Deck 9: Perfect Competition

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

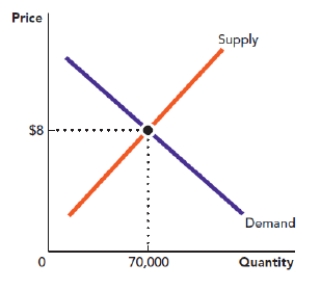

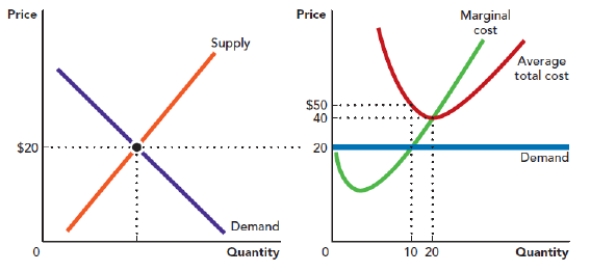

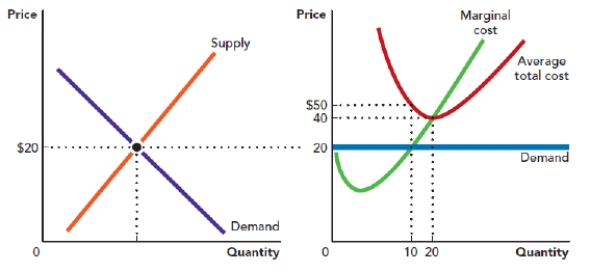

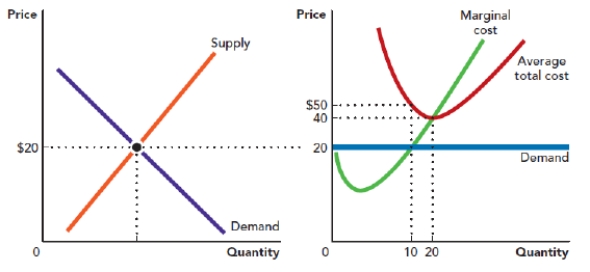

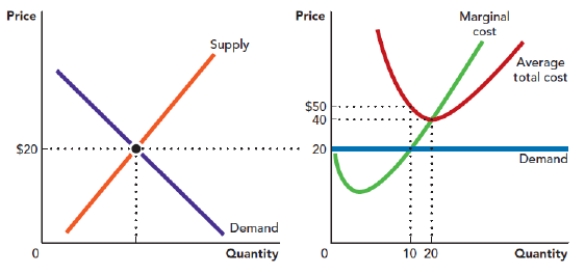

Use the figure A Perfectly Competitive Market. What is the marginal revenue that a firm in this market would earn from its 1,000th unit?

Figure: A Perfectly Competitive Market

A) $8

B) $80,000

C) $7

D) $70,000

Figure: A Perfectly Competitive Market

A) $8

B) $80,000

C) $7

D) $70,000

Question

Question

Question

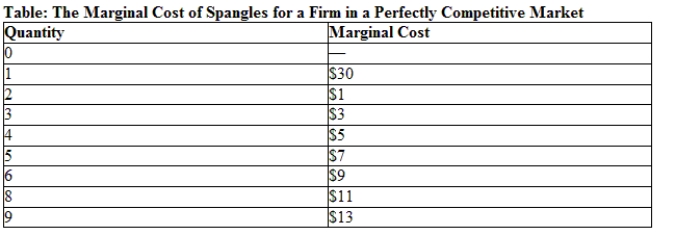

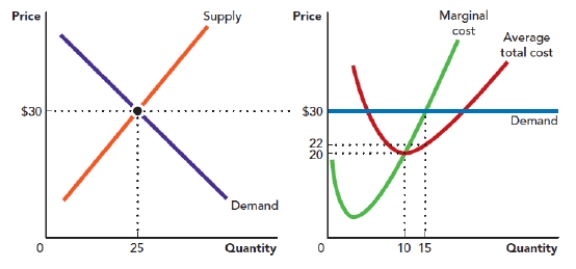

Use the table The Marginal Cost of Spangles for a Firm in a Perfectly Competitive Market. What quantity should this firm produce if the price of a spangle is $9?

A) one spangle

B) eight spangles

C) six spangles

D) nine spangles

A) one spangle

B) eight spangles

C) six spangles

D) nine spangles

Question

Use the figure A Perfectly Competitive Market. What is the optimal quantity that a firm operating in this market should produce?

Figure: A Perfectly Competitive Market

A) any quantity where the marginal cost is less than $8

B) 70,000

C) the quantity that has an average cost of $8

D) the quantity that has a marginal cost of $8

Figure: A Perfectly Competitive Market

A) any quantity where the marginal cost is less than $8

B) 70,000

C) the quantity that has an average cost of $8

D) the quantity that has a marginal cost of $8

Question

Question

Question

Question

Question

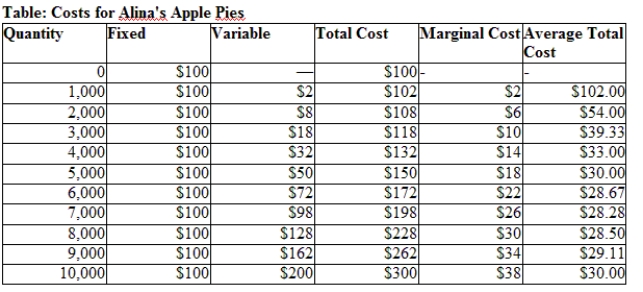

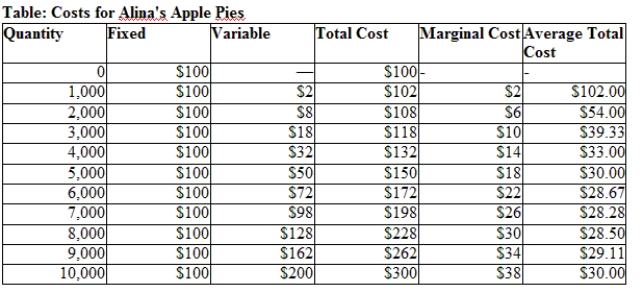

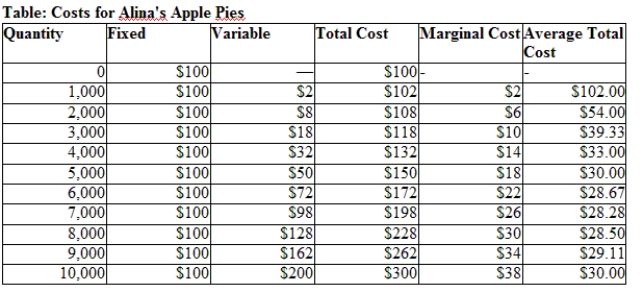

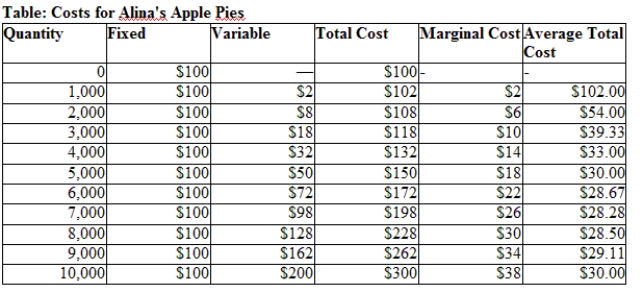

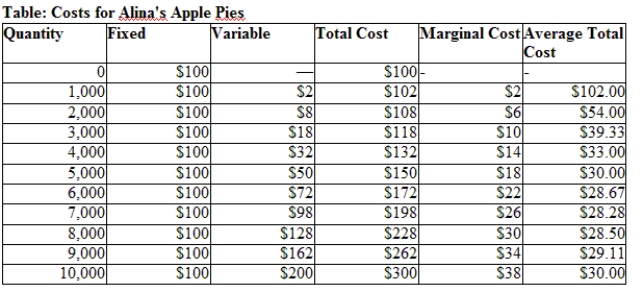

Use the table Costs for Alina's Apple Pies. If Alina's Apple Pies operates in a perfectly competitive market and the market price for a pie is $18, how many pies should Alina's Apple Pies produce?

A) 10,000 pies

B) 5,000 pies

C) 3,000 pies

D) 6,000 pies

A) 10,000 pies

B) 5,000 pies

C) 3,000 pies

D) 6,000 pies

Question

Question

Question

Question

Question

Use the table Costs for Alina's Apple Pies. If Alina's Apple Pies operates in a perfectly competitive market and the market price for a pie is $38, what profit (or loss) will this firm earn?

A) a profit of $80

B) a loss of $30

C) a loss of $200

D) a profit of $200

A) a profit of $80

B) a loss of $30

C) a loss of $200

D) a profit of $200

Question

Use the table Costs for Alina's Apple Pies. If Alina's Apple Pies operates in a perfectly competitive market and the market price for a pie is $18, what profit (or loss) will this firm earn?

A) a profit of $12

B) a loss of $60

C) a loss of $12

D) a profit of $60

A) a profit of $12

B) a loss of $60

C) a loss of $12

D) a profit of $60

Question

Use the figure A Perfectly Competitive Market in the Short Run I. What is the quantity that this firm will produce, and how much profit will it earn?

Figure: A Perfectly Competitive Market in the Short Run I

A) The quantity is 10, and the profit is $100,000.

B) The quantity is 15, and the profit is $120,000.

C) The quantity is 10, and the profit is $80,000.

D) The quantity is 15, and the profit is $150,000.

Figure: A Perfectly Competitive Market in the Short Run I

A) The quantity is 10, and the profit is $100,000.

B) The quantity is 15, and the profit is $120,000.

C) The quantity is 10, and the profit is $80,000.

D) The quantity is 15, and the profit is $150,000.

Question

Use the figure A Perfectly Competitive Market in the Short Run I. What is the quantity that this firm will produce, and how much profit or loss will it earn?

Figure: A Perfectly Competitive Market in the Short Run I

A) The quantity is 20, and the profit is $300,000.

B) The quantity is 10, and the profits is $200,000.

C) The quantity is 20, and the loss is $200,000.

D) The quantity is 10, and the loss is $300,000.

Figure: A Perfectly Competitive Market in the Short Run I

A) The quantity is 20, and the profit is $300,000.

B) The quantity is 10, and the profits is $200,000.

C) The quantity is 20, and the loss is $200,000.

D) The quantity is 10, and the loss is $300,000.

Question

Question

Use the figure A Perfectly Competitive Market in the Short Run I. If the price in this market persists, what will happen in the long run?

Figure: A Perfectly Competitive Market in the Short Run I

A) Firms will enter the market, and the market supply curve shifts to the right, lowering the price.

B) Firms will exit the market, and the average total cost curve shifts down, returning the firm to profit.

C) Firms will exit the market, and the market supply curve shifts to the left, raising the price.

D) Firms will enter the market, raising the marginal cost curve and increasing profits.

Figure: A Perfectly Competitive Market in the Short Run I

A) Firms will enter the market, and the market supply curve shifts to the right, lowering the price.

B) Firms will exit the market, and the average total cost curve shifts down, returning the firm to profit.

C) Firms will exit the market, and the market supply curve shifts to the left, raising the price.

D) Firms will enter the market, raising the marginal cost curve and increasing profits.

Question

Use the figure A Perfectly Competitive Market in the Short Run II. If the price in this market persists, what will happen in the long run?

Figure: A Perfectly Competitive Market in the Short Run II

A) Firms will enter the market, and the market supply curve shifts to the right, lowering the price.

B) Firms will exit the market, and the average total cost curve shifts down, returning the firm to profit.

C) Firms will exit the market, and the market supply curve shifts to the left, raising the price.

D) Firms will enter the market, raising the marginal cost curve and increasing profits.

Figure: A Perfectly Competitive Market in the Short Run II

A) Firms will enter the market, and the market supply curve shifts to the right, lowering the price.

B) Firms will exit the market, and the average total cost curve shifts down, returning the firm to profit.

C) Firms will exit the market, and the market supply curve shifts to the left, raising the price.

D) Firms will enter the market, raising the marginal cost curve and increasing profits.

Question

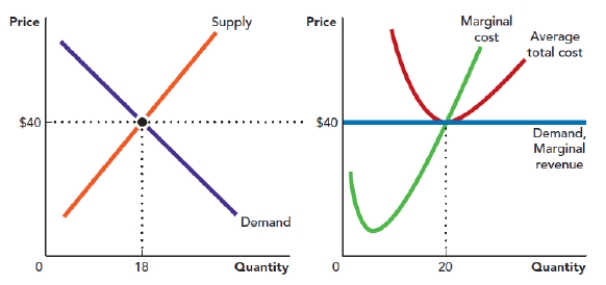

Use the figure A Perfectly Competitive Market in the Short Run III. What is the quantity that this firm will produce, and how much profit or loss will it earn?

Figure: A Perfectly Competitive Market in the Short Run III

A) The quantity is 20, and the profit is $800,000.

B) The quantity is 18, and the profit is $800,000.

C) The quantity is 20, and the profit is zero.

D) The quantity is 20, and the loss is $800,000.

Figure: A Perfectly Competitive Market in the Short Run III

A) The quantity is 20, and the profit is $800,000.

B) The quantity is 18, and the profit is $800,000.

C) The quantity is 20, and the profit is zero.

D) The quantity is 20, and the loss is $800,000.

Question

Use the figure A Perfectly Competitive Market in the Short Run IV. If the price in this market persists, what will happen in the long run?

Figure: A Perfectly Competitive Market in the Short Run IV

A) Firms will enter the market, and the market supply curve shifts to the right, lowering the price.

B) Firms will exit the market, and the average total cost curve shifts down, returning the firm to profit.

C) Firms will exit the market, and the market supply curve shifts to the left, raising the price.

D) Nothing, firms have no incentive to enter or exit this market.

Figure: A Perfectly Competitive Market in the Short Run IV

A) Firms will enter the market, and the market supply curve shifts to the right, lowering the price.

B) Firms will exit the market, and the average total cost curve shifts down, returning the firm to profit.

C) Firms will exit the market, and the market supply curve shifts to the left, raising the price.

D) Nothing, firms have no incentive to enter or exit this market.

Question

Question

Question

Question

Question

Question

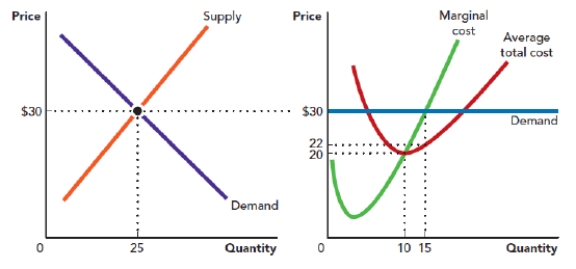

Use the figure A Perfectly Competitive Market in the Short Run II. If every firm in this market has the same costs, what will be the market price in the long run?

Figure: A Perfectly Competitive Market in the Short Run II

A) $29

B) $22

C) $15

D) $20

Figure: A Perfectly Competitive Market in the Short Run II

A) $29

B) $22

C) $15

D) $20

Question

Use the figure A Perfectly Competitive Market in the Short Run I. If every firm in this market has the same costs, what will be the market price in the long run?

Figure: A Perfectly Competitive Market in the Short Run I

A) $20

B) $40

C) $50

D) $60

Figure: A Perfectly Competitive Market in the Short Run I

A) $20

B) $40

C) $50

D) $60

Question

Use the table Costs for Alina's Apple Pies. Alina's Apple Pies operates in a perfectly competitive market where the price of a pie is currently $18. What will happen in the market in the long run?

A) Firms will enter this market, increasing the market supply curve and decreasing price.

B) Firms will exit this market, increasing the market supply curve and decreasing price.

C) Firms will enter this market, decreasing the market supply curve and increasing price.

D) Firms will exit this market, decreasing the market supply curve and increasing price.

A) Firms will enter this market, increasing the market supply curve and decreasing price.

B) Firms will exit this market, increasing the market supply curve and decreasing price.

C) Firms will enter this market, decreasing the market supply curve and increasing price.

D) Firms will exit this market, decreasing the market supply curve and increasing price.

Question

Use the table Costs for Alina's Apple Pies. Alina's Apple Pies operates in a perfectly competitive market. If Alina has no incentive to exit this market and no other firms have incentive to enter this market, what must the price be?

A) $28.28

B) $102

C) $30

D) $2

A) $28.28

B) $102

C) $30

D) $2

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/117

Play

Full screen (f)

Deck 9: Perfect Competition

1

How many buyers are there in a perfectly competitive market?

A) one

B) two

C) many

D) a few

A) one

B) two

C) many

D) a few

C

2

What is true about the products that are sold in a perfectly competitive market?

A) There is a single product.

B) Every firm sells the same standardized product.

C) Every firm sells a product that is slightly differentiated from other products.

D) The products that are sold are completely different from each other.

A) There is a single product.

B) Every firm sells the same standardized product.

C) Every firm sells a product that is slightly differentiated from other products.

D) The products that are sold are completely different from each other.

B

3

How many sellers are there in a perfectly competitive market?

A) one

B) two

C) many

D) a few

A) one

B) two

C) many

D) a few

C

4

How many buyers and sellers are there in a perfectly competitive market?

A) one buyer and many sellers

B) many buyers and one seller

C) many buyers and many sellers

D) a few buyers and one seller

A) one buyer and many sellers

B) many buyers and one seller

C) many buyers and many sellers

D) a few buyers and one seller

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

5

A market in which there are many buyers and sellers, every firm sells the same standardized product, buyers and sellers have full information about the product and its price, and it is easy for firms to enter and exit the market is known as _____ market.

A) an oligopoly

B) a duopoly

C) a monopoly

D) a perfectly competitive

A) an oligopoly

B) a duopoly

C) a monopoly

D) a perfectly competitive

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

6

Which of the following is NOT a feature of a perfectly competitive market?

A) differentiated products

B) easy entry and easy exit

C) many buyers and sellers

D) full information

A) differentiated products

B) easy entry and easy exit

C) many buyers and sellers

D) full information

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

7

In the market for shalanamags, there are many buyers and sellers, and every firm that sells shalanamags also sells an identical product. The market is easy for firms to enter, and buyers and sellers have perfect information. What kind of market is the market for shalanamags?

A) monopoly

B) oligopoly

C) monopolist competition

D) perfect competition

A) monopoly

B) oligopoly

C) monopolist competition

D) perfect competition

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

8

What is a key difference between a perfectly competitive market and a monopolistically competitive market?

A) Perfectly competitive markets have identical products, but monopolistically competitive markets have slightly differentiated products.

B) Perfectly competitive markets have difficult entry and exit, but monopolistically competitive markets have easy entry and exit.

C) Perfectly competitive markets have many buyers and sellers, but monopolistically competitive markets have only a few sellers.

D) Perfectly competitive markets have imperfect information, but monopolistically competitive markets have perfect information.

A) Perfectly competitive markets have identical products, but monopolistically competitive markets have slightly differentiated products.

B) Perfectly competitive markets have difficult entry and exit, but monopolistically competitive markets have easy entry and exit.

C) Perfectly competitive markets have many buyers and sellers, but monopolistically competitive markets have only a few sellers.

D) Perfectly competitive markets have imperfect information, but monopolistically competitive markets have perfect information.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

9

What is true about firms in a perfectly competitive market?

A) There are at least 50 firms.

B) There are enough firms that no firm can charge more than the market price.

C) There are at least 1,000 firms.

D) One firm is price leader and sets its own price, and all other firms copy that firm's price.

A) There are at least 50 firms.

B) There are enough firms that no firm can charge more than the market price.

C) There are at least 1,000 firms.

D) One firm is price leader and sets its own price, and all other firms copy that firm's price.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

10

In a perfectly competitive market:

A) there are few buyers.

B) every firm is selling a slightly different version of the product.

C) there is a single seller of a product.

D) individual firms cannot charge more than the market price.

A) there are few buyers.

B) every firm is selling a slightly different version of the product.

C) there is a single seller of a product.

D) individual firms cannot charge more than the market price.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

11

In the market for empanadas, there are enough sellers that no individual firm can charge more than the market price of $2.95 per empanadas. What feature of perfect competition is this describing?

A) perfect information

B) standardized product

C) easy entry and exit

D) many buyers and sellers

A) perfect information

B) standardized product

C) easy entry and exit

D) many buyers and sellers

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

12

The market for babysitting services in a small town is characterized by many families that want to hire babysitters. The three potential babysitters who are offering their services are all equally qualified, and there are no restrictions on becoming a babysitter. What feature of a perfectly competitive market does this violate?

A) many sellers

B) perfect information

C) many buyers

D) easy entry and exit

A) many sellers

B) perfect information

C) many buyers

D) easy entry and exit

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

13

In the market for empanadas, there are many buyers and sellers. However, Malini's empanadas have a unique seasoning that people are willing to pay more for. What feature of perfect competition does this market violate?

A) many sellers

B) perfect information

C) standardized product

D) easy entry and exit

A) many sellers

B) perfect information

C) standardized product

D) easy entry and exit

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

14

The market for fast food has thousands of restaurants and millions of potential customers. It is relatively easy to open a fast-food restaurant. Buyers are aware of their options and the prices of those options. However, some restaurants specialize in hamburgers, and others specialize in fried chicken. Which feature of a perfectly competitive market does the market for fast food violate?

A) many buyers and sellers

B) product standardization

C) easy entry and exit

D) full information about the product and its price

A) many buyers and sellers

B) product standardization

C) easy entry and exit

D) full information about the product and its price

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

15

Sally is selling homemade tamales in a market where many other firms make and sell tamales and many people want to buy homemade tamales. Everyone knows about all of the other sellers, but they are willing to pay more for Sally's tamales because they have the tastiest fillings. Why is the market for tamales not perfectly competitive?

A) There aren't many sellers.

B) There is imperfect information.

C) There aren't many buyers.

D) There isn't a standardized product.

A) There aren't many sellers.

B) There is imperfect information.

C) There aren't many buyers.

D) There isn't a standardized product.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

16

Why does standardization of products contribute to a firm having to sell its product at the market price in a perfectly competitive market?

A) It limits consumer information.

B) It limits seller information about competitors.

C) One firm's product is a perfect substitute for another firm's product.

D) There are a limited number of firms selling the product.

A) It limits consumer information.

B) It limits seller information about competitors.

C) One firm's product is a perfect substitute for another firm's product.

D) There are a limited number of firms selling the product.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

17

The reason that firms cannot charge more than the market price for a product in perfectly competitive markets is that:

A) one firm's product is a perfect substitute for another firm's product.

B) there are a limited number of sellers to choose from in perfectly competitive markets.

C) firms have imperfect information about the pricing by other firms.

D) firms sell goods that are all slightly differentiated from each other.

A) one firm's product is a perfect substitute for another firm's product.

B) there are a limited number of sellers to choose from in perfectly competitive markets.

C) firms have imperfect information about the pricing by other firms.

D) firms sell goods that are all slightly differentiated from each other.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

18

In imperfectly competitive markets, buyers and sellers have _____ relevant information about the products and prices available.

A) no

B) some

C) limited

D) all

A) no

B) some

C) limited

D) all

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

19

When a firm has full _____, it knows all of the relevant details about the products and prices that are available in a market.

A) utility

B) information

C) profits

D) complements

A) utility

B) information

C) profits

D) complements

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

20

In the market for Halloween pumpkins, there are many buyers and sellers, the pumpkin market is easy to enter, and all pumpkins sold are identical. One seller of pumpkins is on a main highway, and buyers don't know that many more sellers are located nearby. What feature of perfectly competitive markets is violated here?

A) many buyers

B) product standardization

C) easy entry and exit

D) full information

A) many buyers

B) product standardization

C) easy entry and exit

D) full information

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

21

In order for a market to be perfectly competitive so that no firm can charge a price higher than the market price, there must be many buyers and sellers, standardized product, easy entry and exit, and:

A) full faith and credit.

B) full information.

C) cost maximization.

D) inefficient scale.

A) full faith and credit.

B) full information.

C) cost maximization.

D) inefficient scale.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

22

Which of the following is essential in perfect competition?

A) differentiated products

B) imperfect information

C) few sellers

D) easy entry and exit

A) differentiated products

B) imperfect information

C) few sellers

D) easy entry and exit

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

23

The market for taxi services in a major metropolitan area has thousands of taxis and thousands of potential customers. Taxi services are identical, and buyers have full information about pricing. To become a taxi operator in this city requires a permit, which is difficult and expensive to obtain. Which feature of a perfectly competitive market is violated?

A) free entry and exit

B) full information

C) standardized product

D) many buyers and sellers

A) free entry and exit

B) full information

C) standardized product

D) many buyers and sellers

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

24

A firm is a price _____ if it accepts the market price as a given.

A) maker

B) taker

C) faker

D) staker

A) maker

B) taker

C) faker

D) staker

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

25

Tandy's Teas sells iced tea in a perfectly competitive market. Tandy knows that if she tries to sell iced tea at more than $1 per glass, people will buy iced tea from her competitors. What kind of a firm is Tandy's Teas?

A) price setter

B) price delegator

C) price taker

D) price neutral

A) price setter

B) price delegator

C) price taker

D) price neutral

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

26

Each individual seller in a market cannot influence the market price because each seller represents a very small part of the market. What is the term for a firm in that market?

A) oligopoly

B) duopoly

C) price taker

D) profit minimizer

A) oligopoly

B) duopoly

C) price taker

D) profit minimizer

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

27

Which of the following is NOT a reason that firms in a perfectly competitive market are price takers?

A) Each firm's good is a perfect substitute for another firm's good.

B) Each firm can sell more of its good at a lower price than at the market price.

C) Each buyer has perfect information about all alternatives.

D) There are many firms that a buyer can choose from.

A) Each firm's good is a perfect substitute for another firm's good.

B) Each firm can sell more of its good at a lower price than at the market price.

C) Each buyer has perfect information about all alternatives.

D) There are many firms that a buyer can choose from.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

28

What happens if an individual firm in a perfectly competitive market increases its price to be slightly above the market price?

A) All other firms raise their prices, too.

B) Buyers buy more from the firm that raises its price.

C) All other sellers in the market will lower their price below the market price.

D) Buyers will buy the good from other firms.

A) All other firms raise their prices, too.

B) Buyers buy more from the firm that raises its price.

C) All other sellers in the market will lower their price below the market price.

D) Buyers will buy the good from other firms.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

29

When perfectly competitive firms are said to be price takers, it means that firms:

A) are able to set the market price but cannot set the price of their product.

B) must accept the market price and cannot set the price of their own product.

C) must accept the market price but are able to set the price of their own product.

D) are able to set the market price and set the price of their own product.

A) are able to set the market price but cannot set the price of their product.

B) must accept the market price and cannot set the price of their own product.

C) must accept the market price but are able to set the price of their own product.

D) are able to set the market price and set the price of their own product.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

30

In a perfectly competitive market, each firm can sell _____ at the market price, and it can sell _____ at a price higher than the market price.

A) nothing; slightly more

B) all they want; all it wants

C) all they want; less

D) all they want; nothing

A) nothing; slightly more

B) all they want; all it wants

C) all they want; less

D) all they want; nothing

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

31

The demand curve in a perfectly competitive market is _____, and the demand curve facing an individual firm in that market is:

A) downward sloping; upward sloping.

B) downward sloping; downward sloping.

C) downward sloping; horizontal.

D) horizontal; downward sloping.

A) downward sloping; upward sloping.

B) downward sloping; downward sloping.

C) downward sloping; horizontal.

D) horizontal; downward sloping.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

32

The demand curve for a perfectly competitive firm's product is the same as the:

A) supply curve for a perfectly competitive firm.

B) demand curve for the market.

C) supply curve for the market.

D) marginal revenue curve for the firm.

A) supply curve for a perfectly competitive firm.

B) demand curve for the market.

C) supply curve for the market.

D) marginal revenue curve for the firm.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

33

What three things are identical for a perfectly competitive firm?

A) the market price, the firm's demand curve, and the firm's marginal revenue curve

B) the market price, the firm's average total cost curve, and the firm's marginal cost curve

C) the firm's average total cost curve, the market supply, and the market price

D) the firm's marginal cost curve, the market price, and the firm's marginal revenue curve

A) the market price, the firm's demand curve, and the firm's marginal revenue curve

B) the market price, the firm's average total cost curve, and the firm's marginal cost curve

C) the firm's average total cost curve, the market supply, and the market price

D) the firm's marginal cost curve, the market price, and the firm's marginal revenue curve

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

34

Why is a firm's marginal revenue curve horizontal?

A) It must lower its price to sell one more unit.

B) It can get the same price for every additional unit that it sells.

C) It can charge two different customers different prices.

D) It can charge a price higher than the market price.

A) It must lower its price to sell one more unit.

B) It can get the same price for every additional unit that it sells.

C) It can charge two different customers different prices.

D) It can charge a price higher than the market price.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

35

Which of the following statements about market structures is NOT true?

A) Perfect competition and monopoly are opposite extremes of competition.

B) Market structures vary based on number of firms, ease of entry and exit, and product differentiation.

C) Horizontal demand curves exist in all four market structures.

D) A duopoly has more firms than a monopoly.

A) Perfect competition and monopoly are opposite extremes of competition.

B) Market structures vary based on number of firms, ease of entry and exit, and product differentiation.

C) Horizontal demand curves exist in all four market structures.

D) A duopoly has more firms than a monopoly.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

36

The demand curve for an individual firm's product in a perfectly competitive market is:

A) upward sloping.

B) vertical.

C) downward sloping.

D) horizontal.

A) upward sloping.

B) vertical.

C) downward sloping.

D) horizontal.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

37

Spangles are sold in a perfectly competitive market, and the market price of a spangle is $10. A firm in this market can produce 100 spangles at a cost of $4 each. What does this firm's demand curve look like?

A) a horizontal line at $4

B) a vertical line at $14

C) a horizontal line at $6

D) a horizontal line at $10

A) a horizontal line at $4

B) a vertical line at $14

C) a horizontal line at $6

D) a horizontal line at $10

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

38

Use the figure A Perfectly Competitive Market. What is the marginal revenue that a firm in this market would earn from its 1,000th unit?

Figure: A Perfectly Competitive Market

A) $8

B) $80,000

C) $7

D) $70,000

Figure: A Perfectly Competitive Market

A) $8

B) $80,000

C) $7

D) $70,000

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

39

For a firm that is deciding how much to produce, the additional benefit comes in the form of marginal _____, and the additional cost is the _____ cost.

A) utility; marginal

B) revenue; average total

C) revenue; marginal

D) utility; total

A) utility; marginal

B) revenue; average total

C) revenue; marginal

D) utility; total

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

40

For a perfectly competitive firm, the optimal quantity to produce is the quantity where the marginal cost of producing that quantity equals its:

A) total revenue.

B) average total cost.

C) marginal utility.

D) price.

A) total revenue.

B) average total cost.

C) marginal utility.

D) price.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

41

Use the table The Marginal Cost of Spangles for a Firm in a Perfectly Competitive Market. What quantity should this firm produce if the price of a spangle is $9?

A) one spangle

B) eight spangles

C) six spangles

D) nine spangles

A) one spangle

B) eight spangles

C) six spangles

D) nine spangles

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

42

Use the figure A Perfectly Competitive Market. What is the optimal quantity that a firm operating in this market should produce?

Figure: A Perfectly Competitive Market

A) any quantity where the marginal cost is less than $8

B) 70,000

C) the quantity that has an average cost of $8

D) the quantity that has a marginal cost of $8

Figure: A Perfectly Competitive Market

A) any quantity where the marginal cost is less than $8

B) 70,000

C) the quantity that has an average cost of $8

D) the quantity that has a marginal cost of $8

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

43

When a firm in a perfectly competitive market is producing the optimal quantity, what is true?

A) P > MR and MR = MC

B) P = MR = MC

C) P < MC and MR < MC

D) P < MR and MR = MC

A) P > MR and MR = MC

B) P = MR = MC

C) P < MC and MR < MC

D) P < MR and MR = MC

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

44

A firm in a perfectly competitive market produces an optimal quantity when it produces the quantity where marginal:

A) cost equals the minimum of average total cost.

B) cost equals the price of the good.

C) revenue equals minimum average total cost.

D) revenue is greater than the price of the good.

A) cost equals the minimum of average total cost.

B) cost equals the price of the good.

C) revenue equals minimum average total cost.

D) revenue is greater than the price of the good.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

45

The market price of plunckets is $10, and the market for plunckets is perfectly competitive. If a firm in this market is choosing its optimal quantity of 98 plunckets, which of the following is NOT correct?

A) The marginal cost of the 98th unit is zero.

B) The marginal cost of the 97th unit is less than $10.

C) The marginal cost of the 99th unit is more than $10.

D) The marginal revenue of the 98th unit is $10.

A) The marginal cost of the 98th unit is zero.

B) The marginal cost of the 97th unit is less than $10.

C) The marginal cost of the 99th unit is more than $10.

D) The marginal revenue of the 98th unit is $10.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

46

Calini's sells empanadas in a perfectly competitive market. Calini's is currently producing 500 empanadas, and the marginal cost of the 500th empanada produced is $2.95. If the market price of an empanadas is $4, which of the following statements is true?

A) Calini's should increase the quantity of empanadas that it produces.

B) Calini's should decrease the quantity of empanadas that it produces.

C) Calini's should charge a price of $2.95.

D) Calini's should continue to produce 500 empanadas.

A) Calini's should increase the quantity of empanadas that it produces.

B) Calini's should decrease the quantity of empanadas that it produces.

C) Calini's should charge a price of $2.95.

D) Calini's should continue to produce 500 empanadas.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

47

Use the table Costs for Alina's Apple Pies. If Alina's Apple Pies operates in a perfectly competitive market and the market price for a pie is $18, how many pies should Alina's Apple Pies produce?

A) 10,000 pies

B) 5,000 pies

C) 3,000 pies

D) 6,000 pies

A) 10,000 pies

B) 5,000 pies

C) 3,000 pies

D) 6,000 pies

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

48

The height of the profit rectangle is the:

A) price of the good.

B) average total cost of the good.

C) difference between the price of a good and the average total cost of the good.

D) sum of the price of a good and the average total cost of the good.

A) price of the good.

B) average total cost of the good.

C) difference between the price of a good and the average total cost of the good.

D) sum of the price of a good and the average total cost of the good.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

49

The profit that is earned by a firm in a perfectly competitive market is the:

A) quantity produced multiplied by the difference between the price and average total cost.

B) quantity produced multiplied by the difference between the price and marginal cost.

C) quantity produced multiplied by the price.

D) average total cost multiplied by the price of the good.

A) quantity produced multiplied by the difference between the price and average total cost.

B) quantity produced multiplied by the difference between the price and marginal cost.

C) quantity produced multiplied by the price.

D) average total cost multiplied by the price of the good.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

50

Which of the following mathematical expressions accurately describes how to calculate the profit rectangle for a perfectly competitive firm?

A) P(ATC - Q)

B) Q(P - ATC)

C) Q(P - AVC)

D) ATC(P - Q)

A) P(ATC - Q)

B) Q(P - ATC)

C) Q(P - AVC)

D) ATC(P - Q)

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

51

A profit-maximizing firm in a perfectly competitive market is currently producing 1,000 units. The marginal cost of the 1,000th unit is $4, and the average total cost of producing 1,000 units is $1 per unit. Which of the following statements is NOT true?

A) The firm earns a profit of $3,000.

B) The market price is $4.

C) The marginal cost of 1,001 units is more than $4.

D) The firm's profit per unit is $4.

A) The firm earns a profit of $3,000.

B) The market price is $4.

C) The marginal cost of 1,001 units is more than $4.

D) The firm's profit per unit is $4.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

52

Use the table Costs for Alina's Apple Pies. If Alina's Apple Pies operates in a perfectly competitive market and the market price for a pie is $38, what profit (or loss) will this firm earn?

A) a profit of $80

B) a loss of $30

C) a loss of $200

D) a profit of $200

A) a profit of $80

B) a loss of $30

C) a loss of $200

D) a profit of $200

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

53

Use the table Costs for Alina's Apple Pies. If Alina's Apple Pies operates in a perfectly competitive market and the market price for a pie is $18, what profit (or loss) will this firm earn?

A) a profit of $12

B) a loss of $60

C) a loss of $12

D) a profit of $60

A) a profit of $12

B) a loss of $60

C) a loss of $12

D) a profit of $60

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

54

Use the figure A Perfectly Competitive Market in the Short Run I. What is the quantity that this firm will produce, and how much profit will it earn?

Figure: A Perfectly Competitive Market in the Short Run I

A) The quantity is 10, and the profit is $100,000.

B) The quantity is 15, and the profit is $120,000.

C) The quantity is 10, and the profit is $80,000.

D) The quantity is 15, and the profit is $150,000.

Figure: A Perfectly Competitive Market in the Short Run I

A) The quantity is 10, and the profit is $100,000.

B) The quantity is 15, and the profit is $120,000.

C) The quantity is 10, and the profit is $80,000.

D) The quantity is 15, and the profit is $150,000.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

55

Use the figure A Perfectly Competitive Market in the Short Run I. What is the quantity that this firm will produce, and how much profit or loss will it earn?

Figure: A Perfectly Competitive Market in the Short Run I

A) The quantity is 20, and the profit is $300,000.

B) The quantity is 10, and the profits is $200,000.

C) The quantity is 20, and the loss is $200,000.

D) The quantity is 10, and the loss is $300,000.

Figure: A Perfectly Competitive Market in the Short Run I

A) The quantity is 20, and the profit is $300,000.

B) The quantity is 10, and the profits is $200,000.

C) The quantity is 20, and the loss is $200,000.

D) The quantity is 10, and the loss is $300,000.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

56

What happens if price is less than average total cost in a perfectly competitive market?

A) Firms will be attracted to the market, and the market supply curve increases.

B) Firms experience losses.

C) Firms experience economic profit equal to zero.

D) Firms experience economic profits.

A) Firms will be attracted to the market, and the market supply curve increases.

B) Firms experience losses.

C) Firms experience economic profit equal to zero.

D) Firms experience economic profits.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

57

Use the figure A Perfectly Competitive Market in the Short Run I. If the price in this market persists, what will happen in the long run?

Figure: A Perfectly Competitive Market in the Short Run I

A) Firms will enter the market, and the market supply curve shifts to the right, lowering the price.

B) Firms will exit the market, and the average total cost curve shifts down, returning the firm to profit.

C) Firms will exit the market, and the market supply curve shifts to the left, raising the price.

D) Firms will enter the market, raising the marginal cost curve and increasing profits.

Figure: A Perfectly Competitive Market in the Short Run I

A) Firms will enter the market, and the market supply curve shifts to the right, lowering the price.

B) Firms will exit the market, and the average total cost curve shifts down, returning the firm to profit.

C) Firms will exit the market, and the market supply curve shifts to the left, raising the price.

D) Firms will enter the market, raising the marginal cost curve and increasing profits.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

58

Use the figure A Perfectly Competitive Market in the Short Run II. If the price in this market persists, what will happen in the long run?

Figure: A Perfectly Competitive Market in the Short Run II

A) Firms will enter the market, and the market supply curve shifts to the right, lowering the price.

B) Firms will exit the market, and the average total cost curve shifts down, returning the firm to profit.

C) Firms will exit the market, and the market supply curve shifts to the left, raising the price.

D) Firms will enter the market, raising the marginal cost curve and increasing profits.

Figure: A Perfectly Competitive Market in the Short Run II

A) Firms will enter the market, and the market supply curve shifts to the right, lowering the price.

B) Firms will exit the market, and the average total cost curve shifts down, returning the firm to profit.

C) Firms will exit the market, and the market supply curve shifts to the left, raising the price.

D) Firms will enter the market, raising the marginal cost curve and increasing profits.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

59

Use the figure A Perfectly Competitive Market in the Short Run III. What is the quantity that this firm will produce, and how much profit or loss will it earn?

Figure: A Perfectly Competitive Market in the Short Run III

A) The quantity is 20, and the profit is $800,000.

B) The quantity is 18, and the profit is $800,000.

C) The quantity is 20, and the profit is zero.

D) The quantity is 20, and the loss is $800,000.

Figure: A Perfectly Competitive Market in the Short Run III

A) The quantity is 20, and the profit is $800,000.

B) The quantity is 18, and the profit is $800,000.

C) The quantity is 20, and the profit is zero.

D) The quantity is 20, and the loss is $800,000.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

60

Use the figure A Perfectly Competitive Market in the Short Run IV. If the price in this market persists, what will happen in the long run?

Figure: A Perfectly Competitive Market in the Short Run IV

A) Firms will enter the market, and the market supply curve shifts to the right, lowering the price.

B) Firms will exit the market, and the average total cost curve shifts down, returning the firm to profit.

C) Firms will exit the market, and the market supply curve shifts to the left, raising the price.

D) Nothing, firms have no incentive to enter or exit this market.

Figure: A Perfectly Competitive Market in the Short Run IV

A) Firms will enter the market, and the market supply curve shifts to the right, lowering the price.

B) Firms will exit the market, and the average total cost curve shifts down, returning the firm to profit.

C) Firms will exit the market, and the market supply curve shifts to the left, raising the price.

D) Nothing, firms have no incentive to enter or exit this market.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

61

Which of the following is true when a firm in a perfectly competitive market is earning zero economic profits?

A) Price is less than average total cost.

B) Business owners are earning as much income as their next best alternative.

C) Firms will exit the market, driving up price until remaining firms earn positive economic profits.

D) Business owners are earning no income.

A) Price is less than average total cost.

B) Business owners are earning as much income as their next best alternative.

C) Firms will exit the market, driving up price until remaining firms earn positive economic profits.

D) Business owners are earning no income.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

62

Which of the following is NOT true in the long-run equilibrium in a perfectly competitive market?

A) No entrepreneur in the market can earn any more money doing something else.

B) Price is equal to the minimum average total cost of a firm.

C) Firms have an incentive to exit the market.

D) Accounting profits may still be positive.

A) No entrepreneur in the market can earn any more money doing something else.

B) Price is equal to the minimum average total cost of a firm.

C) Firms have an incentive to exit the market.

D) Accounting profits may still be positive.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

63

When perfectly competitive firms are in long-run equilibrium:

A) P = MR = MC = AVC.

B) P > MR > MC > ATC.

C) P = MR = MC = ATC.

D) P > MR = MC > ATC.

A) P = MR = MC = AVC.

B) P > MR > MC > ATC.

C) P = MR = MC = ATC.

D) P > MR = MC > ATC.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

64

A perfectly competitive market is in long-run equilibrium. If the market demand curve shifts to the right, what do we expect to occur in this market?

A) Negative economic profits will attract new firms to the market, decreasing price until price equals average total cost.

B) Positive economic profits will attract new firms to the market, decreasing price until price equals average total cost.

C) Positive economic profits will attract new firms to the market, increasing price until price equals average total cost.

D) Positive economic profits will attract new firms to the market, decreasing price until price equals average variable cost.

A) Negative economic profits will attract new firms to the market, decreasing price until price equals average total cost.

B) Positive economic profits will attract new firms to the market, decreasing price until price equals average total cost.

C) Positive economic profits will attract new firms to the market, increasing price until price equals average total cost.

D) Positive economic profits will attract new firms to the market, decreasing price until price equals average variable cost.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

65

A perfectly competitive market is in long-run equilibrium. If the market demand curve shifts to the left, what do we expect to occur in this market?

A) Negative economic profits will cause firms to exit the market, decreasing price until price equals average total cost.

B) Positive economic profits will attract new firms to the market, decreasing price until price equals average total cost.

C) Negative economic profits will cause firms to exit the market, increasing price until price equals average total cost.

D) Negative economic profits will attract new firms to the market, decreasing price until price equals average variable cost.

A) Negative economic profits will cause firms to exit the market, decreasing price until price equals average total cost.

B) Positive economic profits will attract new firms to the market, decreasing price until price equals average total cost.

C) Negative economic profits will cause firms to exit the market, increasing price until price equals average total cost.

D) Negative economic profits will attract new firms to the market, decreasing price until price equals average variable cost.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

66

Use the figure A Perfectly Competitive Market in the Short Run II. If every firm in this market has the same costs, what will be the market price in the long run?

Figure: A Perfectly Competitive Market in the Short Run II

A) $29

B) $22

C) $15

D) $20

Figure: A Perfectly Competitive Market in the Short Run II

A) $29

B) $22

C) $15

D) $20

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

67

Use the figure A Perfectly Competitive Market in the Short Run I. If every firm in this market has the same costs, what will be the market price in the long run?

Figure: A Perfectly Competitive Market in the Short Run I

A) $20

B) $40

C) $50

D) $60

Figure: A Perfectly Competitive Market in the Short Run I

A) $20

B) $40

C) $50

D) $60

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

68

Use the table Costs for Alina's Apple Pies. Alina's Apple Pies operates in a perfectly competitive market where the price of a pie is currently $18. What will happen in the market in the long run?

A) Firms will enter this market, increasing the market supply curve and decreasing price.

B) Firms will exit this market, increasing the market supply curve and decreasing price.

C) Firms will enter this market, decreasing the market supply curve and increasing price.

D) Firms will exit this market, decreasing the market supply curve and increasing price.

A) Firms will enter this market, increasing the market supply curve and decreasing price.

B) Firms will exit this market, increasing the market supply curve and decreasing price.

C) Firms will enter this market, decreasing the market supply curve and increasing price.

D) Firms will exit this market, decreasing the market supply curve and increasing price.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

69

Use the table Costs for Alina's Apple Pies. Alina's Apple Pies operates in a perfectly competitive market. If Alina has no incentive to exit this market and no other firms have incentive to enter this market, what must the price be?

A) $28.28

B) $102

C) $30

D) $2

A) $28.28

B) $102

C) $30

D) $2

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

70

In a perfectly competitive market, the market price is $5, and firms are producing 100 units. At a quantity of 100 units, average total cost is $4, and average variable cost is $3. In the long run, price will:

A) rise above $5 as firms exit the market.

B) remain at $5.

C) fall to $3 as firms enter the market.

D) fall to $4 as firms enter the market.

A) rise above $5 as firms exit the market.

B) remain at $5.

C) fall to $3 as firms enter the market.

D) fall to $4 as firms enter the market.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

71

In a perfectly competitive market the market price is $4, and firms are producing 100 units. At a quantity of 100 units, average total cost is $4, and average variable cost is $3. In the long run, price will:

A) rise above $5 as firms exit the market.

B) remain at $4.

C) fall to $3 as firms enter the market.

D) fall to $4 as firms enter the market.

A) rise above $5 as firms exit the market.

B) remain at $4.

C) fall to $3 as firms enter the market.

D) fall to $4 as firms enter the market.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

72

In a perfectly competitive market, the market price is $3.50, and firms are producing 100 units. At a quantity of 100 units, average total cost is $4, and average variable cost is $3. In the long run, price will:

A) rise to $4 as firms exit the market.

B) remain at $3.50.

C) fall to $3 as firms enter the market.

D) fall to $4 as firms enter the market.

A) rise to $4 as firms exit the market.

B) remain at $3.50.

C) fall to $3 as firms enter the market.

D) fall to $4 as firms enter the market.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

73

Suppose that Magma Motor Company has total revenue of $400,000, fixed costs of $100,000, and variable costs of $200,000. If Magma Motor company is known to be in a perfectly competitive market, which of the following is true?

A) This market is in long-run equilibrium.

B) Firms will enter this market.

C) Firms will exit this market.

D) Magma's average total cost is as low as it can be.

A) This market is in long-run equilibrium.

B) Firms will enter this market.

C) Firms will exit this market.

D) Magma's average total cost is as low as it can be.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

74

Suppose that Pumice Motor Company has total revenue of $800,000, fixed costs of $200,000, and variable costs of $900,000. If Pumice Motor company is known to be in a perfectly competitive market, which of the following is true?

A) This market is in long-run equilibrium.

B) Firms will enter this market.

C) Firms will exit this market.

D) Pumice Motor Company's average total cost is as low as it can be.

A) This market is in long-run equilibrium.

B) Firms will enter this market.

C) Firms will exit this market.

D) Pumice Motor Company's average total cost is as low as it can be.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

75

Lotus Airways is a passenger carrying airline and has total revenue of $900,000, fixed costs of $500,000, and variable costs of $400,000. What is true if Lotus Airways operates in a perfectly competitive industry?

A) This market is in long-run equilibrium.

B) Lotus Airways should shut down.

C) Lotus Airways should exit the industry

D) Other airlines will enter this industry.

A) This market is in long-run equilibrium.

B) Lotus Airways should shut down.

C) Lotus Airways should exit the industry

D) Other airlines will enter this industry.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

76

Orchid Movers is a price taker in the market for cross-country moving services. The current price to move a two-bedroom house is $1,000, and given the number of homes that it is currently moving, the average cost of providing this service to Orchid Movers is $900. What statement best describes what is likely to happen in the market for moving services?

A) Firms will enter this market and drive down the price of moving services.

B) Firms will exit this market and drive down the price of moving services.

C) Firms do not have an incentive to enter or exit this market.

D) Firms like Orchid Movers will shut down temporarily.

A) Firms will enter this market and drive down the price of moving services.

B) Firms will exit this market and drive down the price of moving services.

C) Firms do not have an incentive to enter or exit this market.

D) Firms like Orchid Movers will shut down temporarily.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

77

Suppose that Pumice Motor Company has total revenue of $800,000, fixed costs of $200,000, and variable costs of $600,000. If Pumice Motor company is known to be in a perfectly competitive market, which of the following is true?

A) This market is in long-run equilibrium.

B) Firms will enter this market.

C) Firms will exit this market.

D) Magma's average total cost is as low as it can be.

A) This market is in long-run equilibrium.

B) Firms will enter this market.

C) Firms will exit this market.

D) Magma's average total cost is as low as it can be.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

78

When a perfectly competitive market is in long-run equilibrium, a firm in that market produces the quantity where _____ is lowest.

A) marginal cost

B) average variable cost

C) average total cost

D) marginal revenue

A) marginal cost

B) average variable cost

C) average total cost

D) marginal revenue

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

79

Chrysanthemum Industries has fixed costs of $10,000 and variable costs of $20,000 when it produces 1,000 units. The 1,000th unit costs Chrysanthemum industries $30. This perfectly competitive industry:

A) will attract more firms.

B) is in long-run equilibrium.

C) will lead to firms existing this industry.

D) should shut down.

A) will attract more firms.

B) is in long-run equilibrium.

C) will lead to firms existing this industry.

D) should shut down.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

80

The decision to shut down a firm depends on whether the market price allows the firm to cover its:

A) marginal cost.

B) average total cost.

C) average variable cost.

D) marginal revenue.

A) marginal cost.

B) average total cost.

C) average variable cost.

D) marginal revenue.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 117 flashcards in this deck.