Deck 20: Time-Series Analytics and Forecasting

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

In measuring seasonal and random variation of a time series with no cyclical effect,we may use the:

A)ratio of the time series divided by the moving average

B)ratio of the time series divided by the predicted values

C)trend value

D)Both a and b

A)ratio of the time series divided by the moving average

B)ratio of the time series divided by the predicted values

C)trend value

D)Both a and b

Question

Question

Question

The way a seasonal index is computed involves which of the following steps?

A)Remove the effect of seasonal and random variation by regression analysis.

B)For each time period,compute the ratio, which removes most of the trend variation for that time period.

which removes most of the trend variation for that time period.

C)Calculate the average of all the ratios: over all time periods to remove random variation and leaving a measure of seasonality.

over all time periods to remove random variation and leaving a measure of seasonality.

D)All of these choices are true.

A)Remove the effect of seasonal and random variation by regression analysis.

B)For each time period,compute the ratio,

which removes most of the trend variation for that time period.C)Calculate the average of all the ratios:

over all time periods to remove random variation and leaving a measure of seasonality.D)All of these choices are true.

Question

Question

The trend line  = 0.70 + 0.005t was calculated from quarterly data for 2000-2004,where t = 1 for the first quarter of 2000.The trend value for the second quarter of the year 2005 is:

= 0.70 + 0.005t was calculated from quarterly data for 2000-2004,where t = 1 for the first quarter of 2000.The trend value for the second quarter of the year 2005 is:

A)0.705

B)0.820

C)0.815

D)0.810

= 0.70 + 0.005t was calculated from quarterly data for 2000-2004,where t = 1 for the first quarter of 2000.The trend value for the second quarter of the year 2005 is:A)0.705

B)0.820

C)0.815

D)0.810

Question

Question

Question

The time-series model yt = Tt×Ct×St×Rt is used for forecasting,where Tt,Ct,St,and Rt are respectively the trend,cyclical,seasonal,and random variation components of the time series,and yt is the value of the time series at time t.The following estimates are obtained:  = 120,

= 120,  = 1.02,

= 1.02,  = 0.95,and

= 0.95,and  = 0.90.The model will produce a forecast of:

= 0.90.The model will produce a forecast of:

A)122.870

B)104.652

C)116.280

D)102.600

= 120, = 1.02, = 0.95,and = 0.90.The model will produce a forecast of:A)122.870

B)104.652

C)116.280

D)102.600

Question

Question

The linear trend  = 115.8 + 2.5t was estimated using a time series with 25 time periods.The forecasted value for time period 26 is:

= 115.8 + 2.5t was estimated using a time series with 25 time periods.The forecasted value for time period 26 is:

A)180.8

B)178.3

C)175.8

D)Not enough information given to answer this question.

= 115.8 + 2.5t was estimated using a time series with 25 time periods.The forecasted value for time period 26 is:A)180.8

B)178.3

C)175.8

D)Not enough information given to answer this question.

Question

Question

Question

Question

The following are the values of a time series for the first four time periods:  Using a four-period moving average,the forecasted value for time period 5 is:

Using a four-period moving average,the forecasted value for time period 5 is:

A)25.3

B)25.7

C)25.0

D)26.0

Using a four-period moving average,the forecasted value for time period 5 is:A)25.3

B)25.7

C)25.0

D)26.0

Question

Question

The following are the values of a time series for the first four time periods:  Using exponential smoothing,with w = 0.30,the forecasted value for time period 5 is:

Using exponential smoothing,with w = 0.30,the forecasted value for time period 5 is:

A)24.920

B)24.644

C)23.600

D)23.000

Using exponential smoothing,with w = 0.30,the forecasted value for time period 5 is:A)24.920

B)24.644

C)23.600

D)23.000

Question

Question

Question

Suppose that we calculate the four-period moving average of the following time series  The centered moving average for period 3 is:

The centered moving average for period 3 is:

A)22.5

B)21.25

C)20.50

D)18.5

The centered moving average for period 3 is:A)22.5

B)21.25

C)20.50

D)18.5

Question

Question

Question

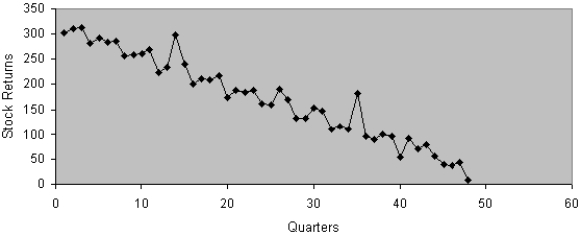

Based on the following scatter plot,which of the time-series components is not present in this quarterly time series?

A)Long-term trend

B)Cyclical variation

C)Seasonal variation

D)Random variation

A)Long-term trend

B)Cyclical variation

C)Seasonal variation

D)Random variation

Question

After estimating a trend model for annual time-series data,you obtain the following residual plot against time.  The problem with your model is that:

The problem with your model is that:

A)the cyclical component has not been accounted for

B)the seasonal component has not been accounted for

C)the trend component has not been accounted for

D)the irregular component has not been accounted for

The problem with your model is that:A)the cyclical component has not been accounted for

B)the seasonal component has not been accounted for

C)the trend component has not been accounted for

D)the irregular component has not been accounted for

Question

Question

Question

Question

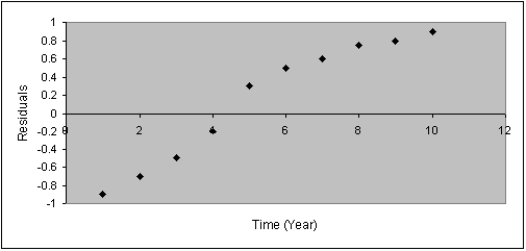

After estimating a trend model for annual time-series data,you obtain the following residual plot against time.  The problem with your model is that:

The problem with your model is that:

A)the cyclical component has not been accounted for

B)the seasonal component has not been accounted for

C)the trend component has not been accounted for

D)the irregular component has not been accounted for

The problem with your model is that:A)the cyclical component has not been accounted for

B)the seasonal component has not been accounted for

C)the trend component has not been accounted for

D)the irregular component has not been accounted for

Question

Question

Question

Question

Question

Question

Liquor Sales

The number of cases of liquor sold by a liquor wholesaler in an 8-year period follows.

{Liquor Sales Narrative} A centered 3-year moving average is to be constructed for the liquor sales.The result of this process will lead to a total of ____________________ moving averages.

The number of cases of liquor sold by a liquor wholesaler in an 8-year period follows.

{Liquor Sales Narrative} A centered 3-year moving average is to be constructed for the liquor sales.The result of this process will lead to a total of ____________________ moving averages.

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/226

Play

Full screen (f)

Deck 20: Time-Series Analytics and Forecasting

1

The time series component that reflects a wavelike pattern describing a long-term trend that is generally apparent over a number of years is called cyclical.

True

2

A trend is one of the four different components of a time series.It is a long-term,relatively smooth pattern or direction exhibited by a series,and its duration is more than one year.

True

3

The cyclical variation component of a time series measures the over-all general directional movement over a long period of time.

False

4

Random variation is one of the four different components of a time series.It is caused by irregular and unpredictable changes in a time series that are not caused by any other component.It tends to mask the existence of the other more predictable components.

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

5

In forecasting,we use data from the past in predicting the future value of the variable of interest.

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

6

The time series component that reflects a long-term,relatively smooth pattern or direction exhibited by a time series over a long time period is called seasonal.

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

7

We calculate the three-period moving average for a time series for all time periods except the first period.

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

8

Any variable that is measured over time in sequential order is called a time series.

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

9

In exponentially smoothed time series,the smoothing constant w is chosen on the basis of how much smoothing is required.In general,a small value of w such as 0.1 results in very little smoothing,while a large value of w such as 0.8 results in too much smoothing.

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

10

The equation: St = w⋅yt + (1 −w)⋅St− 1 (for t≥ 2)refers to exponentially smoothed time series.

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

11

Seasonal variation is one of the four different components of a time series.These are cycles that occur over short repetitive calendar periods and,by definition,have duration of less than one year.

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

12

The purpose of using the moving average is to take away the short-term seasonal and random variation,leaving behind a combined trend and cyclical movement.

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

13

One of the simplest ways to reduce random variation is to smooth the time series using moving averages and exponential smoothing.

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

14

Given a data set with 15 yearly observations,there are only thirteen 3-year moving averages.

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

15

The effect that business recessions and prosperity have on time series values is an example of the disaster component of a time series.

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

16

Smoothing time series data by the moving average method or exponential method is an attempt to dampen the effects of seasonal variation.

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

17

Given a data set with 15 yearly observations,there are only seven 9-year moving averages.

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

18

The term "seasonal variation" may refer to the four traditional seasons,or to systematic patterns that occur during a month,a week,or even one day.

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

19

The time series component that reflects the irregular changes in a time series that are not caused by any other component,and tends to hide the existence of the other more predictable components,is called random variation.

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

20

To calculate the five-period moving average for a time series,we average the value in that time period,the values in the two preceding time periods,and the values in the two following time periods.

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

21

Which of the four time series components is more likely to exhibit the relative steady growth of the population of Las Vegas from 1964 to 2004?

A)Long-term trend

B)Cyclical variation

C)Seasonal variation

D)Random variation

A)Long-term trend

B)Cyclical variation

C)Seasonal variation

D)Random variation

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

22

We compute the five-period moving averages for all time periods except the first two and last two time periods.

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

23

The time series component that reflects a long-term,relatively smooth pattern or direction exhibited by a time series over a long time period (more than one year)is called:

A)random variation

B)cyclical variation

C)seasonal variation

D)long-term trend

A)random variation

B)cyclical variation

C)seasonal variation

D)long-term trend

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

24

The time series component that reflects the irregular changes in a time series that are not caused by any other component,and tends to hide the existence of the other more predictable components,is called:

A)long-term trend

B)cyclical variation

C)seasonal variation

D)random variation

A)long-term trend

B)cyclical variation

C)seasonal variation

D)random variation

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

25

We compute the three-period moving averages for all time periods except the first and the last.

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

26

The principle of parsimony indicates that the simplest model that gets the job done adequately should be used.

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

27

The time series component that reflects a wavelike pattern describing a long-term trend that is generally apparent over a number of years is called:

A)long-term trend

B)cyclical variation

C)seasonal variation

D)random variation

A)long-term trend

B)cyclical variation

C)seasonal variation

D)random variation

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

28

Each forecast using the method of exponential smoothing depends on all the previous observations in the time series.

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

29

Smoothing time series data by the moving average method or exponential smoothing method is an attempt to remove the effect of the random variation component.

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

30

The term "seasonal variation" may refer to:

A)systematic patterns that occur during the period of one week

B)systematic patterns that occur over the course of one day

C)the four traditional seasons

D)All of these choices are true

A)systematic patterns that occur during the period of one week

B)systematic patterns that occur over the course of one day

C)the four traditional seasons

D)All of these choices are true

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

31

Given a data set with 15 yearly observations,a 3-year moving average will have fewer observations than a 5-year moving average.

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

32

A trend is a persistent pattern in annual time-series data that has to be followed for several years.

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

33

A time series is:

A)a set of measurements on a variable collected at the same time or approximately the same period of time.

B)a set of measurements on a variable taken over some time period in sequential order

C)a model that attempts to analyze the relationship between a dependent variable and one or more independent variables

D)a model that attempts to forecast the future value of a variable

A)a set of measurements on a variable collected at the same time or approximately the same period of time.

B)a set of measurements on a variable taken over some time period in sequential order

C)a model that attempts to analyze the relationship between a dependent variable and one or more independent variables

D)a model that attempts to forecast the future value of a variable

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

34

The time series component that reflects variability over short repetitive time periods and has duration of less than one year is called:

A)long-term trend

B)cyclical variation

C)seasonal variation

D)random variation

A)long-term trend

B)cyclical variation

C)seasonal variation

D)random variation

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

35

The seasonal variation,one of the four different components of a time series,is more likely to exhibit the relatively steady growth of the population of the United States from 181 million in 1960 to 273 million in 1999.

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

36

If a time series does not exhibit a long-term trend,the method of exponential smoothing may be used to obtain short-term predictions about the future.

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

37

A time series can consist of four different components: long-term trend,cyclical variation,seasonal variation,and random variation.

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

38

Cyclical variation,one of the four different components of a time series,is more likely to exhibit business cycles that record periods of economic recession and inflation.

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

39

Which of the four-time series component is more likely to exhibit the changes in stock market prices at particular times during the course of one day?

A)Long-term trend

B)Cyclical variation

C)Seasonal variation

D)Random variation

A)Long-term trend

B)Cyclical variation

C)Seasonal variation

D)Random variation

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

40

We calculate the three-period moving averages for a time series for all time periods except the:

A)first period

B)last period

C)first and last period

D)first and last two periods

A)first period

B)last period

C)first and last period

D)first and last two periods

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

41

If data for a time series analysis are collected on a monthly basis only,which component of the time series may be ignored?

A)Long-term trend

B)Cyclical variation

C)Seasonal variation

D)Random variation

A)Long-term trend

B)Cyclical variation

C)Seasonal variation

D)Random variation

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

42

We calculate the five-period moving average for a time series for all time periods except the:

A)first five periods

B)last five periods

C)first and last period

D)first two and last two periods

A)first five periods

B)last five periods

C)first and last period

D)first two and last two periods

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

43

In exponentially smoothed time series,the smoothing constant w is chosen on the basis of how much smoothing is required.In general,which of the following statements is true?

A)A small value of w such as w = 0.1 results in very little smoothing,while a large value such as w = 0.8 results in too much smoothing

B)A small value of w such as w = 0.1 results in too much smoothing,which a large value such as w = 0.8 results in very little smoothing

C)A small value of w such as w = 0.1 and a large value such as w = 0.8 may both result in very little smoothing

D)A small value of w such as w = 0.1 and a large value such as w = 0.8 may both result in too much smoothing

A)A small value of w such as w = 0.1 results in very little smoothing,while a large value such as w = 0.8 results in too much smoothing

B)A small value of w such as w = 0.1 results in too much smoothing,which a large value such as w = 0.8 results in very little smoothing

C)A small value of w such as w = 0.1 and a large value such as w = 0.8 may both result in very little smoothing

D)A small value of w such as w = 0.1 and a large value such as w = 0.8 may both result in too much smoothing

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

44

The number of four-period centered moving averages of a time series with 20 time periods is:

A)16

B)20

C)24

D)28

A)16

B)20

C)24

D)28

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

45

In measuring seasonal and random variation of a time series with no cyclical effect,we may use the:

A)ratio of the time series divided by the moving average

B)ratio of the time series divided by the predicted values

C)trend value

D)Both a and b

A)ratio of the time series divided by the moving average

B)ratio of the time series divided by the predicted values

C)trend value

D)Both a and b

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

46

The formula St = wyt + (1 −w)St−1 is used in time-series forecasting with exponential smoothing,where St is the exponentially smoothed time series at time t,yt is the value of the time series at time t,and w is the smoothing constant.The forecasted value at time t + 1 where w = .4 is given by:

A)Ft + 1 = 0.4yt +1 + 0.6St + 1

B)Ft + 1 = 0.4yt + 0.6St

C)Ft + 1 = 0.4yt + 0.6St− 1

D)Ft + 1 = 0.4yt− 1 + 0.6St

A)Ft + 1 = 0.4yt +1 + 0.6St + 1

B)Ft + 1 = 0.4yt + 0.6St

C)Ft + 1 = 0.4yt + 0.6St− 1

D)Ft + 1 = 0.4yt− 1 + 0.6St

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

47

The NYSE works 5-day work per week.If we want to measure the impact of the day of the week on NYSE performance we would need:

A)7 indicator variables

B)6 indicator variables

C)5 indicator variables

D)4 indicator variables

A)7 indicator variables

B)6 indicator variables

C)5 indicator variables

D)4 indicator variables

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

48

The way a seasonal index is computed involves which of the following steps?

A)Remove the effect of seasonal and random variation by regression analysis.

B)For each time period,compute the ratio, which removes most of the trend variation for that time period.

C)Calculate the average of all the ratios: over all time periods to remove random variation and leaving a measure of seasonality.

D)All of these choices are true.

A)Remove the effect of seasonal and random variation by regression analysis.

B)For each time period,compute the ratio,

which removes most of the trend variation for that time period.C)Calculate the average of all the ratios:

over all time periods to remove random variation and leaving a measure of seasonality.D)All of these choices are true.

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

49

Which of the following statements is false?

A)A moving average for a time period is the simple arithmetic average of the values in that time period and those close to it.

B)A value of the smoothing constant w close to 1 results in a very large smoothing,whereas a value of w close to zero results in very little smoothing.

C)The accuracy of the forecast with exponential smoothing decreases rapidly for predictions of the time series more than one period into the future.

D)A moving average "forgets" most of the previous time-series values and is considered a relatively crude method of removing the random variation.

A)A moving average for a time period is the simple arithmetic average of the values in that time period and those close to it.

B)A value of the smoothing constant w close to 1 results in a very large smoothing,whereas a value of w close to zero results in very little smoothing.

C)The accuracy of the forecast with exponential smoothing decreases rapidly for predictions of the time series more than one period into the future.

D)A moving average "forgets" most of the previous time-series values and is considered a relatively crude method of removing the random variation.

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

50

The trend line = 0.70 + 0.005t was calculated from quarterly data for 2000-2004,where t = 1 for the first quarter of 2000.The trend value for the second quarter of the year 2005 is:

A)0.705

B)0.820

C)0.815

D)0.810

= 0.70 + 0.005t was calculated from quarterly data for 2000-2004,where t = 1 for the first quarter of 2000.The trend value for the second quarter of the year 2005 is:A)0.705

B)0.820

C)0.815

D)0.810

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

51

Which of the following methods is appropriate for forecasting a time series when the trend,cyclical,and seasonal components of the series are not significant?

A)Moving averages

B)Exponential smoothing

C)Mean absolute deviation

D)Seasonal indexes

A)Moving averages

B)Exponential smoothing

C)Mean absolute deviation

D)Seasonal indexes

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

52

If we want to measure the seasonal variations on stock market performance by month,we would need:

A)50 indicator variables since the stock market has a 5-day work per week

B)12 indicator variables to represent the 12 months

C)11 indicator variables

D)52 indicator variables

A)50 indicator variables since the stock market has a 5-day work per week

B)12 indicator variables to represent the 12 months

C)11 indicator variables

D)52 indicator variables

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

53

The time-series model yt = Tt×Ct×St×Rt is used for forecasting,where Tt,Ct,St,and Rt are respectively the trend,cyclical,seasonal,and random variation components of the time series,and yt is the value of the time series at time t.The following estimates are obtained: = 120, = 1.02, = 0.95,and = 0.90.The model will produce a forecast of:

A)122.870

B)104.652

C)116.280

D)102.600

= 120, = 1.02, = 0.95,and = 0.90.The model will produce a forecast of:A)122.870

B)104.652

C)116.280

D)102.600

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

54

Which of the following is not true in regard to the weights used in exponential smoothing?

A)They are all positive

B)The last weight is always the smallest

C)They add up to 1

D)They decrease exponentially into the past

A)They are all positive

B)The last weight is always the smallest

C)They add up to 1

D)They decrease exponentially into the past

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

55

The linear trend = 115.8 + 2.5t was estimated using a time series with 25 time periods.The forecasted value for time period 26 is:

A)180.8

B)178.3

C)175.8

D)Not enough information given to answer this question.

= 115.8 + 2.5t was estimated using a time series with 25 time periods.The forecasted value for time period 26 is:A)180.8

B)178.3

C)175.8

D)Not enough information given to answer this question.

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

56

If we want to measure the seasonal variations on stock market performance by quarter,we would need:

A)4 indicator variables

B)3 indicator variables

C)2 indicator variables

D)1 indicator variable

A)4 indicator variables

B)3 indicator variables

C)2 indicator variables

D)1 indicator variable

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

57

In general,it is easy to identify the trend component of a time series by using:

A)exponential smoothing

B)moving averages

C)regression analysis

D)seasonally adjusted time series

A)exponential smoothing

B)moving averages

C)regression analysis

D)seasonally adjusted time series

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

58

The effect of an unpredictable,rare event will be contained in which component of the time series?

A)Long-term trend

B)Cyclical variation

C)Seasonal variation

D)Random Variation

A)Long-term trend

B)Cyclical variation

C)Seasonal variation

D)Random Variation

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

59

The following are the values of a time series for the first four time periods: Using a four-period moving average,the forecasted value for time period 5 is:

A)25.3

B)25.7

C)25.0

D)26.0

Using a four-period moving average,the forecasted value for time period 5 is:A)25.3

B)25.7

C)25.0

D)26.0

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

60

The model yt = Tt + Ct + St + Rt + εt that assumes the time series value at time t is the sum of the four time series components Tt,Ct,St,and Rt is referred to as:

A)additive model

B)multiplicative model

C)moving averages model

D)forecast model

A)additive model

B)multiplicative model

C)moving averages model

D)forecast model

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

61

The following are the values of a time series for the first four time periods: Using exponential smoothing,with w = 0.30,the forecasted value for time period 5 is:

A)24.920

B)24.644

C)23.600

D)23.000

Using exponential smoothing,with w = 0.30,the forecasted value for time period 5 is:A)24.920

B)24.644

C)23.600

D)23.000

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

62

The high level of airline ticket sales that travel agencies experience during summer is an example of what component of a time series?

A)Long-term trend

B)Cyclical variation

C)Seasonal variation

D)Random variation

A)Long-term trend

B)Cyclical variation

C)Seasonal variation

D)Random variation

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

63

For which of the following values of the smoothing constant w will the smoothed series catch up most quickly whenever the original time series changes direction?

A)0.90

B)0.50

C)0.40

D)0.10

A)0.90

B)0.50

C)0.40

D)0.10

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

64

Suppose that we calculate the four-period moving average of the following time series The centered moving average for period 3 is:

A)22.5

B)21.25

C)20.50

D)18.5

The centered moving average for period 3 is:A)22.5

B)21.25

C)20.50

D)18.5

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

65

The fairly regular fluctuations that occur within each year would be contained in which component of the time series?

A)Long-term trend

B)Cyclical variation

C)Seasonal variation

D)Random variation

A)Long-term trend

B)Cyclical variation

C)Seasonal variation

D)Random variation

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

66

Which of the following smoothing constants causes the most rapid reaction to a change in the current time series value?

A)0.40

B)0.30

C)0.20

D)0.10

A)0.40

B)0.30

C)0.20

D)0.10

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

67

Based on the following scatter plot,which of the time-series components is not present in this quarterly time series?

A)Long-term trend

B)Cyclical variation

C)Seasonal variation

D)Random variation

A)Long-term trend

B)Cyclical variation

C)Seasonal variation

D)Random variation

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

68

After estimating a trend model for annual time-series data,you obtain the following residual plot against time. The problem with your model is that:

A)the cyclical component has not been accounted for

B)the seasonal component has not been accounted for

C)the trend component has not been accounted for

D)the irregular component has not been accounted for

The problem with your model is that:A)the cyclical component has not been accounted for

B)the seasonal component has not been accounted for

C)the trend component has not been accounted for

D)the irregular component has not been accounted for

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

69

The method of moving averages is used to:

A)take away short term seasonal variation

B)reduce random variation

C)leave the combined trend and cyclical movement

D)All of these choices are true.

A)take away short term seasonal variation

B)reduce random variation

C)leave the combined trend and cyclical movement

D)All of these choices are true.

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

70

Smoothing time series data by the moving average method or exponential smoothing method is an attempt to remove the effect of the:

A)trend component

B)cyclical component

C)seasonal component

D)random variation component

A)trend component

B)cyclical component

C)seasonal component

D)random variation component

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

71

Which of the following is not an advantage of exponential smoothing?

A)It enables us to perform on-period ahead forecasting

B)It enables us to perform more than one-period ahead forecasting

C)It enables us to smooth out seasonal components

D)It enables us to smooth out cyclical components

A)It enables us to perform on-period ahead forecasting

B)It enables us to perform more than one-period ahead forecasting

C)It enables us to smooth out seasonal components

D)It enables us to smooth out cyclical components

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

72

After estimating a trend model for annual time-series data,you obtain the following residual plot against time. The problem with your model is that:

A)the cyclical component has not been accounted for

B)the seasonal component has not been accounted for

C)the trend component has not been accounted for

D)the irregular component has not been accounted for

The problem with your model is that:A)the cyclical component has not been accounted for

B)the seasonal component has not been accounted for

C)the trend component has not been accounted for

D)the irregular component has not been accounted for

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

73

Which of the following statements about the method of exponential smoothing is not true?

A)It gives greater weight to more recent data

B)It can be used for forecasting

C)It uses all earlier observations in each smoothing calculation

D)It gives greater weight to the earlier observations in the series

A)It gives greater weight to more recent data

B)It can be used for forecasting

C)It uses all earlier observations in each smoothing calculation

D)It gives greater weight to the earlier observations in the series

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

74

The cyclical component of a time series

A)represents periodic fluctuations which reoccur within one year

B)represents periodic fluctuations which usually occur in two or more years

C)is obtained by adding up the seasonal indexes

D)is obtained by adjusting for calendar variation

A)represents periodic fluctuations which reoccur within one year

B)represents periodic fluctuations which usually occur in two or more years

C)is obtained by adding up the seasonal indexes

D)is obtained by adjusting for calendar variation

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

75

Which of the following statements about moving averages is not true?

A)It can be used to smooth a series

B)It gives equal weight to all values in the computation

C)It is simpler than the method of exponential smoothing

D)It gives greater weight to more recent data

A)It can be used to smooth a series

B)It gives equal weight to all values in the computation

C)It is simpler than the method of exponential smoothing

D)It gives greater weight to more recent data

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

76

The overall upward or downward pattern of the data in an annual time series will be contained in which component of the time series?

A)Long-term trend

B)Cyclical variation

C)Seasonal variation

D)Random variation

A)Long-term trend

B)Cyclical variation

C)Seasonal variation

D)Random variation

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

77

Which of the following terms describes the up and down movements of a time series that vary both in length and intensity?

A)Long-term trend component

B)Cyclical variation component

C)Random variation component

D)Seasonal variation component

A)Long-term trend component

B)Cyclical variation component

C)Random variation component

D)Seasonal variation component

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

78

Liquor Sales

The number of cases of liquor sold by a liquor wholesaler in an 8-year period follows.

{Liquor Sales Narrative} A centered 3-year moving average is to be constructed for the liquor sales.The result of this process will lead to a total of ____________________ moving averages.

The number of cases of liquor sold by a liquor wholesaler in an 8-year period follows.

{Liquor Sales Narrative} A centered 3-year moving average is to be constructed for the liquor sales.The result of this process will lead to a total of ____________________ moving averages.

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

79

The model yt = Tt×Ct×St×Rt that assumes the time series value at time t is the product of the four time series components is referred to as:

A)additive model

B)forecast model

C)moving averages model

D)multiplicative model

A)additive model

B)forecast model

C)moving averages model

D)multiplicative model

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

80

Which of the following terms describes the overall long-term tendency of a time series?

A)Long-term trend component

B)Cyclical variation component

C)Random variation component

D)Seasonal variation component

A)Long-term trend component

B)Cyclical variation component

C)Random variation component

D)Seasonal variation component

Unlock Deck

Unlock for access to all 226 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 226 flashcards in this deck.