Deck 19: Bank Management

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

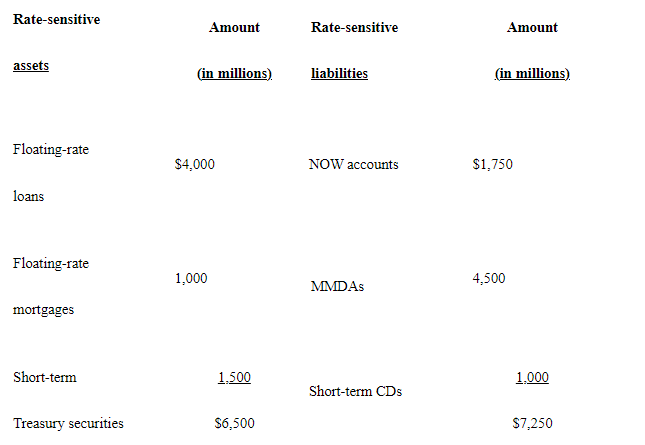

A bank has the following asset and liability portfolios. What is the gap?

A)$750 million

B)- $750 million

C)1.12

D).896

E)None of these are correct.

A)$750 million

B)- $750 million

C)1.12

D).896

E)None of these are correct.

Question

Question

Question

Question

ROE is defined as

A)

B)

C)

D)

A)

B)

C)

D)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/75

Play

Full screen (f)

Deck 19: Bank Management

1

Which of the following statements is NOT correct?

A)Managers may be tempted to make decisions that are in their own best interests rather than shareholder interests.

B)Directors of a bank determine whether loan applications should be approved.

C)To prevent agency problems, some banks provide stock as compensation to managers.

D)The underlying goal behind the managerial policies of a bank is to maximize the wealth of the bank's shareholders

A)Managers may be tempted to make decisions that are in their own best interests rather than shareholder interests.

B)Directors of a bank determine whether loan applications should be approved.

C)To prevent agency problems, some banks provide stock as compensation to managers.

D)The underlying goal behind the managerial policies of a bank is to maximize the wealth of the bank's shareholders

B

2

As the secondary market for loans has become active, banks can attempt to satisfy their liquidity needs with a ____ proportion of loans while achieving ____ profitability.

A)higher; higher

B)lower; lower

C)higher; lower

D)lower; higher

A)higher; higher

B)lower; lower

C)higher; lower

D)lower; higher

A

3

Which of the following is NOT a likely method used by a bank to reduce interest rate risk?

A)maturity matching

B)using fixed-rate loans

C)using interest rate futures contracts

D)using interest rate caps

A)maturity matching

B)using fixed-rate loans

C)using interest rate futures contracts

D)using interest rate caps

B

4

The measure of interest rate risk that uses the difference between rate-sensitive assets and rate-sensitive liabilities is called the

A)gap.

B)duration measurement.

C)duration ratio.

D)gap ratio.

A)gap.

B)duration measurement.

C)duration ratio.

D)gap ratio.

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

5

If a bank that relies heavily on short-term deposits for its funds replaces its investment in long-term Treasury securities with more floating-rate commercial loans, it is likely that the bank's exposure to

A)credit risk would decrease.

B)credit risk would increase.

C)interest rate risk would increase.

D)None of the above.

A)credit risk would decrease.

B)credit risk would increase.

C)interest rate risk would increase.

D)None of the above.

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

6

A gap ratio of less than 1.00 suggests that

A)rate-sensitive assets exceed rate-sensitive liabilities.

B)an increase in interest rates would increase the bank's net interest margin.

C)rate-sensitive liabilities exceed rate-sensitive assets.

D)a decrease in interest rates would decrease the bank's net interest margin.

E)an increase in interest rates would increase the bank's net interest margin AND a decrease in interest rates would decrease the bank's net interest margin.

A)rate-sensitive assets exceed rate-sensitive liabilities.

B)an increase in interest rates would increase the bank's net interest margin.

C)rate-sensitive liabilities exceed rate-sensitive assets.

D)a decrease in interest rates would decrease the bank's net interest margin.

E)an increase in interest rates would increase the bank's net interest margin AND a decrease in interest rates would decrease the bank's net interest margin.

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

7

Petri Bank had interest revenues of $70 million last year and $30 million in interest expenses. About $300 million of Petri's $800 million in assets are rate sensitive, while $600 million of its liabilities are rate sensitive. Petri Bank's net interest margin is ____ percent.

A)4.0

B)3.6

C)6.7

D)5.0

A)4.0

B)3.6

C)6.7

D)5.0

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

8

Other things being equal, assets with shorter maturities have ____ durations. Assets that generate more frequent coupon payments have ____ durations.

A)shorter; longer

B)shorter; shorter

C)longer; shorter

D)longer; longer

A)shorter; longer

B)shorter; shorter

C)longer; shorter

D)longer; longer

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

9

The ____ of interest rate futures ____ the potential adverse effect of rising interest rates on a bank's interest expenses.

A)sale; increases

B)sale; reduces

C)purchase; reduces

D)sale; increases AND purchase; reduces

A)sale; increases

B)sale; reduces

C)purchase; reduces

D)sale; increases AND purchase; reduces

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

10

Other things being equal, assets with ____ maturities and ____ frequent coupon payments have longer durations.

A)shorter; more

B)shorter; less

C)longer; more

D)longer; less

A)shorter; more

B)shorter; less

C)longer; more

D)longer; less

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

11

Each bank may have its own classification system of interest rate sensitivity, because there is no perfect measurement of the gap.

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

12

During a period of rising interest rates, a bank's net interest margin will likely ____ if its liabilities are ____ its assets.

A)increase; more rate sensitive than

B)decrease; more rate sensitive than

C)increase; equally rate sensitive as

D)decrease; equally rate sensitive as

A)increase; more rate sensitive than

B)decrease; more rate sensitive than

C)increase; equally rate sensitive as

D)decrease; equally rate sensitive as

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

13

Floating-rate loans cannot completely eliminate interest rate risk; if the cost of funds is changing more frequently than the rate on assets, the bank's net interest margin is still affected by interest rate fluctuations.

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

14

The duration of zero-coupon bonds will be ____ the duration of coupon bonds with the same maturity.

A)lower than

B)higher than

C)the same as

D)either a or b (depending on the size of the coupon payment)

A)lower than

B)higher than

C)the same as

D)either a or b (depending on the size of the coupon payment)

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

15

For most banks, the average duration of assets ____ the average duration of liabilities, so the duration gap is ____.

A)exceeds; zero

B)exceeds; negative

C)exceeds; positive

D)is less than; negative

A)exceeds; zero

B)exceeds; negative

C)exceeds; positive

D)is less than; negative

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

16

Banks can resolve a liquidity problem by

A)extending new loans.

B)selling assets.

C)buying back common stock.

D)increasing dividend payouts.

E)extending new loans AND selling assets.

A)extending new loans.

B)selling assets.

C)buying back common stock.

D)increasing dividend payouts.

E)extending new loans AND selling assets.

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

17

If a bank expects interest rates to consistently ____ over time, it will consider allocating most funds to rate-____ assets.

A)decrease; sensitive

B)decrease; insensitive

C)increase; insensitive

D)None of these are correct.

A)decrease; sensitive

B)decrease; insensitive

C)increase; insensitive

D)None of these are correct.

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

18

Which of the following financial institutions would be most willing to swap variable-rate payments for fixed-rate payments in order to reduce exposure to interest rate risk?

A)one whose assets and liabilities are equally interest-rate sensitive

B)one whose assets are more interest-rate sensitive than its liabilities

C)one whose liabilities are more interest-rate sensitive than its assets

D)one whose gap ratio is equal to 1.0

A)one whose assets and liabilities are equally interest-rate sensitive

B)one whose assets are more interest-rate sensitive than its liabilities

C)one whose liabilities are more interest-rate sensitive than its assets

D)one whose gap ratio is equal to 1.0

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

19

Banks increase their risk by increasing their capital as a percentage of assets.

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

20

Banks are more liquid as a result of securitization because it allows them to request repayment of the loan principal from the borrower upon demand.

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

21

Banks generally ____ loans and ____ their purchases of low-risk securities when the economy is weak.

A)increase; increase

B)reduce; reduce

C)increase; reduce

D)reduce; increase

A)increase; increase

B)reduce; reduce

C)increase; reduce

D)reduce; increase

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

22

Banks would reduce their liquidity by restructuring their asset portfolio to contain fewer ____ and more ____.

A)Treasury securities; excess reserves

B)loans; Treasury securities

C)corporate bonds; Treasury securities

D)None of these are correct.

A)Treasury securities; excess reserves

B)loans; Treasury securities

C)corporate bonds; Treasury securities

D)None of these are correct.

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

23

International diversification of loans can best reduce a bank's overall credit risk if

A)the loans are made in countries in a single continent.

B)the loans are made in countries whose economic cycles do not move together over time.

C)the loans are made in countries in a single continent AND the loans are made in countries whose economic cycles do not move together over time.

D)None of these are correct.

A)the loans are made in countries in a single continent.

B)the loans are made in countries whose economic cycles do not move together over time.

C)the loans are made in countries in a single continent AND the loans are made in countries whose economic cycles do not move together over time.

D)None of these are correct.

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

24

During a period of rising interest rates, a bank's net interest margin will likely decline if it has a large amount of

A)rate-sensitive assets and no rate-sensitive liabilities.

B)rate-sensitive liabilities and no rate-sensitive assets.

C)loans to technology firms.

D)real estate loans.

A)rate-sensitive assets and no rate-sensitive liabilities.

B)rate-sensitive liabilities and no rate-sensitive assets.

C)loans to technology firms.

D)real estate loans.

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

25

The greater the ____, the greater the amount of assets per dollar's worth of equity.

A)leverage measure

B)ratio of equity to debt

C)capital ratio

D)proportion of loans to securities in the asset portfolio

A)leverage measure

B)ratio of equity to debt

C)capital ratio

D)proportion of loans to securities in the asset portfolio

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

26

Most loan sales enable the bank originating the loan to continue servicing the loan.

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

27

If a bank desires to maximize its net interest margin, it would best achieve its goal by attempting to obtain most of its funds through ____ and use most of its funds for ____ (assuming that all loans will be repaid).

A)traditional demand deposits; commercial loans

B)traditional demand deposits; consumer loans

C)NOW accounts; consumer loans

D)NOW accounts; commercial loans

A)traditional demand deposits; commercial loans

B)traditional demand deposits; consumer loans

C)NOW accounts; consumer loans

D)NOW accounts; commercial loans

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

28

Banks tend to focus their loans in one industry so that they can specialize on that industry and reduce the credit risk of their loan portfolio.

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

29

A bank has a return on assets of 2 percent, $40 million in assets, and $4 million in equity. What is the return on equity?

A)10 percent

B).2 percent

C)2 percent

D)20 percent

E)None of these are correct.

A)10 percent

B).2 percent

C)2 percent

D)20 percent

E)None of these are correct.

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

30

Banks can increase their potential interest revenues by restructuring their asset portfolio to contain fewer ____ and more ____.

A)Treasury bonds; commercial loans

B)Treasury bonds; excess reserves

C)consumer loans; Treasury bills

D)None of these are correct.

A)Treasury bonds; commercial loans

B)Treasury bonds; excess reserves

C)consumer loans; Treasury bills

D)None of these are correct.

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

31

If a bank sells interest rate futures, it ____ the potential adverse effect of rising interest rates and ____ the potential favorable effect of declining interest rates on its interest expenses.

A)reduces; reduces

B)increases; increases

C)reduces; increases

D)increases; reduces

A)reduces; reduces

B)increases; increases

C)reduces; increases

D)increases; reduces

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

32

Banks can improve their liquidity position by restructuring their asset portfolio to contain fewer ____ and more ____.

A)excess reserves; Treasury bills

B)Treasury bonds; corporate bonds

C)loans; Treasury bills

D)None of these are correct.

A)excess reserves; Treasury bills

B)Treasury bonds; corporate bonds

C)loans; Treasury bills

D)None of these are correct.

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

33

A bank has the following asset and liability portfolios. What is the gap?

A)$750 million

B)- $750 million

C)1.12

D).896

E)None of these are correct.

A)$750 million

B)- $750 million

C)1.12

D).896

E)None of these are correct.

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

34

If Bank A has a negative gap and Bank B has a positive gap, which of the following is true?

A)Bank A is favorably affected by rising interest rates.

B)Bank B is favorably affected by falling interest rates.

C)Bank A is adversely affected by falling interest rates.

D)None of these are correct.

A)Bank A is favorably affected by rising interest rates.

B)Bank B is favorably affected by falling interest rates.

C)Bank A is adversely affected by falling interest rates.

D)None of these are correct.

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

35

A common method for banks to reduce their credit risk is to

A)specialize in loans to one or a few industries in which they have expertise in assessing creditworthiness.

B)specialize in loans to companies whose earnings patterns are quite similar over time.

C)specialize in loans to one or a few industries in which they have expertise in assessing creditworthiness AND specialize in loans to companies whose earnings patterns are quite similar over time.

D)None of these are correct.

A)specialize in loans to one or a few industries in which they have expertise in assessing creditworthiness.

B)specialize in loans to companies whose earnings patterns are quite similar over time.

C)specialize in loans to one or a few industries in which they have expertise in assessing creditworthiness AND specialize in loans to companies whose earnings patterns are quite similar over time.

D)None of these are correct.

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

36

A bank's net interest margin is commonly defined as

A)interest revenues minus interest expenses.

B)(interest revenues minus interest expenses)/total assets.

C)(interest revenues minus interest expenses)/total liabilities.

D)(interest revenues minus interest expenses)/capital.

A)interest revenues minus interest expenses.

B)(interest revenues minus interest expenses)/total assets.

C)(interest revenues minus interest expenses)/total liabilities.

D)(interest revenues minus interest expenses)/capital.

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

37

ROE is defined as

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

38

Banks can reduce their credit risk by restructuring their asset portfolio to contain fewer ____ and more ____.

A)Treasury bonds; corporate bonds

B)Treasury bonds; municipal bonds

C)Treasury bonds; commercial loans

D)None of these are correct.

A)Treasury bonds; corporate bonds

B)Treasury bonds; municipal bonds

C)Treasury bonds; commercial loans

D)None of these are correct.

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

39

Which of the following is a measure for banks to use to assess their exposure to interest rate risk?

A)capital ratio

B)leverage measure

C)duration

D)gap ratio

E)duration AND gap ratio

A)capital ratio

B)leverage measure

C)duration

D)gap ratio

E)duration AND gap ratio

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

40

When measuring exposure to market risk, banks commonly use the ________.

A)value-at-risk method

B)operating leverage measure

C)matching maturity method

D)forward rate method

A)value-at-risk method

B)operating leverage measure

C)matching maturity method

D)forward rate method

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

41

Durango Bank has $2 million in rate-sensitive liabilities and $3 million in rate-sensitive assets. Durango's gap is ____, and Durango is probably more concerned about a(n)____ in interest rates.

A)- $1 million; increase

B)- $1 million; decrease

C)$1 million; increase

D)$1 million; decrease

E)None of these are correct.

A)- $1 million; increase

B)- $1 million; decrease

C)$1 million; increase

D)$1 million; decrease

E)None of these are correct.

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

42

If a bank has assets and liabilities in dollars and euros, its exposure to interest rate risk can best be minimized if the

A)currency mix of assets is similar to that of liabilities.

B)overall rate sensitivity of assets and liabilities is similar.

C)rate sensitivity of assets and liabilities is matched for each currency.

D)currency mix of assets is similar to that of liabilities AND overall rate sensitivity of assets and liabilities is similar.

A)currency mix of assets is similar to that of liabilities.

B)overall rate sensitivity of assets and liabilities is similar.

C)rate sensitivity of assets and liabilities is matched for each currency.

D)currency mix of assets is similar to that of liabilities AND overall rate sensitivity of assets and liabilities is similar.

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

43

The performance of a bank that continually concentrates on short-term deposits in euros and adjustable-rate dollar loans with equal rate sensitivity is

A)unaffected if euro interest rates increase and U.S. rates decrease.

B)unaffected if U.S. interest rates increase and euro interest rates decrease.

C)adversely affected if euro interest rates increase and U.S. rates decrease.

D)adversely affected if U.S. interest rates increase and euro rates decrease.

E)unaffected if euro interest rates increase and U.S. rates decrease AND unaffected if U.S. interest rates increase and euro interest rates decrease.

A)unaffected if euro interest rates increase and U.S. rates decrease.

B)unaffected if U.S. interest rates increase and euro interest rates decrease.

C)adversely affected if euro interest rates increase and U.S. rates decrease.

D)adversely affected if U.S. interest rates increase and euro rates decrease.

E)unaffected if euro interest rates increase and U.S. rates decrease AND unaffected if U.S. interest rates increase and euro interest rates decrease.

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

44

For a commercial bank, when the average duration of assets exceeds the average duration of liabilities, the duration gap is

A)zero.

B)positive.

C)negative.

D)either b or c, depending on the maturities of the assets .

A)zero.

B)positive.

C)negative.

D)either b or c, depending on the maturities of the assets .

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

45

When a bank makes an international loan containing a clause that allows repayment in a foreign currency, the bank is exposed to

A)loan settlement risk.

B)exchange rate risk.

C)global exchange risk.

D)currency transaction risk.

A)loan settlement risk.

B)exchange rate risk.

C)global exchange risk.

D)currency transaction risk.

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

46

A positive gap (or gap ratio of more than 1.00)suggests that rate-sensitive liabilities exceed rate-sensitive assets.

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

47

Bank A has interest revenues of $4 million, interest expenses of $5 million, and assets totaling $20 million. Bank A's net interest margin is

A)$1 million.

B)- $1 million.

C)- 5 percent.

D)5 percent.

A)$1 million.

B)- $1 million.

C)- 5 percent.

D)5 percent.

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

48

Floating-rate loans completely eliminate interest rate risk.

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

49

A bank can usually simultaneously maximize its return on assets and minimize credit risk.

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

50

____ is (are)least likely to be used as a method of reducing interest rate risk.

A)Maturity matching

B)Floating-rate loans

C)Stock options

D)Interest rate swaps

E)Interest rate caps

A)Maturity matching

B)Floating-rate loans

C)Stock options

D)Interest rate swaps

E)Interest rate caps

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

51

For most banks, the average duration of liabilities exceeds the average duration of assets, so the duration gap is positive.

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

52

Whether a bank has a temporary or a permanent need for funds, the decision should be to borrow in the federal funds market.

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

53

The Sarbanes-Oxley Act has had little impact on the monitoring conducted by the board members of commercial banks.

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

54

Assume a U.S. bank accepts deposits in dollars and made some fixed-rate loans in British pounds. Which of the following would reduce the bank's profit margin?

A)The pound appreciates against the dollar.

B)The pound depreciates against the dollar.

C)British interest rates decrease.

D)British interest rates increase.

E)British interest rates decrease AND British interest rates increase.

A)The pound appreciates against the dollar.

B)The pound depreciates against the dollar.

C)British interest rates decrease.

D)British interest rates increase.

E)British interest rates decrease AND British interest rates increase.

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

55

Leskar Bank has $2 million in rate-sensitive liabilities and $3 million in rate-sensitive assets. Leskar's gap ratio is ____.

A)1.5

B)0.67

C)$1 million

D)None of these are correct.

A)1.5

B)0.67

C)$1 million

D)None of these are correct.

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

56

____ is not a method used to assess interest rate risk.

A)Efficiency analysis

B)Gap analysis

C)Duration analysis

D)Sensitivity analysis

A)Efficiency analysis

B)Gap analysis

C)Duration analysis

D)Sensitivity analysis

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

57

The risk of a loss due to closing out a transaction is referred to as ____ risk.

A)credit

B)settlement

C)interest rate

D)exchange rate

E)None of these are correct.

A)credit

B)settlement

C)interest rate

D)exchange rate

E)None of these are correct.

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

58

Ringo Bank has a profit after taxes of $3 million, total assets of $300 million, and shareholders' equity of $30 million. Ringo's return on equity (ROE)is ____ percent.

A)1.0

B)10.0

C)3.0

D)None of these are correct.

A)1.0

B)10.0

C)3.0

D)None of these are correct.

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

59

Macon Bank has interest revenues of $5 million, interest expenses of $4 million, and assets totaling $20 million. Macon Bank's net interest margin is

A)$1 million.

B)- $1 million.

C)5 percent.

D)- 5 percent.

A)$1 million.

B)- $1 million.

C)5 percent.

D)- 5 percent.

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

60

If the duration of all of a bank's assets with a maturity of greater than one year is similar to that of its liabilities with a maturity greater than one year, interest rate risk is nonexistent.

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

61

In an interest rate swap, a bank whose liabilities are ____ rate sensitive than its assets can swap payments with a ____ interest rate in exchange for payments with a ____ interest rate.

A)more; fixed; variable

B)more; variable; fixed

C)less; fixed; variable

D)less; fixed; fixed

E)None of these are correct.

A)more; fixed; variable

B)more; variable; fixed

C)less; fixed; variable

D)less; fixed; fixed

E)None of these are correct.

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

62

In a sensitivity analysis using a bank's stock return, an interest rate proxy, and market returns, a ____ coefficient for the interest rate variable suggests that the bank's performance is ____ affected by ____ interest rates.

A)positive; adversely; rising

B)positive; favorably; declining

C)negative; adversely; rising

D)negative; favorably; rising

A)positive; adversely; rising

B)positive; favorably; declining

C)negative; adversely; rising

D)negative; favorably; rising

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

63

Crazer Bank has a profit after taxes of $2 million, total assets of $100 million, and shareholders' equity of $10 million. Crazer's return on equity (ROE)is ____ percent.

A)18

B)210

C)15

D)20

E)None of these are correct.

A)18

B)210

C)15

D)20

E)None of these are correct.

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

64

During a period of ____ interest rates, a bank's net interest margin will likely ____ if its liabilities are more rate sensitive than its assets.

A)decreasing; decrease

B)increasing; increase

C)decreasing; increase

D)increasing; remain stable

A)decreasing; decrease

B)increasing; increase

C)decreasing; increase

D)increasing; remain stable

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

65

Which of the following is a method that a bank can use to reduce its credit risk?

A)diversifying its loans across industries

B)focusing on credit card loans

C)focusing on consumer loans

D)selling its holdings of Treasury securities

A)diversifying its loans across industries

B)focusing on credit card loans

C)focusing on consumer loans

D)selling its holdings of Treasury securities

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

66

If a bank expects interest rates to consistently ____ over time, it will consider allocating most of its funds to rate-____ assets.

A)decrease; sensitive

B)increase; insensitive

C)increase; sensitive

D)decrease; sensitive AND increase; insensitive

E)None of these are correct.

A)decrease; sensitive

B)increase; insensitive

C)increase; sensitive

D)decrease; sensitive AND increase; insensitive

E)None of these are correct.

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

67

A(n)____________ is an agreement for a fee to receive payments when the interest rate of a particular security rises above a specified level by a specified date.

A)interest rate cap

B)interest rate futures contract

C)interest rate swap

D)maximum rate contract

A)interest rate cap

B)interest rate futures contract

C)interest rate swap

D)maximum rate contract

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

68

The Financial Reform Act of 2010 provides that if a bank suffers large losses because it took excessive risk, the Federal Reserve will appoint a new board of directors for the bank.

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

69

If interest rates ____, banks with ____ duration gaps will be ____ affected.

A)rise; positive; positively

B)rise; positive; adversely

C)decrease; positive; adversely

D)decrease; zero; positively

E)None of these are correct.

A)rise; positive; positively

B)rise; positive; adversely

C)decrease; positive; adversely

D)decrease; zero; positively

E)None of these are correct.

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

70

When determining the appropriate interest rate to charge on a loan, a bank uses the Federal Reserve's primary credit rate as a benchmark and adds a premium to this rate for less creditworthy customers.

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

71

If a bank has a ____ duration gap, its average asset duration is probably ____ than its liability duration.

A)zero; smaller

B)positive; larger

C)negative; larger

D)None of these are correct.

A)zero; smaller

B)positive; larger

C)negative; larger

D)None of these are correct.

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

72

An effective way to align bank managers' interests with shareholders' goal of higher returns is to compensate the managers with fixed salaries without a bonus.

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

73

Which of the following is NOT a function of a bank's board of directors?

A)overseeing acquisitions

B)determining a compensation system for the bank's executives

C)overseeing policies for changing the bank's capital structure

D)pursuing a proxy contest to change the bank's dividend policy

A)overseeing acquisitions

B)determining a compensation system for the bank's executives

C)overseeing policies for changing the bank's capital structure

D)pursuing a proxy contest to change the bank's dividend policy

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

74

Because riskier assets offer ____ returns, a bank's strategy to increase its return will typically entail a(n)____ in the overall credit risk of its asset portfolio.

A)lower; increase

B)lower; decrease

C)higher; increase

D)higher; decrease

E)None of these are correct.

A)lower; increase

B)lower; decrease

C)higher; increase

D)higher; decrease

E)None of these are correct.

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

75

____ is NOT a method used to assess interest rate risk.

A)Gap analysis

B)Ratio analysis

C)Duration analysis

D)Sensitivity analysis

E)All of these are methods of assessing interest rate risk.

A)Gap analysis

B)Ratio analysis

C)Duration analysis

D)Sensitivity analysis

E)All of these are methods of assessing interest rate risk.

Unlock Deck

Unlock for access to all 75 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 75 flashcards in this deck.