Deck 12: Principles of Capital Structure

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

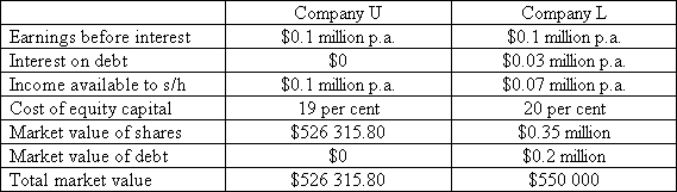

Given the following data,a suitable arbitrage opportunity for an investor with a 2% share in Company L would be to:

A)sell 1% shares in L,borrow on personal account and invest in shares of L.

B)borrow on personal account and buy more shares in L.

C)sell shares in L and buy 2% shares in U.

D)sell shares in L and buy 1% shares in U.

A)sell 1% shares in L,borrow on personal account and invest in shares of L.

B)borrow on personal account and buy more shares in L.

C)sell shares in L and buy 2% shares in U.

D)sell shares in L and buy 1% shares in U.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/57

Play

Full screen (f)

Deck 12: Principles of Capital Structure

1

A key assumption of the MM arbitrage argument is:

A)that business risk is not altered by capital structure.

B)companies and individuals can borrow at the same interest rate.

C)financial risk is unaltered by capital structure.

D)expected return and risk are positively correlated.

A)that business risk is not altered by capital structure.

B)companies and individuals can borrow at the same interest rate.

C)financial risk is unaltered by capital structure.

D)expected return and risk are positively correlated.

companies and individuals can borrow at the same interest rate.

2

Which of the following statements is false?

A)With all-equity companies,the rate of return to shareholders is always equal to the rate of return on assets.

B)With debt,the rate of return to shareholders is always equal to the rate of return on assets providing the rate of return on assets is equal to the interest rate.

C)If the rate of return on assets is greater than the interest on debt,then leverage results in lower rates of return on equity.

D)If the rate of return on assets is less than the interest rate on debt,then leverage results in lower rates of return on equity.

A)With all-equity companies,the rate of return to shareholders is always equal to the rate of return on assets.

B)With debt,the rate of return to shareholders is always equal to the rate of return on assets providing the rate of return on assets is equal to the interest rate.

C)If the rate of return on assets is greater than the interest on debt,then leverage results in lower rates of return on equity.

D)If the rate of return on assets is less than the interest rate on debt,then leverage results in lower rates of return on equity.

If the rate of return on assets is greater than the interest on debt,then leverage results in lower rates of return on equity.

3

Which of the following statements on financial leverage is true?

A)Financial leverage has no effect on expected return to ordinary shareholders.

B)Expected return to ordinary shareholders increases because return on borrowings is expected to exceed the cost of borrowings.

C)Expected return to ordinary shareholders increases because the return on assets increases.

D)Financial leverage may have a positive or negative effect on return to ordinary shareholders.

A)Financial leverage has no effect on expected return to ordinary shareholders.

B)Expected return to ordinary shareholders increases because return on borrowings is expected to exceed the cost of borrowings.

C)Expected return to ordinary shareholders increases because the return on assets increases.

D)Financial leverage may have a positive or negative effect on return to ordinary shareholders.

Financial leverage may have a positive or negative effect on return to ordinary shareholders.

4

Which theory proposes that companies follow a hierarchy of financing sources?

A)Trade-off theory.

B)Reverse pecking order theory.

C)Pecking order theory.

D)Information asymmetry theory.

A)Trade-off theory.

B)Reverse pecking order theory.

C)Pecking order theory.

D)Information asymmetry theory.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

5

A company is said to be in a state of financial distress:

A)when its cost of equity capital is too high.

B)when its cost of debt capital is high.

C)when the D/E exceeds 25 per cent.

D)when it incurs problems in meeting its commitments to lenders.

A)when its cost of equity capital is too high.

B)when its cost of debt capital is high.

C)when the D/E exceeds 25 per cent.

D)when it incurs problems in meeting its commitments to lenders.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

6

Calculate EPS if a company,with 1 million shares with a market price of $4 each and zero debt,decides to buy back 25 per cent of its outstanding shares by borrowing at 10% p.a.Assume current earnings are $0.4 million and taxes do not apply.

A)$4

B)53.3c

C)40c

D)66.6c

A)$4

B)53.3c

C)40c

D)66.6c

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

7

Financial leverage is the relationship between:

A)borrowings and equity.

B)borrowings and liabilities.

C)debt to assets.

D)gearing and assets.

A)borrowings and equity.

B)borrowings and liabilities.

C)debt to assets.

D)gearing and assets.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

8

Which theory proposes that companies have an optimal capital structure based on a trade-off between the benefits and costs of using debt?

A)Trade-off theory.

B)Reverse pecking order theory.

C)Information asymmetry theory.

D)Pecking order theory.

A)Trade-off theory.

B)Reverse pecking order theory.

C)Information asymmetry theory.

D)Pecking order theory.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

9

All companies are subject to:

A)financial risk.

B)technology risk.

C)business risk.

D)all of the given options.

A)financial risk.

B)technology risk.

C)business risk.

D)all of the given options.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

10

The chance that a borrower will fail to meet obligations to pay interest and principal as promised is known as:

A)natural conservation of risk.

B)credit risk.

C)default risk.

D)business risk.

A)natural conservation of risk.

B)credit risk.

C)default risk.

D)business risk.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

11

If a company is financed entirely by equity then variations in the return to shareholders are attributable only to:

A)financial risk.

B)business risk.

C)technology risk.

D)diversifiable risk.

A)financial risk.

B)business risk.

C)technology risk.

D)diversifiable risk.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

12

Financial leverage exposes shareholders to financial risk because:

A)competition forces companies to adopt an optimal capital structure.

B)a company uses debt to increase the expected rate of return to shareholders.

C)interest on debt needs to be paid even when operating performance declines.

D)none of the given options.

A)competition forces companies to adopt an optimal capital structure.

B)a company uses debt to increase the expected rate of return to shareholders.

C)interest on debt needs to be paid even when operating performance declines.

D)none of the given options.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

13

Under the MM theorem,capital structure will not change the total value of a firm because:

A)EPS is not affected by leverage.

B)two firms with the same assets but different capital structures are not considered perfect substitutes.

C)dividend policy is irrelevant.

D)perfect substitutes should not sell at different prices in the same market.

A)EPS is not affected by leverage.

B)two firms with the same assets but different capital structures are not considered perfect substitutes.

C)dividend policy is irrelevant.

D)perfect substitutes should not sell at different prices in the same market.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

14

A company with low financial leverage,large reserve borrowing capacity and few profitable investment opportunities is likely to:

A)have a high cost of capital.

B)generate larger free cash flows.

C)generate smaller free cash flows.

D)have a high cost of debt.

A)have a high cost of capital.

B)generate larger free cash flows.

C)generate smaller free cash flows.

D)have a high cost of debt.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

15

When considering a firm's capital structure,a financial manager must:

A)make sure that business conditions are good when changing the level of debt.

B)balance the benefits of increased expected returns with increased financial risk.

C)be extra cautious during periods when the rate of return on assets is greater than the interest rate on debt.

D)seek to reduce debt at all costs.

A)make sure that business conditions are good when changing the level of debt.

B)balance the benefits of increased expected returns with increased financial risk.

C)be extra cautious during periods when the rate of return on assets is greater than the interest rate on debt.

D)seek to reduce debt at all costs.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

16

MM Proposition I states that:

A)the value of a company depends on its capital structure.

B)the value of a company depends on the debt to assets ratio.

C)the value of a company depends on the debt to total assets ratio.

D)the value of a company is independent of its capital structure.

A)the value of a company depends on its capital structure.

B)the value of a company depends on the debt to assets ratio.

C)the value of a company depends on the debt to total assets ratio.

D)the value of a company is independent of its capital structure.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

17

Financial risk comes about when:

A)new competitors emerge.

B)new government regulations are introduced.

C)the dividend payout ratio is increased.

D)a company uses fixed-charge finance.

A)new competitors emerge.

B)new government regulations are introduced.

C)the dividend payout ratio is increased.

D)a company uses fixed-charge finance.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

18

MM Proposition II is based on the:

A)law of conservation of value.

B)expected return theory.

C)risk-return theory.

D)natural conservation of risk.

A)law of conservation of value.

B)expected return theory.

C)risk-return theory.

D)natural conservation of risk.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

19

Which of the following is true of debt?

A)Variation in expected EPS increases as the level of debt increases.

B)Variation in expected EPS increases as the level of debt decreases.

C)Variation in expected EPS is not affected as the level of debt increases.

D)Variation in expected EPS decreases as the level of debt increases.

A)Variation in expected EPS increases as the level of debt increases.

B)Variation in expected EPS increases as the level of debt decreases.

C)Variation in expected EPS is not affected as the level of debt increases.

D)Variation in expected EPS decreases as the level of debt increases.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

20

Arbitrage refers to:

A)the ability to make a profit.

B)the ability to make a risk-free profit resulting from mispriced securities.

C)settling of disputes between management and shareholders.

D)none of the given options.

A)the ability to make a profit.

B)the ability to make a risk-free profit resulting from mispriced securities.

C)settling of disputes between management and shareholders.

D)none of the given options.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

21

A company's cost of capital is the:

A)amount of interest paid on borrowings.

B)minimum rate of return on assets needed to maintain company value.

C)rate of return required by shareholders.

D)bank overdraft rate.

A)amount of interest paid on borrowings.

B)minimum rate of return on assets needed to maintain company value.

C)rate of return required by shareholders.

D)bank overdraft rate.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

22

Under the MM 'law of conservation of value',a company's cost of capital:

A)reaches its lowest value when it operates at its optimal capital structure.

B)increases as the proportional amount of debt increases.

C)remains unchanged as the proportional amount of debt increases.

D)decreases as the proportional amount of debt increases.

A)reaches its lowest value when it operates at its optimal capital structure.

B)increases as the proportional amount of debt increases.

C)remains unchanged as the proportional amount of debt increases.

D)decreases as the proportional amount of debt increases.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

23

With the introduction of risky debt,MM argues that the:

A)cost of equity increases at a decreasing rate as the debt/equity ratio increases beyond a certain level.

B)cost of equity continues to increase as the debt/equity ratio increases.

C)cost of debt increases at a decreasing rate as the debt/equity ratio increases beyond a certain level.

D)company cost of capital increases as the debt/equity ratio increases beyond a certain level.

A)cost of equity increases at a decreasing rate as the debt/equity ratio increases beyond a certain level.

B)cost of equity continues to increase as the debt/equity ratio increases.

C)cost of debt increases at a decreasing rate as the debt/equity ratio increases beyond a certain level.

D)company cost of capital increases as the debt/equity ratio increases beyond a certain level.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

24

Which statement is false regarding capital structure under dividend imputation?

A)Misleading results regarding the gain from leverage may appear if a company is not at its optimal dividend policy.

B)Dividend policy decisions are probably more important than capital structure decisions.

C)It is not possible to have a negative gain from leverage.

D)If the dividend payout ratio is 1,a gain from leverage may result,providing that investors with equal marginal tax rates hold equity and debt.

A)Misleading results regarding the gain from leverage may appear if a company is not at its optimal dividend policy.

B)Dividend policy decisions are probably more important than capital structure decisions.

C)It is not possible to have a negative gain from leverage.

D)If the dividend payout ratio is 1,a gain from leverage may result,providing that investors with equal marginal tax rates hold equity and debt.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

25

A false example of financial distress is:

A)problems in meeting debt commitments.

B)company liquidation.

C)introduction of new competitors.

D)appointment of receiver/manager.

A)problems in meeting debt commitments.

B)company liquidation.

C)introduction of new competitors.

D)appointment of receiver/manager.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

26

A limitation of the MM analysis in the absence of taxes is that:

A)risky debt is not considered.

B)the possibility of default on debt is not considered.

C)there is no cost associated with default on debt.

D)only risk-free debt is considered.

A)risky debt is not considered.

B)the possibility of default on debt is not considered.

C)there is no cost associated with default on debt.

D)only risk-free debt is considered.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

27

Given the following data,a suitable arbitrage opportunity for an investor with a 2% share in Company L would be to:

A)sell 1% shares in L,borrow on personal account and invest in shares of L.

B)borrow on personal account and buy more shares in L.

C)sell shares in L and buy 2% shares in U.

D)sell shares in L and buy 1% shares in U.

A)sell 1% shares in L,borrow on personal account and invest in shares of L.

B)borrow on personal account and buy more shares in L.

C)sell shares in L and buy 2% shares in U.

D)sell shares in L and buy 1% shares in U.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

28

The 'traditional view' of capital structure argues that:

A)a company's overall cost of capital can be reduced by financial leverage provided that the degree of leverage is not too great.

B)the cost of capital is unaltered by using 'cheaper debt'.

C)a company's cost of capital increases as more debt is used in its capital structure.

D)a firm's value is independent of its capital structure.

A)a company's overall cost of capital can be reduced by financial leverage provided that the degree of leverage is not too great.

B)the cost of capital is unaltered by using 'cheaper debt'.

C)a company's cost of capital increases as more debt is used in its capital structure.

D)a firm's value is independent of its capital structure.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

29

Calculate the cost of equity capital from the following data: cost of debt = 12%,D = $0.2 million,E = $0.3 million,and the increment for financial risk = 4%.

A)16.8%

B)14.8%

C)18.7%

D)15.2%

A)16.8%

B)14.8%

C)18.7%

D)15.2%

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

30

When considering personal taxes (but ignoring imputation):

A)effectively,the marginal tax rate on share income is greater than on debt income.

B)the tax deductibility of interest could never be fully offset by the tax differential on income to debtholders and shareholders.

C)the benefit of the tax deductibility of interest may be offset by the fact that investors need to be compensated for the higher personal tax on income to debtholders than shareholders.

D)tax paid on company income is zero.

A)effectively,the marginal tax rate on share income is greater than on debt income.

B)the tax deductibility of interest could never be fully offset by the tax differential on income to debtholders and shareholders.

C)the benefit of the tax deductibility of interest may be offset by the fact that investors need to be compensated for the higher personal tax on income to debtholders than shareholders.

D)tax paid on company income is zero.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

31

Given the total value of a levered firm is represented by Vu + tcD,and is equal to $1 million,find D.Assume the total value of an equivalent unlevered firm is $0.8 million and the company tax rate is 30 per cent.

A)$0.24 million

B)$0.30 million

C)$0.20 million

D)$0.67 million

A)$0.24 million

B)$0.30 million

C)$0.20 million

D)$0.67 million

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

32

From the following data,calculate the company's cost of capital: annual earnings = $0.2 million,total market value of company = $0.5 million,total value of debt = 0,interest on debt = 12% p.a.

A)28%

B)4.8%

C)12%

D)40%

A)28%

B)4.8%

C)12%

D)40%

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

33

Other things being equal,as the tax deductibility of depreciation on assets increases:

A)the firm borrows more.

B)the firm borrows less.

C)there will be no effect on the firm's borrowings.

D)the firm's effective tax rate decreases.

A)the firm borrows more.

B)the firm borrows less.

C)there will be no effect on the firm's borrowings.

D)the firm's effective tax rate decreases.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

34

Which of the following statements is true?

A)Bankruptcy costs do not concern shareholders because they are borne entirely by other parties.

B)Debtholders rarely realise the potential for bankruptcy and do not demand a higher rate of interest on their loans in compensation.

C)Debtholders will not demand higher interest rates on loans because in so doing they may increase the likelihood of bankruptcy.

D)For any given level of business risk,the higher the financial risk,the greater the probability of bankruptcy.

A)Bankruptcy costs do not concern shareholders because they are borne entirely by other parties.

B)Debtholders rarely realise the potential for bankruptcy and do not demand a higher rate of interest on their loans in compensation.

C)Debtholders will not demand higher interest rates on loans because in so doing they may increase the likelihood of bankruptcy.

D)For any given level of business risk,the higher the financial risk,the greater the probability of bankruptcy.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

35

Which of the following statements is not true regarding Miller's analysis?

A)There is an optimal debt/equity ratio for the corporate sector.

B)There is no optimal debt/equity ratio for individual companies.

C)Shareholders benefit from the tax saving of interest on debt.

D)Securities issued by different companies will appeal to different clientele.

A)There is an optimal debt/equity ratio for the corporate sector.

B)There is no optimal debt/equity ratio for individual companies.

C)Shareholders benefit from the tax saving of interest on debt.

D)Securities issued by different companies will appeal to different clientele.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

36

Calculate the cost of debt from the following information: company cost of capital = 15%,cost of equity capital = 16 per cent,D = $0.2 million,and V = $0.5 million.

A)12.5%

B)13.5%

C)10.5%

D)15.5%

A)12.5%

B)13.5%

C)10.5%

D)15.5%

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

37

From the following data,calculate the total market value of the firm.Earnings before interest = $0.1 million,D = $0.2 million,interest on debt = 10% p.a. ,cost of equity capital = 20%,the dividend payout ratio = 0.5,and assume no taxes.

A)$200 000

B)$500 000

C)$473 684

D)$400 000

A)$200 000

B)$500 000

C)$473 684

D)$400 000

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

38

Which of the following statements is true concerning debt that has no risk of default?

A)A company's cost of capital increases as more debt is used in its capital structure.

B)The cost of debt increases as more debt is used in the company's capital structure.

C)The cost of debt increases as more debt is used in the company's capital structure because total risk increases.

D)The cost of equity capital increases with increasing proportions of debt because,although the total amount of risk does not change,risk is concentrated on a proportionately smaller amount of equity capital.

A)A company's cost of capital increases as more debt is used in its capital structure.

B)The cost of debt increases as more debt is used in the company's capital structure.

C)The cost of debt increases as more debt is used in the company's capital structure because total risk increases.

D)The cost of equity capital increases with increasing proportions of debt because,although the total amount of risk does not change,risk is concentrated on a proportionately smaller amount of equity capital.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

39

Borrowing can add value for companies with high effective tax rates because:

A)borrowing increases total taxes.

B)the company is likely to use tax savings associated with debt.

C)the company tax saved from borrowing is equal to the additional personal tax paid.

D)the company tax saved from borrowing is less than the additional personal tax paid.

A)borrowing increases total taxes.

B)the company is likely to use tax savings associated with debt.

C)the company tax saved from borrowing is equal to the additional personal tax paid.

D)the company tax saved from borrowing is less than the additional personal tax paid.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

40

Earnings before interest = $0.5 million,D = $1 million,cost of debt = 10%,and company tax rate = 30%.What is the present value of the tax saving on interest?

A)$700 000

B)$300 000

C)$30 000

D)$70 000

A)$700 000

B)$300 000

C)$30 000

D)$70 000

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

41

Jensen's Free Cash Flow theory argues that the use of debt financing can add value by forcing managers to pay out cash that might otherwise be wasted.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

42

The effect of debt on the rate of return earned by shareholders of the company is known as _____________________.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

43

The separation of ownership from control creates agency costs because:

A)schemes,such as employee ownership schemes,align employee interests with those of the owners.

B)employees are likely to act in their own interest rather than that of the owners.

C)the threat of retrenchment serves to align the interests of management and owners.

D)the threat of a possible takeover serves to align the interests of management and owners.

A)schemes,such as employee ownership schemes,align employee interests with those of the owners.

B)employees are likely to act in their own interest rather than that of the owners.

C)the threat of retrenchment serves to align the interests of management and owners.

D)the threat of a possible takeover serves to align the interests of management and owners.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

44

The ___________ theory establishes a hierarchy of financing sources which are preferred by the managers of a company.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

45

The proportion of debt and equity financing used by a company is known as its ____________________.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

46

Which of the following is not an example of agency costs between debt and equity?

A)A company issues new debt,which ranks equal or higher than existing debt.

B)A company issues new equity.

C)A company significantly increases its dividend payout ratio.

D)A company rejects low-risk investments with positive NPV.

A)A company issues new debt,which ranks equal or higher than existing debt.

B)A company issues new equity.

C)A company significantly increases its dividend payout ratio.

D)A company rejects low-risk investments with positive NPV.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

47

Which of the following statements generally gives the correct order in which management choose amongst alternatives to finance projects?

A)(1)Retained earnings;(2)ordinary shares;(3)debt;and (4)convertible debt

B)(1)Retained earnings;(2)debt;(3)convertible debt;and (4)ordinary shares

C)(1)Retained earnings;(2)convertible debt;(3)ordinary shares;and (4)debt

D)(1)Convertible debt;(2)ordinary shares;(3)debt;and (4)retained earnings

A)(1)Retained earnings;(2)ordinary shares;(3)debt;and (4)convertible debt

B)(1)Retained earnings;(2)debt;(3)convertible debt;and (4)ordinary shares

C)(1)Retained earnings;(2)convertible debt;(3)ordinary shares;and (4)debt

D)(1)Convertible debt;(2)ordinary shares;(3)debt;and (4)retained earnings

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

48

Lenders may seek to protect themselves from agency costs by requiring that ____________ be included in loan agreements.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

49

The pecking order theory helps to explain why companies:

A)pursue a target debt/equity ratio.

B)issue ordinary shares as a last resort to finance investments.

C)will issue debt following a substantial increase in its share price.

D)do not issue new shares.

A)pursue a target debt/equity ratio.

B)issue ordinary shares as a last resort to finance investments.

C)will issue debt following a substantial increase in its share price.

D)do not issue new shares.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

50

Miller and Modigliani's Proposition 1 states that the dollar value of a company is independent of its capital structure.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

51

____________ costs are costs associated with a formal transfer of control to lenders.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

52

The trade-off theory suggests that a company should use as much debt in its capital structure as possible,given the tax advantages of the use of debt financing.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

53

An example of adverse incentive effects of debt is:

A)an increase in the dividend payout ratio.

B)an appointment of a liquidator.

C)disgruntled employees taking sick leave.

D)none of the given options.

A)an increase in the dividend payout ratio.

B)an appointment of a liquidator.

C)disgruntled employees taking sick leave.

D)none of the given options.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

54

The imputation tax system essentially removes all tax advantages of debt.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

55

The agency costs of equity increase:

A)when management acts in its own interest.

B)as the fraction of debt in a company's capital structure increases.

C)as the fraction of equity owned by outside shareholders increases.

D)when management acts in the interest of debtholders.

A)when management acts in its own interest.

B)as the fraction of debt in a company's capital structure increases.

C)as the fraction of equity owned by outside shareholders increases.

D)when management acts in the interest of debtholders.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

56

The use of equity financing creates a tax shield that results in a significant reduction in a company's tax liability.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

57

A trade-off between the benefits of debt finance and the costs of financial distress may lead to a company increasing its debt/equity ratio because:

A)of the low probability of encountering severe financial difficulties.

B)its existing debt/equity ratio is high.

C)the expected increase in financial distress is expected to outweigh the tax benefits.

D)agency costs of equity increase as the level of debt increases.

A)of the low probability of encountering severe financial difficulties.

B)its existing debt/equity ratio is high.

C)the expected increase in financial distress is expected to outweigh the tax benefits.

D)agency costs of equity increase as the level of debt increases.

Unlock Deck

Unlock for access to all 57 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 57 flashcards in this deck.