Deck 18: Additional Reporting Issues

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

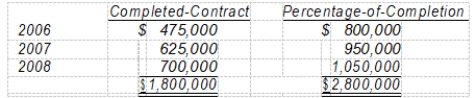

During 2008, a construction company changed from the completed-contract method to the percentage-of-completion method for accounting purposes but not for tax purposes. Gross profit figures under both methods for the past three years appear below:

Assuming an income tax rate of 40% for all years, the affect of this accounting change on prior periods should be reported by a credit of

Assuming an income tax rate of 40% for all years, the affect of this accounting change on prior periods should be reported by a credit of

A) $600,000 on the 2008 income statement.

B) $390,000 on the 2008 income statement.

C) $600,000 on the 2008 retained earnings statement.

D) $390,000 on the 2008 retained earnings statement.

Assuming an income tax rate of 40% for all years, the affect of this accounting change on prior periods should be reported by a credit ofA) $600,000 on the 2008 income statement.

B) $390,000 on the 2008 income statement.

C) $600,000 on the 2008 retained earnings statement.

D) $390,000 on the 2008 retained earnings statement.

Question

Question

Question

Eaton Company began operations on January 1, 2008, and uses the FIFO method in costing its raw materials inventory. Management is contemplating a change to the LIFO method and is interested in determining what effect such a change will have on net income. Accordingly, the following information has been developed:

Based on the above information, a change to the LIFO method in 2009 would result in net income for 2009 of

Based on the above information, a change to the LIFO method in 2009 would result in net income for 2009 of

A) $1,120,000.

B) $1,080,000.

C) $1,004,000.

D) $1,000,000.

Based on the above information, a change to the LIFO method in 2009 would result in net income for 2009 ofA) $1,120,000.

B) $1,080,000.

C) $1,004,000.

D) $1,000,000.

Question

Hannah Company began operations on January 1, 2008, and uses the FIFO method in costing its raw materials inventory. Management is contemplating a change to the LIFO method and is interested in determining what effect such a change will have on net income. Accordingly, the following information has been developed:

Based upon the above information, a change to the LIFO method in 2009 would result in net income for 2009 of

Based upon the above information, a change to the LIFO method in 2009 would result in net income for 2009 of

A) $540,000.

B) $600,000.

C) $620,000.

D) $660,000.

Based upon the above information, a change to the LIFO method in 2009 would result in net income for 2009 ofA) $540,000.

B) $600,000.

C) $620,000.

D) $660,000.

Question

Question

Question

Question

Question

Question

The following information is available for Alley Corporation:

The number of shares to be used in computing earnings per common share for 2008 is

The number of shares to be used in computing earnings per common share for 2008 is

A) 2,825,500.

B) 2,737,500.

C) 2,725,000.

D) 1,706,250.

The number of shares to be used in computing earnings per common share for 2008 isA) 2,825,500.

B) 2,737,500.

C) 2,725,000.

D) 1,706,250.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/70

Play

Full screen (f)

Deck 18: Additional Reporting Issues

1

Accounting alternatives diminish the comparability of financial information between periods and between companies.

True

2

A change in accounting principle results when a company adopts a new principle in recognition of events that were previously immaterial.

False

3

A change in accounting principle results when a company changes from one generally accepted accounting principle to another.

True

4

If the previously used accounting principle was not acceptable, a change to a generally accepted accounting principle is considered a change in principle.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

5

The FASB requires companies to use the prospective (in the future) approach for reporting changes in accounting principles.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

6

When a company changes an accounting principle under the retrospective approach, it adjusts its financial statements for each prior period presented.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

7

When a company changes an accounting principle, it should not adjust any assets or liabilities.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

8

The FASB takes the position that companies should retrospectively apply the indirect effects of a change in accounting principle.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

9

Companies should use retrospective application if the company cannot determine the effects of the retrospective application.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

10

If it becomes impracticable to use retrospective application for a change in accounting principle, a company should prospectively apply the new accounting principle.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

11

If a change in an accounting estimate affects current net income by an amount equal to or greater than 1% of net income, the change should be handled retroactively.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

12

When it is impossible to determine whether a change in principle or change in estimate has occurred, the change is considered a change in estimate.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

13

Companies account for a change in depreciation methods as a change in accounting principle.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

14

A change from an accounting principle that is not generally accepted to an accounting principle that is acceptable should be treated as an accounting error.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

15

FASB Statement No. 16 requires that corrections of errors be handled prospectively and shown in the current operating section of the income statement in the year the correction is made.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

16

A corporation's capital structure is simple if it includes securities that could have a dilutive effect on earnings per common share.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

17

When stock dividends or stock splits occur, computation of the weighted-average number of shares requires restatement of the shares outstanding before the stock dividend or split.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

18

Antidilutive securities are securities which upon their conversion or exercise decrease earnings per share (or increase the loss per share).

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

19

Antidilutive securities should be ignored in all calculations and should not be considered in computing diluted earnings per share.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

20

The treasury stock method will increase the number of shares outstanding whenever the exercise price of an option or warrant is below the market price of the common stock.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

21

Earnings per share data are required for each of the following: (a) income from continuing operations, (b) income before extraordinary items, and (c) net income.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

22

A company should report per share amounts for income before extraordinary items, but not for income from continuing operations.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

23

A change in accounting principle is evidenced by

A) a change from the historical cost principle to current value accounting.

B) adopting the allowance method in estimating bad debts expense when a credit sales policy is instituted.

C) changing the basis of inventory pricing from weighted-average cost to LIFO.

D) a change from current value accounting to the historical cost principle.

A) a change from the historical cost principle to current value accounting.

B) adopting the allowance method in estimating bad debts expense when a credit sales policy is instituted.

C) changing the basis of inventory pricing from weighted-average cost to LIFO.

D) a change from current value accounting to the historical cost principle.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

24

A company that reports changes retrospectively would

A) report the cumulative effect in the current year's income statement as an irregular item.

B) not change any prior-year financial statements.

C) make changes prospectively.

D) show any cumulative effect of the change as an adjustment to beginning retained earnings of the earliest year presented.

A) report the cumulative effect in the current year's income statement as an irregular item.

B) not change any prior-year financial statements.

C) make changes prospectively.

D) show any cumulative effect of the change as an adjustment to beginning retained earnings of the earliest year presented.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

25

According to the FASB, which approach is required for reporting changes in an accounting principle?

A) Currently

B) Retrospectively

C) Prospectively

D) Futuristically

A) Currently

B) Retrospectively

C) Prospectively

D) Futuristically

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

26

Which of the following is not considered a direct effect of a change in accounting principle?

A) An employee profit-sharing plan based on net income when a company uses the percentage-of-completion method.

B) The inventory balance as a result of a change in the inventory valuation method.

C) An impairment adjustment resulting from applying the lower-of-cost-or-market-test to the adjusted inventory balance.

D) Deferred income tax effects of an impairment adjustment resulting from applying the lower-of-cost-or-market test to the adjusted inventory balance.

A) An employee profit-sharing plan based on net income when a company uses the percentage-of-completion method.

B) The inventory balance as a result of a change in the inventory valuation method.

C) An impairment adjustment resulting from applying the lower-of-cost-or-market-test to the adjusted inventory balance.

D) Deferred income tax effects of an impairment adjustment resulting from applying the lower-of-cost-or-market test to the adjusted inventory balance.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

27

Stone Company changed its method of pricing inventories from FIFO to LIFO. What type of accounting change does this represent?

A) A change in accounting estimate for which the financial statements for prior periods included for comparative purposes should be presented as previously reported.

B) A change in accounting principle for which the financial statements for prior periods included for comparative purposes should be presented as previously reported.

C) A change in accounting estimate for which the financial statements for prior periods included for comparative purposes should be restated.

D) A change in accounting principle for which the financial statements for prior periods included for comparative purposes should be restated.

A) A change in accounting estimate for which the financial statements for prior periods included for comparative purposes should be presented as previously reported.

B) A change in accounting principle for which the financial statements for prior periods included for comparative purposes should be presented as previously reported.

C) A change in accounting estimate for which the financial statements for prior periods included for comparative purposes should be restated.

D) A change in accounting principle for which the financial statements for prior periods included for comparative purposes should be restated.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

28

Which of the following is a condition in which retrospective application is not impracticable?

A) The company cannot determine the effects of retrospective application.

B) Retrospective application requires assumptions about management's intent in a prior period.

C) The company has changed auditors.

D) Retrospective application requires significant estimates for a prior period, and the company cannot objectively verify the necessary information to develop these estimates.

A) The company cannot determine the effects of retrospective application.

B) Retrospective application requires assumptions about management's intent in a prior period.

C) The company has changed auditors.

D) Retrospective application requires significant estimates for a prior period, and the company cannot objectively verify the necessary information to develop these estimates.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

29

Which of the following is not a part of applying the current and prospective approach in accounting for a change in an estimate?

A) Report current and future financial statements on a new basis.

B) Restate prior period financial statements.

C) Disclose in the year of change the effect on net income and earnings per share data for that period only.

D) Make no adjustments to current period opening balances for purposes of catch-up.

A) Report current and future financial statements on a new basis.

B) Restate prior period financial statements.

C) Disclose in the year of change the effect on net income and earnings per share data for that period only.

D) Make no adjustments to current period opening balances for purposes of catch-up.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

30

The estimated life of a building that has been depreciated 30 years of an originally estimated life of 50 years has been revised to a remaining life of 10 years. Based on this information, the accountant should

A) continue to depreciate the building over the original 50-year life.

B) depreciate the remaining book value over the remaining life of the asset.

C) adjust accumulated depreciation to its appropriate balance, through net income, based on a 40-year life, and then depreciate the adjusted book value as though the estimated life had always been 40 years.

D) adjust accumulated depreciation to its appropriate balance through retained earnings, based on a 40-year life, and then depreciate the adjusted book value as though the estimated life had always been 40 years.

A) continue to depreciate the building over the original 50-year life.

B) depreciate the remaining book value over the remaining life of the asset.

C) adjust accumulated depreciation to its appropriate balance, through net income, based on a 40-year life, and then depreciate the adjusted book value as though the estimated life had always been 40 years.

D) adjust accumulated depreciation to its appropriate balance through retained earnings, based on a 40-year life, and then depreciate the adjusted book value as though the estimated life had always been 40 years.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

31

Which of the following statements is correct?

A) Changes in accounting principle are always handled in the current or prospective period.

B) Prior statements should be restated for changes in accounting estimates.

C) A change from expensing certain costs to capitalizing these costs due to a change in the period benefited, should be handled as a change in accounting estimate.

D) Correction of an error related to a prior period should be considered as an adjustment to current year net income.

A) Changes in accounting principle are always handled in the current or prospective period.

B) Prior statements should be restated for changes in accounting estimates.

C) A change from expensing certain costs to capitalizing these costs due to a change in the period benefited, should be handled as a change in accounting estimate.

D) Correction of an error related to a prior period should be considered as an adjustment to current year net income.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

32

In computing earnings per share, the equivalent number of shares of convertible preferred stock are added as an adjustment to the denominator (number of shares outstanding). If the preferred stock is cumulative, which amount should then be added as an adjustment to the numerator (net earnings)?

A) Annual preferred dividend

B) Annual preferred dividend times (one minus the income tax rate)

C) Annual preferred dividend times the income tax rate

D) Annual preferred dividend divided by the income tax rate

A) Annual preferred dividend

B) Annual preferred dividend times (one minus the income tax rate)

C) Annual preferred dividend times the income tax rate

D) Annual preferred dividend divided by the income tax rate

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

33

In the diluted earnings per share computation, the treasury stock method is used for options and warrants to reflect assumed reacquisition of common stock at the average market price during the period. If the exercise price of the options or warrants exceeds the average market price, the computation would

A) fairly present diluted earnings per share on a prospective basis.

B) fairly present the maximum potential dilution of diluted earnings per share on a prospective basis.

C) reflect the excess of the number of shares assumed issued over the number of shares assumed reacquired as the potential dilution of earnings per share.

D) be antidilutive.

A) fairly present diluted earnings per share on a prospective basis.

B) fairly present the maximum potential dilution of diluted earnings per share on a prospective basis.

C) reflect the excess of the number of shares assumed issued over the number of shares assumed reacquired as the potential dilution of earnings per share.

D) be antidilutive.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

34

In applying the treasury stock method to determine the dilutive effect of stock options and warrants, the proceeds assumed to be received upon exercise of the options and warrants

A) are used to calculate the number of common shares repurchased at the average market price, when computing diluted earnings per share.

B) are added, net of tax, to the numerator of the calculation for diluted earnings per share.

C) are disregarded in the computation of earnings per share if the exercise price of the options and warrants is less than the ending market price of common stock.

D) none of these.

A) are used to calculate the number of common shares repurchased at the average market price, when computing diluted earnings per share.

B) are added, net of tax, to the numerator of the calculation for diluted earnings per share.

C) are disregarded in the computation of earnings per share if the exercise price of the options and warrants is less than the ending market price of common stock.

D) none of these.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

35

When applying the treasury stock method for diluted earnings per share, the market price of the common stock used for the repurchase is the

A) price at the end of the year.

B) average market price.

C) price at the beginning of the year.

D) none of these.

A) price at the end of the year.

B) average market price.

C) price at the beginning of the year.

D) none of these.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

36

On January 1, 2006, Lynn Corporation acquired equipment at a cost of $600,000. Lynn adopted the double-declining balance method of depreciation for this equipment and had been recording depreciation over an estimated life of eight years, with no residual value. At the beginning of 2009, a decision was made to change to the straight-line method of depreciation for this equipment. Assuming a 30% tax rate, the cumulative effect of this accounting change on beginning retained earnings, net of tax, is

A) $121,875.

B) $0.

C) $78,750.

D) $77,109.

A) $121,875.

B) $0.

C) $78,750.

D) $77,109.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

37

On January 1, 2006, Foley Corporation acquired machinery at a cost of $250,000. Foley adopted the double-declining balance method of depreciation for this machinery and had been recording depreciation over an estimated useful life of ten years, with no residual value. At the beginning of 2009, a decision was made to change to the straight-line method of depreciation for the machinery. The depreciation expense to be recorded for the machinery in 2009 is (round to the nearest dollar)

A) $25,600.

B) $18,286.

C) $22,857.

D) $25,000.

A) $25,600.

B) $18,286.

C) $22,857.

D) $25,000.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

38

On January 1, 2006, Baden Co., purchased a machine (its only depreciable asset) for $300,000. The machine has a five-year life, and no salvage value. Sum-of-the-years'-digits depreciation has been used for financial statement reporting and the elective straight-line method for income tax reporting. Effective January 1, 2009, for financial statement reporting, Baden decided to change to the straight-line method for depreciation of the machine. Assume that Baden can justify the change.

Baden's income before depreciation, before income taxes, and before the cumulative effect of the accounting change (if any), for the year ended December 31, 2009, is $250,000. The income tax rate for 2009, as well as for the years 2006-2008, is 30%. What amount should Baden report as net income for the year ended December 31, 2009?

A) $60,000

B) $91,000

C) $154,000

D) $175,000

Baden's income before depreciation, before income taxes, and before the cumulative effect of the accounting change (if any), for the year ended December 31, 2009, is $250,000. The income tax rate for 2009, as well as for the years 2006-2008, is 30%. What amount should Baden report as net income for the year ended December 31, 2009?

A) $60,000

B) $91,000

C) $154,000

D) $175,000

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

39

During 2008, a construction company changed from the completed-contract method to the percentage-of-completion method for accounting purposes but not for tax purposes. Gross profit figures under both methods for the past three years appear below:

Assuming an income tax rate of 40% for all years, the affect of this accounting change on prior periods should be reported by a credit of

A) $600,000 on the 2008 income statement.

B) $390,000 on the 2008 income statement.

C) $600,000 on the 2008 retained earnings statement.

D) $390,000 on the 2008 retained earnings statement.

Assuming an income tax rate of 40% for all years, the affect of this accounting change on prior periods should be reported by a credit ofA) $600,000 on the 2008 income statement.

B) $390,000 on the 2008 income statement.

C) $600,000 on the 2008 retained earnings statement.

D) $390,000 on the 2008 retained earnings statement.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

40

Weaver Company changes from the LIFO method to the FIFO method in 2009. The increase in pre-tax income as a result of the difference in the two methods prior to 2007 is $100,000, for the year 2007 is $40,000, and for the year 2008 is $30,000. The estimated tax effect is 40%. The entry to record the change at the beginning of 2008 should include

A) debit to Deferred Tax Liability of $68,000.

B) credit to Deferred Tax Liability of $68,000.

C) debit to Deferred Tax Liability of $56,000.

D) credit to Deferred Tax Liability of $56,000.

A) debit to Deferred Tax Liability of $68,000.

B) credit to Deferred Tax Liability of $68,000.

C) debit to Deferred Tax Liability of $56,000.

D) credit to Deferred Tax Liability of $56,000.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

41

In 2008, Flynn Company has changed from the percentage-of-completion method to the completed-contract method for long-term construction contracts. The difference in pre-tax income prior to 2008 is a decrease of $60,000 and for 2008 is a decrease of $20,000. The estimated tax effect is 40%. The journal entry made by Flynn Company should include a

A) debit to Deferred Tax Liability of $24,000.

B) credit to Deferred Tax Liability of $32,000.

C) debit to Deferred Tax Liability of $32,000.

D) credit to Deferred Tax Liability of $24,000.

A) debit to Deferred Tax Liability of $24,000.

B) credit to Deferred Tax Liability of $32,000.

C) debit to Deferred Tax Liability of $32,000.

D) credit to Deferred Tax Liability of $24,000.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

42

Eaton Company began operations on January 1, 2008, and uses the FIFO method in costing its raw materials inventory. Management is contemplating a change to the LIFO method and is interested in determining what effect such a change will have on net income. Accordingly, the following information has been developed:

Based on the above information, a change to the LIFO method in 2009 would result in net income for 2009 of

A) $1,120,000.

B) $1,080,000.

C) $1,004,000.

D) $1,000,000.

Based on the above information, a change to the LIFO method in 2009 would result in net income for 2009 ofA) $1,120,000.

B) $1,080,000.

C) $1,004,000.

D) $1,000,000.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

43

Hannah Company began operations on January 1, 2008, and uses the FIFO method in costing its raw materials inventory. Management is contemplating a change to the LIFO method and is interested in determining what effect such a change will have on net income. Accordingly, the following information has been developed:

Based upon the above information, a change to the LIFO method in 2009 would result in net income for 2009 of

A) $540,000.

B) $600,000.

C) $620,000.

D) $660,000.

Based upon the above information, a change to the LIFO method in 2009 would result in net income for 2009 ofA) $540,000.

B) $600,000.

C) $620,000.

D) $660,000.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

44

Equipment was purchased at the beginning of 2006 for $204,000. At the time of its purchase, the equipment was estimated to have a useful life of six years and a salvage value of $24,000. The equipment was depreciated using the straight-line method of depreciation through 2009. At the beginning of 2009, the estimate of useful life was revised to a total life of eight years and the expected salvage value was changed to $15,000. The amount to be recorded for depreciation for 2009, reflecting these changes in estimates, is

A) $12,375.

B) $19,800.

C) $22,800.

D) $23,625.

A) $12,375.

B) $19,800.

C) $22,800.

D) $23,625.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

45

Carey Company purchased a machine on January 1, 2006, for $300,000. At the date of acquisition, the machine had an estimated useful life of six years with no salvage. The machine is being depreciated on a straight-line basis. On January 1, 2009, Carey determined, as a result of additional information, that the machine had an estimated useful life of eight years from the date of acquisition with no salvage. An accounting change was made in 2009 to reflect this additional information.

-Assume that the direct effects of this change are limited to the effect on depreciation and the related tax provision, and that the income tax rate was 30% in 2006, 2007, 2008, and 2009. What should be reported in Carey's income statement for the year ended December 31, 2009, as the cumulative effect on prior years of changing the estimated useful life of the machine?

A) $0

B) $20,000

C) $30,000

D) $105,000

-Assume that the direct effects of this change are limited to the effect on depreciation and the related tax provision, and that the income tax rate was 30% in 2006, 2007, 2008, and 2009. What should be reported in Carey's income statement for the year ended December 31, 2009, as the cumulative effect on prior years of changing the estimated useful life of the machine?

A) $0

B) $20,000

C) $30,000

D) $105,000

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

46

Handy Company purchased equipment that cost $750,000 on January 1, 2006. The entire cost was recorded as an expense. The equipment had a nine-year life and a $30,000 residual value. Handy uses the straight-line method to account for depreciation expense. The error was discovered on December 10, 2008. Handy is subject to a 40% tax rate.

-Handy's net income for the year ended December 31, 2006, was understated by

A) $402,000.

B) $450,000.

C) $670,000.

D) $750,000.

-Handy's net income for the year ended December 31, 2006, was understated by

A) $402,000.

B) $450,000.

C) $670,000.

D) $750,000.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

47

At December 31, 2008, Norbett Company had 500,000 shares of common stock issued and outstanding, 400,000 of which had been issued and outstanding throughout the year and 100,000 of which were issued on October 1, 2008. Net income for the year ended December 31, 2008, was $1,020,000. What should be Norbett's 2008 earnings per common share, rounded to the nearest penny?

A) $2.02

B) $2.55

C) $2.40

D) $2.27

A) $2.02

B) $2.55

C) $2.40

D) $2.27

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

48

On January 1, 2008, Dingler Corporation had 125,000 shares of its $2 par value common stock outstanding. On March 1, Dingler sold an additional 250,000 shares on the open market at $20 per share. Dingler issued a 20% stock dividend on May 1. On August 1, Dingler purchased 140,000 shares and immediately retired the stock. On November 1, 200,000 shares were sold for $25 per share. What is the weighted-average number of shares outstanding for 2008?

A) 510,000

B) 375,000

C) 358,333

D) 258,333

A) 510,000

B) 375,000

C) 358,333

D) 258,333

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

49

The following information is available for Alley Corporation:

The number of shares to be used in computing earnings per common share for 2008 is

A) 2,825,500.

B) 2,737,500.

C) 2,725,000.

D) 1,706,250.

The number of shares to be used in computing earnings per common share for 2008 isA) 2,825,500.

B) 2,737,500.

C) 2,725,000.

D) 1,706,250.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

50

Caruso Company had 500,000 shares of common stock issued and outstanding at December 31, 2007. On July 1, 2008, an additional 500,000 shares were issued for cash. Caruso also had stock options outstanding at the beginning and end of 2008 which allow the holders to purchase 150,000 shares of common stock at $20 per share. The average market price of Caruso's common stock was $25 during 2008. What is the number of shares that should be used in computing diluted earnings per share for the year ended December 31, 2008?

A) 1,030,000

B) 870,000

C) 787,500

D) 780,000

A) 1,030,000

B) 870,000

C) 787,500

D) 780,000

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

51

Hoffman Corporation had net income for the year of $480,000 and a weighted-average number of common shares outstanding during the period of 200,000 shares. The company has a convertible bond issue outstanding. The bonds were issued four years ago at par ($2,000,000), carry a 7% interest rate, and are convertible into 40,000 shares of common stock. The company has a 40% tax rate. Diluted earnings per share are

A) $1.65.

B) $2.23.

C) $2.35.

D) $2.58.

A) $1.65.

B) $2.23.

C) $2.35.

D) $2.58.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

52

On January 2, 2008, Ramos Co. issued at par $10,000 of 6% bonds convertible in total into 1,000 shares of Ramos's common stock. No bonds were converted during 2008. Throughout 2008, Ramos had 1,000 shares of common stock outstanding. Ramos's 2008 net income was $3,000, and its income tax rate is 30%. No potentially dilutive securities other than the convertible bonds were outstanding during 2008. Ramos's diluted earnings per share for 2008 would be (rounded to the nearest penny)

A) $1.50.

B) $1.71.

C) $1.80.

D) $3.42.

A) $1.50.

B) $1.71.

C) $1.80.

D) $3.42.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

53

At December 31, 2007, Pratt Company had 500,000 shares of common stock outstanding. On October 1, 2008, an additional 100,000 shares of common stock were issued. In addition, Pratt had $10,000,000 of 6% convertible bonds outstanding at December 31, 2007, which are convertible into 225,000 shares of common stock. No bonds were converted into common stock in 2008. The net income for the year ended December 31, 2008, was $3,000,000. Assuming the income tax rate was 30%, the diluted earnings per share for the year ended December 31, 2008, should be (rounded to the nearest penny)

A) $6.52.

B) $4.80.

C) $4.56.

D) $4.00.

A) $6.52.

B) $4.80.

C) $4.56.

D) $4.00.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

54

On January 2, 2008, Dino Co. issued at par $300,000 of 9% convertible bonds. Each $1,000 bond is convertible into 30 shares. No bonds were converted during 2008. Dino had 50,000 shares of common stock outstanding during 2008. Dino's 2008 net income was $160,000 and the income tax rate was 30%. Dino's diluted earnings per share for 2008 would be (rounded to the nearest penny)

A) $2.71.

B) $3.03.

C) $3.20.

D) $3.58.

A) $2.71.

B) $3.03.

C) $3.20.

D) $3.58.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

55

At December 31, 2007, Kegan Co. had 1,200,000 shares of common stock outstanding. In addition, Kegan had 450,000 shares of preferred stock which were convertible into 750,000 shares of common stock. During 2008, Kegan paid $600,000 cash dividends on the common stock and $400,000 cash dividends on the preferred stock. Net income for 2008 was $3,400,000 and the income tax rate was 40%. The diluted earnings per share for 2008 is (rounded to the nearest penny)

A) $1.24.

B) $1.74.

C) $2.51.

D) $2.84.

A) $1.24.

B) $1.74.

C) $2.51.

D) $2.84.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

56

Werth, Incorporated, has 3,200,000 shares of common stock outstanding on December 31, 2007. An additional 800,000 shares of common stock were issued on April 1, 2008, and 400,000 more on July 1, 2008. On October 1, 2008, Werth issued 20,000, $1,000 face value, 8% convertible bonds. Each bond is convertible into 20 shares of common stock. No bonds were converted into common stock in 2008. What is the number of shares to be used in computing basic earnings per share and diluted earnings per share, respectively?

A) 4,000,000 and 4,000,000

B) 4,000,000 and 4,100,000

C) 4,000,000 and 4,400,000

D) 4,400,000 and 5,200,000

A) 4,000,000 and 4,000,000

B) 4,000,000 and 4,100,000

C) 4,000,000 and 4,400,000

D) 4,400,000 and 5,200,000

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

57

Lemke Co. has 4,000,000 shares of common stock outstanding on December 31, 2007. An additional 200,000 shares are issued on April 1, 2008, and 480,000 more on September 1. On October 1, Lemke issued $6,000,000 of 9% convertible bonds. Each $1,000 bond is convertible into 40 shares of common stock. No bonds have been converted. The number of shares to be used in computing basic earnings per share and diluted earnings per share on December 31, 2008 is

A) 4,310,000 and 4,310,000.

B) 4,310,000 and 4,370,000.

C) 4,310,000 and 4,550,000.

D) 5,080,000 and 5,320,000.

A) 4,310,000 and 4,310,000.

B) 4,310,000 and 4,370,000.

C) 4,310,000 and 4,550,000.

D) 5,080,000 and 5,320,000.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

58

At December 31, 2007, Quirk Company had 2,000,000 shares of common stock outstanding. On January 1, 2008, Quirk issued 500,000 shares of preferred stock which were convertible into 1,000,000 shares of common stock. During 2008, Quirk declared and paid $1,500,000 cash dividends on the common stock and $500,000 cash dividends on the preferred stock. Net income for the year ended December 31, 2008, was $5,000,000. Assuming an income tax rate of 30%, what should be diluted earnings per share for the year ended December 31, 2008? (Round to the nearest penny.)

A) $1.50

B) $1.67

C) $2.50

D) $2.08

A) $1.50

B) $1.67

C) $2.50

D) $2.08

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

59

Colaw Company had 300,000 shares of common stock issued and outstanding at December 31, 2007. During 2008, no additional common stock was issued. On January 1, 2008, Colaw issued 400,000 shares of nonconvertible preferred stock. During 2008, Colaw declared and paid $180,000 cash dividends on the common stock and $150,000 on the nonconvertible preferred stock. Net income for the year ended December 31, 2008, was $960,000. What should be Colaw's 2008 earnings per common share, rounded to the nearest penny?

A) $1.16

B) $2.10

C) $2.70

D) $3.20

A) $1.16

B) $2.10

C) $2.70

D) $3.20

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

60

At December 31, 2007, Agler Company had 1,200,000 shares of common stock outstanding. On September 1, 2008, an additional 400,000 shares of common stock were issued. In addition, Agler had $12,000,000 of 6% convertible bonds outstanding at December 31, 2007, which are convertible into 800,000 shares of common stock. No bonds were converted into common stock in 2008. The net income for the year ended December 31, 2008, was $4,500,000. Assuming the income tax rate was 30%, what should be the diluted earnings per share for the year ended December 31, 2008, rounded to the nearest penny?

A) $2.11

B) $3.38

C) $2.35

D) $2.45

A) $2.11

B) $3.38

C) $2.35

D) $2.45

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

61

Foley Company has 1,800,000 shares of common stock outstanding on December 31, 2007. An additional 150,000 shares of common stock were issued on July 1, 2008, and 300,000 more on October 1, 2008. On April 1, 2008, Foley issued 6,000, $1,000 face value, 8% convertible bonds. Each bond is convertible into 40 shares of common stock. No bonds were converted into common stock in 2008. What is the number of shares to be used in computing basic earnings per share and diluted earnings per share, respectively, for the year ended December 31, 2008?

A) 1,950,000 and 2,130,000

B) 1,950,000 and 1,950,000

C) 1,950,000 and 2,190,000

D) 2,250,000 and 2,430,000

A) 1,950,000 and 2,130,000

B) 1,950,000 and 1,950,000

C) 1,950,000 and 2,190,000

D) 2,250,000 and 2,430,000

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

62

Ferry Corporation had 300,000 shares of common stock outstanding at December 31, 2008. In addition, it had 90,000 stock options outstanding, which had been granted to certain executives, and which gave them the right to purchase shares of Ferry's stock at an option price of $37 per share. The average market price of Ferry's common stock for 2008 was $50. What is the number of shares that should be used in computing diluted earnings per share for the year ended December 31, 2008?

A) 300,000

B) 331,622

C) 366,600

D) 323,400

A) 300,000

B) 331,622

C) 366,600

D) 323,400

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

63

On December 31, 2008, Ellworth, Inc. appropriately changed its inventory valuation method to FIFO cost from weighted-average cost for financial statement and income tax purposes. The change will result in a $1,500,000 increase in the beginning inventory at January 1, 2008. Assume a 30% income tax rate. The cumulative effect of this accounting change on beginning retained earnings is

A) $0.

B) $450,000.

C) $1,050,000.

D) $1,500,000.

A) $0.

B) $450,000.

C) $1,050,000.

D) $1,500,000.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

64

On January 1, 2008, Bosco Corp. changed its inventory method to FIFO from LIFO for both financial and income tax reporting purposes. The change resulted in an $800,000 increase in the January 1, 2008 inventory. Assume that the income tax rate for all years is 30%. The cumulative effect of the accounting change should be reported by Bosco in its 2008

A) retained earnings statement as a $560,000 addition to the beginning balance.

B) income statement as a $560,000 cumulative effect of accounting change.

C) retained earnings statement as an $800,000 addition to the beginning balance.

D) income statement as an $800,000 cumulative effect of accounting change.

A) retained earnings statement as a $560,000 addition to the beginning balance.

B) income statement as a $560,000 cumulative effect of accounting change.

C) retained earnings statement as an $800,000 addition to the beginning balance.

D) income statement as an $800,000 cumulative effect of accounting change.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

65

On January 1, 2005, Dent Co. purchased a machine for $792,000 and depreciated it by the straight-line method using an estimated useful life of eight years with no salvage value. On January 1, 2008, Dent determined that the machine had a useful life of six years from the date of acquisition and will have a salvage value of $72,000. An accounting change was made in 2008 to reflect these additional data. The accumulated depreciation for this machine should have a balance at December 31, 2008 of

A) $438,000.

B) $462,000.

C) $480,000.

D) $528,000.

A) $438,000.

B) $462,000.

C) $480,000.

D) $528,000.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

66

On January 1, 2005, Neer Co. purchased a patent for $595,000. The patent is being amortized over its remaining legal life of 15 years expiring on January 1, 2020. During 2008, Neer determined that the economic benefits of the patent would not last longer than ten years from the date of acquisition. What amount should be reported in the balance sheet for the patent, net of accumulated amortization, at December 31, 2008?

A) $357,000

B) $408,000

C) $420,000

D) $436,375

A) $357,000

B) $408,000

C) $420,000

D) $436,375

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

67

On January 1, 2007, Gregg Corp. acquired a machine at a cost of $500,000. It is to be depreciated on the straight-line method over a five-year period with no residual value. Because of a bookkeeping error, no depreciation was recognized in Gregg's 2007 financial statements. The oversight was discovered during the preparation of Gregg's 2008 financial statements. Depreciation expense on this machine for 2008 should be

A) $0.

B) $100,000.

C) $125,000.

D) $200,000.

A) $0.

B) $100,000.

C) $125,000.

D) $200,000.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

68

Peine Co. had 300,000 shares of common stock issued and outstanding at December 31, 2007. No common stock was issued during 2007. On January 1, 2008, Peine issued 200,000 shares of nonconvertible preferred stock. During 2008, Peine declared and paid $100,000 cash dividends on the common stock and $80,000 on the preferred stock. Net income for the year ended December 31, 2008 was $620,000. What should be Peine's 2008 earnings per common share?

A) $2.07

B) $1.80

C) $1.73

D) $1.47

A) $2.07

B) $1.80

C) $1.73

D) $1.47

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

69

Royce Co. had 2,400,000 shares of common stock outstanding on January 1 and December 31, 2007. In connection with the acquisition of a subsidiary company in June 2006, Royce is required to issue 100,000 additional shares of its common stock on July 1, 2008, to the former owners of the subsidiary. Royce paid $200,000 in preferred stock dividends in 2007, and reported net income of $3,400,000 for the year. Royce's diluted earnings per share for 2007 should be

A) $1.42.

B) $1.36.

C) $1.33.

D) $1.28.

A) $1.42.

B) $1.36.

C) $1.33.

D) $1.28.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

70

Eller, Inc., had 560,000 shares of common stock issued and outstanding at December 31, 2006. On July 1, 2007, an additional 40,000 shares of common stock were issued for cash. Eller also had unexercised stock options to purchase 32,000 shares of common stock at $15 per share outstanding at the beginning and end of 2007. The average market price of Eller's common stock was $20 during 2007. What is the number of shares that should be used in computing diluted earnings per share for the year ended December 31, 2007?

A) 580,000

B) 588,000

C) 608,000

D) 612,000

A) 580,000

B) 588,000

C) 608,000

D) 612,000

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 70 flashcards in this deck.