Deck 7: Consolidated Financial Statements: Subsequent to Date of Business Combination

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

The format of a parent company's journal entry (explanation omitted), under the equity method of accounting, to adjust a wholly owned subsidiary's net income or loss for depreciation and amortization of differences between date-of-combination current fair values and carrying amounts of the subsidiary's identifiable net assets, is:

A)

B)

C)

D) Some other format

A)

B)

C)

D) Some other format

Question

A parent company that uses the equity method of accounting for a 90%-owned subsidiary prepared the following journal entry:

A possible explanation for the foregoing journal entry is:

A possible explanation for the foregoing journal entry is:

A) To recognize 90% of subsidiary's net income for year

B) To recognize 90% of subsidiary's net loss for year

C) To amortize differences between current fair values and carrying amounts of subsidiary's identifiable net assets on date of business combination

D) Either a or c

E) Either b or c

A possible explanation for the foregoing journal entry is:A) To recognize 90% of subsidiary's net income for year

B) To recognize 90% of subsidiary's net loss for year

C) To amortize differences between current fair values and carrying amounts of subsidiary's identifiable net assets on date of business combination

D) Either a or c

E) Either b or c

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

The Investment in Sark Company Common Stock ledger account of Poulter Corporation was as follows for the year ended December 31, 2006:

Poulter had acquired 80% of the outstanding common stock of Sark on December 31, 2005 in a business combination.

Poulter had acquired 80% of the outstanding common stock of Sark on December 31, 2005 in a business combination.

For the fiscal year ended December 31, 2006, Poulter had total revenue (excluding intercompany investment income) of $800,000, and total costs and expenses (including goodwill impairment loss) of $600,000. Poulter declared cash dividends of $60,000 during 2006.

a. Reconstruct Poulter Corporation's equity-method journal entries for the operations of Sark Company for 2006. Omit explanations and disregard income taxes.

b. Prepare Poulter Corporation's closing entries on December 31, 2006. Omit explanations.

Poulter had acquired 80% of the outstanding common stock of Sark on December 31, 2005 in a business combination.For the fiscal year ended December 31, 2006, Poulter had total revenue (excluding intercompany investment income) of $800,000, and total costs and expenses (including goodwill impairment loss) of $600,000. Poulter declared cash dividends of $60,000 during 2006.

a. Reconstruct Poulter Corporation's equity-method journal entries for the operations of Sark Company for 2006. Omit explanations and disregard income taxes.

b. Prepare Poulter Corporation's closing entries on December 31, 2006. Omit explanations.

Question

On July 1, 2005, Parson Corporation acquired all the outstanding common stock of Scate Company for $900,000. On that date, the carrying amount of Scate's identifiable net assets was $800,000. The difference of $100,000 was allocated as follows:

Scate had a net income of $190,000 and declared dividends of $100,000 for the fiscal year ended June 30, 2006. Scate uses straight-line depreciation for plant assets. Goodwill was one-thirtieth impaired on June 30, 2006.

Scate had a net income of $190,000 and declared dividends of $100,000 for the fiscal year ended June 30, 2006. Scate uses straight-line depreciation for plant assets. Goodwill was one-thirtieth impaired on June 30, 2006.

Prepare a working paper to compute the following for Parson Corporation under the equity method of accounting (disregard income taxes):

a. Balance of Intercompany Investment Income ledger account on June 30, 2006

b. Balance of Investment in Scate Company Common Stock ledger account on June 30, 2006

Scate had a net income of $190,000 and declared dividends of $100,000 for the fiscal year ended June 30, 2006. Scate uses straight-line depreciation for plant assets. Goodwill was one-thirtieth impaired on June 30, 2006.Prepare a working paper to compute the following for Parson Corporation under the equity method of accounting (disregard income taxes):

a. Balance of Intercompany Investment Income ledger account on June 30, 2006

b. Balance of Investment in Scate Company Common Stock ledger account on June 30, 2006

Question

Selected ledger account balances (before closing entries) of Pome Corporation on September 30, 2006, one year after the business combination with an 80%-owned subsidiary, were as follows:

The carrying amount of Soper's identifiable net assets on September 30, 2005, was $1,200,000, which was the same as their current fair value on that date. Soper had a net income of $80,000 and declared and paid dividends of $20,000 during the fiscal year ended September 30, 2006. Goodwill was unimpaired on September 30, 2006.

The carrying amount of Soper's identifiable net assets on September 30, 2005, was $1,200,000, which was the same as their current fair value on that date. Soper had a net income of $80,000 and declared and paid dividends of $20,000 during the fiscal year ended September 30, 2006. Goodwill was unimpaired on September 30, 2006.

Prepare an adjusting entry on September 30, 2006, to convert Pome Corporation's accounting for the operations of Soper Company to the equity method of accounting from the cost method of accounting. Disregard income taxes.

The carrying amount of Soper's identifiable net assets on September 30, 2005, was $1,200,000, which was the same as their current fair value on that date. Soper had a net income of $80,000 and declared and paid dividends of $20,000 during the fiscal year ended September 30, 2006. Goodwill was unimpaired on September 30, 2006.Prepare an adjusting entry on September 30, 2006, to convert Pome Corporation's accounting for the operations of Soper Company to the equity method of accounting from the cost method of accounting. Disregard income taxes.

Question

Question

Question

Question

On September 30, 2005, Phoenix Corporation paid $400,000 for 75% of the outstanding $1 par common stock of Salem Company and $80,000 for legal fees in connection with the business combination. On that date, Salem's stockholders' equity was as follows:

Current fair values of Salem's inventories (first-in, first-out cost) and depreciable plant assets (net) exceeded their carrying amounts by $20,000 and $90,000, respectively, on September 30, 2005. Current fair values of Salem's other identifiable net assets equaled their carrying amounts on that date. Salem's depreciable plant assets had a composite economic life of nine years on September 30, 2005, and Salem includes straight-line depreciation expense in cost of goods sold.

Current fair values of Salem's inventories (first-in, first-out cost) and depreciable plant assets (net) exceeded their carrying amounts by $20,000 and $90,000, respectively, on September 30, 2005. Current fair values of Salem's other identifiable net assets equaled their carrying amounts on that date. Salem's depreciable plant assets had a composite economic life of nine years on September 30, 2005, and Salem includes straight-line depreciation expense in cost of goods sold.

For the fiscal year ended September 30, 2006, Salem had a net income of $80,000, but did not declare dividends. Goodwill was unimpaired on September 30, 2006.

a. Prepare Phoenix Corporation's journal entries to record the business combination of Phoenix and Salem Company on September 30, 2005.

b. Prepare a working paper elimination (in journal entry format) for Phoenix Corporation and subsidiary on September 30, 2005.

c. Prepare Phoenix Corporation's journal entries, under the equity method of accounting, to record Salem Company's operating results for the fiscal year ended September 30, 2006.

d. Prepare working paper eliminations (in journal entry format) for Phoenix Corporation and subsidiary on September 30, 2006.

Omit explanations and disregard income taxes.

Current fair values of Salem's inventories (first-in, first-out cost) and depreciable plant assets (net) exceeded their carrying amounts by $20,000 and $90,000, respectively, on September 30, 2005. Current fair values of Salem's other identifiable net assets equaled their carrying amounts on that date. Salem's depreciable plant assets had a composite economic life of nine years on September 30, 2005, and Salem includes straight-line depreciation expense in cost of goods sold.For the fiscal year ended September 30, 2006, Salem had a net income of $80,000, but did not declare dividends. Goodwill was unimpaired on September 30, 2006.

a. Prepare Phoenix Corporation's journal entries to record the business combination of Phoenix and Salem Company on September 30, 2005.

b. Prepare a working paper elimination (in journal entry format) for Phoenix Corporation and subsidiary on September 30, 2005.

c. Prepare Phoenix Corporation's journal entries, under the equity method of accounting, to record Salem Company's operating results for the fiscal year ended September 30, 2006.

d. Prepare working paper eliminations (in journal entry format) for Phoenix Corporation and subsidiary on September 30, 2006.

Omit explanations and disregard income taxes.

Question

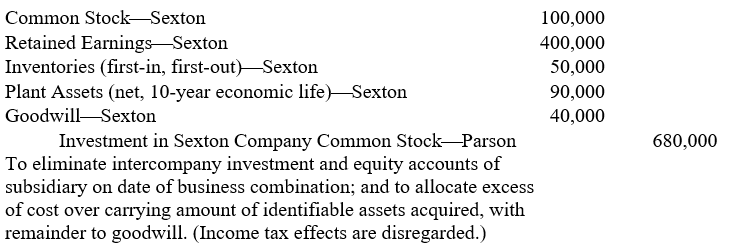

The working paper elimination (in journal entry format) for Parson Corporation and subsidiary on February 28, 2005, (the date of the business combination) was as follows:

For the fiscal year ended February 28, 2006, Sexton had a net income of $120,000 and declared a dividend of $40,000 to Parson. Sexton includes straight-line depreciation in operating expenses. Goodwill was unimpaired on February 28, 2006.

For the fiscal year ended February 28, 2006, Sexton had a net income of $120,000 and declared a dividend of $40,000 to Parson. Sexton includes straight-line depreciation in operating expenses. Goodwill was unimpaired on February 28, 2006.

Prepare a working paper elimination (in journal entry format) for Parson Corporation and subsidiary on February 28, 2006. Omit explanation and disregard income taxes.

For the fiscal year ended February 28, 2006, Sexton had a net income of $120,000 and declared a dividend of $40,000 to Parson. Sexton includes straight-line depreciation in operating expenses. Goodwill was unimpaired on February 28, 2006.Prepare a working paper elimination (in journal entry format) for Parson Corporation and subsidiary on February 28, 2006. Omit explanation and disregard income taxes.

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/39

Play

Full screen (f)

Deck 7: Consolidated Financial Statements: Subsequent to Date of Business Combination

1

Under the equity method of accounting, a parent company credits the Intercompany Investment Income ledger account for dividends declared by the subsidiary.

False

2

Under the equity method of accounting, a parent company's journal entry to record a dividend declared by the subsidiary includes a debit to the Retained Earnings of Subsidiary ledger account and a credit to the Dividends Revenue ledger account.

False

3

Proponents of the equity method of accounting assert that dividends declared by a subsidiary constitute revenue to the parent company.

False

4

A wholly owned subsidiary credits the Dividends Payable ledger account when its board of directors declares a dividend.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

5

Under the equity method of accounting, the parent company credits the Intercompany Investment Income ledger account for dividends declared by the subsidiary.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

6

Under the equity method of accounting, the parent company debits the Intercompany Investment Income ledger account for the depreciation and amortization of differences between the current fair values and carrying amounts of a subsidiary's identifiable net assets on the date of the business combination.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

7

The depreciation and amortization of differences between current fair values and carrying amounts of a subsidiary's identifiable net assets is included in consolidated financial statements by means of a working paper elimination.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

8

In a closing entry for a parent company that has a subsidiary acquired several years ago, there may be either a debit or a credit to the Retained Earnings of Subsidiary ledger account.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

9

Goodwill attributable to a business combination involving a partially owned subsidiary is amortized by means of a working paper elimination.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

10

A parent company that uses the cost method of accounting for the operations of a subsidiary prepares no journal entries to reflect the subsidiary's net income or loss for an accounting period.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

11

Use of the equity method of accounting facilitates a parent company's issuances of unconsolidated financial statements to the Securities and Exchange Commission if the SEC requires such statements.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

12

Dividends declared by a subsidiary subsequent to the date of a business combination are displayed in a consolidated statement of retained earnings.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

13

The equity method of accounting for a subsidiary's operations is similar to home office accounting for a branch's operations.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

14

On October 1, 2006, Poon Corporation acquired for cash all the outstanding common stock of Soong Company, which was not liquidated. Consolidated net income for the fiscal year ended December 31, 2006, includes net income of:

A) Poon for three months and Soong for three months

B) Poon for twelve months and Soong for three months

C) Poon for twelve months and Soong for twelve months

D) Poon for twelve months, but no income from Soong until it declares a cash dividend

A) Poon for three months and Soong for three months

B) Poon for twelve months and Soong for three months

C) Poon for twelve months and Soong for twelve months

D) Poon for twelve months, but no income from Soong until it declares a cash dividend

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

15

The method of accounting for a subsidiary's operations that emphasizes the legal form of the parent company-subsidiary relationship is:

A) The cost method

B) The equity method

C) The purchase method

D) The fair value method

A) The cost method

B) The equity method

C) The purchase method

D) The fair value method

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

16

The format of a parent company's journal entry (explanation omitted), under the equity method of accounting, to adjust a wholly owned subsidiary's net income or loss for depreciation and amortization of differences between date-of-combination current fair values and carrying amounts of the subsidiary's identifiable net assets, is:

A)

B)

C)

D) Some other format

A)

B)

C)

D) Some other format

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

17

A parent company that uses the equity method of accounting for a 90%-owned subsidiary prepared the following journal entry:

A possible explanation for the foregoing journal entry is:

A) To recognize 90% of subsidiary's net income for year

B) To recognize 90% of subsidiary's net loss for year

C) To amortize differences between current fair values and carrying amounts of subsidiary's identifiable net assets on date of business combination

D) Either a or c

E) Either b or c

A possible explanation for the foregoing journal entry is:A) To recognize 90% of subsidiary's net income for year

B) To recognize 90% of subsidiary's net loss for year

C) To amortize differences between current fair values and carrying amounts of subsidiary's identifiable net assets on date of business combination

D) Either a or c

E) Either b or c

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

18

During the fiscal year ended October 31, 2006, a wholly owned subsidiary of Prescott Company had an adjusted net income of $200,000 and declared dividends of $80,000. In its own operations (exclusive of its equity-method journal entries for the subsidiary), Prescott had total revenue of $800,000 and total costs and expenses of $600,000. In an October 31, 2006, closing entry, Prescott should:

A) Credit Intercompany Investment Income $200,000

B) Credit Retained Earnings of Subsidiary $120,000

C) Credit Retained Earnings $400,000

D) Debit Costs and Expenses $800,000

A) Credit Intercompany Investment Income $200,000

B) Credit Retained Earnings of Subsidiary $120,000

C) Credit Retained Earnings $400,000

D) Debit Costs and Expenses $800,000

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

19

The Retained Earnings of Subsidiary ledger account is:

A) An account of the parent company that at all times in any business combination shows the amount of the subsidiary's retained earnings

B) An account of the subsidiary

C) An account that appears only in the working paper for consolidated financial statements

D) None of the foregoing

A) An account of the parent company that at all times in any business combination shows the amount of the subsidiary's retained earnings

B) An account of the subsidiary

C) An account that appears only in the working paper for consolidated financial statements

D) None of the foregoing

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

20

Under the equity method of accounting, depreciation and amortization of the date-of-business-combination differences between current fair values and carrying amounts of a subsidiary's identifiable net assets is debited in a journal entry to the:

A) Subsidiary's expense ledger accounts

B) Parent company's expense ledger accounts

C) Subsidiary's Retained Earnings ledger account

D) Parent company's Intercompany Investment Income ledger account

A) Subsidiary's expense ledger accounts

B) Parent company's expense ledger accounts

C) Subsidiary's Retained Earnings ledger account

D) Parent company's Intercompany Investment Income ledger account

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

21

If a parent company uses the equity method of accounting for a partially owned subsidiary and there are no intercompany profits (gains) or losses eliminated for the measurement of consolidated net income, consolidated retained earnings is equal to the balance of the parent company's:

A) Retained Earnings ledger account

B) Retained Earnings ledger account plus the balance of the subsidiary's Retained Earnings ledger account

C) Retained Earnings ledger account plus the parent's share of the balance of the subsidiary's Retained Earnings ledger account

D) Retained Earnings ledger account plus the parent's share of the net increase in the subsidiary's retained earnings subsequent to the date of the business combination

A) Retained Earnings ledger account

B) Retained Earnings ledger account plus the balance of the subsidiary's Retained Earnings ledger account

C) Retained Earnings ledger account plus the parent's share of the balance of the subsidiary's Retained Earnings ledger account

D) Retained Earnings ledger account plus the parent's share of the net increase in the subsidiary's retained earnings subsequent to the date of the business combination

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

22

Which of the following is not typical of the journal entries prepared by a parent company to account for its subsidiary's operations under the equity method of accounting?

A) Accrual of the parent company's share of the subsidiary's net income or loss

B) A credit to the Intercompany Dividend Revenue ledger account

C) Depreciation and amortization of differences between current fair values and carrying amounts of the subsidiary's identifiable net assets on the date of the business combination

D) None of the foregoing

A) Accrual of the parent company's share of the subsidiary's net income or loss

B) A credit to the Intercompany Dividend Revenue ledger account

C) Depreciation and amortization of differences between current fair values and carrying amounts of the subsidiary's identifiable net assets on the date of the business combination

D) None of the foregoing

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

23

To recognize the impairment of goodwill arising from a business combination involving a partially owned subsidiary:

A) The subsidiary debits the Impairment Loss ledger account and credits the Goodwill account in its accounting records.

B) The parent company debits the Impairment Loss ledger account and credits the Goodwill account in its accounting records.

C) The parent company debits the Intercompany Investment Income ledger account and credits the Investment in Subsidiary Common Stock account in its accounting records.

D) The parent company prepares some other journal entry.

A) The subsidiary debits the Impairment Loss ledger account and credits the Goodwill account in its accounting records.

B) The parent company debits the Impairment Loss ledger account and credits the Goodwill account in its accounting records.

C) The parent company debits the Intercompany Investment Income ledger account and credits the Investment in Subsidiary Common Stock account in its accounting records.

D) The parent company prepares some other journal entry.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

24

Skeene Company, the 70%-owned subsidiary of Probert Corporation, had a net income of $80,000 and declared dividends of $30,000 during the fiscal year ended February 28, 2006. Fiscal Year 2006 depreciation and amortization of differences between current fair values and carrying amounts of Skeene's identifiable net assets on the date of the business combination was $15,000; and Fiscal Year 2006 impairment of goodwill recognized in the Probert-Skeene business combination was $500. The minority interest in net income of Skeene for Fiscal Year 2006 was:

A) $24,000

B) $19,500

C) $19,350

D) $9,000

E) Some other amount

A) $24,000

B) $19,500

C) $19,350

D) $9,000

E) Some other amount

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

25

Which of the following does not affect the computation of the minority interest in the net assets of a partially owned subsidiary?

A) Impairment of goodwill recognized in the business combination

B) Dividends declared by the subsidiary

C) Depreciation and amortization of differences between current fair values and carrying amounts of the subsidiary's identifiable net assets on the date of the business combination

D) None of the foregoing

A) Impairment of goodwill recognized in the business combination

B) Dividends declared by the subsidiary

C) Depreciation and amortization of differences between current fair values and carrying amounts of the subsidiary's identifiable net assets on the date of the business combination

D) None of the foregoing

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

26

Which of the following is not an attribute of the equity method of accounting for the operating results of subsidiaries?

A) It facilitates the preparation of unconsolidated parent company financial statements required by the Securities and Exchange Commission.

B) It emphasizes the legal form of the parent company-subsidiary relationship.

C) It facilitates the use of parent company journal entries rather than working paper eliminations.

D) It provides a useful self-checking technique.

A) It facilitates the preparation of unconsolidated parent company financial statements required by the Securities and Exchange Commission.

B) It emphasizes the legal form of the parent company-subsidiary relationship.

C) It facilitates the use of parent company journal entries rather than working paper eliminations.

D) It provides a useful self-checking technique.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

27

Under the equity method of accounting, dividends declared by a subsidiary are accounted for by the parent company as:

A) A liquidation of a portion of the parent company's investment in the subsidiary

B) Revenue

C) Both a and b if the amount of the dividends exceeds the subsidiary's post-combination net income

D) Some other item

A) A liquidation of a portion of the parent company's investment in the subsidiary

B) Revenue

C) Both a and b if the amount of the dividends exceeds the subsidiary's post-combination net income

D) Some other item

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

28

Plover Corporation accounts for its 80%-owned purchased subsidiary, Swallow Company, under the equity method of accounting. For the fiscal year ended March 31, 2006, Swallow had a net income of $100,000, but declared no dividends. Depreciation and amortization of differences between current fair values and carrying amounts of Swallow's identifiable net assets for the year ended March 31, 2006, totaled $40,000. Plover's closing entry for the year ended March 31, 2006, includes a:

A) Credit of $48,000 to Intercompany Investment Income

B) Credit of $60,000 to Retained Earnings of Subsidiary

C) Debit of $60,000 to Intercompany Investment Income

D) Credit of $48,000 to Retained Earnings of Subsidiary

A) Credit of $48,000 to Intercompany Investment Income

B) Credit of $60,000 to Retained Earnings of Subsidiary

C) Debit of $60,000 to Intercompany Investment Income

D) Credit of $48,000 to Retained Earnings of Subsidiary

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

29

The minority interest in net assets of a partially owned subsidiary is:

A) Decreased by the minority's share of subsidiary dividends and increased by the minority's share of subsidiary adjusted net income

B) Increased by the minority's share of subsidiary dividends and decreased by the minority's share of subsidiary adjusted net income

C) Decreased by the minority's share of both subsidiary dividends and subsidiary adjusted net income

D) Increased by the minority's share of both subsidiary dividends and subsidiary adjusted net income

A) Decreased by the minority's share of subsidiary dividends and increased by the minority's share of subsidiary adjusted net income

B) Increased by the minority's share of subsidiary dividends and decreased by the minority's share of subsidiary adjusted net income

C) Decreased by the minority's share of both subsidiary dividends and subsidiary adjusted net income

D) Increased by the minority's share of both subsidiary dividends and subsidiary adjusted net income

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

30

If a wholly owned subsidiary's net income was $150,000, the subsidiary declared dividends of $80,000, and the depreciation and amortization of current fair value excess was $20,000, the parent company's intercompany investment income under the equity method of accounting is:

A) $60,000

B) $70,000

C) $100,000

D) $130,000

E) Some other amount

A) $60,000

B) $70,000

C) $100,000

D) $130,000

E) Some other amount

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

31

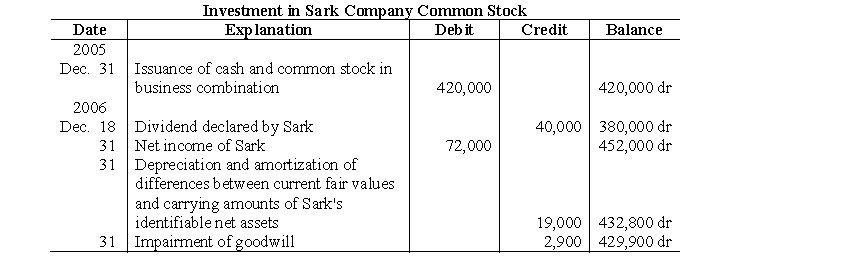

The Investment in Sark Company Common Stock ledger account of Poulter Corporation was as follows for the year ended December 31, 2006:

Poulter had acquired 80% of the outstanding common stock of Sark on December 31, 2005 in a business combination.

For the fiscal year ended December 31, 2006, Poulter had total revenue (excluding intercompany investment income) of $800,000, and total costs and expenses (including goodwill impairment loss) of $600,000. Poulter declared cash dividends of $60,000 during 2006.

a. Reconstruct Poulter Corporation's equity-method journal entries for the operations of Sark Company for 2006. Omit explanations and disregard income taxes.

b. Prepare Poulter Corporation's closing entries on December 31, 2006. Omit explanations.

Poulter had acquired 80% of the outstanding common stock of Sark on December 31, 2005 in a business combination.For the fiscal year ended December 31, 2006, Poulter had total revenue (excluding intercompany investment income) of $800,000, and total costs and expenses (including goodwill impairment loss) of $600,000. Poulter declared cash dividends of $60,000 during 2006.

a. Reconstruct Poulter Corporation's equity-method journal entries for the operations of Sark Company for 2006. Omit explanations and disregard income taxes.

b. Prepare Poulter Corporation's closing entries on December 31, 2006. Omit explanations.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

32

On July 1, 2005, Parson Corporation acquired all the outstanding common stock of Scate Company for $900,000. On that date, the carrying amount of Scate's identifiable net assets was $800,000. The difference of $100,000 was allocated as follows:

Scate had a net income of $190,000 and declared dividends of $100,000 for the fiscal year ended June 30, 2006. Scate uses straight-line depreciation for plant assets. Goodwill was one-thirtieth impaired on June 30, 2006.

Prepare a working paper to compute the following for Parson Corporation under the equity method of accounting (disregard income taxes):

a. Balance of Intercompany Investment Income ledger account on June 30, 2006

b. Balance of Investment in Scate Company Common Stock ledger account on June 30, 2006

Scate had a net income of $190,000 and declared dividends of $100,000 for the fiscal year ended June 30, 2006. Scate uses straight-line depreciation for plant assets. Goodwill was one-thirtieth impaired on June 30, 2006.Prepare a working paper to compute the following for Parson Corporation under the equity method of accounting (disregard income taxes):

a. Balance of Intercompany Investment Income ledger account on June 30, 2006

b. Balance of Investment in Scate Company Common Stock ledger account on June 30, 2006

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

33

Selected ledger account balances (before closing entries) of Pome Corporation on September 30, 2006, one year after the business combination with an 80%-owned subsidiary, were as follows:

The carrying amount of Soper's identifiable net assets on September 30, 2005, was $1,200,000, which was the same as their current fair value on that date. Soper had a net income of $80,000 and declared and paid dividends of $20,000 during the fiscal year ended September 30, 2006. Goodwill was unimpaired on September 30, 2006.

Prepare an adjusting entry on September 30, 2006, to convert Pome Corporation's accounting for the operations of Soper Company to the equity method of accounting from the cost method of accounting. Disregard income taxes.

The carrying amount of Soper's identifiable net assets on September 30, 2005, was $1,200,000, which was the same as their current fair value on that date. Soper had a net income of $80,000 and declared and paid dividends of $20,000 during the fiscal year ended September 30, 2006. Goodwill was unimpaired on September 30, 2006.Prepare an adjusting entry on September 30, 2006, to convert Pome Corporation's accounting for the operations of Soper Company to the equity method of accounting from the cost method of accounting. Disregard income taxes.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

34

For the fiscal year ended March 31, 2006, Sable Company, the 80%-owned subsidiary of Pastel Corporation, had a net income of $600,000 and declared and paid dividends of $200,000. Fiscal Year 2006 depreciation and amortization of differences between current fair values and carrying amounts of Sable's identifiable net assets was $30,000; and Fiscal Year 2006 impairment of goodwill recognized in the business combination was $1,000.

Prepare journal entries for Pastel Corporation to record the Fiscal Year 2006 operating results of Sable Company under the:

a. Equity method of accounting

b. Cost method of accounting

Omit explanations for the journal entries and disregard income taxes.

Prepare journal entries for Pastel Corporation to record the Fiscal Year 2006 operating results of Sable Company under the:

a. Equity method of accounting

b. Cost method of accounting

Omit explanations for the journal entries and disregard income taxes.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

35

Refer to the above facts. Assume that, in addition to the revenue and expenses it recognized for Sable Company's operations, Pastel Corporation had net sales of $4,800,000 and total costs and expenses of $3,300,000, but declared no dividends.

Prepare closing entries (omit explanations) on March 31, 2006, for Pastel Corporation under the:

a. Equity method of accounting

b. Cost method of accounting

Prepare closing entries (omit explanations) on March 31, 2006, for Pastel Corporation under the:

a. Equity method of accounting

b. Cost method of accounting

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

36

On the date of the business combination of Passman Corporation and Slago Company, the following working paper elimination was prepared (in journal entry format):

Additional Information

1. On January 31, 2005, the remaining economic life of Slago's plant assets was 10 years, and Slago includes straight-line depreciation in operating expenses.

2. Goodwill was unimpaired on January 31, 2006.

3. Slago declared a dividend of $20,000 to Passman on December 27, 2005, and paid the dividend on January 17, 2006. Slago had a net income of $90,000 for the fiscal year ended January 31, 2006.

a. Prepare journal entries for Passman Corporation to record the operating results of Slago Company for the year ended January 31, 2006, under the equity method of accounting. Omit explanations and disregard income taxes.

b. Prepare a working paper elimination (in journal entry format) for Passman Corporation and subsidiary on January 31, 2006. Omit explanation and disregard income taxes.

Additional Information

1. On January 31, 2005, the remaining economic life of Slago's plant assets was 10 years, and Slago includes straight-line depreciation in operating expenses.

2. Goodwill was unimpaired on January 31, 2006.

3. Slago declared a dividend of $20,000 to Passman on December 27, 2005, and paid the dividend on January 17, 2006. Slago had a net income of $90,000 for the fiscal year ended January 31, 2006.

a. Prepare journal entries for Passman Corporation to record the operating results of Slago Company for the year ended January 31, 2006, under the equity method of accounting. Omit explanations and disregard income taxes.

b. Prepare a working paper elimination (in journal entry format) for Passman Corporation and subsidiary on January 31, 2006. Omit explanation and disregard income taxes.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

37

On September 30, 2005, Phoenix Corporation paid $400,000 for 75% of the outstanding $1 par common stock of Salem Company and $80,000 for legal fees in connection with the business combination. On that date, Salem's stockholders' equity was as follows:

Current fair values of Salem's inventories (first-in, first-out cost) and depreciable plant assets (net) exceeded their carrying amounts by $20,000 and $90,000, respectively, on September 30, 2005. Current fair values of Salem's other identifiable net assets equaled their carrying amounts on that date. Salem's depreciable plant assets had a composite economic life of nine years on September 30, 2005, and Salem includes straight-line depreciation expense in cost of goods sold.

For the fiscal year ended September 30, 2006, Salem had a net income of $80,000, but did not declare dividends. Goodwill was unimpaired on September 30, 2006.

a. Prepare Phoenix Corporation's journal entries to record the business combination of Phoenix and Salem Company on September 30, 2005.

b. Prepare a working paper elimination (in journal entry format) for Phoenix Corporation and subsidiary on September 30, 2005.

c. Prepare Phoenix Corporation's journal entries, under the equity method of accounting, to record Salem Company's operating results for the fiscal year ended September 30, 2006.

d. Prepare working paper eliminations (in journal entry format) for Phoenix Corporation and subsidiary on September 30, 2006.

Omit explanations and disregard income taxes.

Current fair values of Salem's inventories (first-in, first-out cost) and depreciable plant assets (net) exceeded their carrying amounts by $20,000 and $90,000, respectively, on September 30, 2005. Current fair values of Salem's other identifiable net assets equaled their carrying amounts on that date. Salem's depreciable plant assets had a composite economic life of nine years on September 30, 2005, and Salem includes straight-line depreciation expense in cost of goods sold.For the fiscal year ended September 30, 2006, Salem had a net income of $80,000, but did not declare dividends. Goodwill was unimpaired on September 30, 2006.

a. Prepare Phoenix Corporation's journal entries to record the business combination of Phoenix and Salem Company on September 30, 2005.

b. Prepare a working paper elimination (in journal entry format) for Phoenix Corporation and subsidiary on September 30, 2005.

c. Prepare Phoenix Corporation's journal entries, under the equity method of accounting, to record Salem Company's operating results for the fiscal year ended September 30, 2006.

d. Prepare working paper eliminations (in journal entry format) for Phoenix Corporation and subsidiary on September 30, 2006.

Omit explanations and disregard income taxes.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

38

The working paper elimination (in journal entry format) for Parson Corporation and subsidiary on February 28, 2005, (the date of the business combination) was as follows:

For the fiscal year ended February 28, 2006, Sexton had a net income of $120,000 and declared a dividend of $40,000 to Parson. Sexton includes straight-line depreciation in operating expenses. Goodwill was unimpaired on February 28, 2006.

Prepare a working paper elimination (in journal entry format) for Parson Corporation and subsidiary on February 28, 2006. Omit explanation and disregard income taxes.

For the fiscal year ended February 28, 2006, Sexton had a net income of $120,000 and declared a dividend of $40,000 to Parson. Sexton includes straight-line depreciation in operating expenses. Goodwill was unimpaired on February 28, 2006.Prepare a working paper elimination (in journal entry format) for Parson Corporation and subsidiary on February 28, 2006. Omit explanation and disregard income taxes.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

39

In a classroom discussion of the relative merits of the equity method and the cost method of accounting for operations of subsidiaries, most students of Professor Long's advanced accounting class expressed a preference for the equity method, influenced in large part by their textbook's support for that method. Student Rita, however, suggested that, for a parent company with several subsidiaries, the cost method of accounting might be more cost-effective because it entails fewer journal entries than does the equity method. In Rita's view, it would be more efficient in such circumstances to make the multitudinous entries for subsidiaries' operations in the working paper for consolidated financial statements than in several ledger accounts in computerized accounting records.

Do you agree with student Rita's view? Explain.

Do you agree with student Rita's view? Explain.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 39 flashcards in this deck.