Deck 7: Applications of Simple Interest

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Calculate missing value for the promissory note:

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Calculate missing value for the promissory note:

Question

Question

Calculate missing value for the promissory note:

Question

Calculate missing value for the promissory note:

Question

Question

Question

Question

Question

Question

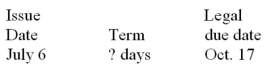

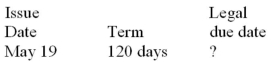

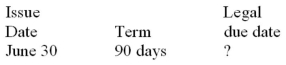

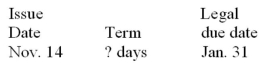

Calculate missing value for the promissory note:

Question

Calculate missing value for the promissory note:

Question

Question

Calculate missing value for the promissory note:

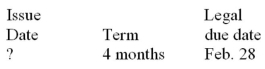

Question

Calculate missing value for the promissory note:

Question

Calculate missing value for the promissory note:

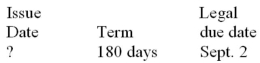

Question

Calculate missing value for the promissory note:

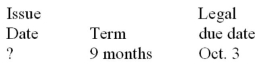

Question

Calculate missing value for the promissory note:

Question

Calculate missing value for the promissory note:

Question

Calculate missing value for the promissory note:

Question

Calculate missing value for the promissory note:

Question

Calculate missing value for the promissory note:

Question

Question

Calculate missing value for the promissory note:

Question

Calculate missing value for the promissory note:

Question

Question

Calculate missing value for the promissory note:

Question

Calculate missing value for the promissory note:

Question

Calculate missing value for the promissory note:

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/168

Play

Full screen (f)

Deck 7: Applications of Simple Interest

1

Certificate A pays $1,000 in 4 months and another $1,000 in 8 months. Certificate B pays $1,000 in 5 months and another $1,000 in 9 months. If the current rate of return required on this type of investment certificate is 5.75%, determine the current value of each of the certificates. Give an explanation for the lower value of

A = $1,944.28 and B = $1,935.26. Since the payments from B are received a month after the respective payments from A, certificate B is not as valuable as certificate A.

2

An Investment Savings account offered by a trust company pays a rate of 0.25% on the first $1,000 of daily closing balance, 0.5% on the portion of the balance between $1,000 and $3,000, and 0.75% on any balance in excess of $3,000. What interest will be paid for the month of April if the opening balance was $2,439, $950 was deposited on April 10, and $500 was withdrawn on April 23?

$1.05

3

a) What will be the maturity value of $15,000 placed in a 120-day term deposit paying an interest rate of1.25%?

b) If on the maturity date the combined principal and interest are "rolled over" into a 90-day term deposit paying1.15%, what amount will the depositor receive when the second term deposit matures?

b) If on the maturity date the combined principal and interest are "rolled over" into a 90-day term deposit paying1.15%, what amount will the depositor receive when the second term deposit matures?

a) $15,061.64; b) $15,104.35

4

An assignable loan contract executed 3 months ago requires two payments of $3,200 plus interest at 9% from the date of the contract, to be paid 4 and 8 months after the contract date. The payee is offering to sell the contract to a finance company in order to raise urgently needed cash. If the finance company requires a 16% rate of return, what price will it be prepared to pay today for the contract?

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

5

If you purchase an investment privately, how do you determine the maximum price you are prepared to pay?

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

6

For principal amounts of $5,000 to $49,999, a bank pays an interest rate of 0.95% on 180- to 269-day non-redeemable GICs, and 1.00% on 270- to 364-day non-redeemable GICs. Ranjit has $10,000 to invest for 364 days. Because he thinks interest rates will be higher six months from now, he is debating whether to choose a 182-day GIC now (and reinvest its maturity value in another 182-day GIC) or to choose a 364-day GIC today. What would the interest rate on 182-day GICs have to be on the reinvestment date for both alternatives to yield the same maturity value 364 days from now?

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

7

On a $10,000 principal investment, a bank offered interest rates of 1.45% on 270- to 364-day GIC's and 1.15% on 180- to 269-day GICs. How much more will an investor earn from a 364-day GIC than from two consecutive 182-day GICs? (Assume that the interest rate on 180- to 269-day GICs will be the same on the renewal date as it is today. Remember that both the principal and the interest from the first 182-day GIC can be invested in the second 182-day GIC.)

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

8

For amounts between $10,000 and $24,999, a credit union pays a rate of 1.25% on term deposits with maturities in the 91 to 120-day range. However, early redemption will result in a rate of 0.55% being applied. How much more interest will a 91-day $20,000 term deposit earn if it is held until maturity than if it is redeemed after 80 days?

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

9

An investment promises two payments of $500 on dates 3 and 6 months from today. If the required return on investment is 9%:

a) What is the value of the investment today?

b) What will its value be in 1 month if the required rate of return remains at 9%?

c) Give an explanation for the change in value as time passes.

a) What is the value of the investment today?

b) What will its value be in 1 month if the required rate of return remains at 9%?

c) Give an explanation for the change in value as time passes.

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

10

Suppose that the current rates on 60 and 120-day GICs are 1.50% and 1.75%, respectively. An investor is weighing the alternatives of purchasing a 120-day GIC versus purchasing a 60-day GIC and then reinvesting its maturity value in a second 60-day GIC. What would the interest rate on 60-day GICs have to be 60 days from now for the investor to end up in the same financial position with either alternative?

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

11

An agreement stipulates payments of $4,500, $3,000, and $5,500 in 4, 8, and 12 months, respectively, from today. What is the highest price an investor will offer today to purchase the agreement if he requires a minimum rate of return of 5.5%?

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

12

Joan has savings of $12,000 on June 1. Since she may need some of the savings during the next 3 months, she is considering two options at her bank. (1) An Investment Builder savings account earns a 0.25% rate of interest. The interest is calculated on the daily closing balance and paid on the first day of the following month. (2) A 90- to 179-day cashable term deposit earns a rate of 0.8%, paid at maturity. If interest rates do not change and Joan does not withdraw any of the funds, how much more will she earn from the term deposit up to September 1? (Keep in mind that savings account interest paid on the first day of the month will itself subsequently earn interest during the subsequent month.)

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

13

Paul has $20,000 to invest for 6 months. For this amount, his bank pays 1.3% on a 90-day GIC and 1.5% on a 180-day GIC. If the interest rate on a 90-day GIC is the same 3 months from now, how much more interest will Paul earn by purchasing the 180-day GIC than by buying a 90-day GIC and then reinvesting its maturity value in a second 90-day GIC?

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

14

An agreement stipulates payments of $4,000, $2,500, and $5,000 in 3, 6, and 9 months, respectively, from today. What is the highest price an investor will offer today to purchase the agreement if he requires a minimum rate of return of 6.25%?

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

15

A savings account pays interest of 1.5%. Interest is calculated on the daily closing balance and paid at the close of business on the last day of the month. A depositor had a $2,239 opening balance on September 1, deposited $734 on September 7 and $627 on September 21, and withdrew $300 on both September 10 and September 21. What interest will be credited to the account at the month's end?

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

16

An Investment Savings account offered by a trust company pays a rate of 1.00% on the first $1,000 of daily closing balance, 1.75% on the portion of the balance between $1,000 and $3,000, and 2.25% on any balance in excess of $3,000. What interest will be paid for the month of January if the opening balance was $3678, $2800 was withdrawn on the 14th of the month, and $950 was deposited on the 25th of the month?

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

17

A contract requires payments of $1,500, $2,000, and $1,000 in 100, 150, and 200 days, respectively, from today. What is the value of the contract today if the payments are discounted to yield a 3.5% rate of return?

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

18

What do you need to know to be able to calculate the fair market value of an investment that will deliver two future payments?

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

19

An investment promises two payments of $1,000, on dates 60 and 90 days from today. What price will an investor pay today if her required return is 3%?

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

20

Assume that the expected cash flows from an investment and the market-determined rate of return do not change as time passes.

a) What will happen to the investment's fair market value leading up to the first scheduled payment? Explain.

b) If the first scheduled payment is $500, what will happen to the fair market value of the investment just after the payment is made? Explain.

a) What will happen to the investment's fair market value leading up to the first scheduled payment? Explain.

b) If the first scheduled payment is $500, what will happen to the fair market value of the investment just after the payment is made? Explain.

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

21

A $100,000, 90-day commercial paper certificate issued by Bell Canada Enterprises was sold on its issue date for $98,950. What annual rate of return (to the nearest 0.001%) will it yield to the buyer?

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

22

A $100,000, 168-day Government of Canada Treasury bill was purchased on its date of issue to yield 2.1%.

a) What price did the investor pay?

b) Calculate the market value of the T-bill 85 days later if the rate of return then required by the market has:

(i) risen to 2.4%. (ii) remained at 2.1%. (iii) fallen to 1.8%.

c) Calculate the rate of return actually realized by the investor if the T-bill is sold at each of the three prices calculated in part (b).

a) What price did the investor pay?

b) Calculate the market value of the T-bill 85 days later if the rate of return then required by the market has:

(i) risen to 2.4%. (ii) remained at 2.1%. (iii) fallen to 1.8%.

c) Calculate the rate of return actually realized by the investor if the T-bill is sold at each of the three prices calculated in part (b).

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

23

A 168-day, $100,000 T-bill was initially issued at a price that would yield the buyer 4.19%. If the yield required by the market remains at 4.19%, how many days before its maturity date will the T-bill's market price first exceed $99,000?

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

24

Over the past 35 years, the prevailing market yield or discount rate on 90-day T-bills has ranged from a low of 0.17% in February 2010 to a high of 20.82% in August of 1981. (The period from 1979 to 1990 was a time of historically high inflation rates and interest rates.) How much more would you have paid for a $100,000 face value 90-day T-bill at the February 2010 discount rate than at the August 1981 discount rate?

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

25

Claude Scales, a commercial fisherman, bought a new navigation system for $10,000 from Coast Marine Electronics on March 20. He paid $2,000 in cash and signed a conditional sales contract requiring a payment on July 1 of $3,000 plus interest on the $3,000 at a rate of 8%, and another payment on September 1 of $5,000 plus interest at 8% from the date of the sale. The vendor immediately sold the contract to a finance company, which discounted the payments at its required return of 12%. What proceeds did Coast Marine receive from the sale of the contract?

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

26

A conditional sale contract requires two payments 3 and 6 months after the date of the contract. Each payment consists of $1,900 principal plus interest at 10.5% on $1,900 from the date of the contract. One month into the contract, what price would a finance company pay for the contract if it requires an 16% rate of return on its purchases?

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

27

If short-term interest rates do not change, what happens to a T-bill's fair market value as time passes?

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

28

George borrowed $4,000 on demand from CIBC on January 28 for an RRSP contribution. Because he used the loan proceeds to purchase CIBC's mutual funds for his RRSP, the interest rate on the loan was set at the bank's prime rate. George agreed to make monthly payments of $600 (except for a smaller final payment) on the twenty-first of each month, beginning February 21. The prime rate was initially 3.75%, dropped to 3.5% effective May 15, and decreased another 0.25% on July 5. It was not a leap year. Construct a repayment schedule showing the amount of each payment and the allocation of each payment to interest and principal.

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

29

A $100,000, 91-day Province of Ontario Treasury bill was issued 37 days ago. What will it sell at today in order to yield the purchaser 3.14%?

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

30

A $100,000, 90-day commercial paper certificate issued by Wells Fargo Financial Canada was sold on its issue date for $99,250. What rate of return will it yield to the buyer?

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

31

Mayfair Fashions has a $90,000 line of credit from the Bank of Montreal. Interest at prime plus 2% is deducted from Mayfair's chequing account on the 24th of each month. Mayfair initially drew down $40,000 on March 8 and another $15,000 on April 2. On June 5, $25,000 of principal was repaid. If the prime rate was 3.25% on March 8 and rose by 0.25% effective May 13, what were the first four interest deductions charged to the store's account?

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

32

Calculate and compare the market values of a $100,000 face value Government of Canada Treasury bill on dates that are 91 days, 61 days, 31 days, and one day before maturity. Assume that the rate of return required in the market stays constant at 3% over the lifetime of the T-bill.

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

33

An assignable loan contract executed three months ago requires two payments to be paid five and ten months after the contract date. Each payment consists of a principal portion of $1,800 plus interest at 5% on $1,800 from the date of the contract. The payee is offering to sell the contract to a finance company in order to raise cash. If the finance company requires a return of 10%, what price will it be prepared to pay today for the contract?

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

34

Is the price of a 98-day $100,000 T-bill higher or lower than the price of a 168-day $100,000 T-bill? Why?

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

35

A $25,000, 91-day Province of Newfoundland Treasury bill was originally purchased at a price that would yield the investor a 5.438% rate of return if the T-bill is held until maturity. Thirty-four days later, the investor sold the T-bill through his broker for $24,775.

a) What price did the original investor pay for the T-bill?

b) What rate of return will the second investor realize if she holds the T-bill until maturity?

c) What rate of return did the first investor realize during his holding period?

a) What price did the original investor pay for the T-bill?

b) What rate of return will the second investor realize if she holds the T-bill until maturity?

c) What rate of return did the first investor realize during his holding period?

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

36

Calculate the price of a $25,000, 91-day Province of British Columbia Treasury bill on its issue date if the current market rate of return is 3.672%.

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

37

An investor purchased a 182-day, $25,000 Province of Alberta Treasury bill on its date of issue for $24,610 and sold it 60 days later for $24,750.

a) What rate of return was implied in the original price?

b) What rate of return did the market require on the sale date?

c) What rate of return did the original investor actually realize during the 60-day holding period?

a) What rate of return was implied in the original price?

b) What rate of return did the market require on the sale date?

c) What rate of return did the original investor actually realize during the 60-day holding period?

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

38

Calculate the price on its issue date of $100,000 face value, 90-day commercial paper issued by G E Capital Canada if the prevailing market rate of return is 0.932%.

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

39

A $100,000, 182-day Province of New Brunswick Treasury bill was issued 66 days ago. What will it sell at today to yield the purchaser 2.48%?

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

40

A money market mutual fund purchased $1 million face value of Honda Canada Finance Inc. 90-day commercial paper 28 days after its issue. What price was paid if the paper was discounted at 2.10%?

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

41

Calculate missing value for the promissory note:

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

42

On the June 12 interest payment date, the outstanding balance on Delta Nurseries' revolving loan was $65,000. The floating interest rate on the loan stood at 6.25% on June 12, but rose to 6.5% on July 3, and to 7% on July 29. An additional $10,000 was drawn on June 30. What were the interest charges to Delta's bank account on July 12 and August 12?

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

43

Ruxandra's Canada Student Loans totalled $7200 by the time she finished Conestoga College in April. The accrued interest at prime plus 2.5% for the grace period was converted to principal on October 31. She chose the floating interest rate option and began monthly payments of $120 on November 30. The prime rate of interest was 3.5% on May 1, 3.25% effective July 9, and 4% effective December 13. Prepare a repayment schedule presenting details of the first three payments.

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

44

A $5,000 demand loan was advanced on June 3. Fixed monthly payments of $1,000 were required on the first day of each month beginning July 1. Prepare the full repayment schedule for the loan. Assume that the interest rate remained at 8.75% for the life of the loan.

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

45

Giovando, Lindstrom & Co. obtained a $6,000 demand loan at prime plus 1.5% on April 1 to purchase new office furniture. The company agreed to fixed monthly payments of $1,000 on the first of each month, beginning May 1. Calculate the total interest charges over the life of the loan if the prime rate started at 3.75% on April 1, decreased to 3.5% effective June 7, and returned to 3.75% on August 27. Present a repayment schedule in support of your answer.

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

46

Keesha borrowed $7000 from her credit union on a demand loan on July 20 to purchase a motorcycle. The terms of the loan require fixed monthly payments of $1400 on the first day of each month, beginning September 1. The floating rate on the loan started at 8.75%, but rose to 9.25% on August 19, and to 9.5% effective November 2. Prepare a loan repayment schedule presenting the amount of each payment and the allocation of each payment to interest and principal.

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

47

Monica finished her program at New Brunswick Community College on June 3 with Canada Student Loans totalling $6,800. She decided to capitalize the interest that accrued (at prime plus 2.5%) during the grace period. In addition to regular end-of-month payments of $200, she made an extra $500 lump payment on March 25 that was applied entirely to principal. The prime rate dropped from 5% to 4.75% effective September 22, and declined another 0.5% effective March 2. Calculate the balance owed on the floating rate option after the regular March 31 payment. The relevant February had 28 days.

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

48

Dr. Chan obtained a $15,000 demand loan at prime plus 1.5% on September 13 from the Bank of Montreal to purchase a new dental X-ray machine. Fixed payments of $700 will be deducted from the dentist's chequing account on the 20th of each month, beginning October 20. The prime rate was 7.5% at the outset, dropped to 7.25% on the subsequent November 26, and rose to 7.75% on January 29. Prepare a loan repayment schedule showing the details of the first five payments.

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

49

McKenzie Wood Products negotiated a $200,000 revolving line of credit with the Bank of Montreal at prime plus 2%. On the 20th of each month, interest is calculated (up to but not including the 20th) and deducted from the company's chequing account. If the initial loan advance of $25,000 on July 3 was followed by a further advance of $30,000 on July 29, how much interest was charged on July 20 and August 20? The prime rate was at 3% on July 3 and fell to 2.75% on August 5.

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

50

Duncan Developments Ltd. obtained a $120,000 line of credit from its bank to subdivide a parcel of land it owned into four residential lots and to install water, sewer, and underground electrical services. Amounts advanced from time to time are payable on demand to its bank. Interest at prime plus 4% on the daily principal balance is charged to the developer's bank account on the 26th of each month. The developer must apply at least $30,000 from the proceeds of the sale of each lot against the loan principal. Duncan drew down $50,000 on June 3, $40,000 on June 30, and $25,000 on July 17. Two lots quickly sold, and Duncan repaid $30,000 on July 31 and $35,000 on August 18. The initial prime rate of 5% changed to 5.25% effective July 5 and 5.5% effective July 26. Prepare a repayment schedule showing loan activity and interest charges up to and including the interest payment on August 26.

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

51

Kari had Canada Student Loans totalling $3,800 when she completed her program at Niagara College in December. She had enough savings at the end of June to pay the interest that had accrued during the 6-month grace period. Kari made arrangements with her credit union to start end-of-month payments of $60 in July. She chose the fixed interest rate option (at prime plus 5%) when the prime rate was at 5.5%. Prepare a loan repayment schedule up to and including the September 30 payment.

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

52

Calculate missing value for the promissory note:

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

53

Harjap completed his program at Nova Scotia Community College in December. On June 30, he paid all the interest that had accrued (at prime plus 2.5%) on his $5,800 Canada Student Loan during the 6-month grace period. He selected the fixed rate option (prime plus 5%) and agreed to make end-of-month payments of $95 beginning July 31. The prime rate began the grace period at 4% and rose by 0.5% effective March 29. On August 13, the prime rate rose another 0.5%. The relevant February had 28 days.

a) What amount of interest accrued during the grace period?

b) Calculate the total interest paid in the first three regular payments, and the balance owed after the third payment.

a) What amount of interest accrued during the grace period?

b) Calculate the total interest paid in the first three regular payments, and the balance owed after the third payment.

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

54

Calculate missing value for the promissory note:

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

55

Calculate missing value for the promissory note:

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

56

Mr. Michaluk has a $50,000 personal (revolving) line of credit with the Canadian Imperial Bank of Commerce (CIBC). The loan is on a demand basis at a floating rate of prime plus 1.5%. On the fifteenth of each month, a payment equal to the greater of $100 or 3% of the combined principal and accrued interest is deducted from his chequing account. The principal balance after a payment on September 15 stood at $23,465.72. Prepare the loan repayment schedule from September 15 up to and including the payment on January 15. Assume that he makes the minimum payments and the prime rate remains at 5.25%.

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

57

Ms. Wadeson obtained a $15,000 demand loan from the Canadian Imperial Bank of Commerce on May 23 to purchase a car. The interest rate on the loan was prime plus 2%. The loan required payments of $700 on the 15th of each month, beginning June 15. The prime rate was 4.5% at the outset, dropped to 4.25% on July 26, and then jumped by 0.5% on September 14. Prepare a loan repayment schedule showing the details of the first five payments.

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

58

Sarah's Canada Student Loans totalled $9,400 by the time she graduated from Red River College in May. She arranged to capitalize the interest on November 30 and to begin monthly payments of $135 on December 31. Sarah elected the floating rate interest option (prime plus 2.5%). The prime rate stood at 3.75% on June 1, dropped to 3.5% effective September 3, and then increased by 0.25% on January 17. Prepare a repayment schedule presenting details of the first three payments. February has 28 days.

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

59

Seth had accumulated Canada Student Loans totalling $5,200 by the time he graduated from Mount Royal College in May. He arranged with the Bank of Nova Scotia to select the floating-rate option (at prime plus 2½%) and to begin monthly payments of $110 on December 31. Prepare a loan repayment schedule up to and including the February 28 payment. The prime rate was initially at 3.25%. It dropped by 0.25% effective January 31. Seth made an additional principal payment of $300 on February 14.

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

60

Dr. Robillard obtained a $75,000 operating line of credit at prime plus 1%. Accrued interest up to but not including the last day of the month is deducted from his bank account on the last day of each month. On February 5 (of a non-leap year) he received the first draw of $15,000. He made a payment of $10,000 toward principal on March 15, but took another draw of $7,000 on May 1. Prepare a loan repayment schedule showing the amount of interest charged to his bank account on the last days of February, March, April, and May. Assume that the prime rate remained at 3.5% through to the end of May.

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

61

Calculate missing value for the promissory note:

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

62

Calculate missing value for the promissory note:

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

63

Determine the legal due date for:

a) A 5-month note dated September 29, 2014.

b) A 150-day note issued September 29, 2014.

a) A 5-month note dated September 29, 2014.

b) A 150-day note issued September 29, 2014.

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

64

Calculate missing value for the promissory note:

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

65

Calculate missing value for the promissory note:

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

66

Calculate missing value for the promissory note:

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

67

Calculate missing value for the promissory note:

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

68

Calculate missing value for the promissory note:

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

69

Calculate missing value for the promissory note:

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

70

Calculate missing value for the promissory note:

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

71

Calculate missing value for the promissory note:

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

72

Calculate missing value for the promissory note:

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

73

Determine the legal due date for:

a) A 4-month note dated April 30, 2015.

b) A 120-day note issued April 30, 2015.

a) A 4-month note dated April 30, 2015.

b) A 120-day note issued April 30, 2015.

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

74

Calculate missing value for the promissory note:

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

75

Calculate missing value for the promissory note:

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

76

Calculate the maturity value of a $1,000 face value, 5-month note dated December 31, 2014, and bearing interest at 9.5%.

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

77

Calculate missing value for the promissory note:

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

78

Calculate missing value for the promissory note:

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

79

Calculate missing value for the promissory note:

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

80

Calculate the maturity value of a 120-day, $1,000 face value note dated November 30, 2014, and earning interest at 4.75%.

Unlock Deck

Unlock for access to all 168 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 168 flashcards in this deck.