Deck 10: Consolidated Financial Statements: Special Problems

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Changes in a parent company's Investment in Common Stock of Subsidiary ledger account and in minority interest in net assets of subsidiary resulting from the subsidiary's issuance of common stock to the public at net proceeds per share in excess of the per-share carrying amount of the parent company's investment generally are as follows:

A)

B)

C)

D)

A)

B)

C)

D)

Question

Question

Question

Question

Question

The end-of-period journal entries of Pillard Corporation included the following (explanation omitted):

The probable explanation for the journal entry is:

The probable explanation for the journal entry is:

A) To accrue cumulative preferred dividend passed by subsidiary's board of directors

B) To record share of subsidiary's net income applicable to preferred stock

C) To apply provisions of the participation clause of preferred stock to the subsidiary's net income

D) Some other explanation

The probable explanation for the journal entry is:A) To accrue cumulative preferred dividend passed by subsidiary's board of directors

B) To record share of subsidiary's net income applicable to preferred stock

C) To apply provisions of the participation clause of preferred stock to the subsidiary's net income

D) Some other explanation

Question

Question

Question

On October 31, 2006, Palomar Corporation prepared the following journal entry (explanation, omitted) regarding its investment in its partially owned subsidiary, San Diego Company: If no accompanying journal entry was prepared by Palomar, the most likely cause of the foregoing journal entry was:

A) San Diego issued additional shares of common stock to the public at a price per share less than the per-share carrying amount of Palomar's investment in San Diego

B) Palomar disposed of some of its investment in San Diego at a price per share less than the per-share carrying amount of Palomar's investment in San Diego

C) San Diego issued additional shares of common stock to Palomar at a price per share greater than the per-share carrying amount of Palomar's earlier investment in San Diego

D) Some other transaction or event

A) San Diego issued additional shares of common stock to the public at a price per share less than the per-share carrying amount of Palomar's investment in San Diego

B) Palomar disposed of some of its investment in San Diego at a price per share less than the per-share carrying amount of Palomar's investment in San Diego

C) San Diego issued additional shares of common stock to Palomar at a price per share greater than the per-share carrying amount of Palomar's earlier investment in San Diego

D) Some other transaction or event

Question

Question

Question

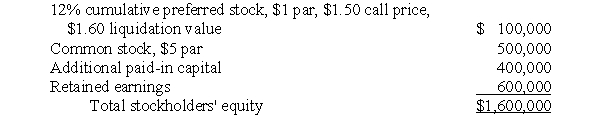

The stockholders' equity of Sidding Company on September 30, 2006, the end of a fiscal year, was as follows:

Sidding had no cumulative preferred dividends in arrears. The current fair values of Sidding's identifiable net assets equaled their carrying amounts on September 30, 2006.

Sidding had no cumulative preferred dividends in arrears. The current fair values of Sidding's identifiable net assets equaled their carrying amounts on September 30, 2006.

On October 1, 2006, Preen Corporation paid $1,400,000 for 70,000 shares of Sidding's outstanding preferred stock and 80,000 shares of Sidding's outstanding common stock. Out-of-pocket costs of the business combination may be disregarded.

a. Prepare a journal entry on October 1, 2006, to record Preen Corporation's business combination with Sidding Company. Omit explanation and disregard income taxes.

b. Prepare a working paper elimination (in journal entry format) for Preen Corporation and subsidiary on October 1, 2006. Omit explanation and disregard income taxes.

Sidding had no cumulative preferred dividends in arrears. The current fair values of Sidding's identifiable net assets equaled their carrying amounts on September 30, 2006.On October 1, 2006, Preen Corporation paid $1,400,000 for 70,000 shares of Sidding's outstanding preferred stock and 80,000 shares of Sidding's outstanding common stock. Out-of-pocket costs of the business combination may be disregarded.

a. Prepare a journal entry on October 1, 2006, to record Preen Corporation's business combination with Sidding Company. Omit explanation and disregard income taxes.

b. Prepare a working paper elimination (in journal entry format) for Preen Corporation and subsidiary on October 1, 2006. Omit explanation and disregard income taxes.

Question

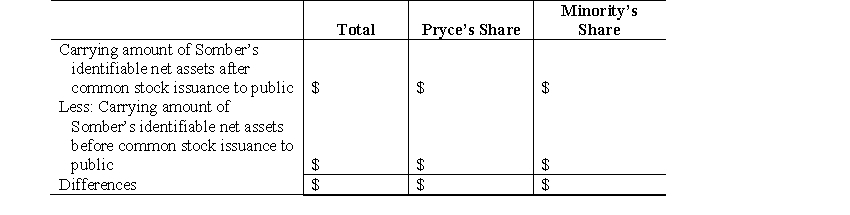

Pryce Corporation owns 8,000 of the 10,000 shares of outstanding common stock of Somber Company. On July 31, 2006, the end of a fiscal year, the stockholders' equity of Somber was $800,000, and the balance of Pryce's Investment in Somber Company Common Stock ledger account was $678,000, of which $38,000 was attributable to unimpaired goodwill. The current fair values of Somber's identifiable net assets had equaled their carrying amounts on the date of the Pryce-Somber business combination.

On August 1, 2006, Somber issued 2,000 shares of common stock to the public at $110 a share, net of out-of-pocket costs of issuing the stock. Both Pryce and Somber's minority stockholders waived their preemptive right.

Prepare a working paper to compute the nonoperating gain or loss to Pryce Corporation resulting from Somber Company's issuance of common stock to the public. Use the following format:

On August 1, 2006, Somber issued 2,000 shares of common stock to the public at $110 a share, net of out-of-pocket costs of issuing the stock. Both Pryce and Somber's minority stockholders waived their preemptive right.

Prepare a working paper to compute the nonoperating gain or loss to Pryce Corporation resulting from Somber Company's issuance of common stock to the public. Use the following format:

Question

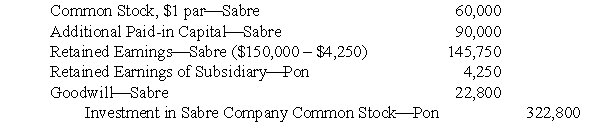

The first working paper elimination (in journal entry format) for Pon Corporation and subsidiary on May 31, 2006, the end of a fiscal year, was as follows (explanation omitted):

EOn June 1, 2006, when the current fair value of its $1 par common stock was $8 a share, Sabre declared a 15% common stock dividend, to be issued June 15, 2006. Sabre prepared the following journal entry (explanation omitted) for the dividend:

EOn June 1, 2006, when the current fair value of its $1 par common stock was $8 a share, Sabre declared a 15% common stock dividend, to be issued June 15, 2006. Sabre prepared the following journal entry (explanation omitted) for the dividend:

Prepare a working paper elimination (in journal entry format) for Pon Corporation and subsidiary on June 1, 2006. Omit explanation and disregard income taxes.

Prepare a working paper elimination (in journal entry format) for Pon Corporation and subsidiary on June 1, 2006. Omit explanation and disregard income taxes.

EOn June 1, 2006, when the current fair value of its $1 par common stock was $8 a share, Sabre declared a 15% common stock dividend, to be issued June 15, 2006. Sabre prepared the following journal entry (explanation omitted) for the dividend: Prepare a working paper elimination (in journal entry format) for Pon Corporation and subsidiary on June 1, 2006. Omit explanation and disregard income taxes. Question

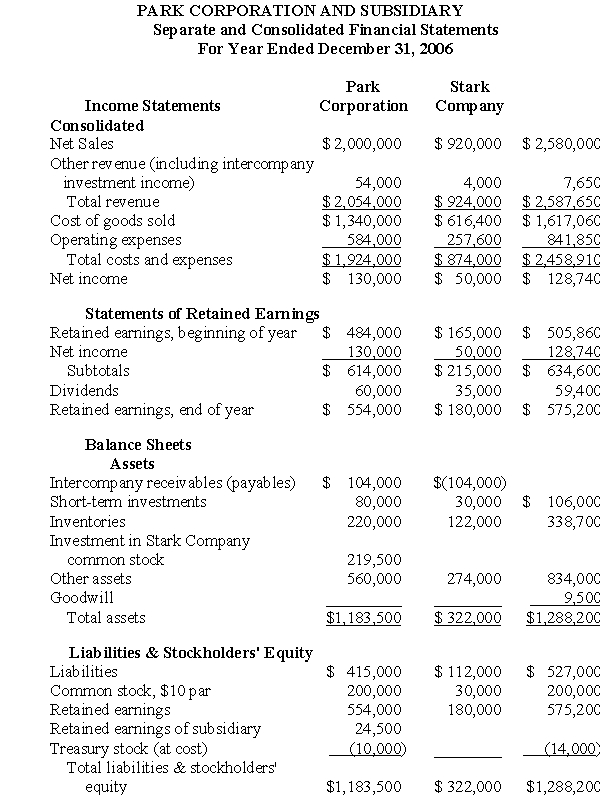

Separate and consolidated financial statements of Park Corporation and its subsidiary, Stark Company, for the fiscal year ended December 31, 2006, are shown below. Park used the equity method of accounting for its investment in Stark, but neither enterprise used separate ledger accounts for intercompany revenue, expenses, gains, or losses.

Additional Information :

Additional Information :

1. All of Stark's identifiable net assets were fairly stated at their carrying amounts on the date Park combined with Stark. The $10,000 excess of Park's investment in Stark over the current fair values (and carrying amounts) of Stark's identifiable net assets was allocated to goodwill, which was unimpaired on December 31, 2006.

2. Park sold merchandise to Stark at the same markup that Park realized on sales to its other customers.

3. Stark had acquired shares of Park's outstanding common stock on December 31, 2005. These shares were included in Stark's short-term investments.

4. Park acquired shares of its common stock for the treasury late in 2006 after the fourth-quarter dividend had been declared and paid.

From the foregoing information, provide answers for the following:

a. Percentage of Stark Company outstanding common stock owned by Park Corporation _______%

b. Intercompany sales by Park to Stark $________

c. Intercompany cost of goods sold eliminated $________

d. Intercompany investment income recognized by Park under the equity method of accounting $________

e. Amount of dividends received by Stark from Park and eliminated from other revenue $________

f. Amount of intercompany profit eliminated from ending inventories of Stark $_________

g. Number of shares of Park's common stock owned by Stark ________ shares

h. Carrying amount of Park common stock owned by Stark $________

Additional Information :1. All of Stark's identifiable net assets were fairly stated at their carrying amounts on the date Park combined with Stark. The $10,000 excess of Park's investment in Stark over the current fair values (and carrying amounts) of Stark's identifiable net assets was allocated to goodwill, which was unimpaired on December 31, 2006.

2. Park sold merchandise to Stark at the same markup that Park realized on sales to its other customers.

3. Stark had acquired shares of Park's outstanding common stock on December 31, 2005. These shares were included in Stark's short-term investments.

4. Park acquired shares of its common stock for the treasury late in 2006 after the fourth-quarter dividend had been declared and paid.

From the foregoing information, provide answers for the following:

a. Percentage of Stark Company outstanding common stock owned by Park Corporation _______%

b. Intercompany sales by Park to Stark $________

c. Intercompany cost of goods sold eliminated $________

d. Intercompany investment income recognized by Park under the equity method of accounting $________

e. Amount of dividends received by Stark from Park and eliminated from other revenue $________

f. Amount of intercompany profit eliminated from ending inventories of Stark $_________

g. Number of shares of Park's common stock owned by Stark ________ shares

h. Carrying amount of Park common stock owned by Stark $________

Question

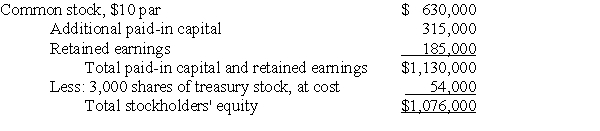

The stockholders' equity of Sprague Company on August 31, 2006, was as follows:

On August 31, 2006, Pommel Corporation paid $900,000 cash, including direct out-of-pocket costs of the business combination, for 48,000 shares of Sprague's outstanding common stock. The current fair values of Sprague's identifiable net assets were equal to their carrying amounts on August 31, 2006.

On August 31, 2006, Pommel Corporation paid $900,000 cash, including direct out-of-pocket costs of the business combination, for 48,000 shares of Sprague's outstanding common stock. The current fair values of Sprague's identifiable net assets were equal to their carrying amounts on August 31, 2006.

Prepare working paper eliminations (in journal entry format) for Pommel Corporation and subsidiary on August 31, 2006. Omit explanations and disregard income taxes.

On August 31, 2006, Pommel Corporation paid $900,000 cash, including direct out-of-pocket costs of the business combination, for 48,000 shares of Sprague's outstanding common stock. The current fair values of Sprague's identifiable net assets were equal to their carrying amounts on August 31, 2006.Prepare working paper eliminations (in journal entry format) for Pommel Corporation and subsidiary on August 31, 2006. Omit explanations and disregard income taxes.

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/29

Play

Full screen (f)

Deck 10: Consolidated Financial Statements: Special Problems

1

If less than 100% of a subsidiary's preferred stock is acquired by the parent company in their business combination, the preferences associated with the preferred stock must be considered in the measurement of goodwill acquired by the parent company in the business combination.

False

2

Application of mathematical allocations for reciprocal shareholdings of common stock violates the going-concern principle for consolidated financial statements.

True

3

A nonoperating loss to the parent company resulting from the subsidiary's issuance of additional shares of common stock to the public is debited to the Retained Earnings ledger account of the parent company.

False

4

Treasury stock of a subsidiary on the date of a business combination is displayed as treasury stock in the consolidated balance sheet.

Unlock Deck

Unlock for access to all 29 flashcards in this deck.

Unlock Deck

k this deck

5

If a parent company owns 20% of the outstanding cumulative preferred stock of its subsidiary, 80% of the preferred stockholders' equity (aggregate call price plus any dividends in arrears) is included in minority interest in net assets of subsidiary in the consolidated balance sheet.

Unlock Deck

Unlock for access to all 29 flashcards in this deck.

Unlock Deck

k this deck

6

If the parent company issues its common stock to acquire the minority interest in a subsidiary, the transaction is recorded under purchase accounting.

Unlock Deck

Unlock for access to all 29 flashcards in this deck.

Unlock Deck

k this deck

7

The gain or loss resulting from the parent company's disposal of a portion of its investment in a subsidiary is included in income before extraordinary items in the consolidated income statement for the accounting period of the disposal.

Unlock Deck

Unlock for access to all 29 flashcards in this deck.

Unlock Deck

k this deck

8

A parent company uses the equity method of accounting for passed dividends on the subsidiary's outstanding cumulative preferred stock owned by the parent.

Unlock Deck

Unlock for access to all 29 flashcards in this deck.

Unlock Deck

k this deck

9

A subsidiary's declaration and distribution of a stock dividend has no effect on the Investment in Subsidiary Common Stock ledger account of a parent company that uses the equity method of accounting for the subsidiary's operations.

Unlock Deck

Unlock for access to all 29 flashcards in this deck.

Unlock Deck

k this deck

10

A subsidiary's holdings of the parent company's common stock in substance are treasury stock of the consolidated entity.

Unlock Deck

Unlock for access to all 29 flashcards in this deck.

Unlock Deck

k this deck

11

A subsidiary's acquisition of shares of stock from minority stockholders, to be carried as treasury stock, may result in the recognition of goodwill by the subsidiary.

Unlock Deck

Unlock for access to all 29 flashcards in this deck.

Unlock Deck

k this deck

12

If Pol Corporation owns 25% of the outstanding common stock of Sel Company and 90% of the outstanding common stock of Slu Company, which in turn owns 40% of Sel's outstanding common stock, the financial statements of Slu and Sel must be consolidated before the financial statements of Pol and Slu are consolidated.

Unlock Deck

Unlock for access to all 29 flashcards in this deck.

Unlock Deck

k this deck

13

Changes in a parent company's Investment in Common Stock of Subsidiary ledger account and in minority interest in net assets of subsidiary resulting from the subsidiary's issuance of common stock to the public at net proceeds per share in excess of the per-share carrying amount of the parent company's investment generally are as follows:

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 29 flashcards in this deck.

Unlock Deck

k this deck

14

Palp Corporation had 300,000 shares of common stock outstanding. It owned 75% of the outstanding common stock of Shill Company. Shill owned 20,000 shares of Palp's outstanding common stock. In the consolidated balance sheet of Palp Corporation and subsidiary, Palp's common stock is reported as:

A) 280,000 shares issued and outstanding

B) 300,000 shares issued less 20,000 shares of treasury stock; 280,000 shares outstanding

C) 300,000 shares issued and outstanding

D) 300,000 shares issued, with a note to the financial statements disclosing that Shill owns 20,000 shares

E) None of the foregoing

A) 280,000 shares issued and outstanding

B) 300,000 shares issued less 20,000 shares of treasury stock; 280,000 shares outstanding

C) 300,000 shares issued and outstanding

D) 300,000 shares issued, with a note to the financial statements disclosing that Shill owns 20,000 shares

E) None of the foregoing

Unlock Deck

Unlock for access to all 29 flashcards in this deck.

Unlock Deck

k this deck

15

Philo Corporation issued common stock in exchange for 90% of the outstanding common stock of Stype Company in a business combination. If Philo later issued common stock with a par of $1,000 and a current fair value of $100,000 for the remaining 10% of Stype's outstanding common stock, which had a stated value of $5,000, Philo's consolidated assets would increase by:

A) $100,000

B) $5,000

C) $1,000

D) $0

E) Some other amount

A) $100,000

B) $5,000

C) $1,000

D) $0

E) Some other amount

Unlock Deck

Unlock for access to all 29 flashcards in this deck.

Unlock Deck

k this deck

16

A subsidiary's issuance of additional common stock to outsiders results in:

A) A gain to the parent company if the net proceeds per share exceed the per-share carrying amount of the parent's Investment in Subsidiary Common Stock ledger account prior to the subsidiary's stock issuance

B) An increase in subsidiary goodwill acquired by the parent company

C) A decrease in the balance of the parent company's Investment in Subsidiary Common Stock ledger account in all cases

D) A decrease in consolidated retained earnings

A) A gain to the parent company if the net proceeds per share exceed the per-share carrying amount of the parent's Investment in Subsidiary Common Stock ledger account prior to the subsidiary's stock issuance

B) An increase in subsidiary goodwill acquired by the parent company

C) A decrease in the balance of the parent company's Investment in Subsidiary Common Stock ledger account in all cases

D) A decrease in consolidated retained earnings

Unlock Deck

Unlock for access to all 29 flashcards in this deck.

Unlock Deck

k this deck

17

If a parent company acquires a majority of the outstanding preferred stock and common stock of a subsidiary, the amount of goodwill acquired by the parent in the business combination is measured by the cost of the parent's investment assigned to:

A) The preferred stock acquired only

B) The common stock acquired only

C) Both the preferred stock and the common stock acquired

D) Neither the preferred stock nor the common stock acquired

A) The preferred stock acquired only

B) The common stock acquired only

C) Both the preferred stock and the common stock acquired

D) Neither the preferred stock nor the common stock acquired

Unlock Deck

Unlock for access to all 29 flashcards in this deck.

Unlock Deck

k this deck

18

The end-of-period journal entries of Pillard Corporation included the following (explanation omitted):

The probable explanation for the journal entry is:

A) To accrue cumulative preferred dividend passed by subsidiary's board of directors

B) To record share of subsidiary's net income applicable to preferred stock

C) To apply provisions of the participation clause of preferred stock to the subsidiary's net income

D) Some other explanation

The probable explanation for the journal entry is:A) To accrue cumulative preferred dividend passed by subsidiary's board of directors

B) To record share of subsidiary's net income applicable to preferred stock

C) To apply provisions of the participation clause of preferred stock to the subsidiary's net income

D) Some other explanation

Unlock Deck

Unlock for access to all 29 flashcards in this deck.

Unlock Deck

k this deck

19

A subsidiary's acquisition of its common stock from minority stockholders for the treasury at a cost (equal to current fair value) of $84 a share results in:

A) A nonoperating gain if the per-share carrying amount of the parent company's investment in the subsidiary is more than $84 a share

B) An extraordinary gain if the per-share carrying amount of the parent company's investment in the subsidiary is less than $84 a share

C) An extraordinary loss if the per-share carrying amount of the parent company's investment in the subsidiary is more than $84 a share

D) Subsidiary goodwill if the per-share carrying amount of the minority interest acquired is less than $84 a share

A) A nonoperating gain if the per-share carrying amount of the parent company's investment in the subsidiary is more than $84 a share

B) An extraordinary gain if the per-share carrying amount of the parent company's investment in the subsidiary is less than $84 a share

C) An extraordinary loss if the per-share carrying amount of the parent company's investment in the subsidiary is more than $84 a share

D) Subsidiary goodwill if the per-share carrying amount of the minority interest acquired is less than $84 a share

Unlock Deck

Unlock for access to all 29 flashcards in this deck.

Unlock Deck

k this deck

20

The minority interest of a subsidiary's preferred stockholders in the net assets of the subsidiary is measured by the preferred stock's:

A) Par or stated value

B) Current fair value

C) Liquidation value

D) Call price

A) Par or stated value

B) Current fair value

C) Liquidation value

D) Call price

Unlock Deck

Unlock for access to all 29 flashcards in this deck.

Unlock Deck

k this deck

21

On October 31, 2006, Palomar Corporation prepared the following journal entry (explanation, omitted) regarding its investment in its partially owned subsidiary, San Diego Company: If no accompanying journal entry was prepared by Palomar, the most likely cause of the foregoing journal entry was:

A) San Diego issued additional shares of common stock to the public at a price per share less than the per-share carrying amount of Palomar's investment in San Diego

B) Palomar disposed of some of its investment in San Diego at a price per share less than the per-share carrying amount of Palomar's investment in San Diego

C) San Diego issued additional shares of common stock to Palomar at a price per share greater than the per-share carrying amount of Palomar's earlier investment in San Diego

D) Some other transaction or event

A) San Diego issued additional shares of common stock to the public at a price per share less than the per-share carrying amount of Palomar's investment in San Diego

B) Palomar disposed of some of its investment in San Diego at a price per share less than the per-share carrying amount of Palomar's investment in San Diego

C) San Diego issued additional shares of common stock to Palomar at a price per share greater than the per-share carrying amount of Palomar's earlier investment in San Diego

D) Some other transaction or event

Unlock Deck

Unlock for access to all 29 flashcards in this deck.

Unlock Deck

k this deck

22

In working paper eliminations for a parent company and a subsidiary that acquired its outstanding common stock for the treasury subsequent to the business combination, the subsidiary's treasury stock is:

A) Disregarded

B) Deducted from the subsidiary's beginning-of-year retained earnings

C) Accounted for as though it had been retired

D) Offset against the parent company's Retained Earnings of Subsidiary ledger account balance

A) Disregarded

B) Deducted from the subsidiary's beginning-of-year retained earnings

C) Accounted for as though it had been retired

D) Offset against the parent company's Retained Earnings of Subsidiary ledger account balance

Unlock Deck

Unlock for access to all 29 flashcards in this deck.

Unlock Deck

k this deck

23

A parent company's disposal of a portion of its holdings of a subsidiary's common stock results in:

A) A realized gain or loss that is not eliminated in consolidation

B) An unrealized gain or loss that is eliminated in consolidation

C) A realized gain or loss that is eliminated in consolidation

D) An unrealized gain or loss that is not eliminated in consolidation

A) A realized gain or loss that is not eliminated in consolidation

B) An unrealized gain or loss that is eliminated in consolidation

C) A realized gain or loss that is eliminated in consolidation

D) An unrealized gain or loss that is not eliminated in consolidation

Unlock Deck

Unlock for access to all 29 flashcards in this deck.

Unlock Deck

k this deck

24

The stockholders' equity of Sidding Company on September 30, 2006, the end of a fiscal year, was as follows:

Sidding had no cumulative preferred dividends in arrears. The current fair values of Sidding's identifiable net assets equaled their carrying amounts on September 30, 2006.

On October 1, 2006, Preen Corporation paid $1,400,000 for 70,000 shares of Sidding's outstanding preferred stock and 80,000 shares of Sidding's outstanding common stock. Out-of-pocket costs of the business combination may be disregarded.

a. Prepare a journal entry on October 1, 2006, to record Preen Corporation's business combination with Sidding Company. Omit explanation and disregard income taxes.

b. Prepare a working paper elimination (in journal entry format) for Preen Corporation and subsidiary on October 1, 2006. Omit explanation and disregard income taxes.

Sidding had no cumulative preferred dividends in arrears. The current fair values of Sidding's identifiable net assets equaled their carrying amounts on September 30, 2006.On October 1, 2006, Preen Corporation paid $1,400,000 for 70,000 shares of Sidding's outstanding preferred stock and 80,000 shares of Sidding's outstanding common stock. Out-of-pocket costs of the business combination may be disregarded.

a. Prepare a journal entry on October 1, 2006, to record Preen Corporation's business combination with Sidding Company. Omit explanation and disregard income taxes.

b. Prepare a working paper elimination (in journal entry format) for Preen Corporation and subsidiary on October 1, 2006. Omit explanation and disregard income taxes.

Unlock Deck

Unlock for access to all 29 flashcards in this deck.

Unlock Deck

k this deck

25

Pryce Corporation owns 8,000 of the 10,000 shares of outstanding common stock of Somber Company. On July 31, 2006, the end of a fiscal year, the stockholders' equity of Somber was $800,000, and the balance of Pryce's Investment in Somber Company Common Stock ledger account was $678,000, of which $38,000 was attributable to unimpaired goodwill. The current fair values of Somber's identifiable net assets had equaled their carrying amounts on the date of the Pryce-Somber business combination.

On August 1, 2006, Somber issued 2,000 shares of common stock to the public at $110 a share, net of out-of-pocket costs of issuing the stock. Both Pryce and Somber's minority stockholders waived their preemptive right.

Prepare a working paper to compute the nonoperating gain or loss to Pryce Corporation resulting from Somber Company's issuance of common stock to the public. Use the following format:

On August 1, 2006, Somber issued 2,000 shares of common stock to the public at $110 a share, net of out-of-pocket costs of issuing the stock. Both Pryce and Somber's minority stockholders waived their preemptive right.

Prepare a working paper to compute the nonoperating gain or loss to Pryce Corporation resulting from Somber Company's issuance of common stock to the public. Use the following format:

Unlock Deck

Unlock for access to all 29 flashcards in this deck.

Unlock Deck

k this deck

26

The first working paper elimination (in journal entry format) for Pon Corporation and subsidiary on May 31, 2006, the end of a fiscal year, was as follows (explanation omitted):

EOn June 1, 2006, when the current fair value of its $1 par common stock was $8 a share, Sabre declared a 15% common stock dividend, to be issued June 15, 2006. Sabre prepared the following journal entry (explanation omitted) for the dividend:

Prepare a working paper elimination (in journal entry format) for Pon Corporation and subsidiary on June 1, 2006. Omit explanation and disregard income taxes.

EOn June 1, 2006, when the current fair value of its $1 par common stock was $8 a share, Sabre declared a 15% common stock dividend, to be issued June 15, 2006. Sabre prepared the following journal entry (explanation omitted) for the dividend: Prepare a working paper elimination (in journal entry format) for Pon Corporation and subsidiary on June 1, 2006. Omit explanation and disregard income taxes. Unlock Deck

Unlock for access to all 29 flashcards in this deck.

Unlock Deck

k this deck

27

Separate and consolidated financial statements of Park Corporation and its subsidiary, Stark Company, for the fiscal year ended December 31, 2006, are shown below. Park used the equity method of accounting for its investment in Stark, but neither enterprise used separate ledger accounts for intercompany revenue, expenses, gains, or losses.

Additional Information :

1. All of Stark's identifiable net assets were fairly stated at their carrying amounts on the date Park combined with Stark. The $10,000 excess of Park's investment in Stark over the current fair values (and carrying amounts) of Stark's identifiable net assets was allocated to goodwill, which was unimpaired on December 31, 2006.

2. Park sold merchandise to Stark at the same markup that Park realized on sales to its other customers.

3. Stark had acquired shares of Park's outstanding common stock on December 31, 2005. These shares were included in Stark's short-term investments.

4. Park acquired shares of its common stock for the treasury late in 2006 after the fourth-quarter dividend had been declared and paid.

From the foregoing information, provide answers for the following:

a. Percentage of Stark Company outstanding common stock owned by Park Corporation _______%

b. Intercompany sales by Park to Stark $________

c. Intercompany cost of goods sold eliminated $________

d. Intercompany investment income recognized by Park under the equity method of accounting $________

e. Amount of dividends received by Stark from Park and eliminated from other revenue $________

f. Amount of intercompany profit eliminated from ending inventories of Stark $_________

g. Number of shares of Park's common stock owned by Stark ________ shares

h. Carrying amount of Park common stock owned by Stark $________

Additional Information :1. All of Stark's identifiable net assets were fairly stated at their carrying amounts on the date Park combined with Stark. The $10,000 excess of Park's investment in Stark over the current fair values (and carrying amounts) of Stark's identifiable net assets was allocated to goodwill, which was unimpaired on December 31, 2006.

2. Park sold merchandise to Stark at the same markup that Park realized on sales to its other customers.

3. Stark had acquired shares of Park's outstanding common stock on December 31, 2005. These shares were included in Stark's short-term investments.

4. Park acquired shares of its common stock for the treasury late in 2006 after the fourth-quarter dividend had been declared and paid.

From the foregoing information, provide answers for the following:

a. Percentage of Stark Company outstanding common stock owned by Park Corporation _______%

b. Intercompany sales by Park to Stark $________

c. Intercompany cost of goods sold eliminated $________

d. Intercompany investment income recognized by Park under the equity method of accounting $________

e. Amount of dividends received by Stark from Park and eliminated from other revenue $________

f. Amount of intercompany profit eliminated from ending inventories of Stark $_________

g. Number of shares of Park's common stock owned by Stark ________ shares

h. Carrying amount of Park common stock owned by Stark $________

Unlock Deck

Unlock for access to all 29 flashcards in this deck.

Unlock Deck

k this deck

28

The stockholders' equity of Sprague Company on August 31, 2006, was as follows:

On August 31, 2006, Pommel Corporation paid $900,000 cash, including direct out-of-pocket costs of the business combination, for 48,000 shares of Sprague's outstanding common stock. The current fair values of Sprague's identifiable net assets were equal to their carrying amounts on August 31, 2006.

Prepare working paper eliminations (in journal entry format) for Pommel Corporation and subsidiary on August 31, 2006. Omit explanations and disregard income taxes.

On August 31, 2006, Pommel Corporation paid $900,000 cash, including direct out-of-pocket costs of the business combination, for 48,000 shares of Sprague's outstanding common stock. The current fair values of Sprague's identifiable net assets were equal to their carrying amounts on August 31, 2006.Prepare working paper eliminations (in journal entry format) for Pommel Corporation and subsidiary on August 31, 2006. Omit explanations and disregard income taxes.

Unlock Deck

Unlock for access to all 29 flashcards in this deck.

Unlock Deck

k this deck

29

If a partially owned subsidiary issues additional shares of common stock to the public or to the parent company, with minority stockholders waiving their preemptive right, the parent company recognizes a nonoperating gain or loss. What would be the effect on the parent company if:

(1) The subsidiary issued additional shares of common stock to the public, but the minority stockholders exercised their preemptive right to participate pro rata in the stock issuance?

(2) The subsidiary issued additional shares of common stock to the parent company, but the minority stockholders exercised their preemptive right to participate pro rata in the stock issuance?

Explain.

(1) The subsidiary issued additional shares of common stock to the public, but the minority stockholders exercised their preemptive right to participate pro rata in the stock issuance?

(2) The subsidiary issued additional shares of common stock to the parent company, but the minority stockholders exercised their preemptive right to participate pro rata in the stock issuance?

Explain.

Unlock Deck

Unlock for access to all 29 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 29 flashcards in this deck.