Deck 23: Inventory Valuation

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

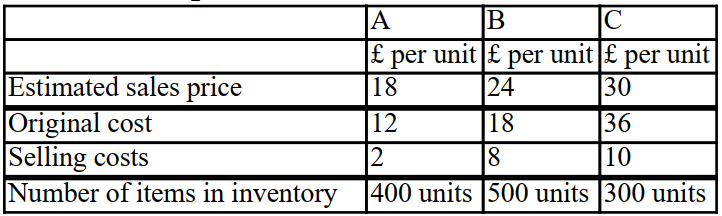

The value of inventory at the year end should be:

X sells three products - A, B and C. The following information was available at the year end.

A) £16,800

B) £18,800

C) £22,800

D) £24,600

X sells three products - A, B and C. The following information was available at the year end.

A) £16,800

B) £18,800

C) £22,800

D) £24,600

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/16

Play

Full screen (f)

Deck 23: Inventory Valuation

1

Which of the following cost flow assumption methods of inventory valuation assumes that the oldest inventory in stores is sold first?

A) FIFO assumption

B) LIFO assumption

C) AVCO assumption

D) None of the above

A) FIFO assumption

B) LIFO assumption

C) AVCO assumption

D) None of the above

FIFO assumption

2

Under IAS 2 which of the following does not form part of the purchase cost of inventory?

A) Import duties and other taxes that are not recoverable

B) Value added tax when VAT registered

C) Transport costs for delivery

D) Inventory handling costs

A) Import duties and other taxes that are not recoverable

B) Value added tax when VAT registered

C) Transport costs for delivery

D) Inventory handling costs

Value added tax when VAT registered

3

In times of falling prices, which of the following methods of closing inventory valuation would be selected, if the business wants to achieve the highest possible level of gross profit:

A) FIFO assumption

B) LIFO assumption

C) AVCO assumption

D) Any of the above as they all produce the same result

A) FIFO assumption

B) LIFO assumption

C) AVCO assumption

D) Any of the above as they all produce the same result

LIFO assumption

4

Some of Anna's Inventory at the year end had been damaged. This inventory cost £590, however, due to the damage would require a further £100 to be spent on them to make them saleable. In addition, Anna thinks she will have to incur £100 advertising the goods. She predicts that they could then be sold for £900.

What value should the inventory be included in the accounts at?

A) £390

B) £590

C) £700

D) £800

What value should the inventory be included in the accounts at?

A) £390

B) £590

C) £700

D) £800

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

5

The following information should be used to answer questions 5 to 10 inclusive

An inventory ledger card shows the following details:

June 1 50 units in inventory at £20 per unit.

June 7 100 units purchased at a cost of £22.50

June 14 80 units sold at £48.00

June 21 50 units purchased at a cost of £25 per unit

June 22 60 units sold at £51.00

-What is the value of inventory at 30 June using the FIFO method (to the nearest pound)?

A) £1,225

B) £1,383

C) £1,475

D) £1,500

An inventory ledger card shows the following details:

June 1 50 units in inventory at £20 per unit.

June 7 100 units purchased at a cost of £22.50

June 14 80 units sold at £48.00

June 21 50 units purchased at a cost of £25 per unit

June 22 60 units sold at £51.00

-What is the value of inventory at 30 June using the FIFO method (to the nearest pound)?

A) £1,225

B) £1,383

C) £1,475

D) £1,500

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

6

The following information should be used to answer questions 5 to 10 inclusive

An inventory ledger card shows the following details:

June 1 50 units in inventory at £20 per unit.

June 7 100 units purchased at a cost of £22.50

June 14 80 units sold at £48.00

June 21 50 units purchased at a cost of £25 per unit

June 22 60 units sold at £51.00

-What is the value of inventory at 30 June using the LIFO method?

A) £1,225

B) £1,383

C) £1,475

D) £1,500

An inventory ledger card shows the following details:

June 1 50 units in inventory at £20 per unit.

June 7 100 units purchased at a cost of £22.50

June 14 80 units sold at £48.00

June 21 50 units purchased at a cost of £25 per unit

June 22 60 units sold at £51.00

-What is the value of inventory at 30 June using the LIFO method?

A) £1,225

B) £1,383

C) £1,475

D) £1,500

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

7

The following information should be used to answer questions 5 to 10 inclusive

An inventory ledger card shows the following details:

June 1 50 units in inventory at £20 per unit.

June 7 100 units purchased at a cost of £22.50

June 14 80 units sold at £48.00

June 21 50 units purchased at a cost of £25 per unit

June 22 60 units sold at £51.00

-What is the value of inventory at 30 June using the AVCO method?

A) £1,225

B) £1,383

C) £1,475

D) £1,500

An inventory ledger card shows the following details:

June 1 50 units in inventory at £20 per unit.

June 7 100 units purchased at a cost of £22.50

June 14 80 units sold at £48.00

June 21 50 units purchased at a cost of £25 per unit

June 22 60 units sold at £51.00

-What is the value of inventory at 30 June using the AVCO method?

A) £1,225

B) £1,383

C) £1,475

D) £1,500

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

8

The following information should be used to answer questions 5 to 10 inclusive

An inventory ledger card shows the following details:

June 1 50 units in inventory at £20 per unit.

June 7 100 units purchased at a cost of £22.50

June 14 80 units sold at £48.00

June 21 50 units purchased at a cost of £25 per unit

June 22 60 units sold at £51.00

-What is the profit for the month of June, assuming the FIFO method of inventory valuation is used (to the nearest pound)?

A) £2,875

B) £3,625

C) £3,783

D) £3,875

An inventory ledger card shows the following details:

June 1 50 units in inventory at £20 per unit.

June 7 100 units purchased at a cost of £22.50

June 14 80 units sold at £48.00

June 21 50 units purchased at a cost of £25 per unit

June 22 60 units sold at £51.00

-What is the profit for the month of June, assuming the FIFO method of inventory valuation is used (to the nearest pound)?

A) £2,875

B) £3,625

C) £3,783

D) £3,875

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

9

The following information should be used to answer questions 5 to 10 inclusive

An inventory ledger card shows the following details:

June 1 50 units in inventory at £20 per unit.

June 7 100 units purchased at a cost of £22.50

June 14 80 units sold at £48.00

June 21 50 units purchased at a cost of £25 per unit

June 22 60 units sold at £51.00

-What is the profit for the month of June, assuming the LIFO method of inventory valuation is used (to the nearest pound)?

A) £2,875

B) £3,625

C) £3,783

D) £3,875

An inventory ledger card shows the following details:

June 1 50 units in inventory at £20 per unit.

June 7 100 units purchased at a cost of £22.50

June 14 80 units sold at £48.00

June 21 50 units purchased at a cost of £25 per unit

June 22 60 units sold at £51.00

-What is the profit for the month of June, assuming the LIFO method of inventory valuation is used (to the nearest pound)?

A) £2,875

B) £3,625

C) £3,783

D) £3,875

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

10

The following information should be used to answer questions 5 to 10 inclusive

An inventory ledger card shows the following details:

June 1 50 units in inventory at £20 per unit.

June 7 100 units purchased at a cost of £22.50

June 14 80 units sold at £48.00

June 21 50 units purchased at a cost of £25 per unit

June 22 60 units sold at £51.00

-What is the profit for the month of June, assuming the LIFO method of inventory valuation is used (to the nearest pound)?

A) £2,875

B) £3,625

C) £3,783

D) £3,875

An inventory ledger card shows the following details:

June 1 50 units in inventory at £20 per unit.

June 7 100 units purchased at a cost of £22.50

June 14 80 units sold at £48.00

June 21 50 units purchased at a cost of £25 per unit

June 22 60 units sold at £51.00

-What is the profit for the month of June, assuming the LIFO method of inventory valuation is used (to the nearest pound)?

A) £2,875

B) £3,625

C) £3,783

D) £3,875

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

11

The value of inventory at the year end should be:

X sells three products - A, B and C. The following information was available at the year end.

A) £16,800

B) £18,800

C) £22,800

D) £24,600

X sells three products - A, B and C. The following information was available at the year end.

A) £16,800

B) £18,800

C) £22,800

D) £24,600

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

12

Which of the following best captures the net realisable value of inventory?

A) The market price

B) The replacement cost of the inventory

C) The expected selling price of the inventory less costs of sale.

D) The expected selling price of the inventory.

A) The market price

B) The replacement cost of the inventory

C) The expected selling price of the inventory less costs of sale.

D) The expected selling price of the inventory.

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

13

FIFO, AVCO and LIFO are inventory cost flow valuation methods. Which of the following statements is correct?

A) Average cost is recalculated following every issue and receipt of inventory.

B) When prices are rising FIFO produces the highest profit figure of the three methods.

C) When prices are rising LIFO produces the highest profit figure of the three methods.

D) The LIFO method is permissible under IAS 2.

A) Average cost is recalculated following every issue and receipt of inventory.

B) When prices are rising FIFO produces the highest profit figure of the three methods.

C) When prices are rising LIFO produces the highest profit figure of the three methods.

D) The LIFO method is permissible under IAS 2.

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

14

The entities stores were flooded resulting in a loss of inventory (Value £30,500). The entity had not insured its inventory. How should this loss be accounted for?

A) Dr. Cost of goods sold Cr. Inventory (statement of financial position)

B) Dr. Inventory (statement of financial position) Cr. Cost of goods sold

C) Dr Drawings account Cr. Cost of goods sold

D) Dr. Trading account Cr. Income statement account

A) Dr. Cost of goods sold Cr. Inventory (statement of financial position)

B) Dr. Inventory (statement of financial position) Cr. Cost of goods sold

C) Dr Drawings account Cr. Cost of goods sold

D) Dr. Trading account Cr. Income statement account

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

15

Sales for the year were £222,000. Gross profit was £60,000, purchases were £150,000 and opening inventory was £51,000.

The value of closing inventory is:

A) £81,000

B) £63,000

C) £39,000

D) £36,000

The value of closing inventory is:

A) £81,000

B) £63,000

C) £39,000

D) £36,000

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

16

Sales for the year were £438,000. Gross profit was £65,000, purchases were £308,000 and opening inventory was £81,000. Carriage inwards was £5,000 and carriage outwards was £6,000. Returns inward were £20,000.

The value of closing inventory is:

A) £21,000

B) £26,000

C) £20,000

D) £41,000

The value of closing inventory is:

A) £21,000

B) £26,000

C) £20,000

D) £41,000

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 16 flashcards in this deck.