. The structure of the letter should be as follows:

Body of management letter:

-Identification of weaknesses in the existing internal control system

-Potential implications of these weaknesses

-Recommendations for improvement

You are a member of the audit team for the audit of Learnersinnit plc, a private provider of high quality educational services. The team have just completed the interim audit for the current year. You performed the work on the salaries system where you have noted the following issues:

The company currently has over three hundred teaching and office staff, organised into several different departments. The staff are paid on a fixed scale with annual increments agreed by the board. The Salaries Department prepares one month's payroll from the names on the previous payroll, adding or deleting names as instructed by the personnel department. Details of increased pay rates resulting from promotion are also supplied by the Personnel Department. Sometimes, however, the Personnel Department is so busy that they forget to telephone the Salaries Department with details of staff changes or promotions. To correct these oversights, there is sometimes an extra payroll run to prepare additional payments where necessary.

The payroll is prepared by either of the two Salaries Department staff, depending on whoever is available. The payroll calculations are usually checked for accuracy by the other employee in the department, unless one of them is absent through illness or is on holiday.

The Personnel Department manager corrects any payroll errors identified on her own computer, which is part of the same computer network, and then signs the payroll electronically to indicate overall approval. She does not have time to authorise any additional runs which are necessary, however, as these are usually required urgently.

Payments are made to staff by credit transfer directly to their bank accounts. Payments to statutory authorities, pension funds etc of the amounts deducted from employees plus the employers contributions are also paid by credit transfer within the required timescales.

Draft a formal Management Letter (or Letter of Weaknesses) in respect of the internal control systems of Learnersinnit plc, as outlined above. The structure of the letter should be as follows:

Body of management letter:

-Identification of weaknesses in the existing internal control system

-Potential implications of these weaknesses

-Recommendations for improvement

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

23

State whether the following are true or false

Emphasis of matter reports are not a modification of opinion but merely draw attention to some disclosure in the financial statements

Negative assurance is given in all non audit engagements

Failure of auditors to obtain sufficient, appropriate evidence will result in an adverse audit opinion

Compilation assignments require no audit opinion at all

Emphasis of matter reports are not a modification of opinion but merely draw attention to some disclosure in the financial statements

Negative assurance is given in all non audit engagements

Failure of auditors to obtain sufficient, appropriate evidence will result in an adverse audit opinion

Compilation assignments require no audit opinion at all

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

24

The audit of Bouncy Co is nearly complete and the financial statements and the audit report are due to be signed next week. However, the following additional information has just been presented to the auditor. The company's yearend was 30 September 2X17.

The springs in a new type of mattress have been found to be defective making the mattress unsafe for use. There have been no sales of this mattress; it was due to be marketed in the next few weeks. The company's insurers estimate that inventory to the value of R1,750,000 has been affected. The insurers also estimate that the mattresses are now only worth R1,225,000. No claim can be made against the supplier of springs as this company is in liquidation with no prospect of any amounts being paid to third parties. The insurers will not pay Bouncy for the fall in value of the inventory as the company was underinsured. All of this inventory was in the finished goods store at the end of the year and no movements of inventory have been recorded post year-end.

What actions should the auditors take and what will be the effect on the accounts for the year ended 30 September 2X17?

The springs in a new type of mattress have been found to be defective making the mattress unsafe for use. There have been no sales of this mattress; it was due to be marketed in the next few weeks. The company's insurers estimate that inventory to the value of R1,750,000 has been affected. The insurers also estimate that the mattresses are now only worth R1,225,000. No claim can be made against the supplier of springs as this company is in liquidation with no prospect of any amounts being paid to third parties. The insurers will not pay Bouncy for the fall in value of the inventory as the company was underinsured. All of this inventory was in the finished goods store at the end of the year and no movements of inventory have been recorded post year-end.

What actions should the auditors take and what will be the effect on the accounts for the year ended 30 September 2X17?

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

25

State whether the following are true or false

The purpose of a management letter is to provide good audit evidence about the state of the company's finances

A significant deficiency in internal control is one which must be reported to the management or those charged with governance

A Type 2 report is useful when evaluating service providers where a company has outsourced services but it is does not replace independent audit evidence

Auditors may rely on representations made by the directors in identifying related parties as they are often very difficult to identify

The purpose of a management letter is to provide good audit evidence about the state of the company's finances

A significant deficiency in internal control is one which must be reported to the management or those charged with governance

A Type 2 report is useful when evaluating service providers where a company has outsourced services but it is does not replace independent audit evidence

Auditors may rely on representations made by the directors in identifying related parties as they are often very difficult to identify

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

26

Use the information in the following paragraph to answer questions 22 and 23

You are a member of the audit team for the audit of Learnersinnit plc, a private provider of high quality educational services. The team have just completed the interim audit for the current year. You performed the work on the salaries system where you have noted the following issues:

The company currently has over three hundred teaching and office staff, organised into several different departments. The staff are paid on a fixed scale with annual increments agreed by the board. The Salaries Department prepares one month's payroll from the names on the previous payroll, adding or deleting names as instructed by the personnel department. Details of increased pay rates resulting from promotion are also supplied by the Personnel Department. Sometimes, however, the Personnel Department is so busy that they forget to telephone the Salaries Department with details of staff changes or promotions. To correct these oversights, there is sometimes an extra payroll run to prepare additional payments where necessary.

The payroll is prepared by either of the two Salaries Department staff, depending on whoever is available. The payroll calculations are usually checked for accuracy by the other employee in the department, unless one of them is absent through illness or is on holiday.

The Personnel Department manager corrects any payroll errors identified on her own computer, which is part of the same computer network, and then signs the payroll electronically to indicate overall approval. She does not have time to authorise any additional runs which are necessary, however, as these are usually required urgently.

Payments are made to staff by credit transfer directly to their bank accounts. Payments to statutory authorities, pension funds etc of the amounts deducted from employees plus the employers contributions are also paid by credit transfer within the required timescales.

Describe TWO different ways in which fraud could be carried out in the above salaries system.

You are a member of the audit team for the audit of Learnersinnit plc, a private provider of high quality educational services. The team have just completed the interim audit for the current year. You performed the work on the salaries system where you have noted the following issues:

The company currently has over three hundred teaching and office staff, organised into several different departments. The staff are paid on a fixed scale with annual increments agreed by the board. The Salaries Department prepares one month's payroll from the names on the previous payroll, adding or deleting names as instructed by the personnel department. Details of increased pay rates resulting from promotion are also supplied by the Personnel Department. Sometimes, however, the Personnel Department is so busy that they forget to telephone the Salaries Department with details of staff changes or promotions. To correct these oversights, there is sometimes an extra payroll run to prepare additional payments where necessary.

The payroll is prepared by either of the two Salaries Department staff, depending on whoever is available. The payroll calculations are usually checked for accuracy by the other employee in the department, unless one of them is absent through illness or is on holiday.

The Personnel Department manager corrects any payroll errors identified on her own computer, which is part of the same computer network, and then signs the payroll electronically to indicate overall approval. She does not have time to authorise any additional runs which are necessary, however, as these are usually required urgently.

Payments are made to staff by credit transfer directly to their bank accounts. Payments to statutory authorities, pension funds etc of the amounts deducted from employees plus the employers contributions are also paid by credit transfer within the required timescales.

Describe TWO different ways in which fraud could be carried out in the above salaries system.

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

27

The audit team at Harmonium Ltd, a manufacturer of toys and games, have noted several points which they have brought to the attention of you, the audit partner. These include

-Harmonium's product range hasn't changed in five years and newer products are appearing in the market in direct competition

-The management of Harmonium have not replaced their Head of Marketing who has left the company to join a competitor

-The bank has refused to increase Harmonium's overdraft and turned down an application for as loan for new equipment

-Orders from two key customers have declined steadily over the year and turnover volume is dropping. The directors point out that revenues are equivalent to those of the previous year but the auditors point out that this is due to price rises not to volumes of goods sold

-The audit team reviewed the future budgets and cash flows of Harmonium prepared by the directors and stated that, whilst some of the assumptions were optimistic the projections were not completely unreasonable

There are no other points which give any indication that the financial statements are incorrectly stated and the audit process was satisfactory.

You have to decide whether any of these issues affect your audit opinion for the year and which course of action is the most appropriate

a) The company is likely to be in trouble so issue a qualified auditors' report on the financial statements on the basis that it is not a going concern

b) None of these points are of significance to the financial report for the current year and it is not for the auditors to tell the directors what to do so no action is required

c) None of these points are of significance to the financial report for the current financial year. However they indicate a worrying trend which it might be appropriate to discuss with the directors after the audit is finalised.

d) The audit team should go back to the company and try to discover further evidence that the company is not a going concern so the audit report can be modified

-Harmonium's product range hasn't changed in five years and newer products are appearing in the market in direct competition

-The management of Harmonium have not replaced their Head of Marketing who has left the company to join a competitor

-The bank has refused to increase Harmonium's overdraft and turned down an application for as loan for new equipment

-Orders from two key customers have declined steadily over the year and turnover volume is dropping. The directors point out that revenues are equivalent to those of the previous year but the auditors point out that this is due to price rises not to volumes of goods sold

-The audit team reviewed the future budgets and cash flows of Harmonium prepared by the directors and stated that, whilst some of the assumptions were optimistic the projections were not completely unreasonable

There are no other points which give any indication that the financial statements are incorrectly stated and the audit process was satisfactory.

You have to decide whether any of these issues affect your audit opinion for the year and which course of action is the most appropriate

a) The company is likely to be in trouble so issue a qualified auditors' report on the financial statements on the basis that it is not a going concern

b) None of these points are of significance to the financial report for the current year and it is not for the auditors to tell the directors what to do so no action is required

c) None of these points are of significance to the financial report for the current financial year. However they indicate a worrying trend which it might be appropriate to discuss with the directors after the audit is finalised.

d) The audit team should go back to the company and try to discover further evidence that the company is not a going concern so the audit report can be modified

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

28

The auditing profession is facing unique technical challenges. These can be summarised briefly as:

-The rise of Internet based retailers and service providers with diversified international operations.

-The siting of key aspects of Internet based retailing operations in low tax jurisdictions using transfer pricing to move funds out of high tax areas into low tax jurisdictions or by carrying out actual trade in one country and invoicing from another, low tax, one - thus claiming that they are actually trading from the low tax jurisdiction even though all they have there is an office and computer invoicing system.

-The increasing use of blockchain and cryptocurrencies, principally Bitcoin.

-The question of going concern relating to high technology businesses developing specialised software applications.

Required:

a) How are these types of development likely to affect the auditing profession of the future?

b) How will this affect the skills required of individual auditors?

-The rise of Internet based retailers and service providers with diversified international operations.

-The siting of key aspects of Internet based retailing operations in low tax jurisdictions using transfer pricing to move funds out of high tax areas into low tax jurisdictions or by carrying out actual trade in one country and invoicing from another, low tax, one - thus claiming that they are actually trading from the low tax jurisdiction even though all they have there is an office and computer invoicing system.

-The increasing use of blockchain and cryptocurrencies, principally Bitcoin.

-The question of going concern relating to high technology businesses developing specialised software applications.

Required:

a) How are these types of development likely to affect the auditing profession of the future?

b) How will this affect the skills required of individual auditors?

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

29

Sniffit & Koff plc is an established pharmaceutical company that has for many years generated 90% of its revenue through the sale of two specific cold and flu remedies. Sniffit & Koff plc has lately seen a real growth in the level of competition that it faces in its market and demand for its products has significantly declined. To make matters worse, in the past the company has not invested sufficiently in new product development and so has been trying to remedy this by recruiting suitably trained scientific staff, but this has proved more difficult than anticipated.

In addition to recruiting staff the company also needed to invest R12m in plant and machinery. The company wanted to borrow this sum but was unable to agree suitable terms with the bank; therefore it used its overdraft facility, which carried a higher interest rate.

Consequently, some of Sniffit & Koff's suppliers have been paid much later than usual and

hence some of them have withdrawn credit terms meaning the company must pay cash on delivery. As a result of the above the company's overdraft balance has grown substantially.

The directors have produced a cash flow forecast and this shows a significantly worsening position over the coming 12 months.

The directors have informed you that the bank overdraft facility is due for renewal next month, but they are confident that it will be renewed. They also strongly believe that the new products which are being developed will be ready to market soon and hence trading levels will improve and therefore that the company is a going concern. Therefore they do not intend to make any disclosures in the accounts regarding going concern.

Identify any potential indicators that the company is not a going concern and outline the procedures the auditors should carry out in this situation.

In addition to recruiting staff the company also needed to invest R12m in plant and machinery. The company wanted to borrow this sum but was unable to agree suitable terms with the bank; therefore it used its overdraft facility, which carried a higher interest rate.

Consequently, some of Sniffit & Koff's suppliers have been paid much later than usual and

hence some of them have withdrawn credit terms meaning the company must pay cash on delivery. As a result of the above the company's overdraft balance has grown substantially.

The directors have produced a cash flow forecast and this shows a significantly worsening position over the coming 12 months.

The directors have informed you that the bank overdraft facility is due for renewal next month, but they are confident that it will be renewed. They also strongly believe that the new products which are being developed will be ready to market soon and hence trading levels will improve and therefore that the company is a going concern. Therefore they do not intend to make any disclosures in the accounts regarding going concern.

Identify any potential indicators that the company is not a going concern and outline the procedures the auditors should carry out in this situation.

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

30

Demand for increased regulation of the audit profession has come from audit firms themselves, particularly medium sized firms that find it difficult to secure audit contracts for public limited companies (PLCs) given the predominance of the 'Big Four' firms. One medium sized firm has written to the House of Lords inquiry asking for a cap on the number of big audit contracts any one firm can have.

Set out in not more than 500 words the effect of increased regulation to compel Big 4 audit firms to give up large multinational audits.

Set out in not more than 500 words the effect of increased regulation to compel Big 4 audit firms to give up large multinational audits.

Unlock Deck

Unlock for access to all 30 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 30 flashcards in this deck.