Deck 15: Competitive Markets in the Long Run

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

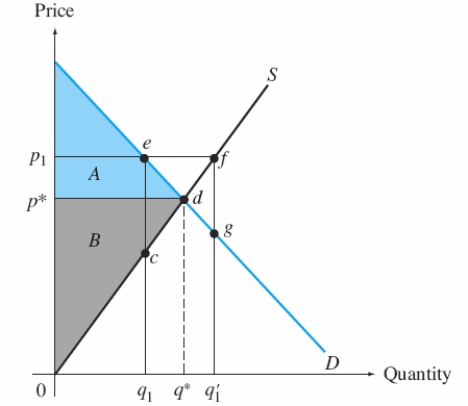

Refer to Exhibit 15-1. Which quantity minimizes deadweight loss to society?

A) q1

B) q*

C) q1'

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/40

Play

Full screen (f)

Deck 15: Competitive Markets in the Long Run

1

Constant-cost rent is the average cost of the firm when economic rent is included as a cost.

False

2

As long as firms in a perfectly competitive industry earn extra-normal profits, other firms will be attracted and will decide to enter the industry.

True

3

In constant-cost industires, the long-run supply curve is flat.

True

4

Pecuniary externalities exist when the action of one agent increases the price of a good to other agents.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

5

Which of the following is the third step in deriving a flat long-run supply curve?

A) market demand increases

B) market supply increases until price returns to the original value

C) firms earn extra-normal profits

A) market demand increases

B) market supply increases until price returns to the original value

C) firms earn extra-normal profits

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

6

In the long run, a firm has enough time to adjust ___________ factors of production to meet any level of demand.

A) all

B) only one

C) no

A) all

B) only one

C) no

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

7

In a long-run equilibrium in a perfectly competitive industry, no firm will want to

A) exit the industry because it is earning an amount at least equal to its opportunity cost

B) enter the industry because it will not be able to make extra-normal profits

C) Both answers are correct

A) exit the industry because it is earning an amount at least equal to its opportunity cost

B) enter the industry because it will not be able to make extra-normal profits

C) Both answers are correct

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

8

When new firms enter an industry, the supply curve

A) does not shift

B) shifts to the right

C) shifts to the left

A) does not shift

B) shifts to the right

C) shifts to the left

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

9

In the long run, when demand increases, equilibrium price unambiguously goes

A) up

B) down

C) Neither answer is correct

A) up

B) down

C) Neither answer is correct

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

10

At a price above the perfectly competitive equilibrium, society will suffer a deadweight loss.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

11

A long-run equilibrium is one price-quantity combination that exists as a perfectly competitive market moves from the short run to the long run.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

12

The average cost of the firm when economic rent is included as a cost is called

A) rent-exclusive average cost

B) rent-controlled fixed cost

C) rent-inclusive average cost

A) rent-exclusive average cost

B) rent-controlled fixed cost

C) rent-inclusive average cost

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

13

At the long-run equilibrium of a perfectly competitive industry, price is set so that it is greater than marginal cost.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

14

Decreasing-cost industries have a long-run cost curve that is downward sloping.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

15

Which of the following does not characterize long-run equilibrium?

A) No individual firm wishes to change the amount of the good it is supplying to the market

B) At least one firm in the market has an incentive to change the amount of one of the inputs it is using

C) The aggregate supply in the market equals the aggregate demand for the good

A) No individual firm wishes to change the amount of the good it is supplying to the market

B) At least one firm in the market has an incentive to change the amount of one of the inputs it is using

C) The aggregate supply in the market equals the aggregate demand for the good

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

16

The return to a factor of production over and above what is needed to secure the services of that factor is known as economic rent.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

17

In a long-run perfectly competitive equilibrium with heterogeneous firms, the market price __________ driven down to the bottom of each firm's average cost curve.

A) may not be

B) must be

C) will never be

A) may not be

B) must be

C) will never be

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

18

The country of Delta has two electricity-generating plants. One is located near a dam that has a reservoir that can be used to generate electricity hydroelectrically. The other plant must burn high-priced oil to generate power. Which firm should have the lower LRAC?

A) the hydroelectric plant

B) the oil-burning plant

C) There is not enough information to answer the question

A) the hydroelectric plant

B) the oil-burning plant

C) There is not enough information to answer the question

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

19

Industries with a long-run cost curve that is upward sloping are increasing-cost industries.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

20

The price-quantity combination that will prevail in a perfectly competitive market in the long run is called

A) short-run equilibrium

B) Nash equilibrium

C) long-run equilibrium

A) short-run equilibrium

B) Nash equilibrium

C) long-run equilibrium

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

21

For a constant-cost industry,

A) the industry must consume a large share of the inputs in the market

B) the entry of one additional firm causes a pecuniary externality

C) inputs must be in abundant supply

A) the industry must consume a large share of the inputs in the market

B) the entry of one additional firm causes a pecuniary externality

C) inputs must be in abundant supply

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

22

At the long-run equilibrium of a perfectly competitive industry, price is set so that it is equal to

A) average fixed cost

B) average total cost

C) marginal cost

A) average fixed cost

B) average total cost

C) marginal cost

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

23

You own a firm that possesses some special factor that gives you a cost advantage. Why would you incur an opportunity cost for holding this special factor?

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

24

In a perfectly competitive industry over the long run, competition ensures that goods sold to consumers will be produced at _____________________ cost.

A) the lowest possible

B) zero

C) the highest possible

A) the lowest possible

B) zero

C) the highest possible

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

25

An industry's long-run supply curve will be flat if inputs are in abundant supply and if the industry consumes only a small share of the inputs in the market. Why?

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

26

At the long-run equilibrium of a perfectly competitive industry, the sum of consumer surplus and producer surplus is

A) minimized

B) maximized

C) equal to the deadweight loss

A) minimized

B) maximized

C) equal to the deadweight loss

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

27

Each firm in a competitive industry finds its optimal quantity to produce by setting its marginal cost to be _______________ the market price.

A) greater than

B) equal to

C) less than

A) greater than

B) equal to

C) less than

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

28

Perfect competition

A) ensures that the goods sold to consumers will be produced at the lowest possible cost

B) leads to the efficient organization of production

C) Both answers are correct

A) ensures that the goods sold to consumers will be produced at the lowest possible cost

B) leads to the efficient organization of production

C) Both answers are correct

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

29

What is the difference between how economic planners and a perfectly competitive market would allocate production in an industry?

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

30

Perfectly competitive markets will set a price and quantity at which the deadweight loss to society is

A) zero

B) small

C) very large

A) zero

B) small

C) very large

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

31

Refer to Exhibit 15-1. Which quantity minimizes deadweight loss to society?

A) q1

B) q*

C) q1'

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

32

In long-run equilibrium for a perfectly competitive market, no firm earns extra-normal profits. Describe why firms that earn zero extra-normal profits would stay in business.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

33

A price that is set at the intersection of the supply and demand curves must be _______________ the marginal cost.

A) greater than

B) less than

C) equal to

A) greater than

B) less than

C) equal to

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

34

Industries in which the long-run supply curve is upward sloping are

A) constant-cost industries

B) increasing-cost industries

C) decreasing-cost industries

A) constant-cost industries

B) increasing-cost industries

C) decreasing-cost industries

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

35

At the long-run equilibrium of a competitive industry, goods are produced at ______________________ average cost.

A) zero

B) the highest possible

C) the lowest possible

A) zero

B) the highest possible

C) the lowest possible

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

36

What does it mean to say that society experiences a deadweight loss when markets are organized as monopolies?

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

37

The market structure that is optimal in terms of welfare and that produces goods in the most efficient manner is

A) perfect competition

B) monopoly

C) oligopoly

A) perfect competition

B) monopoly

C) oligopoly

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

38

The ideal for which economists aim is the market structure of

A) oligopoly

B) perfect competition

C) monopoly

A) oligopoly

B) perfect competition

C) monopoly

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

39

Industries in which the long-run supply curve is downward sloping are

A) constant-cost industries

B) increasing-cost industries

C) decreasing-cost industries

A) constant-cost industries

B) increasing-cost industries

C) decreasing-cost industries

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

40

Industries in which the long-run supply curve is flat are

A) constant-cost industries

B) increasing-cost industries

C) decreasing-cost industries

A) constant-cost industries

B) increasing-cost industries

C) decreasing-cost industries

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 40 flashcards in this deck.