Deck 20: Transfer Pricing, Multinational Considerations, and Management Information System

Full screen (f)

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/3

Play

Full screen (f)

Deck 20: Transfer Pricing, Multinational Considerations, and Management Information System

Answer the following questions using the information below:

Division A sells potatoes internally to Division B, which in turn, produces chips that sell for $10 per pound. Division A incurs costs of $1.50 per pound while Division B incurs additional costs of $5.00 per pound.

-Which of the following formulas correctly reflects the company's operating income per pound?

A) $10.00 - ($0.50 + $2.50 + $7.00) = 0

B) $10.00 - ($1.50 + $7.50) = $1.00

C) $10.00 - ($2.50 + $5.00) = $2.50

D) $10.00 - ($1.50 + $5.00) = $3.50

Division A sells potatoes internally to Division B, which in turn, produces chips that sell for $10 per pound. Division A incurs costs of $1.50 per pound while Division B incurs additional costs of $5.00 per pound.

-Which of the following formulas correctly reflects the company's operating income per pound?

A) $10.00 - ($0.50 + $2.50 + $7.00) = 0

B) $10.00 - ($1.50 + $7.50) = $1.00

C) $10.00 - ($2.50 + $5.00) = $2.50

D) $10.00 - ($1.50 + $5.00) = $3.50

$10.00 - ($1.50 + $5.00) = $3.50

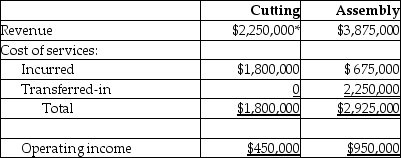

Salleh's Sheet Metal Company has two divisions. The Raw Material Division prepares sheet metal at its warehouse facility. The Fabrication Division prepares the cut sheet metal into finished products for the air conditioning industry. No inventories exist in either division at the beginning of 2014. During the year, the Raw Material Division prepared 450,000 square feet of sheet metal at a cost of $1,800,000. All the sheet metal was transferred to the Fabrication Division, where additional operating costs of $1.50 per square foot were incurred. The 450,000 square feet of finished fabricated sheet metal products were sold for $3,875,000.

Required:

a. Determine the operating income for each division if the transfer price from Raw Material to Fabrication is at a cost of $4 per square foot.

b. Determine the operating income for each division if the transfer price is $5 per square foot.

c. Since the Raw Materials Division sells all of its sheet metal internally to the Fabrication Division, does the Raw Materials manager care what price is selected? Why? Should the Raw Materials Division be a cost center or a profit center under the circumstances?

Required:

a. Determine the operating income for each division if the transfer price from Raw Material to Fabrication is at a cost of $4 per square foot.

b. Determine the operating income for each division if the transfer price is $5 per square foot.

c. Since the Raw Materials Division sells all of its sheet metal internally to the Fabrication Division, does the Raw Materials manager care what price is selected? Why? Should the Raw Materials Division be a cost center or a profit center under the circumstances?

a.

* 60,000 cords × $11 = $660,000

* 60,000 cords × $11 = $660,000

b.

* 60,000 cords × $9 = $540,000

* 60,000 cords × $9 = $540,000

c. The manager of Raw materials cares about the transfer price if the division is a profit center but not if it is a cost center. Under the circumstances, the division probably should be a cost center and should not worry about the profit it pretends to make by selling to another division.

* 60,000 cords × $11 = $660,000b.

* 60,000 cords × $9 = $540,000c. The manager of Raw materials cares about the transfer price if the division is a profit center but not if it is a cost center. Under the circumstances, the division probably should be a cost center and should not worry about the profit it pretends to make by selling to another division.

Soft Cushion Company is highly decentralized. Each division is empowered to make its own sales decisions. The Assembly Division can purchase stuffing, a key component, from the Production Division or from external suppliers. The Production Division has been the major supplier of stuffing in recent years. The Assembly Division has announced that two external suppliers will be used to purchase the stuffing at $20 per pound for the next year. The Production Division recently increased its unit price to $40. The manager of the Production Division presented the following information - variable cost $32 and fixed cost $8 - to top management in order to attempt to force the Assembly Division to purchase the stuffing internally. The Assembly Division purchases 20,000 pounds of stuffing per month.

What would be the monthly operating advantage (disadvantage) of purchasing the goods internally, assuming the external supplier increased its price to $50 per pound and the Production Division is able to utilize the facilities for other operations, resulting in a monthly cash-operating savings of $30 per pound?

A) $(240,000)

B) $1,000,000

C) $(400,000)

D) $360,000

What would be the monthly operating advantage (disadvantage) of purchasing the goods internally, assuming the external supplier increased its price to $50 per pound and the Production Division is able to utilize the facilities for other operations, resulting in a monthly cash-operating savings of $30 per pound?

A) $(240,000)

B) $1,000,000

C) $(400,000)

D) $360,000

$(240,000)

Unlock Deck

Unlock for access to all 3 flashcards in this deck.